Macro & Market Views

Mechanics and Benefits of Securitization

Mechanics and Benefits of Securitization

- Securitization transforms pools of loans into investable securities, creating differentiated risk and return profiles. By selling or pledging loans to a trust and dividing the resulting securities into tranches, issuers can appeal to a broad range of investors with varying risk tolerances.

- The structure of securitized deals is designed to reduce funding costs while improving capital efficiency for lenders. Companies can use high-quality collateral to access lower-cost financing through securitized markets rather than relying solely on more expensive unsecured debt.

- Post-financial crisis reforms and credit enhancements have strengthened the securitized market. Risk-retention requirements, subordination, reserve accounts, overcollateralization and excess spread help align issuer and investor interests while providing layers of protection against collateral losses.

Securitization is not a new concept. In its most basic form, securitization dates back to the late 18th century. The first modern residential mortgage- backed security was issued by the Government National Mortgage Association in 1970, fueling a dramatic expansion in the housing market.

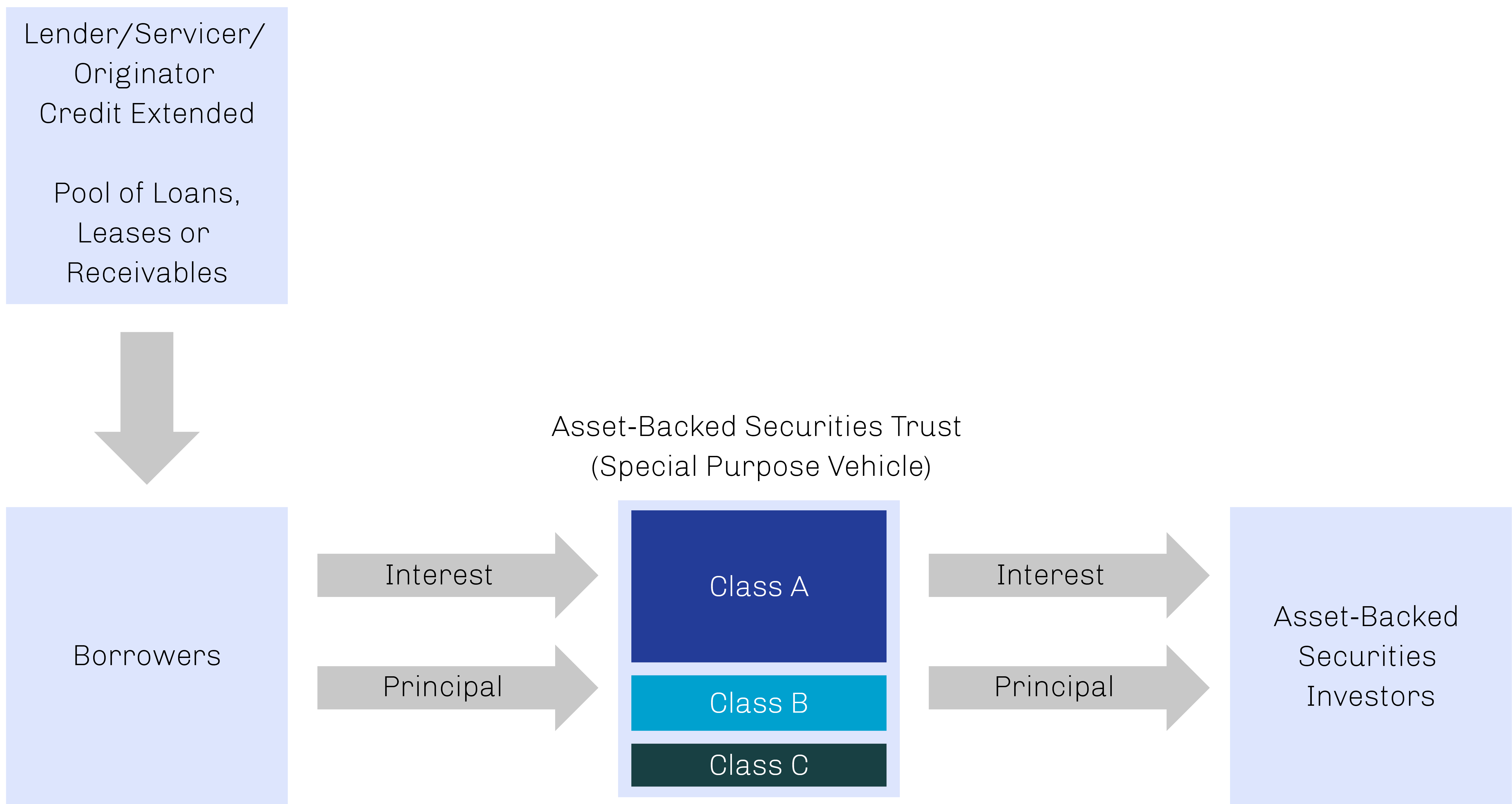

A securitized deal begins with an agreement between a lender and a borrower as to the amount borrowed, interest rate paid, collateral to secure the loan and loan maturity. The borrower’s obligation is then sold or pledged to a trust along with a variety of similar loans, creating the securitized product.

Securitized issues are split into tranches, which are categorized into varying degrees of subordination. Each tranche is separate and distinct from the other tranches, and each has a different level of credit protection or risk exposure.

The primary benefit of securitization is to reduce funding costs. Through securitization, a company that is rated BB but maintains assets that are very high in quality (AAA or AA) can borrow at significantly lower rates, using the high-quality assets as collateral, as opposed to issuing unsecured debt.

The History of Securitization

Securitization originated in its most basic form in the late 18th century with farm securitization by railroads to assist in funding the expansion of the railroad system across the United States. The mortgage-backed securities market as we know it began in February 1970 when the US Department of Housing and Urban Development (HUD) created the first modern residential mortgage-backed security, issued by Government National Mortgage Association (Ginnie Mae).

Mortgage securitization allowed banks to transfer risk and allowed home buyers to put up only a fraction of the cost and mortgage the balance. This key evolution of the mortgage market extended the American dream of home ownership to those who were unable to raise the large down payment previously needed to purchase a home, resulting in a dramatic housing market expansion. By 1985, the securitization market evolved to include the first non-mortgage assets that would serve as collateral: automobiles. This was the beginning of the asset-backed securities (ABS) market and would quickly lead to other categories of collateralization including but not limited to credit cards, equipment, aircraft, private student loans and, most recently, cell phones.

Impacts of the Financial Crisis on Securitization

Before securitization, banks would retain loans on their balance sheets (a process often referred to as “originate to hold”). Because banks would be the entity bearing the risk should a loan default, banks were incentivized to originate high credit quality loans.

With the evolution of the securitized market and pooling of assets, the “originate to distribute” model came into existence. Lenders were now able to transfer the risk associated with securitized deals by selling those assets to a variety of investors who would then assume the risks associated with the deals. While this new model had the advantage of increasing the lenders’ liquidity (by moving assets off their books and receiving the funding much sooner than waiting for loans to pay off), the risks associated with the loans were transferred to the investors who bought these securities.

Leading up to the financial crisis, we saw an epidemic of lenders pushing the originate to distribute model to grow their business and profits. Since lenders would not suffer if the loans were not repaid, they no longer had an incentive to ensure the loans would be of appropriate quality. Evidence is quite clear that leading up to the financial crisis, mortgage lenders increasingly loosened their underwriting standards and often disregarded a borrower’s ability to pay. Again, the underwriters were not concerned since they were going to package the various mortgages and sell them to investors, thus transferring any credit risk away from their own business. This misalignment of interest led to a widespread drop in loan credit quality. The lack of due diligence by investors combined with the seemingly nonchalant attitude of the rating agencies resulted in widespread deterioration of the mortgage-backed securities market.

Emerging from the financial crisis, the securitized market has been forced to implement a new methodology that ensures underwriters maintain a vested interest in loans they are underwriting. “Skin in the game” refers to a provision put forth in the Dodd-Frank legislation that requires underwriting parties to maintain a certain level of economic interest—typically 5% or greater—in any deals that are brought to the market. There are also rules in place that prevent underwriters from diluting or hedging the associated risk of their securitized offerings. This change has resulted in stronger underwriting, with higher levels of scrutiny for borrowers and higher-quality issuance in the securitized market.

Structuring a Securitized Deal

So how does a loan end up in a securitized deal? Who are the parties involved in bringing these products to market, managing their cash flows and monitoring the deals?

The first step is an agreement between the lender and the borrower as to the amount borrowed, interest rate paid, collateral utilized to secure the loan and the maturity of the loan (a car loan is a perfect example). The borrower’s obligation is then sold or pledged to a trust along with a variety of similar loans, creating the securitized product. To provide broad diversification within the pool of loans, this selection process typically does not allow “cherry picking”—i.e., selecting the most attractive loans while leaving out less favorable loans. Bankers then analyze the amount and timing of cash flows generated by the collateral, which is determined by the scheduled interest and principal payments as well as expected prepayment rates, delinquencies, defaults and any potential recoveries. The interest and principal cash flow payments are then structured into securities (Class A, B and C) that are sold to investors.

For certain segments of the market like credit cards and automobiles, the expected cash flows and deal structures are well established with a long history. Both issuers and investors have access to historical data on credit trends like delinquencies, defaults, recoveries, cumulative net losses and prepayment speeds. If the deals are going to be rated, they are submitted to the rating agencies for a review and a preliminary rating, which takes into consideration any included credit enhancements. Credit enhancements affect credit risk by providing more or less protection for promised cash flows for a security. We’ll cover this in more detail later in this paper.

Over the past several years, the market for non-rated securitized deals has grown, as issuers often prefer to not pay the rating agencies for ratings and rating agencies are unwilling to offer ratings on securities like non-performing loans. More of the deals coming to the market are issued under Rule 144A, which provides a mechanism for the sale of privately placed securities that do not have, and are not required to have, a Securities and Exchange Commission (SEC) registration in place. This usually means some kind of yield compensation for investors who purchase these securities, since they may not be as liquid as rated securities and will not meet certain investment guideline criteria for some institutional investors as well as almost all private investors.

Exhibit 1. The Flow of Assets and Cash in a Securitized Deal

Source: Diamond Hill; data as of June 30, 2026 (most recent available).

Tranches, Classes and Subordination

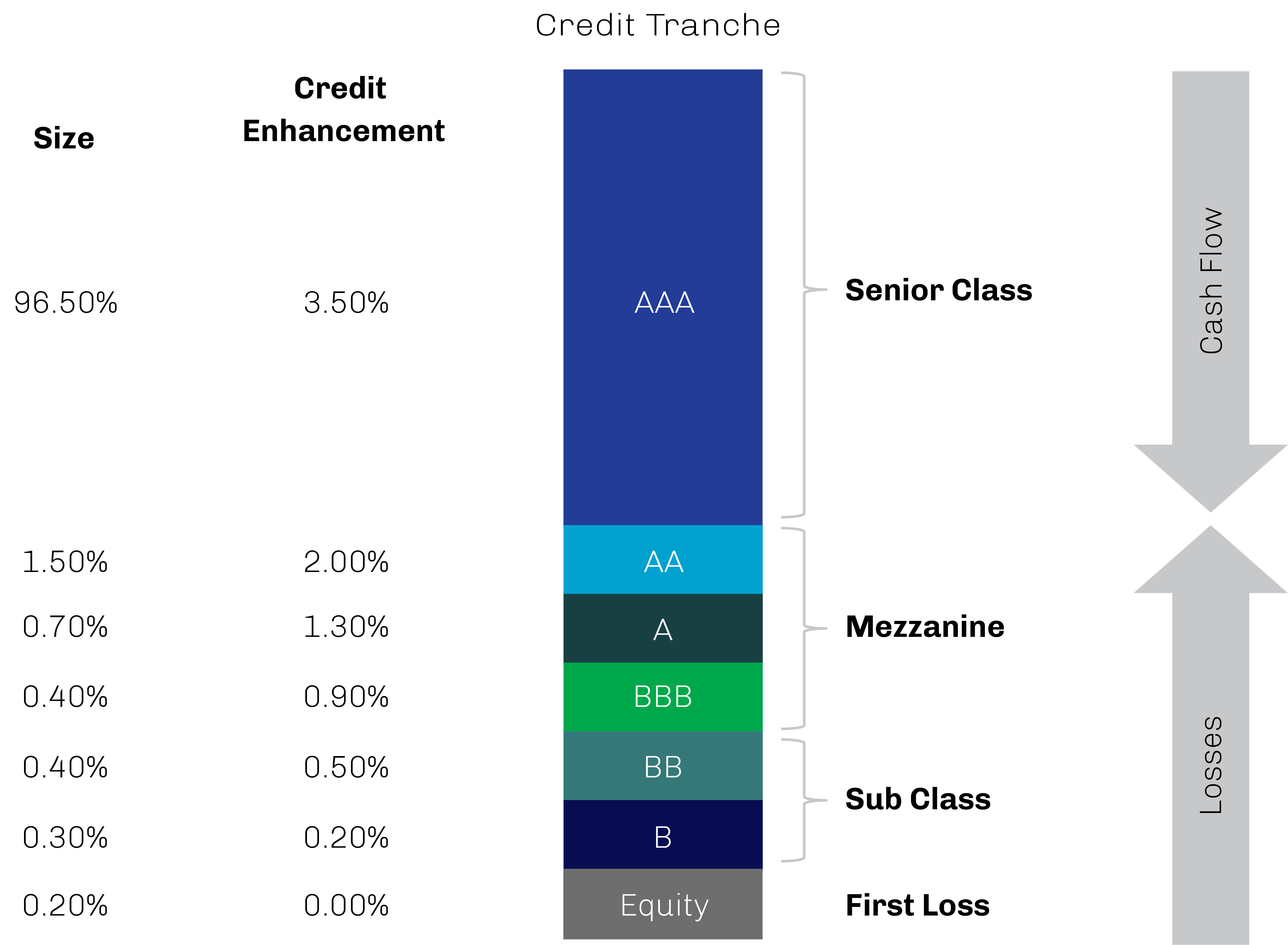

Securitized issues are split into tranches, which are categorized into varying degrees of subordination. Each tranche is separate and distinct from the other tranches, and each has a different level of credit protection or risk exposure. In a typical sequential structure, there is a senior class (usually referred to as the A tranche) with a potential wide variety of junior or subordinated tranches (B, C, etc.). The subordinated tranches serve as protection for the senior classes as well as any other tranches above them in the capital structure (B class supports A class, C class supports both B and A, and so on).

Typically, the senior classes have first claim on the cash that the deal receives while the junior classes only start receiving principal repayment after the more senior classes have been repaid in full. Because of the cascading nature of the cash flows, this arrangement is often referred to as a cash flow waterfall. If the underlying asset pool becomes insufficient to make payments on the securities (in the event of a loan default, for example), the loss is absorbed first by the subordinated tranches, and the upper-level tranches remain unaffected until the losses exceed the entire amount of the subordinated tranches. The senior securities might be AAA or AA rated, signifying lower risk, while the lower credit quality subordinated classes receive a lower credit rating, signifying higher risk.

The most junior class (often called the equity class) is the most exposed to default risk. In some cases, this is a special type of instrument that is retained by the originator as a potential profit flow. The equity class receives the residual cash flow after all the other classes if any have been paid, but no coupon. The issuer typically retains the coupon to demonstrate their skin in the game.

Exhibit 2. Typical Capital Structure of a Securitization

Source: Diamond Hill; data as of June 30, 2026 (most recent available).

Credit Enhancement Can Mitigate Risk

One of the key components that rating agencies consider when reviewing securities is the level of credit enhancement. Credit enhancement is a method of lowering the credit risk of securities within a pool of assets being sold to investors. There are different types of credit enhancement, but, for the purposes of this paper, we will focus on the four most common: excess spread, reserve account, overcollateralization and subordination.

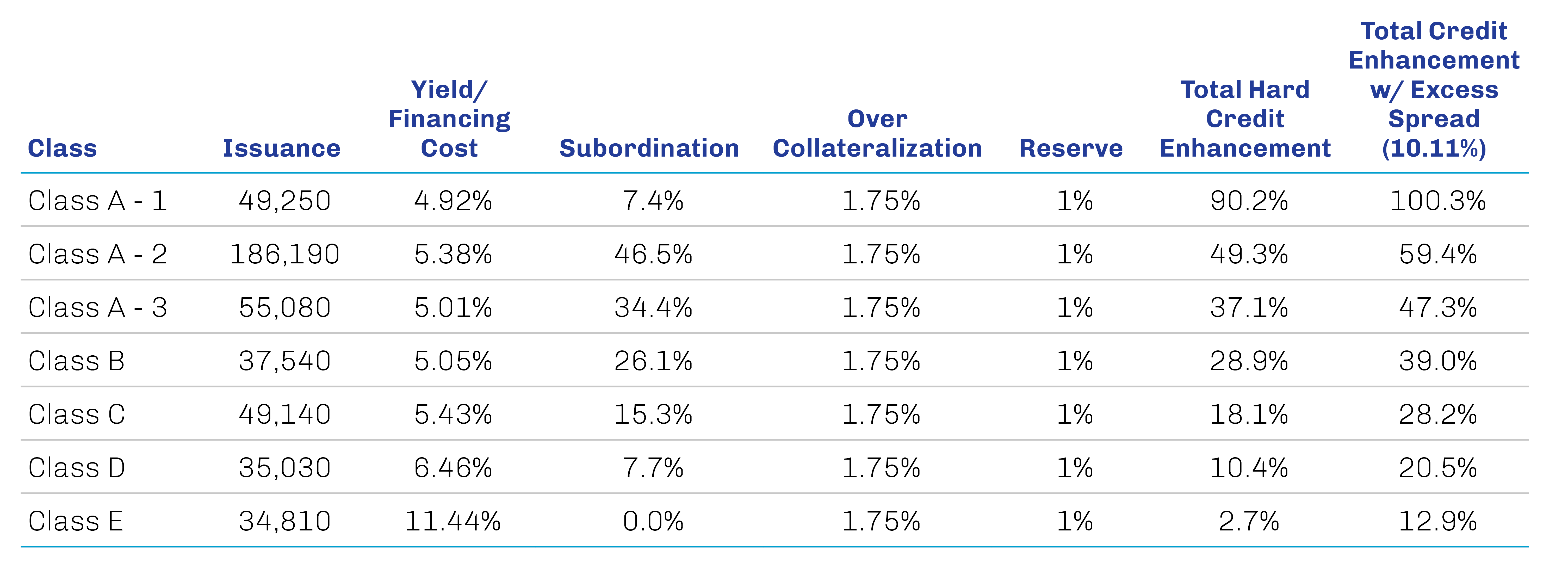

Below we illustrate the initial enhancement level per tranche utilizing a recent Flagship Credit Auto Trust deal (FCAT 2023-1) that was sold in a variety of classes and totaled $447 million.

Excess spread. Excess spread is net interest that is left over after all expenses are covered with an asset-backed security. This type of extra interest can be deposited into a separate account to provide extra assurances on an investment. The lender will often collect extra money on the spread so that they can make up for potential missed payments in the future. This excess spread enhancement will be applied to all tranches of a deal.

Exhibit 3. Excess Spread Example

* Financing costs refers to the amount paid by the deal to the investor.

Source: Flagship Credit Auto Trust 2023-1 initial listing prospectus.

Weighted average coupon (WAC) can vary based upon how quickly various loans in the pool are paid off. For example, if a borrower with an interest payment of 18% pays off his loan, the WAC of the deal will decrease slightly.

Reserve account. The issuer agrees to put aside a small percentage of the market value of the deal to serve as the reserve account. These assets would be used to support the outstanding tranches of the deal should any disruption in cash flows impact the trust’s ability to pay for its monthly obligations. For FCAT 2023-1, the reserve account started with a level of $4,550,000, or 1% of the total deal.

Overcollateralization. Overcollateralization is the process by which the lender constructs the offered bonds such that they will be worth less than the actual value of the pledged assets acting as collateral. In the FCAT example above, the total deal balance was $455.0 million while the total amount of issuance was $447 million, representing overcollateralization of 1.7%.

Exhibit 4. Overcollateralization Example

Source: Flagship Credit Auto Trust 2023-1 initial listing prospectus.

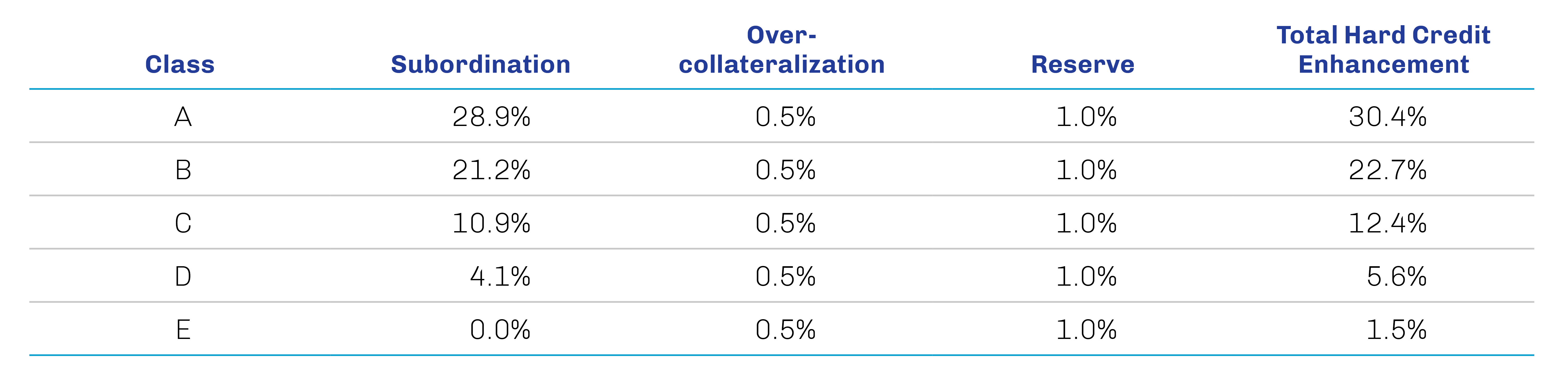

Subordination. A popular type of internal credit support is the senior/subordinated (or A/B) structure. It is characterized by a senior (A) class of securities and one or more subordinated (B, C, etc.) classes that function as the protective layers for the A tranche. If a loan in the pool defaults, any loss thus incurred is absorbed by the subordinated securities first. The A tranche is unaffected unless losses exceed the amount of the subordinated tranches.

The senior securities are the portion of the ABS issue that has the most credit protection, while the lower quality (but presumably higher yielding) subordinated classes receive a lower rating or are unrated.

Exhibit 5. Subordination Example

Source: Flagship Credit Auto Trust 2023-1 initial listing prospectus.

Evolution of a Securitized Deal

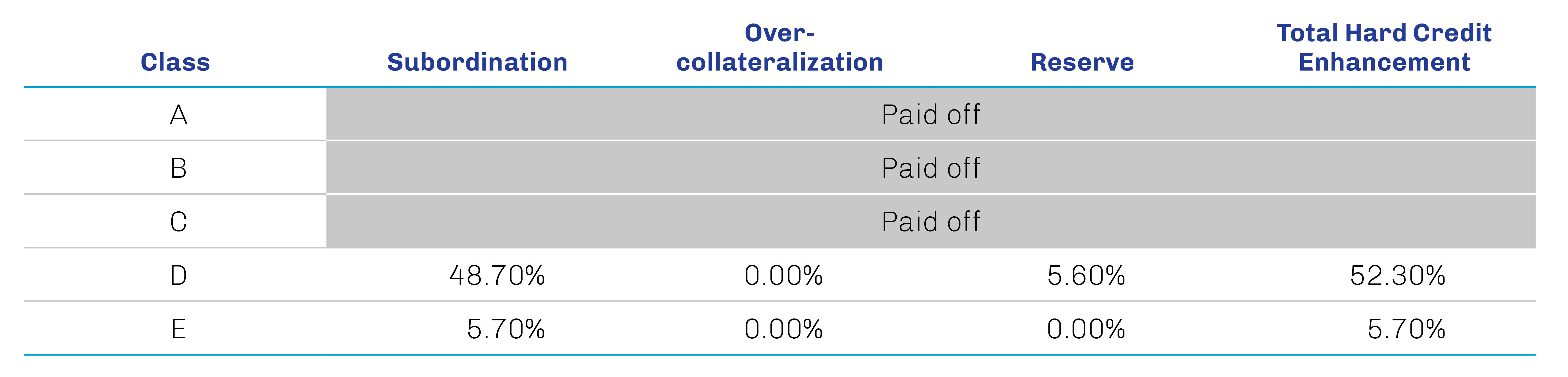

The following is an example of how these deals evolve over time and the process of amortization (paying down balances as borrower payments are made). The security is the Flagship Credit Auto Trust 2021-3, issued on August 19, 2021. We are able to examine how the loans in the security have performed by reviewing the monthly remittance report, which is published for all owners of the bonds by the trustee of the security. In the following tables, data for the deal on the date of issuance is compared to data as of April 15, 2026, nearly five years into the life of the security. The credit enhancement in the transaction has grown for each class since issuance due to changes in the three key areas of credit support.

Subordination. The level of subordination increases as loan payments made by borrowers flow into the deal. For example, the subordination support on the D tranche increased from 4.1% at issuance to 46.7% more recently as that portion of the deal paid down from a balance of $25.8 million to $17.8 million. The increase in subordination reflects the impact of both the reduction of the tranche size along with the reduction of the remaining balance. With tranches A through C paid off, all of the principal payments are applied to D tranche, while tranche E is receiving only interest payments until the D tranche is paid off.

Reserve account. The original amount was 1.0% of the pool balance, or roughly $3.8 million at closing. The reserve account has declined to $1.9 million over the past five years, reflecting funds used to pay losses in the pool since its inception. However, the remaining $1.9 million represents a larger percentage of the outstanding pool (5.6%) as it has paid down from the original balance of $378.0 million to $33.4 million.

Overcollateralization. The increased level of overcollateralization is the result of the difference between the principal balance on the receivables (auto loans) and the current value of the remaining notes. Once the deal reaches the maximum level of overcollateralization (in this case 3.40%), excess cash flows are then used to pay the residual securities associated with the structure.

Exhibit 6. Flagship Credit Auto Trust 2021-3

At Issuance on August 19, 2021

Source: Flagship Credit Auto Trust 2023-1 initial listing prospectus.

As of April 15, 2026

Source: Flagship Credit Auto Trust 2021-3, May 2026 remittance report.

Lender Benefits of Securitization

But what is the purpose behind securitization? Why would a company package up assets to which they have a claim on the interest and principal payments and sell them on the open market?

The main reason for securitization is to reduce a company’s funding costs. Through securitization, a company that is rated BB but maintains assets that are very high in quality (AAA or AA) can borrow at significantly lower rates, using the high-quality assets as collateral as opposed to issuing unsecured debt. For example, Moody’s downgraded Ford Motor Credit’s rating in January 2002, but senior automobile-backed securities, issued by Ford Motor Credit in January 2002 and April 2002, continued to be rated AAA because of the strength of the underlying collateral and other credit enhancements.

Let’s look at a more recent example from Ford.

Ford Motor Co. lends money to consumers to facilitate the process of selling their cars. Ford securitizes these loans and receives money for them from investors. Ford can now use these proceeds to lend additional money to new borrowers to sell more cars. If they did not securitize these loans and only used corporate balance sheet assets to fund these transactions, they’d have to issue additional unsecured—and more expensive—debt, further weighing on credit quality and increasing the cost of funding. Companies can access the securitized market to move these transactions off their balance sheet and utilize a cheaper funding source for part of their business, while maintaining higher credit quality.

Ford recently issued a new securitized deal (FORDO 2023-A) with a weighted average life of 1.62 years and a weighted average yield of 5.00%, which is the amount that investors will receive as borrowers pay off their car loans. Ford moves the liability off their balance sheet and collects an upfront lump sum that is used to pay down unsecured debt or fund business operations. Unsecured three-year Ford debt has a yield of 6.80% and a lower credit quality rating (Ba2/BB+) than the securitized deal. So, Ford can acquire $1.6 billion in funding at 5.00% using auto loans as collateral on the deal instead of paying over 100 basis points more for unsecured bonds.