Macro & Market Views

Caution Is the New Conviction

Caution Is the New Conviction

Reflections 2025-2026

Base rates remain compelling, but tight spreads and rising idiosyncratic risk demand discipline. In such an environment, Jon Dorfman, chief investment officer of Napier Park Global Capital, believes caution is warranted across credit markets. As he discusses, the Napier Park team is positioned for volatility, emphasizing selectivity and flexibility to potentially capitalize on opportunities across what for them is a newly expanded investment universe.

Q:

“Bubble-talk is breaking out everywhere,” according to the Financial Times and other observers, noting increased commentary around potential overvaluations across markets.1 Do you share this view?

Jon:

We agree that systemic risks are elevated, and we see clear evidence of late-cycle behavior across markets. Investors continue to reach for yield, driven by elevated base rates that have boosted income potential, even as spreads sit at multidecade lows and idiosyncratic risks rise. This paradox of high base rates alongside compressed spreads reinforces our conviction that caution, not complacency, is the right approach. We believe attractive all-in yields exist, but they require disciplined selection and a focus on structures with strong downside mitigation with the goal of avoiding the pitfalls of late-cycle excess.

The paradox of high base rates alongside compressed spreads reinforces our conviction that now is the time for caution.

Are certain segments in a bubble? We see signs of reduced discipline and unjustified pricing in pockets of the market, but not systemically—at least not yet. If these trends persist and broaden, the risk of a more widespread bubble could become significant.

Q:

What have you seen this year within structured credit specifically?

Jon:

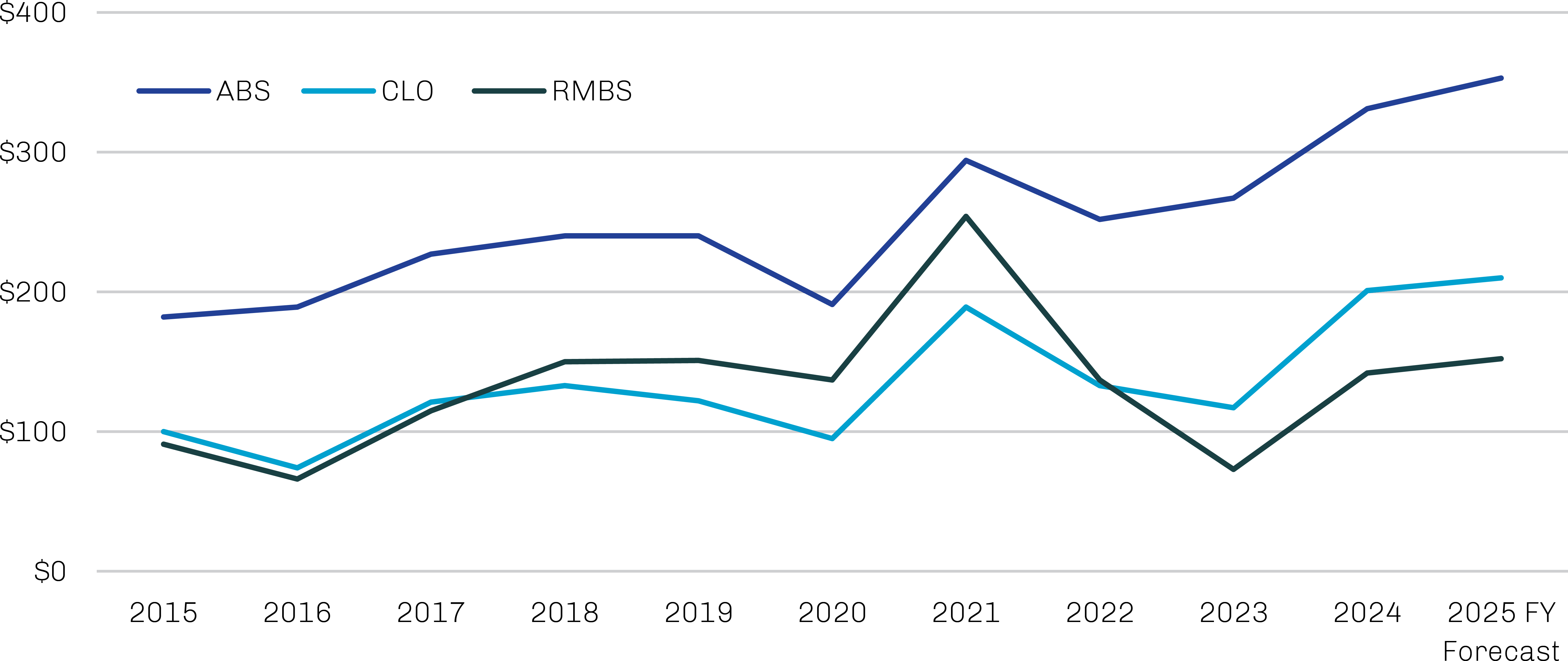

Structured credit markets in 2025 have been defined by strong demand for yield-oriented assets, and issuance has surged in response. As shown in Exhibit 1, issuance of both collateralized loan obligations (CLOs) and asset-backed securities (ABS) are on pace for new annual highs, while residential mortgage-backed securities (RMBS) volumes are also elevated, if below peak levels.

Exhibit 1. Structured Credit Supply Remains Robust

Annual Gross Supply in Billions of US Dollars

Source: Citi; data as of September 30, 2025. Figures and projections are estimates only. Due to various risks and uncertainties, actual results may differ materially.

Despite strong demand, spreads have not broadly tightened across the structured credit universe. Instead, we’ve seen meaningful dispersion, with a clear flight to quality and a reduction in demand within more credit-intensive sectors.2 This dynamic highlights the importance of disciplined underwriting and structural protections as the cycle matures. As a result, careful underwriting remains paramount to identifying selective pockets of opportunity and reducing the risk of late-cycle excess.

In addition, our work within specialty private credit— focused on residential real estate and other niche lending segments—continues to uncover a deep and diversified opportunity set. These areas often feature amortizing exposures, moderate duration profiles and embedded structural protections, which together are designed to support compelling, risk-adjusted returns.

Our work within specialty private credit continues to uncover a deep and diversified opportunity set.

It remains difficult to call a floor for credit spreads. In our view, the still-growing US economy and healthy corporate earnings have provided near-term support, but elevated base rates and tighter financial conditions are gradually eroding risk appetites. Importantly, on-the-run, liquid noninvestment grade credit exhibits a negatively convex return profile heading into 2026, given par-based valuations and limited room for further spread compression.3 This reinforces our view that caution is the prudent stance at this stage of the cycle.

While unemployment has edged higher, the labor market remains broadly healthy, suggesting a gradual cooling rather than a sharp downturn.4 Beneath the surface, however, conditions are becoming more uneven, with certain sectors and borrower segments showing early signs of strain. For now, strong technical demand and ample liquidity continue to provide support across markets.

Q:

How do you identify end-cycle behavior in credit markets?

Jon:

We monitor three key indicators across the broader credit universe: underwriting standards, leverage and fundamentals. Heading into year-end, these signals are mixed.

Underwriting standards have clearly deteriorated in parts of the private credit market. We are seeing increased lending to middle market borrowers that either feature weaker or no covenant protections or have yet to demonstrate sustained positive free cash flow—two separate but important signs of late-cycle behavior. These trends are less prevalent in the lower middle market, where transactions typically involve closer lender engagement, stronger structural protections and more conservative underwriting, and these areas remain central to our focus. We have also seen a rise in transactions with payment-in-kind (PIK) interest, allowing borrowers to roll accrued interest into principal rather than paying cash. Additionally, there’s been an increase in limited-transparency structures, such as forward-flow transactions, blind pools and deals completed without loan-level data.

Leverage tells a different story. We haven’t seen broad-based re-leveraging in structured credit, as managers appear to have learned from the Covid-19 era when mismatched vehicles suffered losses and redemptions. However, we have observed some newer strategies—particularly leveraged long/short or “liquid alternatives”— are running with high betas and thin liquidity buffers, characteristics that could prove problematic if aggregate liquidity begins to recede.

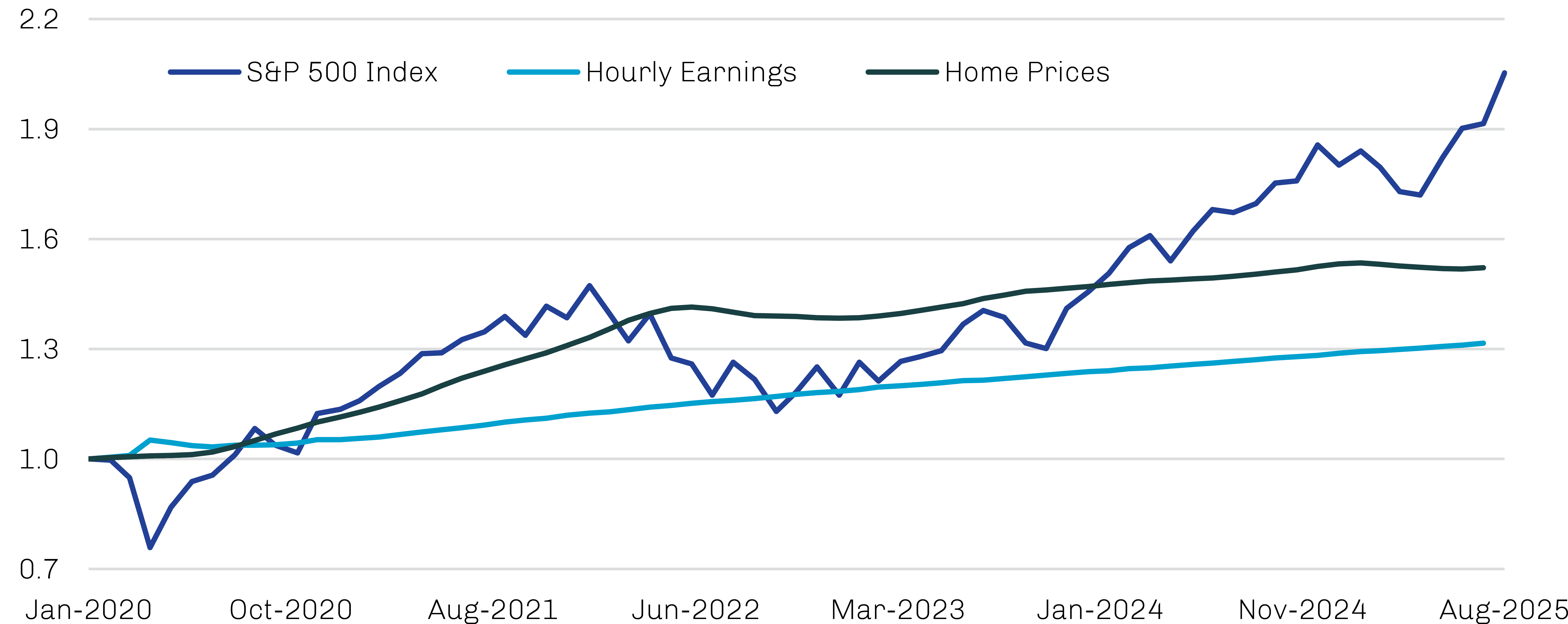

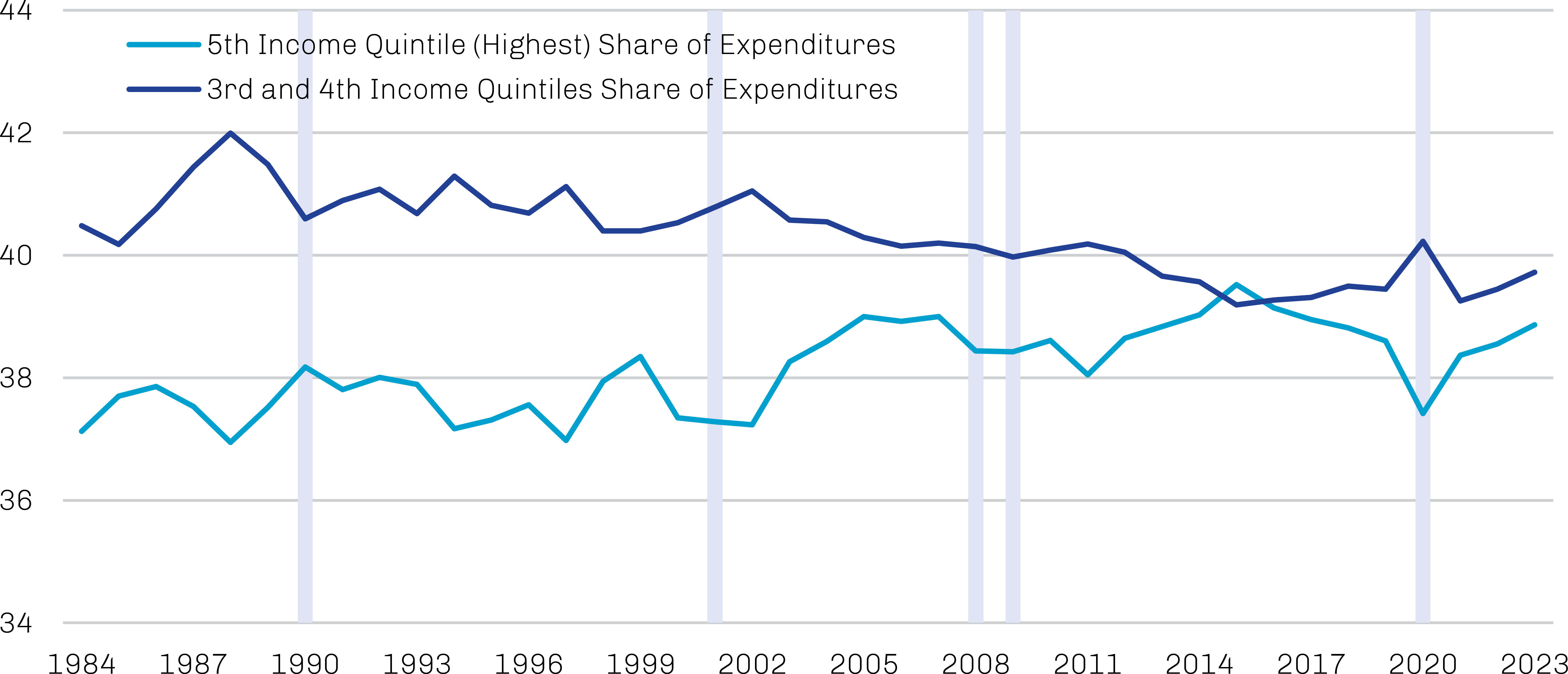

Fundamentals, meanwhile, show growing bifurcation. Higher-income households remain resilient, supported by gains in equity and housing markets, while lower-income households continue to face pressure from high borrowing costs, elevated rents and persistent inflation. The result is a consumer economy that looks strong on the surface but is increasingly reliant on affluent cohorts to sustain demand. As shown in Exhibits 2 and 3, asset appreciation has far outpaced wage growth in the US, and the share of spending driven by the top 20% of households has continued to rise. Both are hallmarks of late-cycle divergence.

Fundamentals show growing bifurcation.

Exhibit 2. Higher-Income Households Have Seen Greater Asset Gains…

Index: January 2020 = 1

Source: Bloomberg; data as of November 12, 2025.

Exhibit 3. …and Have Been Responsible for a Greater Share of Spending

Share of Expenditures by Income

Source: Consumer Expenditure Survey, Haver Analytics, Deutsche Bank; data as of October 30, 2025.

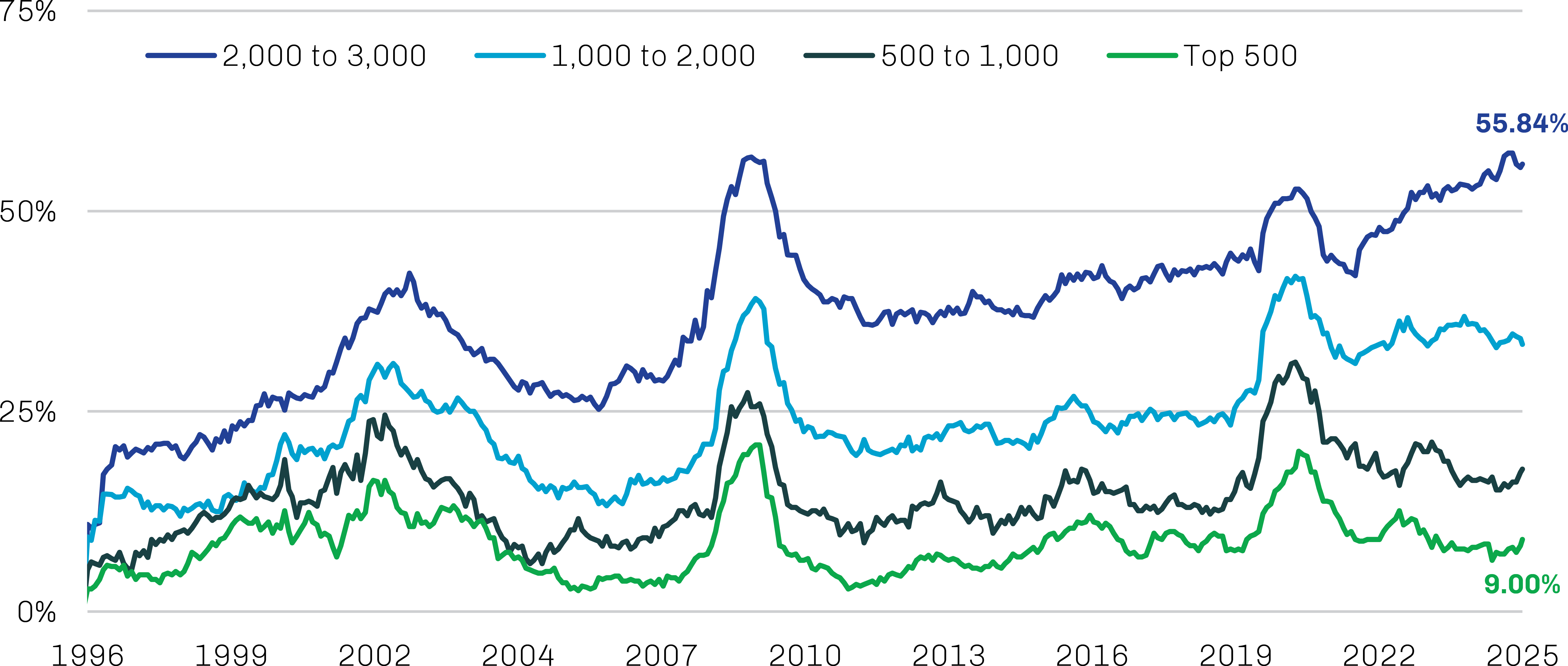

On the corporate side, fundamentals tell a similar story. Larger issuers generally maintain solid balance sheets and access to capital markets, but smaller firms are under mounting strain, as shown in Exhibit 4. The percentage of unprofitable companies among the smallest US public issuers is approaching record levels, underscoring the uneven distribution of earnings strength within the corporate sector. This widening gap between large and small firms mirrors the divergence seen among consumers and often emerges late in the cycle.

An uneven distribution of corporate earnings strength often emerges late in the cycle.

Exhibit 4. Earnings and Balance Sheet Strength Are Concentrated in Larger Issuers

Percentage of Unprofitable Companies by Size Cohort

Source: S&P Global, BCA Equity Analyzer; data as of October 15, 2025.

Q:

How are you positioned in light of these complexities?

Jon:

Today’s credit markets—marked by abundant liquidity, compressed spreads and the proliferation of more accessible investment vehicles—evoke memories of previous late-cycle periods. While these dynamics have buoyed asset prices, they also reflect a growing imbalance between perceived liquidity and underlying fundamentals. History reminds us that this illusion can fade quickly when the cycle turns.

Napier Park’s posture is purposefully different. We continue to avoid leverage, emphasizing relative value, hedged positioning and embedded structural protection. Our credit derivatives strategies remain among our largest allocations, providing flexibility to potentially capture spread and volatility mispricing while maintaining strong downside mitigation through systematic hedging. This disciplined approach—minimal leverage, limited beta exposure and targeting convexity where it still exists—has allowed us to navigate rising dispersion and focus on protecting capital as late-cycle dynamics have intensified.

Our portfolios remain deliberately conservative, preserving both optionality and the capacity to act opportunistically. We are prepared to scale risk when valuations normalize, supported by significant dry powder within our money-in-the-ground investment vehicles and in contingent capital structures designed to deploy quickly in the event of a market dislocation.

As we look ahead, we believe that preserving convexity and optionality is far more valuable than maximizing short-term return. When spreads are trending toward their tights in certain areas, patience truly pays most. And with the recent integration of First Eagle Alternative Credit (FEAC), Napier Park now may benefit from a broader investment universe and enhanced flexibility to capitalize on opportunities as market conditions evolve.

Q:

Tell us more about the integration of Napier Park and FEAC and how the combined platform will operate moving forward.

Jon:

In September 2025, we brought together First Eagle’s two alternative credit businesses under the Napier Park brand and management, creating a single, unified platform. This integration combines FEAC’s direct lending and asset-based lending capabilities with Napier Park’s expertise in opportunistic credit, structured products and real-asset leasing. The result is a global credit platform with approximately $42 billion in assets under management.5

The integration of FEAC and Napier Park results in a global platform able to serve clients across the full spectrum of alternative credit.

The combined business is organized around six core areas: US structured products, global credit derivatives, European structured products, asset-backed securities and asset-based lending, lower middle market direct lending and real-asset leasing. This breadth gives us the ability to serve clients across the full spectrum of alternative credit, from liquid markets to private transactions.

It’s not just scale that makes this integration meaningful—it’s the depth of expertise and flexibility it brings. Our teams share a common philosophy: focus on markets where capital is scarce and complexity creates opportunity while leveraging disciplined underwriting to deliver durable returns. By uniting these capabilities on a single platform, we can offer clients a more holistic approach to credit investing, with the agility to pivot as market conditions evolve.