Macro & Market Views

The Small Idea: It Don't Come Easy

The Small Idea: It Don't Come Easy

When poring over a company’s financials the other day to ascertain whether its depressed valuation reflected transitory weakness or evidence of deep-seated decay, the sage wisdom of that well-known investment guru Ringo Starr came rushing back into my head: “You know, it don’t come easy.” Though often derided as the least essential Beatle, Ringo could be counted on for more than just a steady backbeat.

This edition of The Small Idea was written by Bill Hench, head of the Small Cap team and portfolio manager.

Markets tend to demonstrate patterns, and investors try to identify and exploit such patterns for profit. Weakness in the price of a small cap stock—typically exacerbated by the market’s relatively limited liquidity—often reflects a collective overreaction to some disappointment. Once the source of disappointment is addressed, emotion subsides and the shares may rally to normalized levels. Of course, it’s never easy to buy into a stock you believe is undervalued when its price suggests the market at large disagrees. Only in retrospect—after idiosyncratic concerns have been ameliorated and perceptions have shifted—does buying cheap appear to have been the obvious move. And here’s the punchline, which makes me alternately chuckle and grimace: The investment gains that serve as proof of concept often deter future commitments to buying into uncertainty, as many investors reason that the ”easy money” already has been made.

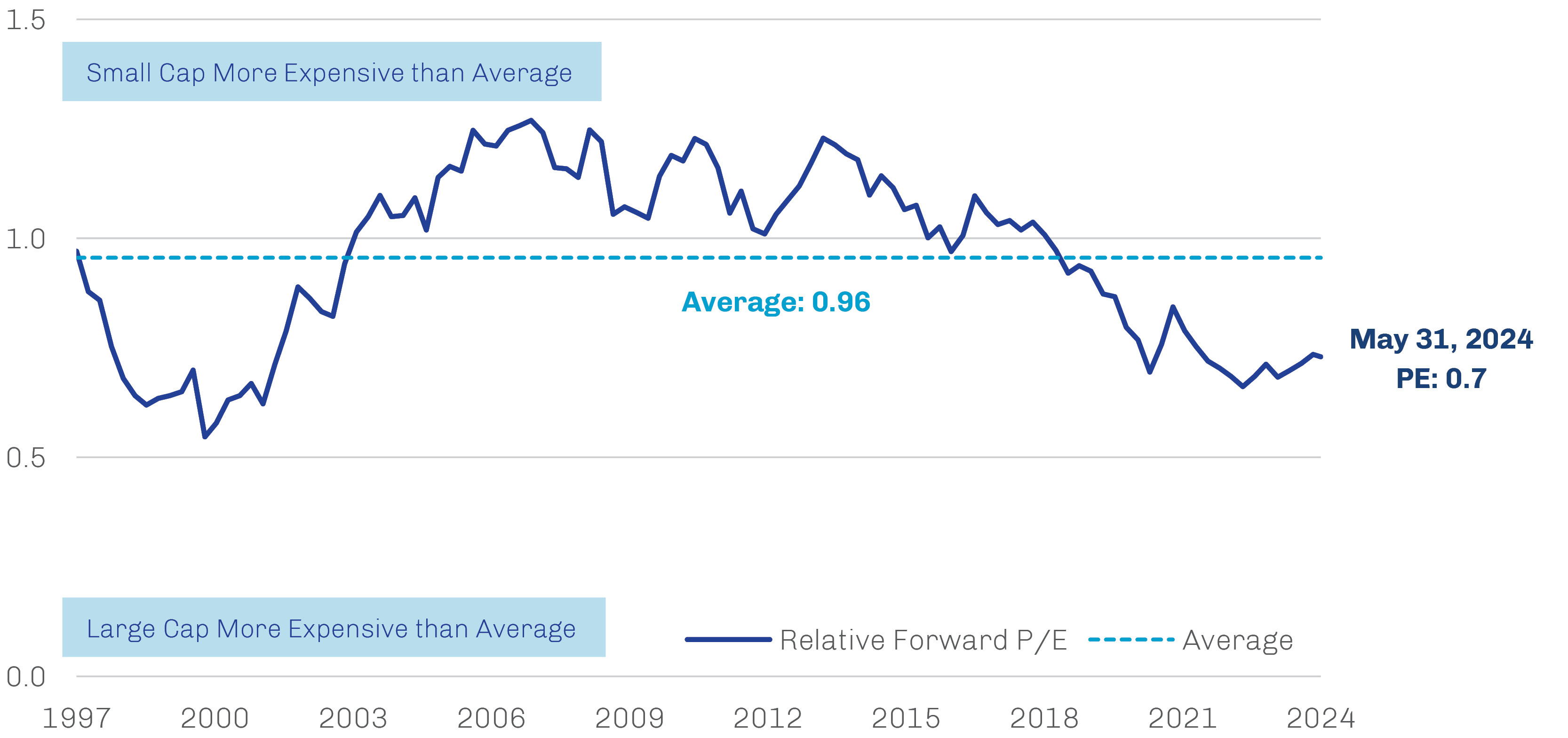

Thus, small cap stocks can get stuck in a loop of diminished expectations. To wit, the last decade has seen small cap indexes underperform large cap indexes pretty consistently despite an almost century-long track record of delivering higher returns over full investment cycles.1 Many clients have asked what it may take for small caps to return to their historical form. Looking at the documented interplay of the small and large cap equity markets, we believe there are valid reasons to think that some sort of mean reversion is likely. As shown in Exhibit 1, small caps traded at a premium to large caps for most of the period between 2003 and 2017, and the current valuation discount approaches levels not experienced since the early 2000s. Moreover, small cap companies historically have led markets in up periods and when inflation has run above the long-term average.2

Exhibit 1. Relative Valuations Favor the Small Cap Universe

Relative Forward 12-Month Price/Earnings Ratio, Russell 2000 Index versus Russell 1000 Index

Source: FactSet; data as of May 31, 2024.

Chart is for illustrative purposes only.

And let’s not forget that we live in a world of quickly shifting macro, market and industry dynamics, any number of which could also potentially trigger a resurgence in small caps. A few come to mind:

Fiscal/Monetary Policy

- Inflation continues to abate, and the Federal Reserve cuts its policy rate. Smaller companies, in particular, may find a tailwind in the lower cost of capital.

- A Washington budget deal reduces growth in federal spending, easing longer-term secular pressure on inflation and interest rates.

Politics/Government

- The 2024 elections result in Republican control of the White House and both branches of Congress. New, more laissez-faire leadership at government agencies like the Federal Trade Commission, Environmental Protection Agency and Department of Justice dramatically changes the environment for mergers and acquisitions activity and capital investment. Strategic buying of smaller companies by well-financed larger businesses surges.

Market Leadership/Secular Trends

- Reflecting the outsized contribution to performance of certain, typically tech-related names, investors begin to question the value proposition of index portfolios that seek merely to replicate market-level returns. Instead, they are motivated to embrace investment selectivity and the alpha generation that may accompany it, tempered by the flexibility and responsiveness of active managers.

Industry Developments

- Smaller manufacturers are buoyed as reshoring continues to gain momentum.

- Breakthrough discoveries in biotech lead to major improvements in cancer treatment and cardiovascular therapies, prompting a rally in the oft-maligned “non-earning” small cap biotech sector.

- Artificial intelligence applications prove more beneficial than even their proponents had imagined, and skeptical investors are forced to reevaluate the opportunity cost of their lack of exposure. A wave of initial public offerings by small AI-related companies hits the market at a rate that surpasses the birth of the internet.

- Continued market share gains by private capital providers squeeze out the weakest local banks, forcing mergers and/or closures. A new breed of semi-regional banks—centered in the South and lower-tax states—emerges with higher profitability and faster growth, creating an opportunity in a small cap banking sector long home to fundamentally challenged businesses.

Back to the Grind

Conjecture can be fun. But rather than basing investment decisions on guesswork, adhering to disciplined processes, focused on fundamental research and valuation, may best position diversified portfolios to be paid for taking the risks inherent to the small cap market. Key to this effort is concentrating on factors that can be controlled; namely, which stocks to buy and how much to pay for them.

While we would love to see a roaring small cap bull market, we’re ultimately riding with Ringo: “got to pay your dues if you wanna sing the blues.” Thus are our heads down even as our hearts sometimes leap into our mouths. In the final analysis, however, the ongoing underperformance of smaller stocks may represent an opportunity to find attractively valued companies we believe have the potential to benefit from catalysts for future earnings recovery.