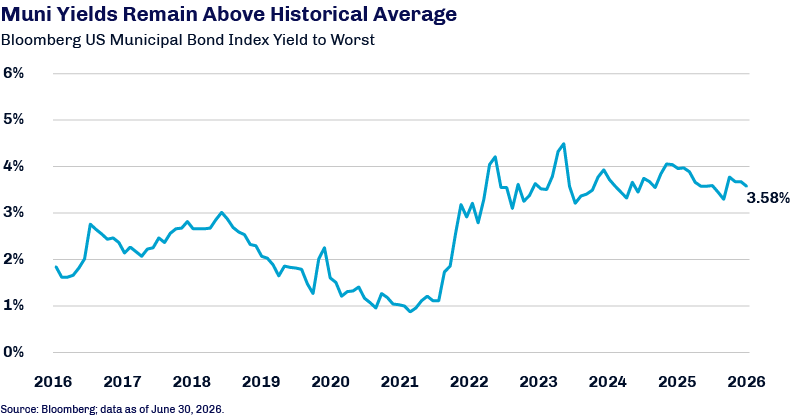

1 Source: Bloomberg; data as of July 15, 2026.

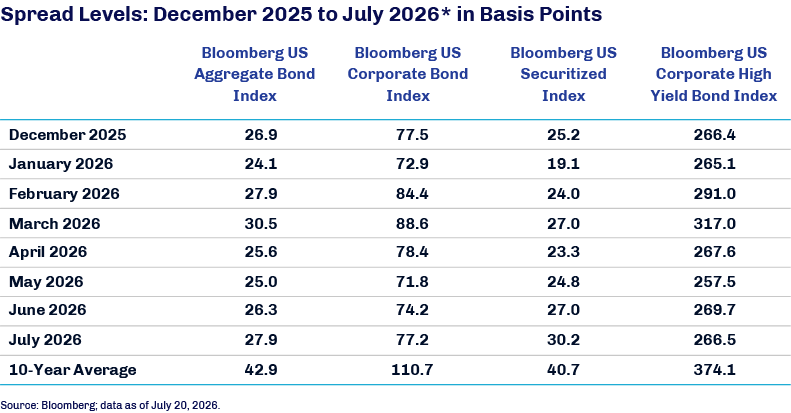

2 Source: Bloomberg; data as of July 20, 2026.

The information contained in this material is provided by First Eagle Investment Management, LLC (“FEIM”) and its global subsidiaries (collectively, “First Eagle”). FEIM is an investment adviser registered with the US Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training.

This material is for informational purposes only and reflects prevailing conditions and the judgment of the author(s) as of the date of publication, all of which are subject to change. This material should not be relied upon as investment advice; it does not constitute a recommendation to buy or sell a security or other investment; and it is not intended to predict or depict the performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or consider the specific objectives or circumstances of any investor. We consider the information in this material to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment.

Prospective investors should inform themselves and consult with an investment, tax or legal professional as to any applicable legal requirements, taxation and exchange control regulations in the countries of their citizenship, residence or domicile that may be relevant prior to investing.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

All investments involve the risk of loss of principal.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Investments in bonds are subject to interest-rate risk and can lose principal value when interest rates rise, while they typically increase their principal values when interest rates decline. Bonds are also subject to credit risk, in which the bond issuer may fail to pay interest and principal in a timely manner, or that negative perception of the issuer's ability to make such payments may cause the price of that bond to decline.

Investments that are concentrated in a specific industry or sector may be subject to a higher degree of risk than funds whose investments are diversified and may not be suitable for all investors.

Federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis.

Bloomberg US Aggregate Bond Index (Gross/Total) measures the performance of the investment grade, US dollar-denominated, fixed-rate taxable bond market in the US, including Treasuries, government-related and corporate securities, fixed-rate agency MBS (agency fixed-rate and hybrid ARM passthroughs), ABS, and CMBS. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Corporate Bond Index (Gross/Total) measures the performance of investment grade, fixed-rate, taxable corporate bond market. It includes US dollar denominated securities publicly issued by US and non-US industrial, utility and financial issuers. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Securitized Index (Gross/Total) measures the performance of US mortgage-backed-securities (MBS), asset-backed securities (ABS), commercial mortgage-backed securities (CMBS) and covered assets. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Corporate High Yield Bond Index (Gross/Total) measures the US dollar-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below and is composed of fixed-rate, publicly issued, non-investment grade debt, is unmanaged, with dividends reinvested, and is not available for purchase. The index includes both corporate and non-corporate sectors. The corporate sectors are Industrial, Utility and Finance, which include both US and non-US corporations. A total-return index tracks price changes and reinvestment of distribution income. All investments involve the risk of loss of principal.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The information presented does not reflect the performance of any fund, strategy or account managed or serviced by First Eagle, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this material will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

Availability of the products or services described may be restricted by law in certain jurisdictions. This material may not be distributed, published or used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

United Kingdom

Napier Park Global Capital Ltd is authorised and regulated by the Financial Conduct Authority (FRN: 541427) in the United Kingdom.

Middle East

This material is for information purposes only and has not been, and will not be, registered with or reviewed or approved by any regulator located in the Middle East. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe to or purchase, any products, strategies or other services, nor shall it, or the fact of its distribution, form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this material wishes to receive further information regarding any products, strategies or other services, it shall specifically request the same in writing from an authorized financial adviser.

Canada

Pursuant to the international adviser registration exemption in National Instrument 31-103, First Eagle Investment Management, LLC. is informing you that: (i) First Eagle Investment Management, LLC. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration under National Instrument 31-103; (ii) First Eagle Investment Management, LLC’s jurisdiction of residence is New York, USA; (iii) there may be difficulty enforcing legal rights against First Eagle Investment Management, LLC. because it is a resident outside of Canada and all or substantially all of its assets may be situated outside of Canada.

FEF Distributors, LLC (“FEFD”) (SIPC), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy or product.

First Eagle Investments is the brand name for First Eagle Investment Management, LLC and its subsidiary investment advisers. Diamond Hill is the brand name for Diamond Hill Capital Management, LLC, an investment adviser.

© 2026 First Eagle Investment Management, LLC. All rights reserved.