BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

The New Normal: AI Growth in an Inflationary World

Portfolio Manager and Senior Research Analyst

As the war with Iran enters its fourth month, financial conditions have largely adjusted back to pre-war conditions, but the stagflationary impulse still threatens the global economy. Although Brent crude prices have eased approximately 20% off their peak, the Strait of Hormuz remains closed.1 While most governments have taken measures to mitigate the impact of higher energy prices on households and businesses, we have already begun to see early indicators of demand destruction in emerging economies that are heavily reliant on imported energy from the Middle East.2

Meanwhile, the boon in capital expenditures for artificial intelligence (AI)-related infrastructure has buoyed growth in the US and in select economies in Asia, most notably Korea and Taiwan, where surging technology exports have offset the impacts of energy shocks.3 While the US is not reliant on energy imports, higher energy prices have exacerbated the risk of higher core prices from tariffs and the impact of immigration policy on wage inflation.4

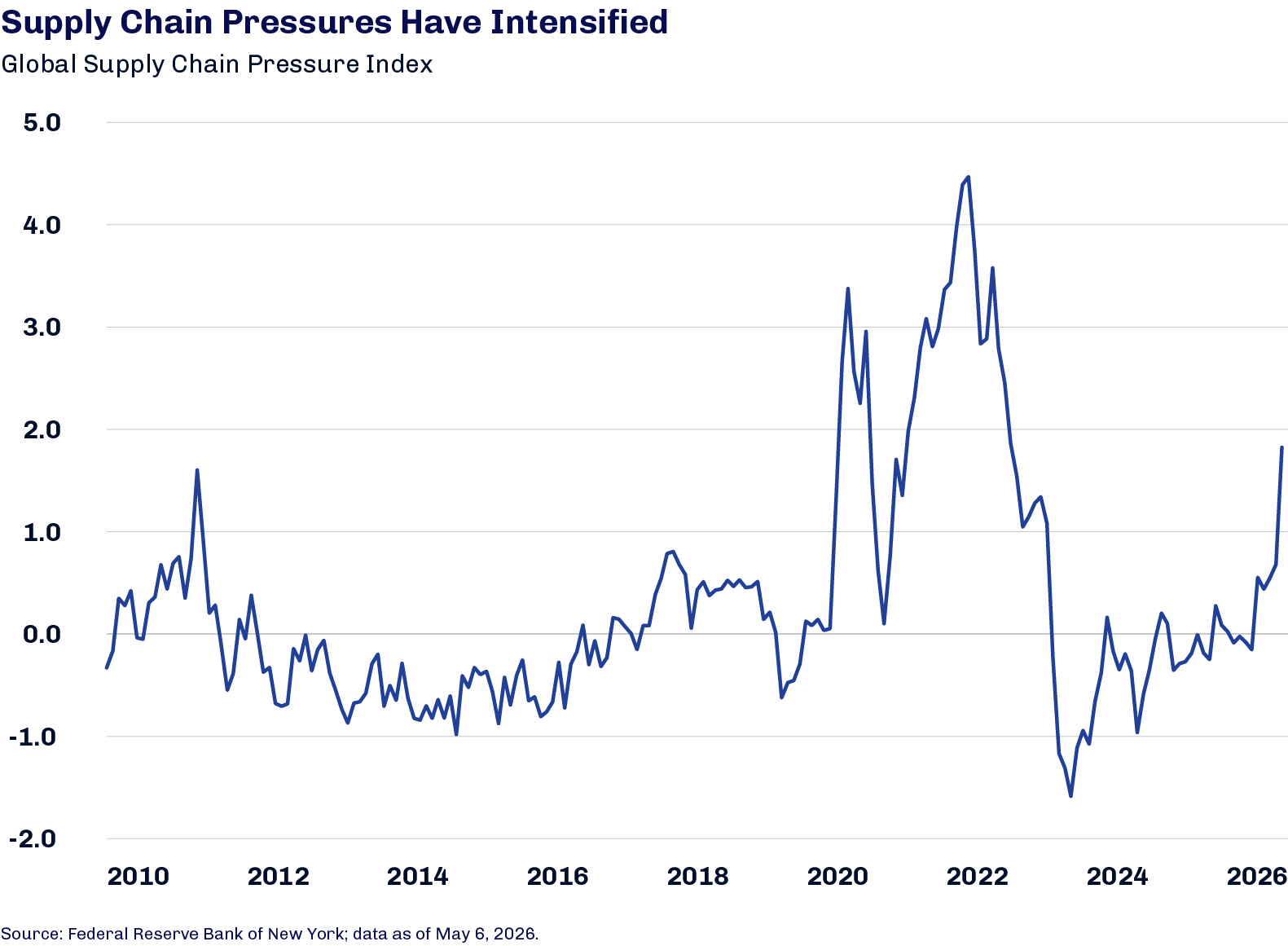

Input and output prices have been increasing as supply chain pressures have intensified worldwide.5 Some economies have begun to tighten monetary policy, and it’s likely more central banks will begin to raise rates in the coming months.

The duration of the current ceasefire remains unclear, as does the question of who will control the flow of traffic through the Strait of Hormuz over the long term. We continue to believe that supply conditions will not immediately return to normal upon the Strait’s eventual reopening, as the need to replenish oil stocks and repair damaged infrastructure will support still-elevated energy prices. In the face of this “new normal,” we believe that assets with the potential to participate in this inflationary dynamic are well positioned to demonstrate resilience across multiple states of the world.

US Consumers: Headline Strength, Hidden Strain

Portfolio Manager, Diamond Hill Capital Management

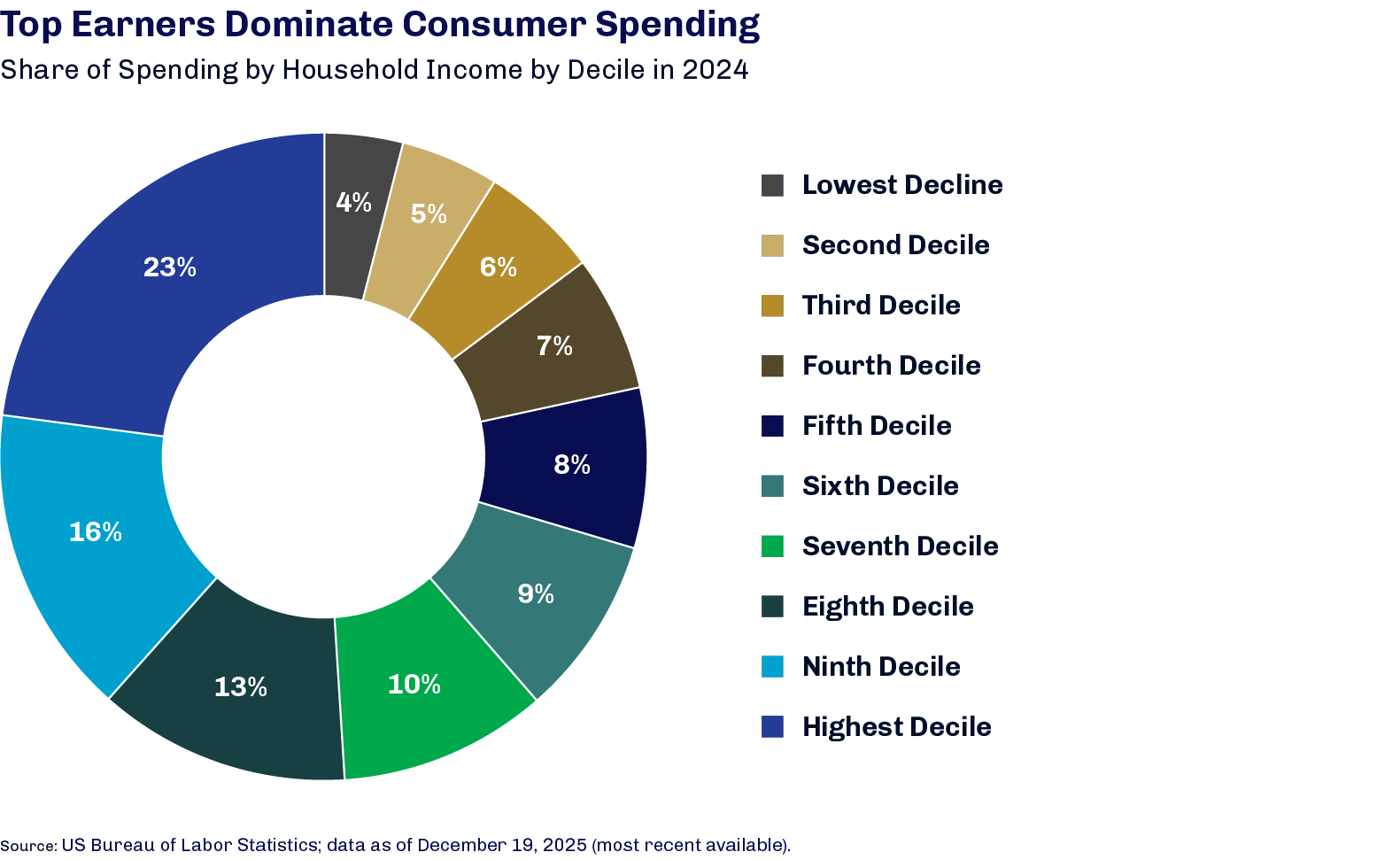

Consumer demand has held up better than many expected in the face of stubborn inflation, a cooling labor market, ongoing tariff uncertainty and war in the Middle East. While the high-level data still support the case for a healthy consumer environment, a closer look suggests an increasingly bifurcated economy. As shown below, the top-earning 30% of households account for over 50% of total consumer spending while the bottom 50% account for less than 30% of spending. In other words, many consumers are far more financially constrained than the headline numbers imply.1

Bond investors can gain exposure to the strongest consumers through high-quality credit card issuers and prime loan structures, but these higher-quality areas often don’t offer much incremental compensation. More attractive yield can be found further down the credit spectrum into near-prime and subprime borrowers, but performance can deteriorate quickly if the economy weakens.

We believe the tradeoff between yield and stability is where strong, bottom-up credit analysis becomes crucial. Today, data indicate early signs of consumer stress, including a modest uptick in delinquencies even within prime cohorts.2 While it’s too soon to know whether that’s simply noise or the beginning of a broader trend, caution seems warranted.

The current environment suggests to us that the potential for losses has increased, highlighting the importance of credit investments that can remain resilient if economic conditions deteriorate. This means higher-quality tranches within consumer credit, for example, and a higher bar for investing in subprime opportunities. Issuer selection also remains key. Strong, proven issuers—particularly those with durable funding structures—are more likely to operate without disruption in tighter markets and therefore are less likely to create servicing transfer risk in a downturn.