Macro & Market Views

Everything Old Is New Again

Everything Old Is New Again

Reflections 2025-2026

Observing the current mania for private assets, Bill Hench, head of the Small Cap team, reflects on why he believes investment fundamentals ultimately trump vehicle structure. While private equity investments benefited from a number of tailwinds coming out of the global financial crisis, Bill thinks the winds may be shifting in favor of quality, publicly listed smaller companies. The potential reversion to the long-term mean could be powerful.

Illiquidity Is the “New New Thing” for Investors…

Oh, for the good old days when fundamentals were king.

Back when I was a lad coming up through the ranks, liquidity—and its corollary, price discovery—were prized investment features. Active trading with real-time marks to market—and the concomitant quick escape hatch, if desired—were generally valued by investors.

Since the global financial crisis, however, heads have been turned by eye-popping returns generated in private equity. Underpinned by belief that the real money is made before a company goes public—and only for those with privileged access, such as institutions and family offices—the proverbial everyman has been clamoring for access to private alternatives. Heeding the cry—and following an executive order issued by President Trump—the US Department of Labor in August paved the way for inclusion of alts in retirement plans by removing 2021 guidelines discouraging private investments, with plan sponsors maintaining their fiduciary responsibility to identify suitable investments.1

With pre-public access the current rage, menus of new private alts have proliferated, with themed offerings in artificial intelligence (AI), data centers and infrastructure. Charles Schwab has announced the purchase of Forge Global Holdings to provide its retail clients with access to shares in companies before they go public. Interval funds and business development companies have become popular vehicles through which managers may provide investors liquidity in assets that are inherently illiquid.2

Lucrative returns in some private assets may reflect the zero interest rates that prevailed when these investments were made.

While it’s tempting to attribute lucrative returns to sponsor acumen and/or to the private vehicle structure itself, it seems to us that most of the kudos should go to the zero interest rates that prevailed when these investments were made. The ample capital readily available in the years following the global financial crisis and resulting low hurdle rates enabled private equity sponsors to acquire young and/or broken businesses, nurture them to some semblance of maturity, and then monetize their investments through sale to a strategic or financial buyer or to the public through initial public offerings (IPOs). Since the interest rate environment shifted higher in 2022, the cost of acquiring and building businesses has increased, as have the financing costs and return targets for subsequent buyers.

…but It Comes at a Cost

While a long lockup period—that is, structural illiquidity—has been characteristic of private investment vehicles, it does not in and of itself contribute to investment success. The fundamental qualities of an investment—private or public—ultimately underpin its returns.

Moreover, illiquidity can convey a false sense of security. Scrutiny of an investment may be less stringent without daily marks to market, and the rapid deterioration of a business can take investors unaware. For example, the September 2025 bankruptcies of subprime auto lender Tricolor Holdings and auto parts supplier First Brands Group—alongside allegations of fraud—surprised bankers and syndicated loan investors alike.3 A similar unraveling was seen at home-improvement rollup Renovo Home Partners, whose debt was marked down by its largest lender from par to zero in only a few weeks.4 While these occurrences have been characterized as idiosyncratic, for now, more systemic risk may become apparent over time.

Vintage matters. We would be surprised if the returns realized on private investments entered into today—given a meaningful cost of capital, higher hurdle rates and longer holding periods—kept pace with those made between the global financial crisis and rate tightening in 2022. With exit paths and big gains harder to come by, we expect the lure of privates—and illiquid assets—may ease within the general investing populace.

Liquidity may be most important when it’s least accessible. Should private equity sponsors eventually be laden with investments they can’t monetize, redemption gates likely will go down, leaving investors barred from the exits. As the pendulum swings from one extreme to the other, liquidity may reemerge as the old, and more desirable, new thing.

Liquidity may be most important when it's least accessible.

Fundamentals Remain Our Lodestar

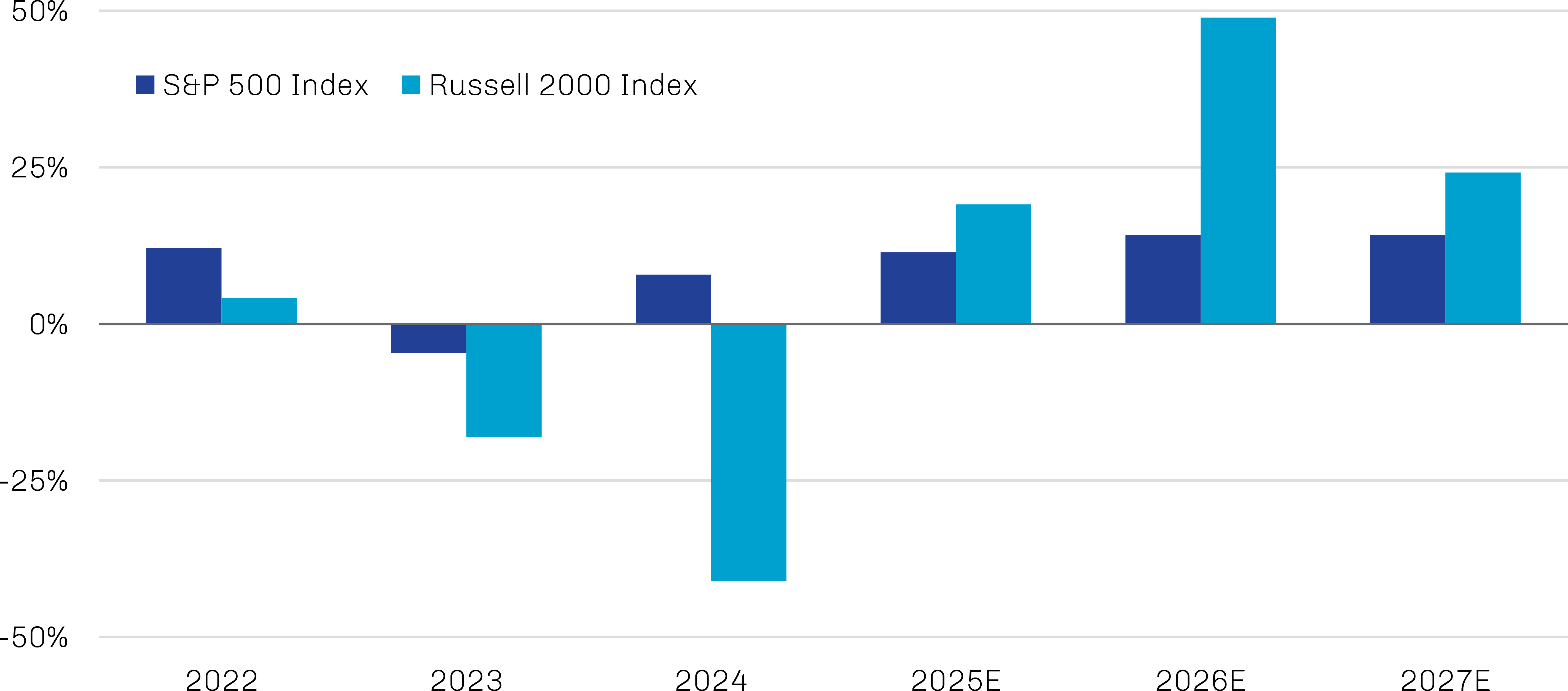

As fundamental investors, we continue to believe that underappreciated earnings potential is the true holy grail and has historically been rewarded in the marketplace. For the past three years, small cap earnings have been overshadowed by those generated by S&P 500 companies—especially the Magnificent Seven—which also were able to sidestep such small cap challenges as access to capital and management depth. But there are signs that a recovery in small cap earnings may at last be underway.

As shown in Exhibit 1, earnings for the Russell 2000 Index are forecast to outpace those of the S&P 500 Index through at least 2027. Even without multiple expansion, earnings growth alone can propel small cap performance.

Exhibit 1. Small Company Earnings May Be on the Upswing

Actual and Estimated Earnings Growth, Year-over-Year Percent Change

Source: LSEG I/B/E/S; data as of November 30, 2025.

Further, we see multiple paths to success for small cap businesses. Among the most compelling potential earnings drivers are:

Technology-driven growth. Outsourced software and servicing, broadly, may provide resources that enable small companies to scale their operations, improve efficiency and facilitate the conversion of some costs from fixed to variable, easing the need for working capital.

More specifically, AI may benefit small cap companies over a very long cycle. Pick-and-shovel suppliers to infrastructure and data center construction, for instance, can expand their customer base without triggering incremental spending on research and development (R&D), thus supporting margin expansion. These suppliers may include providers of cable, rebar, HVAC systems and components of energy systems like gas turbines. Healthcare and consumer goods companies could conceivably see even greater benefits from AI. In addition to reduced spending on R&D and selling, general and administrative expenses (SG&A), AI may also enhance development of superior products to drive pricing power.

Supportive trade and monetary policy.

Prospective policy developments and lower interest rates could also bolster small cap earnings. Although the domestic orientation of many smaller companies has provided some insulation against tariffs, additional relief on this front may come from the Supreme Court as it considers Trump’s ability to impose tariffs under the International Emergency Economic Powers Act. While it’s possible the administration would seek other legal statutes to reimpose tariffs were they removed, it’s also possible that Trump could point to several trillion dollars of investment promised from abroad and declare victory in the trade war, potentially easing inflation ahead of the November 2026 midterm elections.5 This may also clear the way for additional rate cuts by the Federal Reserve on top of the 75 basis points of cuts since September. Reduced inflation and lower interest rates could further benefit small companies, which still often carry substantial levels of variable-rate debt.

Lower interest rates could benefit small companies, which often carry substantial levels of variable-rate debt.

A resurgent IPO market. We anticipate the IPO market to continue reopening, to the potential benefit of small cap companies. With free money a thing of the past and meaningful hurdle rates, private equity sponsors are incentivized to monetize their investments through the public market, even if they are unable to realize previously hoped-for returns. As discussed earlier, the days of extended holding periods facilitated by zero funding costs appear to be behind us.

The Past Decade Has Generally Favored Larger Stocks

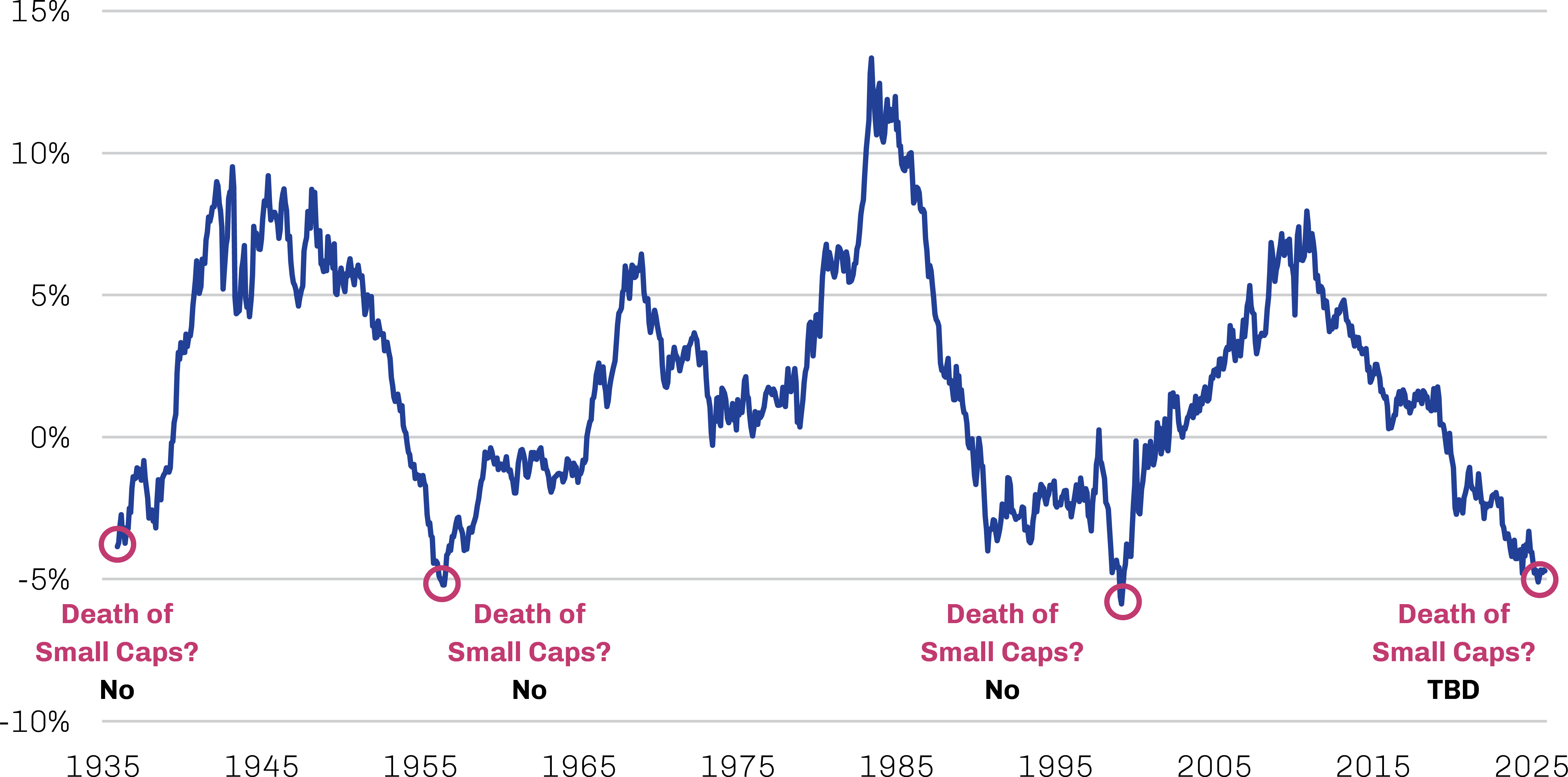

The 39.3% rally in the Russell 2000 Index from its post-Liberation Day swoon through the end of November outpaced the S&P 500 by nearly 300 basis points and reminded us that the small cap beast still has claws.6 Despite this recent show of strength, longer-term performance trends remain skewed toward large names. As shown in Exhibit 2, the relative performance of small caps remains near previous cyclical troughs. Respecting the tendency for reversion to the mean, our confidence in eventual strong sustained returns from small caps—driven by fundamentals— remains firm.

The strong rally following the Liberation Day swoon reminded us that the small cap beast still has claws.

Exhibit 2. Small Cap Returns May Be Near an Inflection Point

Relative Trailing 10 Year Annualized Returns, Russell 2000 Index Less S&P 500 Index

Source: Furey Research Partners, FactSet; data as of November 30, 2025.

Recall that small caps historically have been the most rewarding tradable segment of the market over the long term.7 While the volatility inherent to the asset class can sometimes be unnerving in the short term, it often provides opportunity to buy what we perceive as good companies at attractive valuations.