Macro & Market Views

The Small Idea: Onward and (Hopefully) Upward!

The Small Idea: Onward and (Hopefully) Upward!

Learning from the past, rather than being stymied by it, we’re always grateful for a silver lining or two.

To wit, the tariff-induced equity market volatility year-to-date has created numerous opportunities for us to reposition our portfolio and—our enthusiasm for globalization notwithstanding—instilled an appreciation that the domestically oriented small cap companies we favor may be at least somewhat insulated from trade-policy gyrations. From a wider perspective, shifting priorities in Washington could reawaken moribund mergers and acquisitions (M&A) activity, to the potential benefit of small cap stocks.

Over-Discounting Despair

Layering the same macro worries—from tariffs to interest rates to potential recession to freeform uncertainty—on top of one another can only go so far. At some point, the bad news loses its sting and investors stop re-discounting the same hypotheticals. Death-spiral prognostications to the contrary, the economy thus far has been more resilient to tariff pressures than was generally anticipated. Though GDP contracted in the first quarter as importers sought to get ahead of tariff implementation, some other readings were less dire; the job market has remained stable, for example, while retail spending has persisted in the face of abysmal sentiment.1

Renewed inflation was among the most feared byproducts of the Trump-tariff onslaught, but relatively benign prices for energy and other commodities have kept pressures in check. Inflation that in aggregate is contained serves as a good reminder of elasticity in an economy; as the price of one thing goes up, consumers often opt for a more economical alternative rather than buying nothing. While shifting preferences may ultimately dampen overall demand, assuming an unlikely confluence of negativity—everything everywhere all at once—can result in market overreactions and attractive buying opportunities.

Opportunity Amid the Carnage

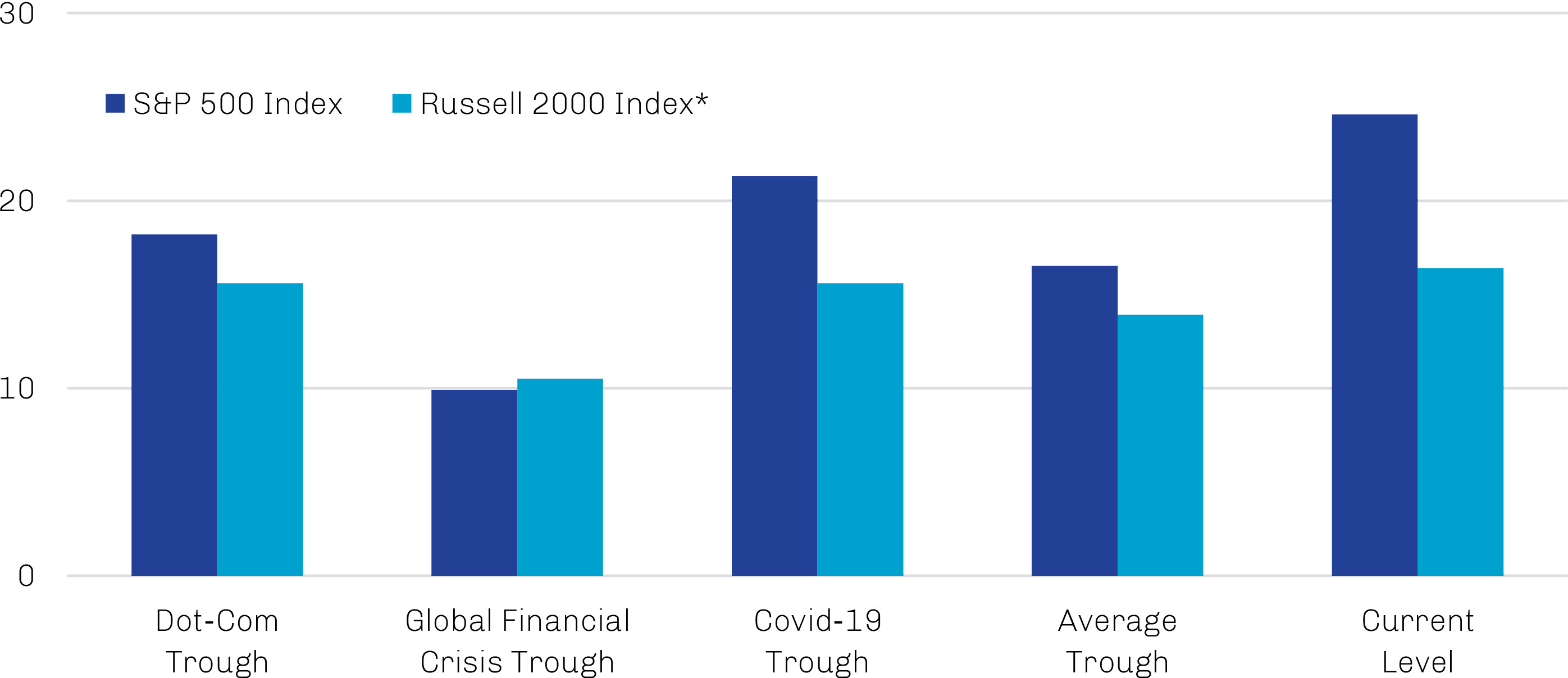

Bubbling tariff pressures came to a head with Trump’s “Liberation Day” announcement of widespread levies against friends and foes alike, triggering aggressive selling in passively managed portfolios and also allowing us to reposition our portfolio into newly attractive opportunities. Though it has rallied 17% since its April 8 bottom, the Russell 2000 Index is still 15% below its November 2024 high and, as shown in Exhibit 1, its current valuation is more consistent with the low points of recent market dislocations than a healthy environment.2

Exhibit 1. Small Cap Valuations Hover Near Previous Lows

Trailing-12-Month Price-to-Earnings Ratio

*Excludes companies with negative earnings.

Source: FactSet; data as of May 21, 2025.

Recent market dynamics have created notable investment opportunities within two segments of the small cap universe:

- Companies that appear statistically cheap, many with cyclical exposure. Some homebuilders and suppliers, for instance, currently are trading at or below book value. With the US housing market remaining vastly undersupplied, we expect these companies to do well as the cycle normalizes.

- Companies trading at distressed multiples despite projected earnings growth well above the index average. It’s rare to find high-growth companies at prices we’re willing to pay given our value discipline, but this combination historically has generated strong returns.

Hints of Hope: Supportive Policy May Yet Prevail (and Propel)

While the post-Liberation Day selloff was pronounced, the marginal impact of unabated bad news eventually began to fade. As we have often observed, sometimes the mere cessation of selling can underpin price appreciation in small caps, even absent meaningful changes in fundamentals.

With hopes that the most severe impacts of tariffs may be behind us, it’s worth noting that they also may produce tailwinds for some companies; reshored manufacturing, for example, may bolster certain domestic small companies. Meanwhile, companies in general appear likely to receive a “free pass” from the market when reporting second quarter results, as managements largely suspended forward guidance amid the tariff uncertainty that accompanied their first quarter releases.

While Trump’s policy emphasis entering his second term—namely, tariffs and DOGE-abetted cost-cutting—appeared to catch markets off guard, Washington’s focus appears to have shifted toward more business-friendly issues, such as tax policy and regulation. With the Republicans who control both houses of Congress under pressure from their constituents as a result of the Trump administration’s priorities thus far, the need to deliver the “good stuff” in advance of midterm elections may be acute.

A lighter regulatory touch from the Federal Trade Commission and Department of Justice, for example, could stimulate the economy at the voter level while also reigniting moribund M&A activity. Although dealmaking started 2025 with a bang, tariff anxiety has produced an M&A environment as slow as we have seen since at least the global financial crisis. Absent competition from private equity sponsors unwilling to sell portfolio companies at soft market prices, we anticipate public companies will be the subjects of attention from flush strategic buyers that are unencumbered by legacy holdings and have easy access to debt or equity financing. Many small companies, for example, are cheap, underleveraged and domestically focused—essentially plug-and-play add-ons for buyers interested in non-dilutive, tariff-resistant expansion. The right mix of conditions could potentially trigger a surge of small-company acquisitions reminiscent of the boom in 2003, when a spate of software, networking and industrial companies were acquired.

Speaking of private equity, we’re somewhat surprised that investors continue to pile into new vehicles, even as liquidity—not to mention returns—elude investors in older vintages. With a number of sophisticated investors seeking balance sheet respite through secondary transactions and net asset value loans, the benefits of liquidity may again be appreciated, especially in high-quality, small cap companies trading at what appear to be attractive multiples.3

For our money, we’ll take the flexibility of publicly traded small caps over the challenges inherent in capturing the illiquidity-premia potential in private equity investments.