Macro & Market Views

The Small Idea: Turn! Turn! Turn!

The Small Idea: Turn! Turn! Turn!

While songwriter Pete Seeger’s communist bonafides suggest the titular 1960s chestnut was probably not written to provide succor in the face of callous markets, as small-cap investors we can’t help but find comfort in the idea that “to everything...there is a season.”1

In fact, the strong outperformance of small cap stocks in July had us hoping that summer 2024 might finally be the season investors turned back to our target market after an extended period of relative indifference. Smaller stocks appeared poised to benefit from a string of macroeconomic releases that set the table for a federal funds rate cut in September and raised hopes the central bank could achieve a soft landing. The Russell 2000 Index surged 10.2% during July in response, outpacing the S&P 500 Index by 900 basis points.2 But one month does not make a durable rotation, and smaller stocks spent the rest of the summer in a funk.

Of course, performance relationships tend to ebb and flow over time. But while it’s been our experience that small cap/large cap leadership cycles tend to last around 10 years, the current bout of small cap underperformance has been in place since 2010. We think the elongation is at least partly due to the Covid-19 pandemic and the massive liquidity response to it. Easy capital tends to be ripe for misallocation, and the resulting distortions can take time to normalize.

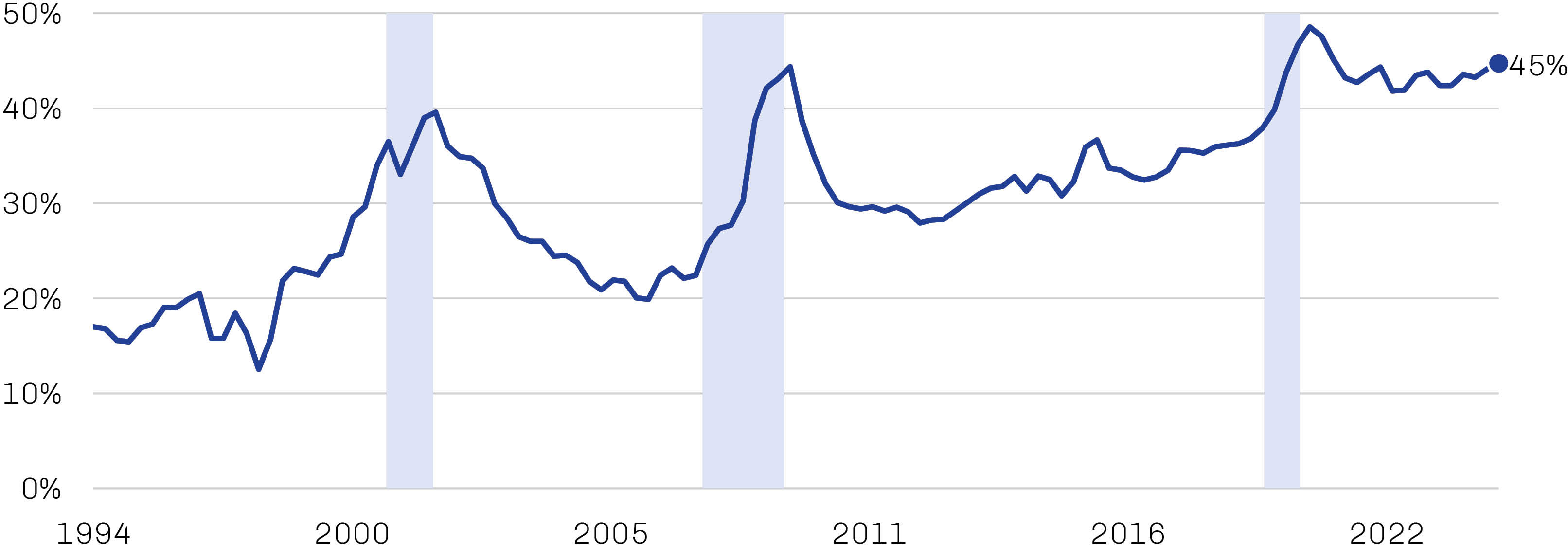

For example, the percentage of unprofitable companies in the Russell 2000 peaked at an all-time high just shy of 50% in 2020 as the impacts of pandemic-related shutterings filtered into financial results. This percentage has declined only marginally in the four years since, to a level more or less equal to its peak in the aftermath of the global financial crisis.3 Too many companies have been able to scuttle along on the back of cheap financing, and investors in general have demonstrated little interest in trying to differentiate between quality small cap names and the dross.

The Number of Money-Losing Companies in the Russell 2000 Remains Elevated

Percentage of Russell 2000 Index Companies With Negative Trailing-12-Month Earnings per Share, January 1995 through September 2024

Source: FactSet; data as of September 30, 2024.

We do see some signs that the factors contributing to this long cycle of underperformance may be reversing, however. As a result of the sharpest rate-hike cycle in Federal Reserve history, capital now has a cost—though not one so high that credit fundamentals have been broadly impacted. Rates have rallied from their midyear peaks in anticipation of Fed rate cuts—the first cut, at an oversized 50 basis points, came to pass in September—which should ease the burden of companies with floating-rate debt while lowering the cost of capital investment for all.4

As we’ve seen in the index’s underperformance over the past few years, however, it’s not enough for a company to simply remain solvent; successful names must demonstrate that they are positioned for future earnings growth and upside potential. Economic resilience may help support this. While we can’t predict whether or not a recession is on the horizon, the US economy has continued to expand despite the tighter financial conditions that have prevailed for much of the past two years, with the labor market well supported and consumer metrics remaining solid. Anecdotally, there was little in the July/August batch of conference calls among the small cap cohort to suggest companies were overly concerned about the potential for recession or planning mass layoffs.

And a Time to Every Purpose

As we were reminded over the summer, swift changes in the relative performance of small and large cap stocks can often be a deke, reflecting nothing more than a mini-burst of excitement across a long slog of weakness. A true shift in sentiment requires consistent buying interest among market participants who perceive the same undervaluation in the space we do. Often, this takes the form of mergers and acquisition activity. Strategic buyers, in particular, are often willing to pay attractive premiums for companies that have rationalized their cost structures, survived difficult times and maintained sound business models and balance sheets.

We have observed an uptick in takeout activity within the small cap universe during 2024, and we are hopeful that persistent interest from sophisticated buyers may call greater attention to the latent value we seein this market and help spark a turn of fortune. In the meantime, we remain focused on what we as investors can control: namely, the stocks we invest in and the price we pay for them.