Macro & Market Views

Grace Under Pressure

Grace Under Pressure

Reflections 2025-2026

Though 2025 was not without its ups and downs, the municipal bond market was able to absorb another period of very heavy new supply with relative aplomb. The technical headwinds seen earlier in the year began to dissipate in the second half to reveal what remains a fundamentally solid issuer base, according to John Miller, head and chief investment officer of the Municipal Credit team. Given a highly fragmented market with significant yield dispersion among its constituents, John continues to leverage his team’s many years of underwriting experience to target, among other things, out-of-favor segments with attractive risk-reward profiles.

Drinking from the Fire Hose

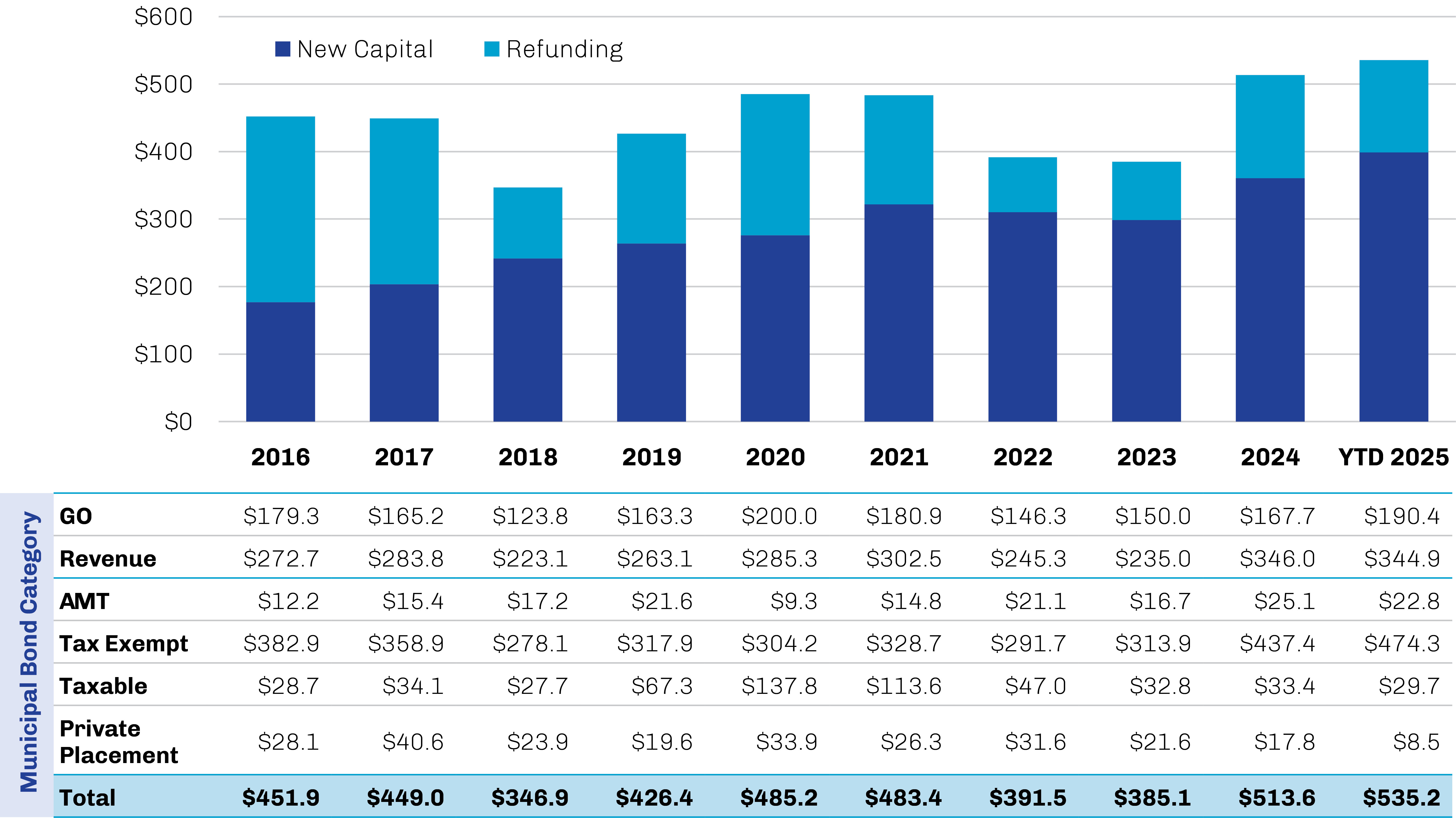

Municipal bond markets saw record new issuance in 2024, and 2025 has already exceeded that high-water mark through November, as shown in Exhibit 1. There are a few factors we believe have contributed to the ongoing surge. After sitting on the sidelines during the 2022–23 rate-hike period, municipalities have a pent-up need to issue paper as the benefits of Covid-19-era federal funding and post-pandemic tax receipts wane. Meanwhile, the cost of capital projects has increased substantially due to inflation across inputs like steel, concrete, lumber, civil engineering, skilled and unskilled labor, and others.

Much of this spending has been concentrated on infrastructure projects, as an estimated 90% of the dollars raised and spent on US infrastructure is financed through municipal bonds.1 Moreover, US infrastructure spending needs are not likely to slow—the American Society of Civil Engineers graded America’s infrastructure a C in its 2025 report card, which was actually a modest improvement from its 2017 grade of D+.2 In our view, the muni bond market is the most efficient source of funding for sorely needed infrastructure projects across the country.

Exhibit 1. Municipal Bonds Set Another Issuance Record in 2025

Annual Issuance in Billions of US Dollars

Note Totals reflect annual issuance aggregated both by bond type (GO and Revenue) and by tax type (AMT, Tax Exempt, Taxable and Private Placement).

Source: SIFMA; data as of November 30, 2025.

Since-dispelled concerns about potential changes to the tax-exempt status of municipal bond interest income may also have prompted issuers to lock in favorable tax treatment ahead of any potential changes. Though the One Big Beautiful Bill Act, as enacted in July, ultimately had no impact on the tax-exempt status of muni bonds, the leadup to the bill’s passage brought with it the usual concerns that adjustments could be afoot. While the issue arises from time to time, the exemption’s broad popularity among voters of all geographies, political orientations and income brackets is likely to limit the potential for future changes or restrictions, in our opinion.

Municipal Fundamentals Remain Healthy

The fiscal conditions of states and municipalities remained strong in 2025, which continued to support issuer fundamentals. State budgets for fiscal 2026 generally reflect a healthy environment, with fund balances well above the historical average.3 Though state general fund revenue has fallen off the record pace of fiscal 2021 and 2022 with the waning of Covid-19-era relief, it has continued to grow, and modest revenue gains are expected in fiscal 2026. Budgets that have been enacted to date call for only small increases in general fund spending.

States are also seeing an increase in tax collection rates across three key revenue components: individual income tax, sales tax and property tax.4 Rainy-day reserve funds continue to be healthy, although they have begun to recede from fiscal 2024 peak levels. At the end of fiscal 2025, state rainy-day funds could cover a median 46.9 days of operations, which was 62% higher compared to fiscal 2019.5

States are seeing an increase in collection rates across income, sales and property taxes.

Another sign of fiscal strength can be found in pension funding, as the aggregate median ratio for local government pensions improved to 80% in fiscal 2024 from 78% in fiscal 2022.6 While this can be attributed in part to financial market appreciation, local governments have increased contributions and tweaked their benefit structures, demonstrating improved funding discipline and better long-term sustainability.

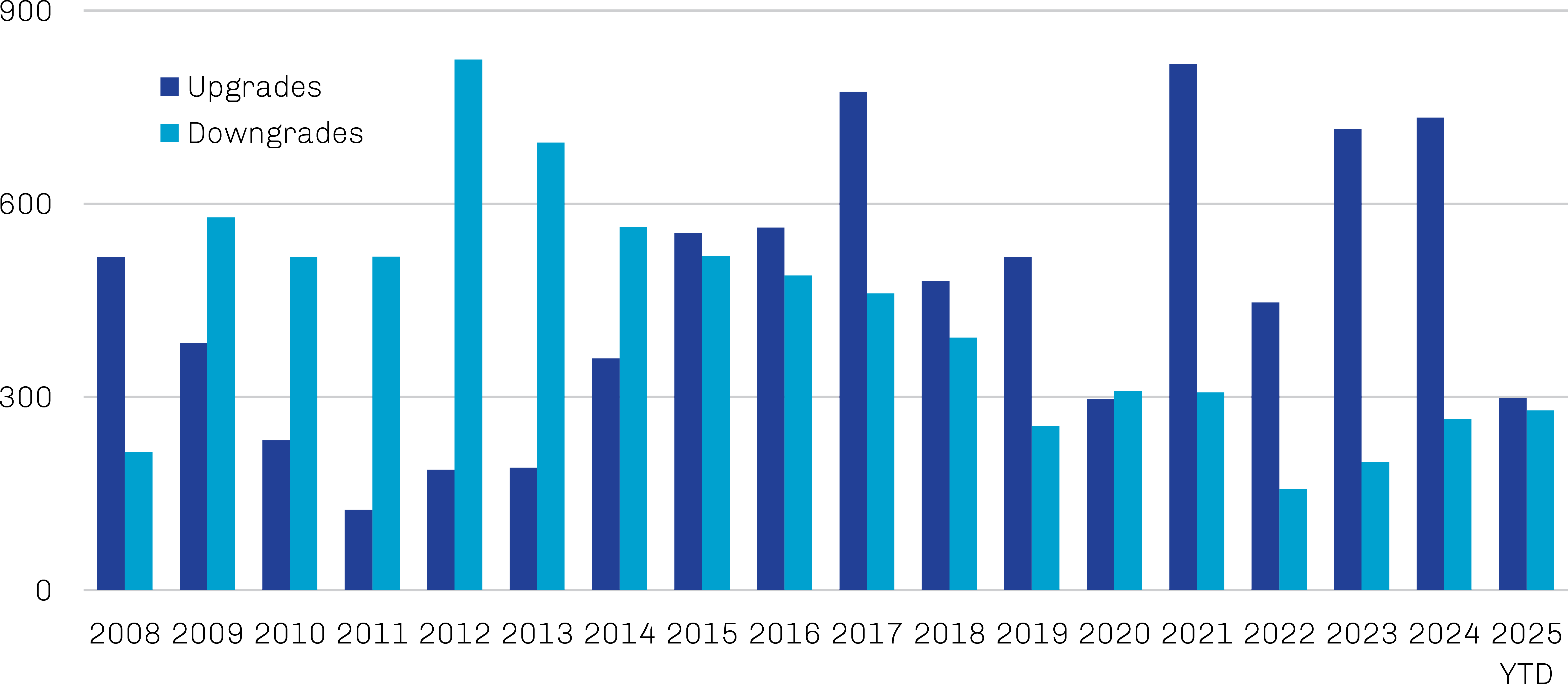

All in all, muni bond ratings activity has continued to be positive in 2025, but just barely. As shown in Exhibit 2, year-to-date positive activity (including both upgrades and favorable outlook revisions) outpaced negative activity at a rate of 1.1x, down from 3.5x in 2022. Defaults remain very low, however, even by the standards of an asset class accustomed to very low default activity.

Exhibit 2. Rating Upgrades Have Continued to Outpace Downgrades

Annual Rating Revisions by Number

Source: Moody’s Investors Service; data as of November 30, 2025.

Technical Headwinds Mask Underlying Strength…

While the muni market was able to absorb much of early 2025’s issuance, it was not immune to the market dislocations caused by the Liberation Day tariffs announcement in early April. Municipal bond mutual funds and exchange-traded funds (ETFs) saw significant outflows as performance sagged, with longer-duration and lower-quality issues particularly challenged.7

These headwinds finally began to ease in the third quarter as investors adjusted to the uncertainty of trade policy. Also supporting demand for muni bonds has been the Fed’s dovish tilt, which began to focus more on softening labor markets and delivered three rate cuts in the fall. Should the Fed’s more accommodative policy weigh on long-term Treasury yields, investors may increasingly view municipal bonds as a more appealing cash equivalent. The Fed ended its quantitative tightening program in December and soon after began buying Treasury bills at a rate of approximately $40 billion per month in what it terms “reserve management purchases.” These actions may provide organic support for improving liquidity as it reinvests the proceeds of maturing Treasuries and agency mortgage-backed securities back into Treasuries.8

The Fed ended its quantitative tightening program in December, which may provide organic support for improving liquidity.

…And Set the Stage for Credit Selection

Although the muni bond market has recovered from the technical headwinds, yields remained attractive relative to their historical averages, as shown in Exhibit 3. While we are constructive on the municipal market as a whole, we believe that current dynamics provide particularly favorable opportunities for managers to uncover attractive opportunities through fundamental, research-driven credit selection.

Exhibit 3. Municipal Yields Remain Higher than the Historical Average

Bloomberg US Municipal Bond Index Yield to Worst

Source: Bloomberg; data as of November 30, 2025.

One area we believe is particularly rich with opportunity is the healthcare sector, which underperformed in 2025. Healthcare began to recover from the dislocations of Covid-19—including deferrals of higher-margin elective procedures, a surge in much less profitable pandemic care and severe wage inflation—in 2023–24, but this rebound proved short-lived. Investors grew concerned about the policy ramifications of Trump’s tax-and-spending bill, including lower reimbursement rates, lower utilization rates and pressure on federal and state aid, as well as the impacts of immigration and tariffs on labor and operating costs.

Cuts to Medicaid and Medicare—which comprise approximately 44% of US hospital spending9— outlined in the bill will total more than $1 trillion through 203410 and are estimated to eliminate healthcare coverage for up to 15 million people.11 Though set to begin in 2026, many of these cuts will ramp up over time, which we believe will give hospitals, healthcare providers and insurance carriers time to adjust their operating models. The delayed nature of the cuts will also give Medicaid and proponents of the Affordable Care Act opportunities to push back or eliminate the implementation of the cuts. Lastly, we believe an aging population in need of chronic disease management and long-term care will further support healthcare utilization.

Many Medicaid and Medicare cuts will ramp up over time, which we believe will give hospitals, healthcare providers and insurance carriers time to adjust their operating models.

Within this sector, we believe that larger, well-managed hospital systems, specialty-care hospitals and hospitals that provide essential care in geographies with population growth and a favorable payer mix are more likely to be resilient in the face of policy changes. These policy changes may also drive consolidation of the hospital space as smaller hospital systems and providers in rural areas seek financial stability and access to capital. By identifying what we view as essential-care providers in larger, well-funded geographies or smaller hospitals that may be well positioned to be acquired by larger providers with a more favorable payer mix, we believe we can identify credits with attractive yields and prices and lower default risk.

We also believe that senior care and senior living is an adjacent sector where fundamental analysis may help identify attractive bonds that stand to benefit from the “silver tsunami” of Americans that will retire by 2030. While this sector has recovered from Covid-19 disruptions, it still accounted for a meaningful portion of the first-time muni defaults in 2025.12 Similar to our security selection process for hospitals, we seek well-managed senior living facilities that are located in growing states and are less dependent on government-subsidized residents.

Seeking Resilience Amid Technical Pressures

We believe municipal bonds are a key pillar of US economic growth and Americans’ quality of life. In our view, the municipal bond market’s ability to absorb a second year of record issuance amid an environment rife with uncertainty, as it did in 2025, reflects underlying strength in issuer fundamentals and the ongoing appeal of these securities to investors. Should longer Treasury yields decline, demand for munis may increase further as investors roll more short-term holdings into fixed rate municipal bonds.

While municipal credit conditions currently remain solid overall—with a low incidence of new defaults, record tax revenue collections and upgrades continuing to outpace downgrades—yields remain attractive. As fundamental managers, we believe that research-driven underwriting can help us identify investment opportunities in out-of-favor areas with wide dispersions in credit spreads, both across sectors and among individual names.