BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

Record Issuance Meets Resilience

Head and Chief Investment Officer of Municipal Credit Team

During the first quarter, municipal issuance set another new record with $119 billion in tax-exempt bonds and $128 billion overall.1 In the face of complicated and rapidly evolving dynamics that included the outbreak of war, spiking energy prices, renewed inflation concerns, whipsawing policy expectations and acute Treasury volatility, we were impressed by the municipal market’s ability to absorb significant issuance; in our view, it is a testament to steady investor interest in the asset class and the appealing yields on offer.

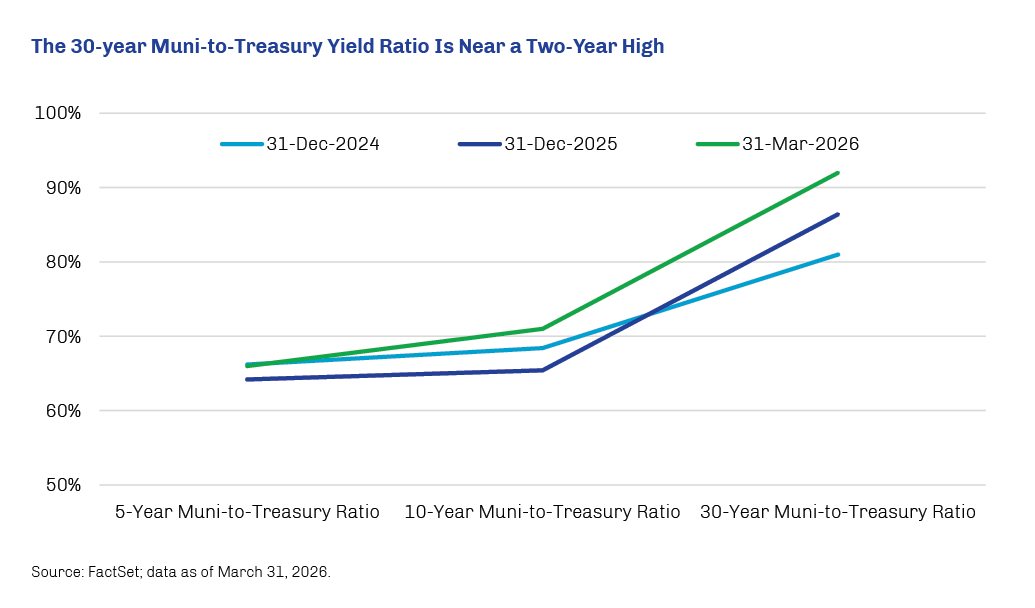

Municipal bond yields mostly followed the trend of Treasuries during the first quarter, easing across the curve early in the year before rising sharply in March as a shock to the global energy supply chain brought on by the war with Iran sent energy prices sharply higher and raised concerns about renewed inflation. The end result was a bear steepening of the muni curve in which longer-term yields increased more than short-term yields, and, as shown in the chart below, the 30-year municipal-to-Treasury yield ratio increased to a nearly two-year high.2

Meanwhile, issuer fundamentals continue to be supportive, as state budgets for fiscal 2026 overall reflect a healthy environment, general fund balances remain well above the historical average,3 and pension funding continued to improve.4 These dynamics have supported muni bond ratings activity, which has remained positive even as the ratio of upgrades to downgrades continued to moderate.5 Both defaults and first-time distressed debt remained very low in the first quarter.6

Though well off its early-year peak, the Russell 2000 Index managed to hold a 0.9% gain for the first quarter, easily outpacing the 4.3% decline of the S&P 500 Index. The Russell 2500 Index was even more resilient through the quarter’s turmoil, posting a 2.0% advance.1 While heartened by the recent relative strength of smaller stocks, we’re girding for a long race ahead, as longer-term performance trends remain significantly skewed toward large growth names.2

While the war with Iran has prompted a major disruption to world oil markets that is likely to weigh on global economic activity while contributing to inflation pressures, expectations of very strong earnings growth have us constructive on smaller names.3 This includes direct beneficiaries of higher energy prices and the war itself, such as providers to oil servicers and chemical processors; companies with upside exposure to higher chemical, fertilizer and metals prices; and suppliers to defense contractors.

Expectations of very strong earnings growth have us constructive on smaller names.

Meanwhile, aggressive capex by large companies could provide an offset to the potential impact of higher energy prices. We believe smaller tech companies supporting the AI-infrastructure build are positioned to flourish—with very little need for additional spending on research and development. Additionally, semiconductor and semiconductor capital equipment companies are finally reaping the rewards of a long-awaited upturn in the cycle.4

While the valuation gap between smaller and larger company stocks could persist for some time, we believe that solid fundamentals—underpinned by earnings—will ultimately prevail. At the same time, the higher market volatility that has emerged alongside the start of the Iran war may bring opportunities to acquire attractive businesses at distorted valuations.