BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

Harvesting AI Productivity with Smart Farming

Portfolio Manager and Senior Research Analyst

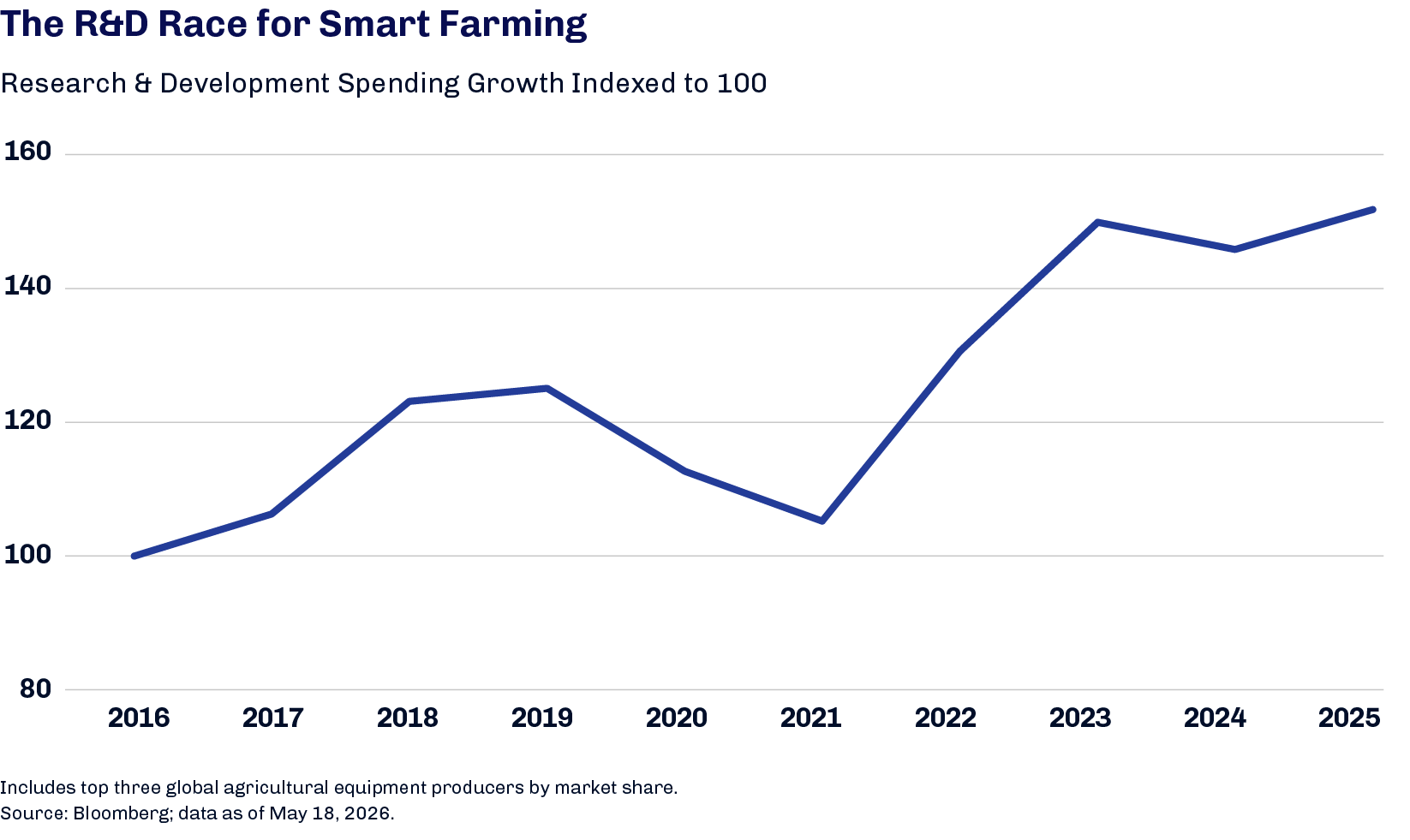

While much of the excitement about artificial intelligence (AI) is focused on the promise of transformational productivity from the massive capital expenditures in data centers and infrastructure, we are already seeing what we believe to be practical and economically meaningful AI applications in sectors that are not traditionally associated with AI. One such example is “smart farming” where farmers use AI to help lower input costs, improve labor efficiency and make better decisions in the field.

In our view, one of the clearest examples is precision application. AI-enabled systems can now identify weeds in real time and apply herbicide only where it is needed, rather than spraying an entire field evenly. That helps reduce chemical use and lowers costs, while also supporting more sustainable farming practices. This can be a real economic benefit for an industry where input costs matter enormously.

Because labor is often difficult to find or expensive to retain, AI is also being used to address labor constraints. Farmers have narrow windows to plant, spray and harvest, and AI-powered equipment have autonomous or semi-autonomous capabilities to help farmers operate more efficiently and with greater consistency, especially during these critical periods. This is another example of AI creating potential value through better execution.

AI is becoming part of how farms are managed through connected platforms that can analyze machine data, field-level information and operating results to help farmers monitor performance and make better decisions across their operations. Over time, that data is also used to improve the tools, creating a feedback loop that makes the technology more useful.

Autonomous equipment and digital farm management tools show how AI is already being embedded into the farm economy in a practical and economically valuable way. In our view, agricultural equipment is an indirect way to invest in real AI-driven productivity gains, while avoiding some of the valuation excesses that have come with more narrative-driven parts of the market in recent years. We are particularly drawn to resilient market leaders that are best positioned to adopt and integrate new technologies because they combine deep research and development (R&D) capabilities, strong customer relationships and a clear understanding of their end markets. As equipment becomes more connected, software-enabled and data-driven, service and maintenance can become more embedded in the customer relationship, potentially increasing switching costs and strengthening the stickiness of the installed base over time.

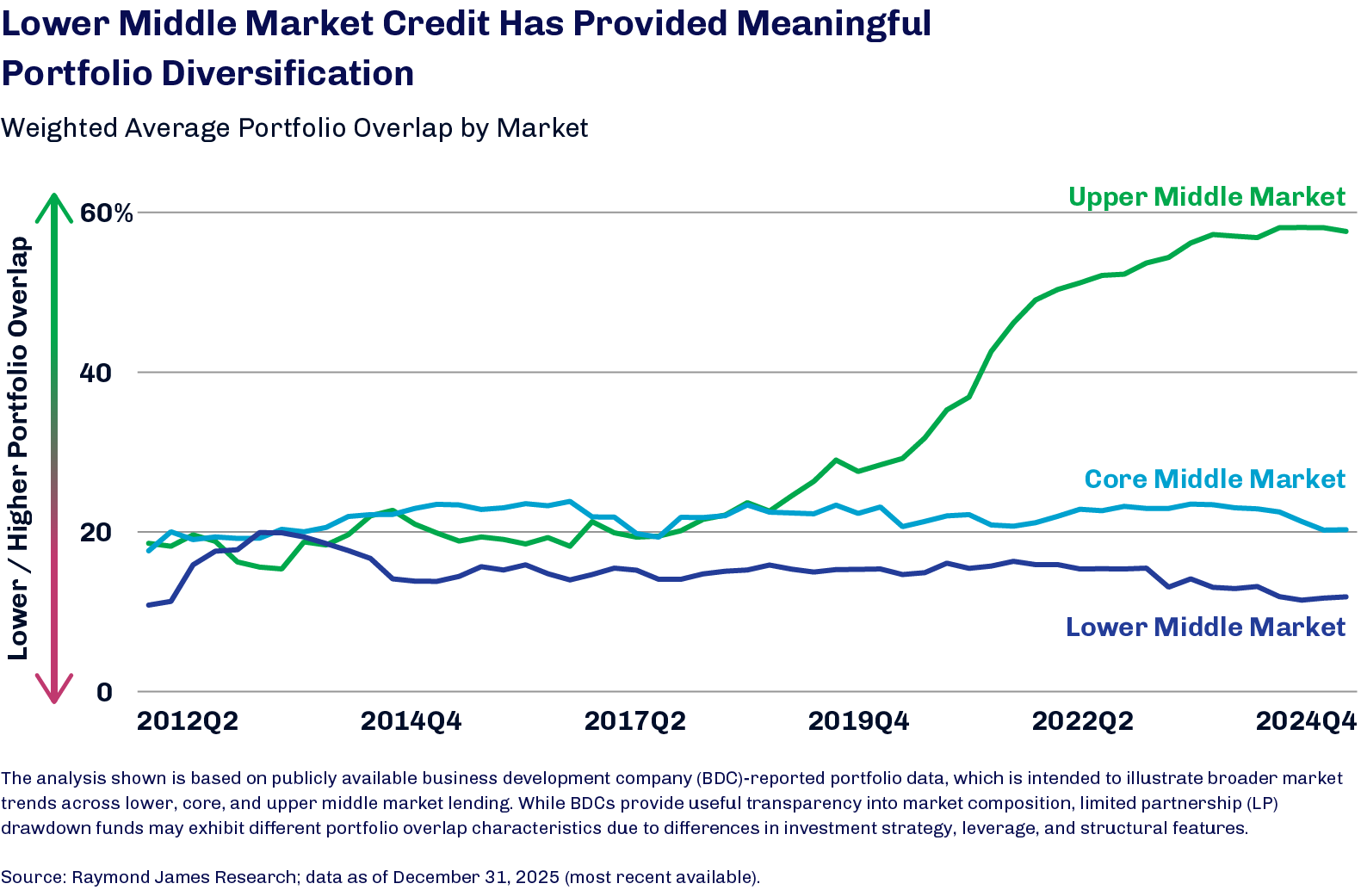

As private credit grew in popularity and capital poured in, lenders increasingly focused their dry powder on the larger end of the middle market. Not only has this trend hastened the deterioration of many structural protections in core and upper middle market deals, it has also resulted in increased overlap among lenders in these spaces—and made investors’ access to diversification more challenging.1

As shown in the chart below, the percentage of portfolio overlap among core and upper middle market deals has been on the rise over the past three-plus years, suggesting portfolio exposures are more concentrated than they may appear on the surface. Overlap among lower middle market deals, in contrast, has remained limited.

We think there are a few reasons for this. The higher volume of transactions in the lower middle market—the number of loans to these borrowers annually is about seven times that made in the upper and core middle markets combined—provides lenders with ample opportunity to source deals, and the smaller average size of these loans often enables them to be funded by a single lender.2 Beyond greater diversification, the relatively muted competition in the lower middle market that has resulted from the upmarket migration of lenders has supported the preservation of robust covenants, conservative leverage and lender control that originally drew investors to the asset class.

The lower middle market—comprising approximately 180,000 companies with earnings before interest, taxes, depreciation and amortization between $5 and $25 million—offers exposure to the “backbone of the American economy”.3 Even with less competition than larger segments of the market, however, lending to these smaller companies still carry risks such as greater sensitivity to economic conditions, management risks and less diversified operations. In our view, these risks highlight why we believe high quality sponsored deals are essential and the importance of a dedicated sourcing network, as well as disciplined underwriting, term structuring and credit documentation.