BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

Taxable Fixed Income Markets Update: May 2026

Client Portfolio Manager, Diamond Hill Capital Management

Markets in May remained focused on geopolitical developments, evolving economic conditions and leadership changes at the Federal Reserve. Investors balanced signs of labor market resilience against mixed economic data while closely monitoring central bank independence and governance issues, which continued to influence sentiment and policy expectations.

Corporate credit. Investment grade corporate markets continue to rebound from one of the worst months in recent history—a loss of 1.98% in March—with another solid gain of 0.76% in May. Corporate spreads continued to tighten during May, reversing the widening seen earlier in the year amid geopolitical uncertainty and ending the month at 72 basis points. Despite tighter spreads, the yield-to-worst for the Bloomberg US Corporate Bond Index remained attractive at 5.13%. Investor demand for yield stayed strong, supporting $163 billion of issuance in May and helping year-to-date issuance reach a record $993 billion, up 25% year over year.1

Securitized credit. The spread on the Bloomberg US Securitized Index was essentially flat during May, in contrast with the tightening trend seen across other risk sectors. Even so, spread levels remain near historically tight ranges, reflecting continued investor support for the asset class. The sector returned 0.29% during the month, outperforming Treasuries but trailing investment grade corporates. Securitized assets have generated positive returns during all but one month since August 2025, producing a cumulative return of 5.29%.2

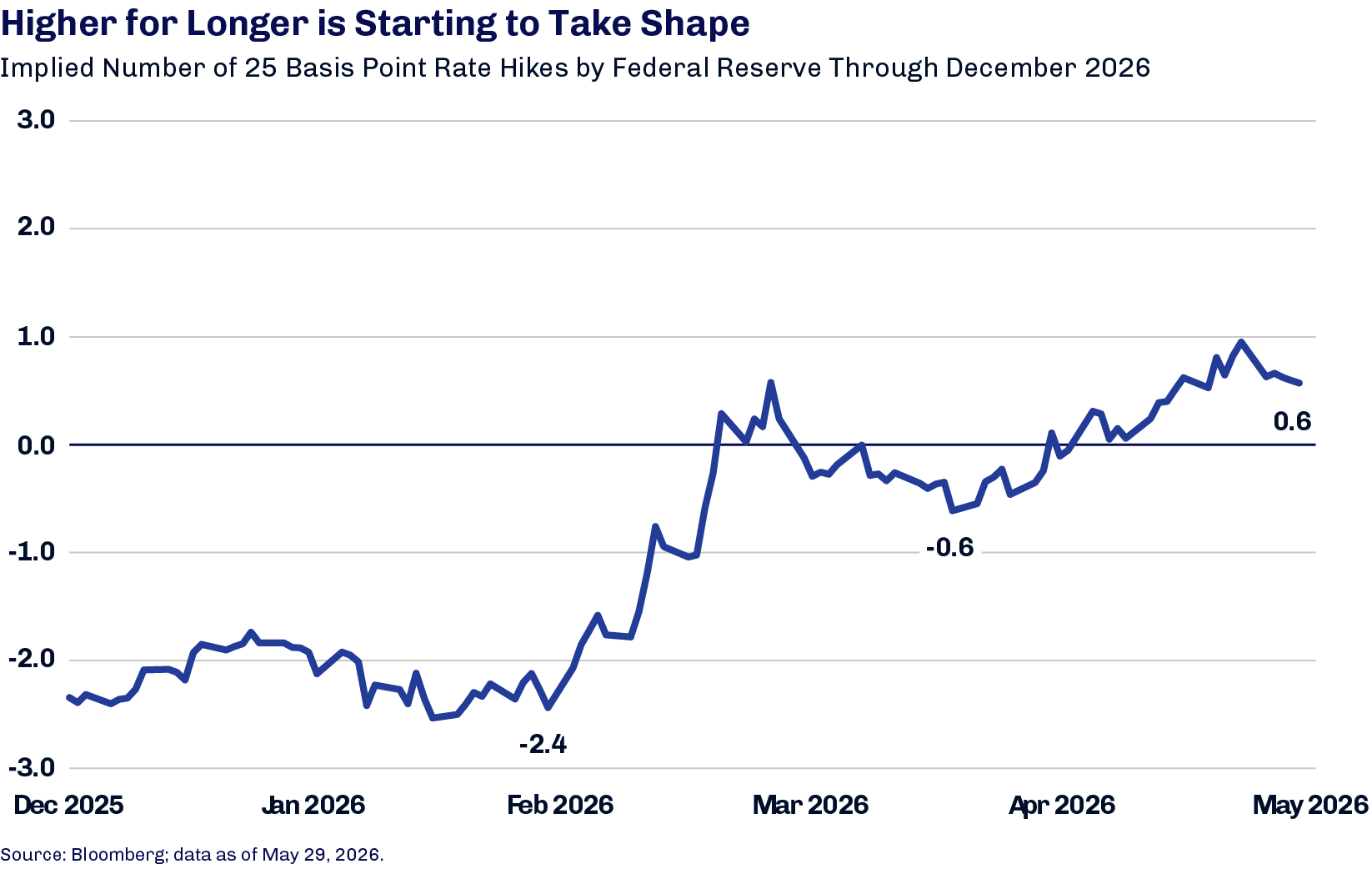

Treasury and rates. Treasury yields were volatile throughout May as markets responded to developments surrounding the Middle East ceasefire and shifting economic data. The labor market showed continued improvement, marking three consecutive months of payroll growth above 100,000 and contributing to higher rates as expectations for a potential year-end rate hike increased.3 Inflation data released on May 12 cast a shadow on interest rate markets, with Treasury yields climbing across the curve on fears that inflation will remain more persistent. After trading between 4.35% and 4.67% during the month, the 10-year Treasury yield declined over the final seven trading days and ended May at 4.45%.4

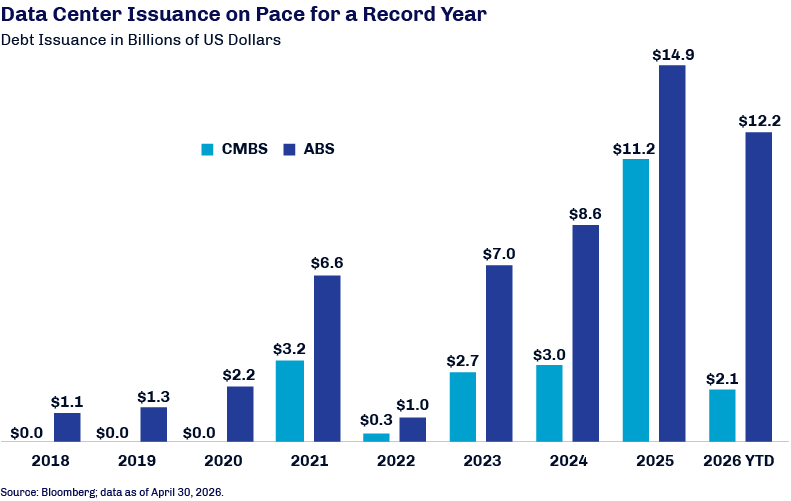

AI’s Securitized Footprint: The Data Center Boom

Portfolio Manager, Diamond Hill Capital Management

Client Portfolio Manager, Diamond Hill Capital Management

Outside of the conflict in the Middle East, few topics have dominated recent market conversations more than artificial intelligence (AI), its potential impact on the global economy and the rapid growth of data-center financing.

Despite concerns around energy use and their impact on surrounding communities, data centers have rapidly expanded across the US as cloud computing and AI continue to drive demand for computing power. For fixed income investors, this growth has created a new category of securitized collateral with distinct structural features and risk considerations.

Data-center asset-backed securities (ABS) typically utilize master trust structures, allowing issuers to add qualifying collateral and issue new note series over time. Cash flows are tied to underlying tenant leases, making retention a key risk, especially when renewals extend beyond anticipated repayment dates. For investors, these securities can offer exposure to a fast-growing economic segment, backed by standard ABS credit enhancements.

Data-center commercial mortgage-backed securities (CMBS) growth has centered on the single-asset single-borrower market, where credit risk is tied to one borrower and one loan backed by a property or portfolio. Today, hyperscaler facilities dominate issuance given their limited tenant volatility.1 Unlike ABS, which is backed by lease cash flows and can add assets over time, CMBS typically relies on a fixed collateral pool and the underlying real estate. These loans generally have a five-year hard maturity, with refinancing driven largely by property valuation. While borrowers cannot prepay on these loans, they can use a process called defeasance, substituting US Treasuries as collateral to replicate the original loan’s remaining cash flows and thus improve credit quality.

While the segment continues to expand, spreads across both the ABS and CMBS markets have remained exceptionally tight alongside increasing demand for AI-linked investment exposure.2