Macro & Market Views

The Small Idea: Risky Business

The Small Idea: Risky Business

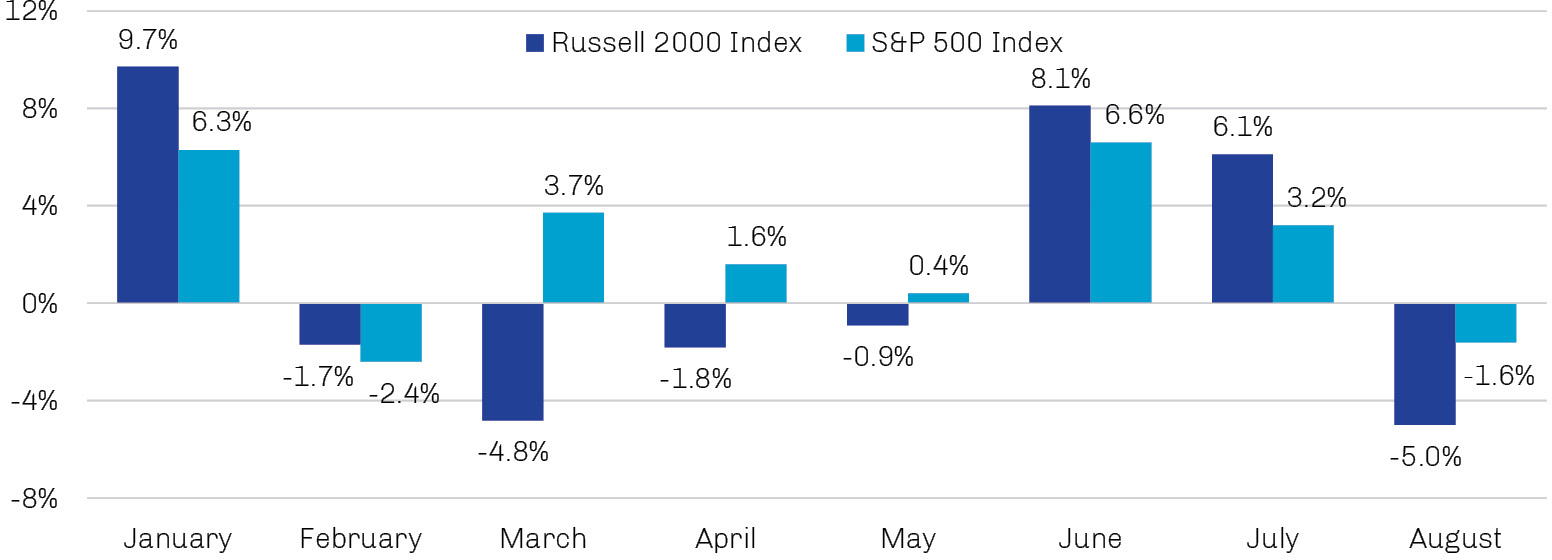

As most of the country continued to swelter through a hot summer, a chill fell over the small cap market during August.

After a very strong June and July during which the Russell 2000 Index outpaced the S&P 500 Index by more than 400 basis points (shown below), August performance for the small cap market swung deeply negative. While it can be unnerving, such volatility is consistent with the Rusell 2000’s historical patterns, both in 2023 and over the long term. To wit, annualized standard deviation of monthly returns over the past 10 years for the Russell 2000 stands at 21.0% compared to 15.5% for the S&P 500.1

From our viewpoint as active, fundamentally driven investors, however, the small cap market’s volatility is not a bug, but a feature.

Pronounced Swings in Performance Are Nothing Unusual for Small Caps

Monthly Returns, Year-to-Date 2023

Source: FactSet; data as of August 31, 2023.

This edition of The Small Idea was written by Bill Hench, head of the Small Cap team and portfolio manager.

Volatility ≠ Risk

Having spent my entire 20-year portfolio management career in the small cap space, my experience has been that high levels of volatility are either currently present or soon to begin—pretty much like an episode of Seinfeld on cable. Because of the consistent inconsistency of the market in which we invest, the team and I have grown accustomed to certain questions emerging whenever performance whipsaws lower: How do you think about volatility? How should we think about it? What can be done?

While the amount of volatility that constitutes too much volatility is within the purview of each investor, the only way to avoid the relatively high volatility inherent in small cap investing is to not invest in small cap stocks. That is not our idea of fun; more important, it denies investors exposure to what has been the most profitable segment of the equity markets going back to 1927.2 Further, by accepting our view that the greatest risk investors face is not day-to-day market volatility but the permanent impairment of their capital, it seems likely that perhaps the best way to deal with volatility is to accept it, prepare for it and make it work for you.

We sometimes think of volatility much the same way that Winston Churchill must have thought of alcohol when he said, “I have taken more out of alcohol than alcohol has taken out of me.” Sure, the team has had days or weeks or even months when we were ready to forswear small caps and go cold turkey. But then we look back on these periods of heavy volatility in the small cap markets, however unpleasant they may have felt at the time, and recall fondly the attractive investment opportunities we gained access to as a result.

As Churchill is not necessarily our go-to for investment wisdom, let’s turn instead to someone who knows a thing or two about finding value in the stock market: Warren Buffett. In a 1994 letter to Berkshire Hathaway shareholders, Buffett referenced the unpredictable and often illogical behaviors of the allegorical “Mr. Market,” as introduced by Ben Graham in The Intelligent Investor, concluding that “…a wildly fluctuating market means that irrationally low prices will periodically be attached to solid businesses.”3 As the most Mr. Market-y cohort of US equities, small cap stocks have closely followed the volatile pattern Buffett described, and in doing so have presented chances for disciplined active managers to identify individual names they believed were temporarily trading below their normalized valuation and potentially could drive index-beating performance in the future.

To continue the quote above, Buffett goes on to decouple volatility from risk, saying “it is impossible to see how the availability of such [irrationally low] prices can be thought of as increasing the hazards for an investor who is totally free to either ignore the market or exploit its folly.”4 While some may choose to ignore the small cap market because of its volatility, count us among those looking to exploit that volatility.

- Source: FactSet; data as of August 31, 2023.

- Source: Kenneth R. French data library; data as of August 31, 2023.

- ,4. Warren E. Buffett to the Shareholders of Berkshire Hathaway Inc., March 1, 1994.