BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

Is the Stagflationary Impulse Transitory or Troubling?

Head of Global Value Team and Portfolio Manager

"Never let us be elated by the fatal hope of the war being quickly ended by a devastation of their lands,” warned Thucydides in his recounting of the Peloponnesian War, a conflict that lasted for 27 years.1

April has seen a number of equity indexes bounce off their wartime lows as markets took advantage of less-bad news to rotate back into risk assets; notably, the tech-heavy Nasdaq Composite Index has posted consecutive positive trading days.2 Considering the wisdom of Thucydides, however, we’d be wary of a quick declaration of victory and a return to normal macroeconomic and market conditions.

The war with Iran has prompted what appears to be the largest-ever physical supply disruption to world oil markets and has sent a stagflationary impulse to the global economy that, the longer it persists, is likely to weigh on economic growth while adding to inflationary pressures. The rebound in risk assets seems to reflect expectations that the disruption of energy flows through the Strait of Hormuz could be short lived, but we’re leaning toward the possibility that the inflationary impacts of the conflict could linger.3

Uncertainty around this link in the global supply chain remains high. While oil and liquified natural gas prices eased with the April 8 announcement of a two-week ceasefire, the Strait remains virtually closed to traffic thanks to the subsequent US naval blockade.4 Meanwhile, damage to energy infrastructure in the Gulf suggests disruptions could be longer than widely appreciated even were hostilities to end, and Iran’s ability to weaponize the Strait at a moment’s notice may result in a persistent price premium for commodities dependent upon this shipping route.

Extended supply disruptions could result in significant demand destruction (which we are already seeing signs of in Asia through fuel rationing and flight cancelations), food-price spikes and shortages of important industrial inputs such as helium and sulfur.5 It may also tie the hands of central banks struggling to boost their deteriorating economies amid price pressures.

Extended supply disruptions could result in significant demand destruction.

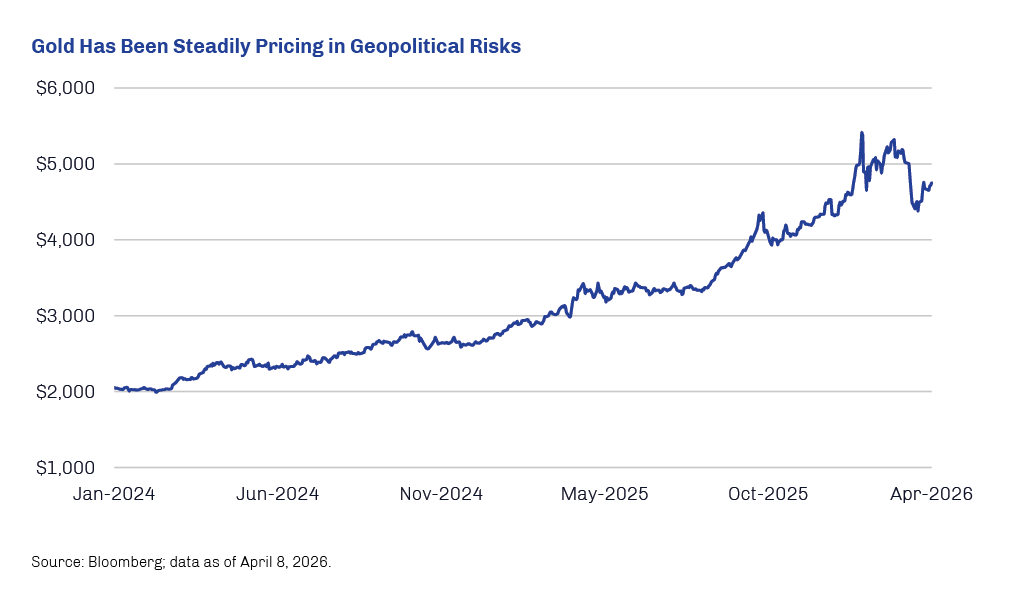

We often note how gold can sometimes serve as a proverbial canary in a coal mine, sussing out potential dangers before they are perceived by the financial markets more broadly.

This prognostic ability may help explain the massive advance in gold over the past two years through periods in which traditional drivers of the gold price—such as the direction of real and nominal interest rates, US dollar strength and central bank policy bias—were not always supportive of a rally. Essentially, it appears that gold had been steadily pricing in a large-scale geopolitical event, which ultimately came to fruition when war broke out between the US/Israel and Iran on February 28. In fact, with the drumbeats of war growing louder, gold surged 14% in January, preceding advances in integrated oil majors and spot oil prices. 1

Importantly, war changed the calculus of gold ownership, and record-high prices needed to adjust to its monetary and financial implications, including higher inflation and a more hawkish Federal Reserve. While some may view the subsequent volatility in the gold price as a disappointment given its reputation as a store of value during challenging times, those with a strategic allocation to the metal over the past couple of years have benefited handsomely.2

While markets, including gold, let out a sigh of relief with the ceasefire agreement on April 7, risks remain abundant. The Iran conflict is far from resolved, and the fighting between Ukraine and Russia has entered its fourth year with no end in sight. Meanwhile, economies worldwide face troubling debt dynamics and the potential for continued currency debasement. In other words, the long-term fundamentals for gold—and the case for strategic portfolio exposure—remain strong even as short-term trends may occasionally batter the price.3