Macro & Market Views

The Small Idea: RESPECT!

The Small Idea: RESPECT!

“I can handle things. I’m smart, and I want respect.”

From Aretha Franklin, to Rodney Dangerfield, to Fredo Corleone in The Godfather Part II (as quoted above), I’m often reminded just how hard it can be to secure status in the pantheon of asset management.

Although my fellow small cap manager friends and I frequently compare notes and commiserate, I was struck this quarter by the gallows humor that prevailed. As background to our shared professional dejection, the Russell 2000 Index is up less than 8% in total since my team joined First Eagle in late April of 2021, while the S&P 500 Index is up almost 65% over that same period.1 Thus, it’s easy to understand why many small cap managers can feel diminished, sharing Fredo’s sentiment in an industry dominated by Michaels.

Extraordinary Growth from Mega Caps Has Overshadowed Small Caps

Comparing notes with a friend who has long managed a successful small cap growth strategy, we both marveled at how—for the better part of two and a half decades—we rarely mentioned to investors, and were seldom asked about, the performance gap between small and large cap stocks. Nor were we prodded to account for the valuation discrepancy between the two groups. These days, however, the dichotomy between large and small returns appears to dominate the thoughts of current and potential investors.

The litany of factors contributing to the relative underperformance of small stocks is familiar but worth revisiting. In our view, the unique confluence of zero interest rates and massive money printing by the federal government combined with truly outstanding earnings from the largest companies in the US triggered the divide. In many ways, these conditions may have enabled investors to wrest the extra growth normally associated with small caps through much bigger, well-financed companies without worrying about liquidity, effectively slamming the window on initial public offerings (IPOs) for small companies

In the pre-Covid world, many investors assumed that small caps provided the best exposure to fast-growing stocks, juicing the odds of generating massive returns—the elusive “ten bagger.” Today, this presumption is under scrutiny as hypergrowth from huge businesses has propelled the market capitalizations of single companies— including Nvidia and Microsoft—beyond that of the entire Russell 2000.2

Small Cap Earnings May Be Poised for a Rebound…

Exacerbating the performance chasm, small company earnings left much to be desired from 2021 to 2024, as low rates punished the banks that account for an outsized share of the small cap universe. But characterizing the Russell 2000 as a dustbin of “non earners” and/or “low-quality” companies feels punitive at this point—and largely irrelevant when considering the large pool of small US companies trading at what we view as compelling valuations.

So enough with the rationalizations. We now find ourselves at a juncture where most of the excuses for poor performance have passed. Although the US still has a massive budget deficit financed by massive bond issuances, it is no longer printing money at the same frenzied pace as the Covid era. Gone, too, are the zero policy rates that plagued small banks while bolstering earnings for large cap, high-growth, long-duration tech stocks.

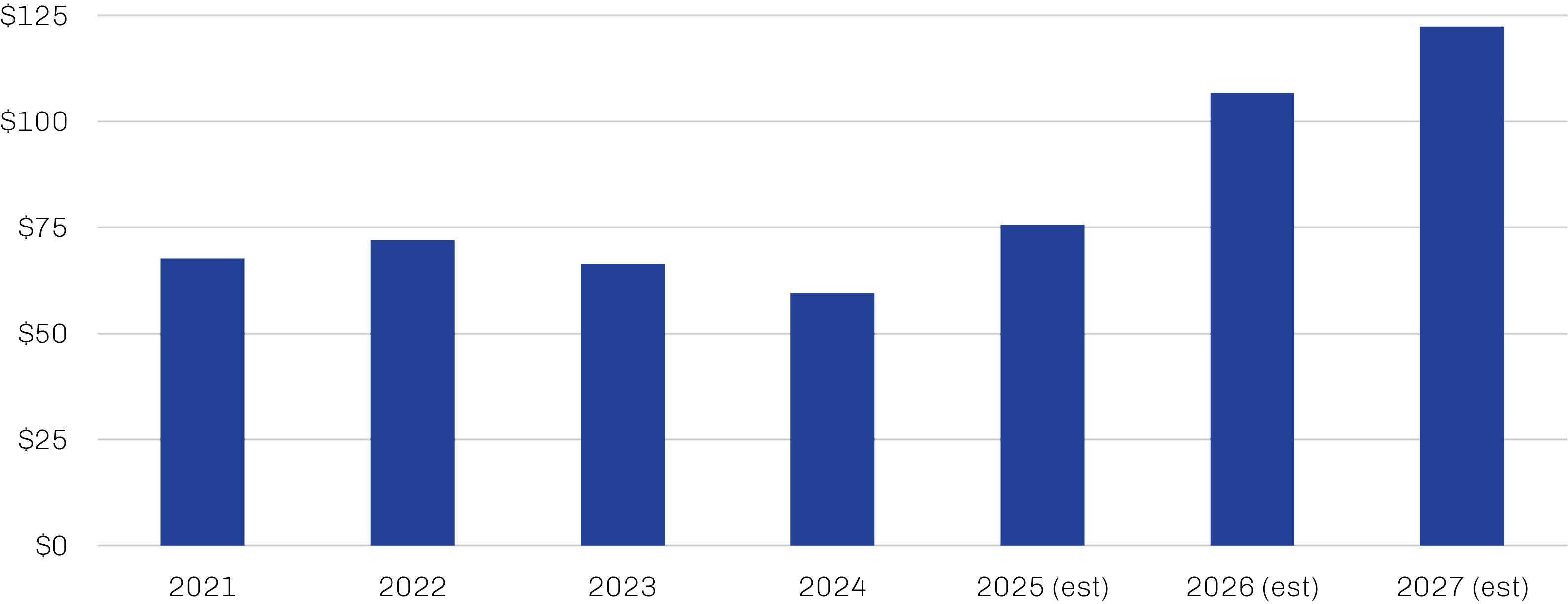

Elbowing aside past disappointments, I remain optimistic about small caps going forward, in part because there are signs earnings growth may be back on track after years of decline. Boosted by a strong first half, Russell 2000 annual earnings growth is expected to return in 2025 and persist throughout the forecast window, as shown in Exhibit 1.

Exhibit 1. Earnings for Small Caps May Be on an Upswing

Actual and Estimated Russell 2000 Index Earnings, Dollars per Share

Source: LSEG I/B/E/S; data as of June 30, 2025.

…While Still Compressed Valuations Suggest Possible Upside

To us, there appears more than enough potential opportunity in turnarounds, undervalued growth stories and asset plays to compensate for the risk of owning small stocks. Valuation premiums on recent takeovers suggest a substantial gap between where many small stocks are trading and their potential ultimate worth. Prospective rates cuts over the coming year—markets are expecting two or three by year end3—could trigger acquisition activity, potentially fueled by $2.5 trillion of private equity dry powder.4

Without a crystal ball, and with persistent macroeconomic risks—tariffs, inflation, slowing growth, higher oil prices among them—I remind myself that consensus views on many issues often prove wrong. For my fellow small cap investors and me, I hope our Michael days are in sight!