Macro & Market Views

The Tide Is High

The Tide Is High

Reflections 2024-2025

While the underperformance of small cap stocks relative to larger names over the past decade-plus has been disappointing, a range of factors may be coalescing to ease what has been a key breakwater for the market segment: middling bottom-line growth. Bill Hench, head of the Small Cap team, ponders the forces that in the years ahead could unleash a wave of earnings growth, including lower interest rates, a more benign regulatory environment and reenergized mergers and acquisitions and capital markets activity.

Growth Has Been Elusive, but Change May Be Afoot

Given the increasing number of money-losing small cap companies since the global financial crisis— 45% of the Russell 2000 Index lost money on a trailing-12-month basis through the end of the third quarter—lackluster earnings at the benchmark for relative under-performance as market capitalization preferences.1 However, there are reasons to believe resuscitated earnings may finally be in prospect for 2025 as accelerating top-line growth and continued margin improvements filter through to the bottom line, as shown in Exhibit 1 and Exhibit 2. As we discuss below, multiple forces at the industry level could amplify company-specific earnings momentum.

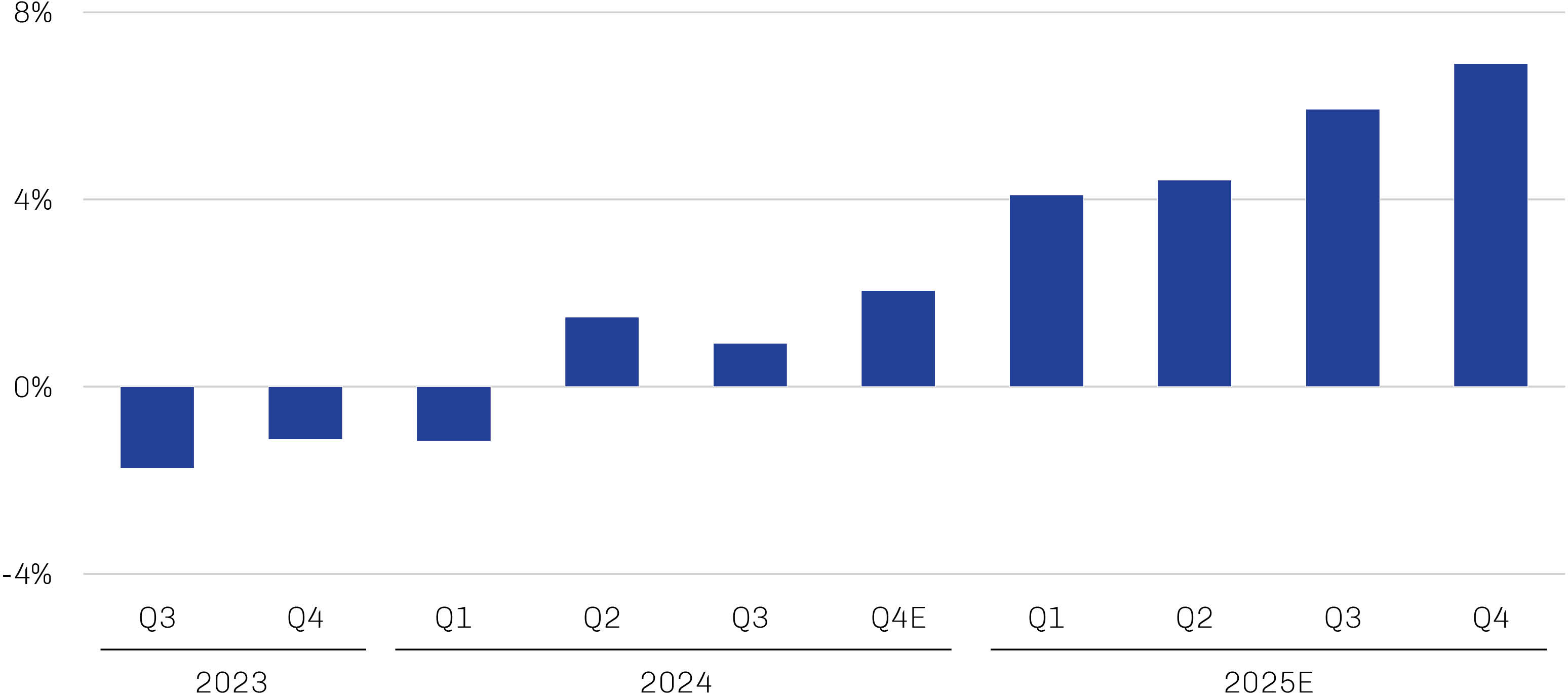

Exhibit 1. Sales Growth Is Forecast to Accelerate in 2025…

Realized and Estimated Russell 2000 Index Year-Over-Year Sales Growth, Third Quarter 2023 through Fourth Quarter 2025

Source. Furey Research Partners, FactSet; data as of November 14, 2024.

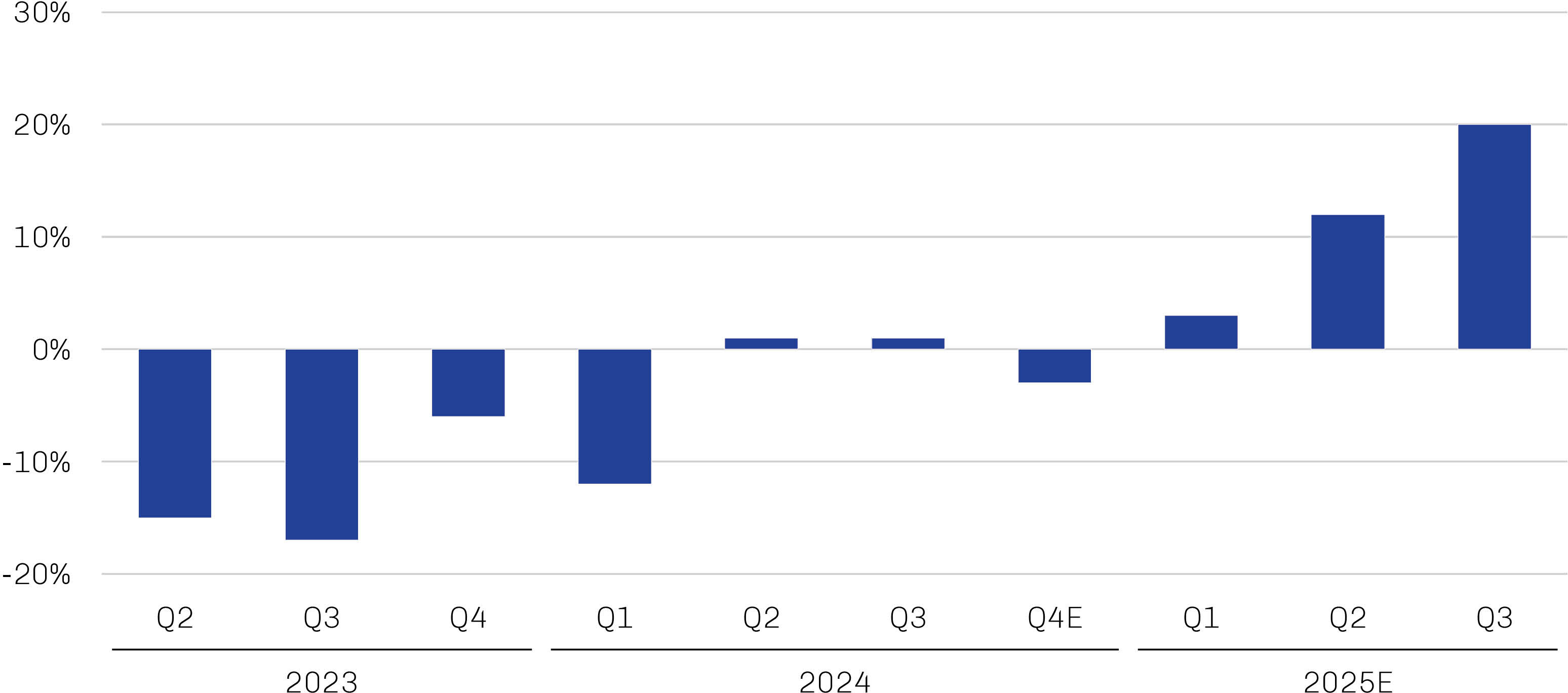

Exhibit 2 …Boosting Margins and Earnings Growth

Realized and Estimated Russell 2000 Index Year-Over-Year Earnings Growth, Second Quarter 2023 through Third Quarter 2025

Source: Furey Research Partners, FactSet; data as of November 14, 2024.

As small caps overall are more leveraged to floating-rate debt than larger companies, further Federal Reserve policy easing beyond the 100 basis points worth of rate cuts in 2024 would have a meaningfully positive incremental impact on these businesses’ interest expenses. While we won’t hazard a guess at the trajectory of Fed policy going forward, the latest dot plot Federal Open Market Committee forecasts suggest an additional 50 basis points of cuts are on tap in 2025.2 A reduced cost of capital across the US economy—for both consumers and levered small cap companies—could trigger a resurgence in small cap stocks, especially those in the housing, consumer discretionary and energy sectors. In addition to reducing borrowing costs and buoying economic activity, lower rates historically have lured investment capital in from the sidelines, propelling small caps higher.3

Even without further rate relief, however, small cap balance sheets are the strongest they’ve been since the global financial crisis, in our view. Improved supply-chain management post-Covid has helped managers rationalize inventories and reduce working capital. Some companies have been able to leverage the proliferation of cloud applications to reduce the capital intensity of their businesses and improve operating leverage; specifically, what had been large, fixed-hardware infrastructure investments financed through capital expenditures become variable operational costs.

Policy Changes and Regulatory Reform May Have an Outsized Impact on Smaller Companies

In addition to wider operating margins, strengthened balance sheets and potentially lower rates, prospective policy changes and easier regulations facilitated by the 2024 Republican sweep of the November US elections could serve as an additional tailwind to earnings growth for US-domiciled companies. This could be especially true for smaller companies, in our view. Not only do large companies have the scale to monitor and adapt to regulatory changes, their lobbying muscle often enables them to influence regulations at the design stage to their benefit. Smaller companies, in contrast, usually are left to “play it as it lays” and bear the fixed costs of compliance over a smaller base. A less restrictive regulatory environment may have an amplified salutary impact on small companies.

Tariffs. Given that we already operate in a trade-protected world, the impact of any new tariffs will be incremental rather than de novo, potentially limiting their overall effect. That said, any redomestication of manufacturing would likely benefit US-centric producers, including the small cap companies that in the aggregate source about 90% of revenue from home.4

Taxes. While many of the provisions of the Tax Cuts and Jobs Act of 2017 affecting individual taxpayers are set to expire at the end of 2025 barring Congressional intervention—which seems likely given the results of the US election—changes to the corporate tax code were made permanent at the time of the bill’s passage. That said, Trump on the campaign trail proposed further easing of corporate taxes, including lowering them to 15% for domestic production.5 As corporate taxes tend to be regressive, US-focused small cap companies may be particularly well positioned for tax savings that could be redirected to reducing fixed costs and thus enhancing margins and productivity.

Regulations. As president, Trump reportedly is prepared to nullify “thousands” of rules and regulations he and his team deem to represent executive overreach.6 Generally speaking, such a dismantling of the regulatory state would reduce outlays on compliance—with consumer protection laws, for example, or environmental requirements— and thus operating costs, boosting margins and profitability. Meanwhile, looser antitrust provisions could unleash a spate of mergers and acquisitions (M&A), potentially triggering buyout premiums for targeted small cap companies.

Enhanced Efficiency/Reduced Government Spending. Improved efficiency and the elimination of unnecessary federal expenditures could reduce government spending and Treasury issuance, enabling assets that would otherwise be invested in government debt to be put to better use in the private sector. That said, discretionary nondefense spending represents only about 15% of total federal outlays; efforts to rein in government spending without reform to popular and politically untouchable entitlements like Social Security, Medicare and Medicaid seem unlikely to have a meaningful impact on the country’s fiscal trajectory.7

Industry-Specific Trends Could Lift a Narrower Swath of Small Cap Companies

Beyond the potentially broad sweep of policy changes under the new administration, industry-specific developments could benefit a more focused range of small cap companies.

Artificial Intelligence (AI). AI could be even more meaningful over a long cycle than the dawn of the internet was in 2000, transforming companies across industries and capitalizations into more efficient digital- and data-driven operations, resulting in reduced costs and faster innovation. Sectors already deep in the digital space like finance, healthcare and logistics could be especially well positioned to benefit from emerging technologies. Additionally, much as the telcos had early-mover advantage into broadband communications in the 1980s, many smaller companies may be able to tweak their business models for relevance in a new AI-driven world rather than embark upon a whole-scale reinvention. For example, one small cap manufacturer in the Midwest has leveraged its century-plus of expertise in thermal management for trucks and tractors to produce cooling systems for data centers.8

Energy/Industrials. AI’s broad penetration across industries is driving a spike in demand for energy; data centers are projected to account for 11–12% of US power demand by 2030, up from 3–4% today.9 Meeting this demand will present opportunities for an array of businesses, from drillers and oil servicers to the providers of power infrastructure.

Biotech. Well represented by small caps, the biotech industry is almost purely domestic and therefore leveraged to positive effects from regulatory easing. Looser policies for developing and approving new drugs could facilitate major improvements—perhaps even breakthrough discoveries—in a range of treatment and therapies, unleashing heretofore unseen earnings power.

Financials. While potential regulatory reform and lower capital requirements could compromise the balance sheets of small banks over the long term, a less burdensome regulatory environment likely would reduce compliance costs in the short term. Separately, continued market share gains by private capital providers could squeeze out the weakest local banks, forcing mergers and/or closures and paving the way for a new breed of small cap banks—notably, semi-regionals centered in the South and lower-tax states—with higher profitability and faster growth.

Security Selection and Price Discipline Underpin Resilience

Within the context of a long period of relative small cap underperformance, it’s worth remembering that small caps historically have been the most rewarding sector of the market over the long run back to 1927.10 Although a lagging market can be unsettling in the short term, it can also provide opportunity to buy good companies at attractive valuations. Should growth prospects broaden beyond a narrow cohort of megacap tech stocks, thoughtful active management rather than passive beta exposure may once again be the key to investment success.11