BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

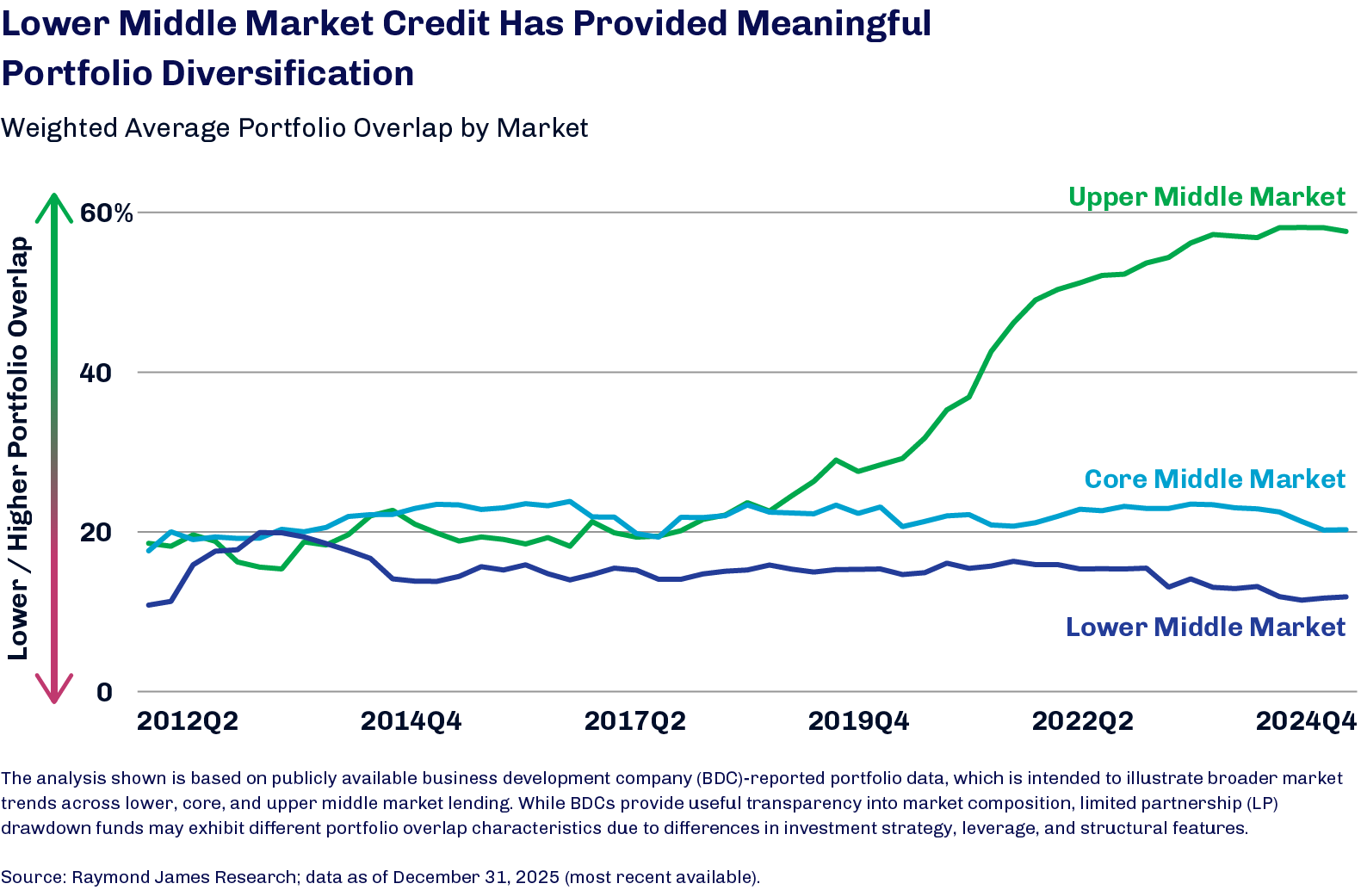

As private credit grew in popularity and capital poured in, lenders increasingly focused their dry powder on the larger end of the middle market. Not only has this trend hastened the deterioration of many structural protections in core and upper middle market deals, it has also resulted in increased overlap among lenders in these spaces—and made investors’ access to diversification more challenging.1

As shown in the chart below, the percentage of portfolio overlap among core and upper middle market deals has been on the rise over the past three-plus years, suggesting portfolio exposures are more concentrated than they may appear on the surface. Overlap among lower middle market deals, in contrast, has remained limited.

We think there are a few reasons for this. The higher volume of transactions in the lower middle market—the number of loans to these borrowers annually is about seven times that made in the upper and core middle markets combined—provides lenders with ample opportunity to source deals, and the smaller average size of these loans often enables them to be funded by a single lender.2 Beyond greater diversification, the relatively muted competition in the lower middle market that has resulted from the upmarket migration of lenders has supported the preservation of robust covenants, conservative leverage and lender control that originally drew investors to the asset class.

The lower middle market—comprising approximately 180,000 companies with earnings before interest, taxes, depreciation and amortization between $5 and $25 million—offers exposure to the “backbone of the American economy”.3 Even with less competition than larger segments of the market, however, lending to these smaller companies still carry risks such as greater sensitivity to economic conditions, management risks and less diversified operations. In our view, these risks highlight why we believe high quality sponsored deals are essential and the importance of a dedicated sourcing network, as well as disciplined underwriting, term structuring and credit documentation.

High Tide for Equities amid Inflation Undertow

Head of Global Value Team and Portfolio Manager

After selling off sharply in March with the outbreak of the Iran war, a number of global equity benchmarks—including the S&P 500 Index and MSCI World Index—have established new all-time highs in recent weeks. Driven by renewed enthusiasm around artificial intelligence and strong corporate earnings, equity investors appear to have adjusted to the impacts of the war.1

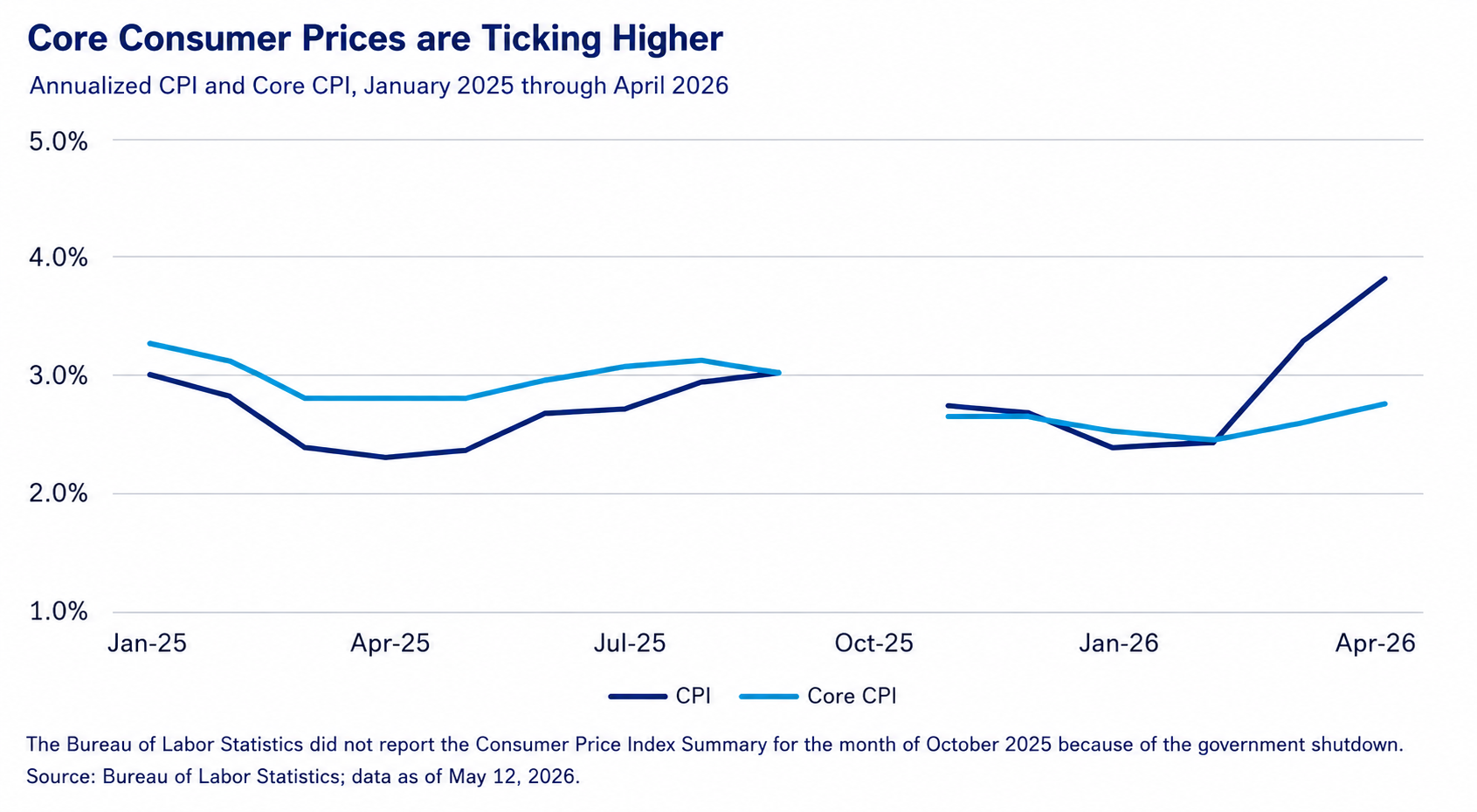

As demonstrated by the Treasury curve’s bear steepening, bond markets have been more sensitive to the deteriorating inflation dynamic—the result of the war’s energy supply shock and the very large fiscal deficits facing the US and other major economies.2 While headline inflation climbed to 3.8% in April, from 2.4% in February, higher energy and food prices have begun to seep into core readings as well; April core inflation (all items ex-food and energy) was 2.8% compared to 2.5% in February.3 Notably, bond markets have not priced in incremental credit risk, as spreads tightened back to where they were at the beginning of the year.4

This bifurcation of performance and risk perception reinforces the importance of investing in assets and businesses that can participate in nominal inflation over time. As fixed principal assets, the yield paid to investors for debt securities is fixed, as is the nominal value of the principal at maturity. While fixed principal has its merits, it also has its drawbacks, namely the inability to keep pace with inflation and pass through higher nominal prices the way assets that are fixed in supply can.

We remain skeptical that even a quick resolution in Iran would usher in a swift return to normal conditions given the damage to energy infrastructure and the need to incentivize production and development around the world. Energy prices may remain elevated for some time, in our view, with the impact continuing to diffuse across the economy. Assets able to leverage the inflationary dynamic to get better pricing may be positioned to benefit.