Macro & Market Views

Homing in on Residential Real Estate Debt

Homing in on Residential Real Estate Debt

Reflections 2024-2025

With supply constrained and demand persistent amid high home prices and high mortgage rates, the secular themes supporting the US housing market remain intact. Napier Park’s Head of Real Estate Debt Strategies Rajesh Agarwal and Managing Director Tim Ruberti discuss why they believe the current environment favors private investment opportunities in real estate specialty lending.

US Residential Real Estate Market Remains Imbalanced

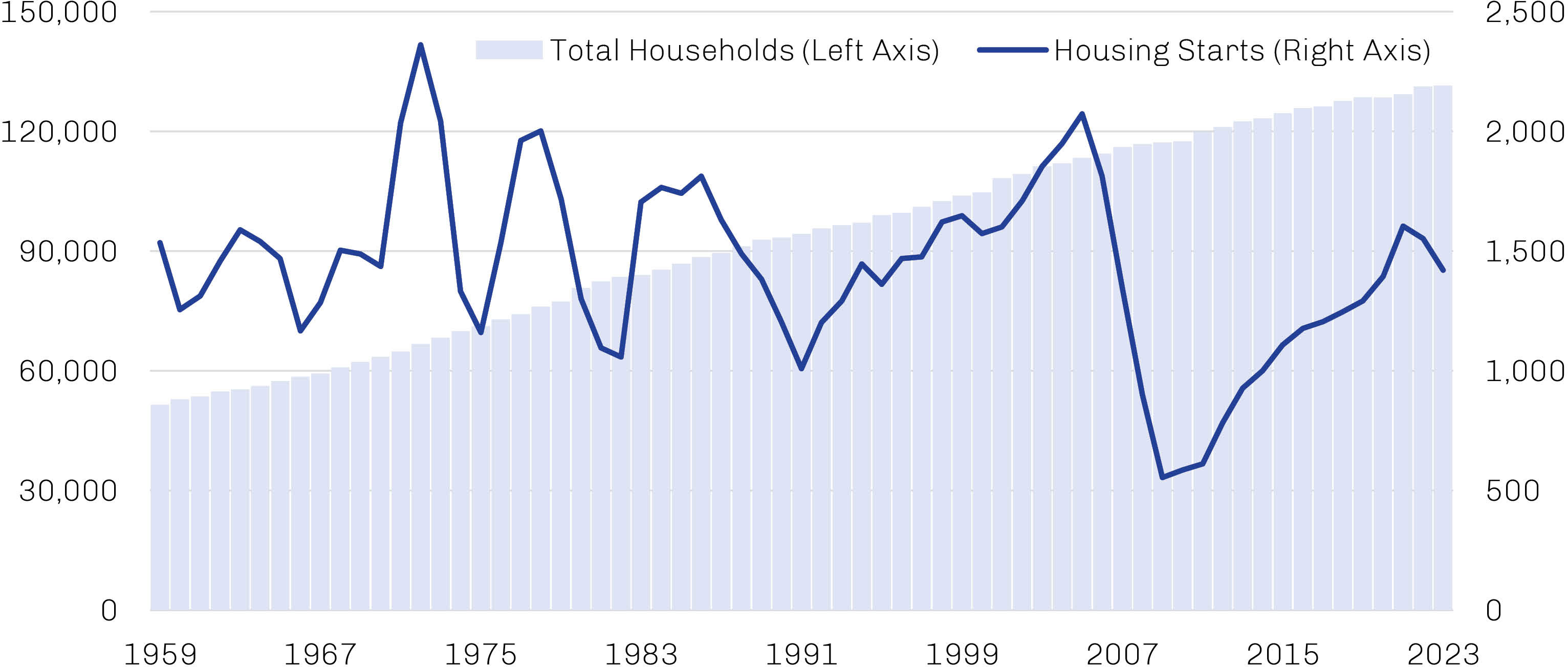

The supply of housing in the US has grown increasingly strained in the years following the global financial crisis, as a credit crunch amid the turmoil of that period prompted a massive decline in housing starts from which the construction industry has yet to fully recover. The demand side of the equation, meanwhile, has been well supported by unabated household formation. As shown in Exhibit 1, the number of US households has doubled since 1970 while housing starts remain stuck at the same level.

Exhibit 1. New Housing Supply Has Lagged Household Formation for Most of This Century

In Thousands, 1959 through 2023

Source: Federal Reserve; data as of December 31, 2023.

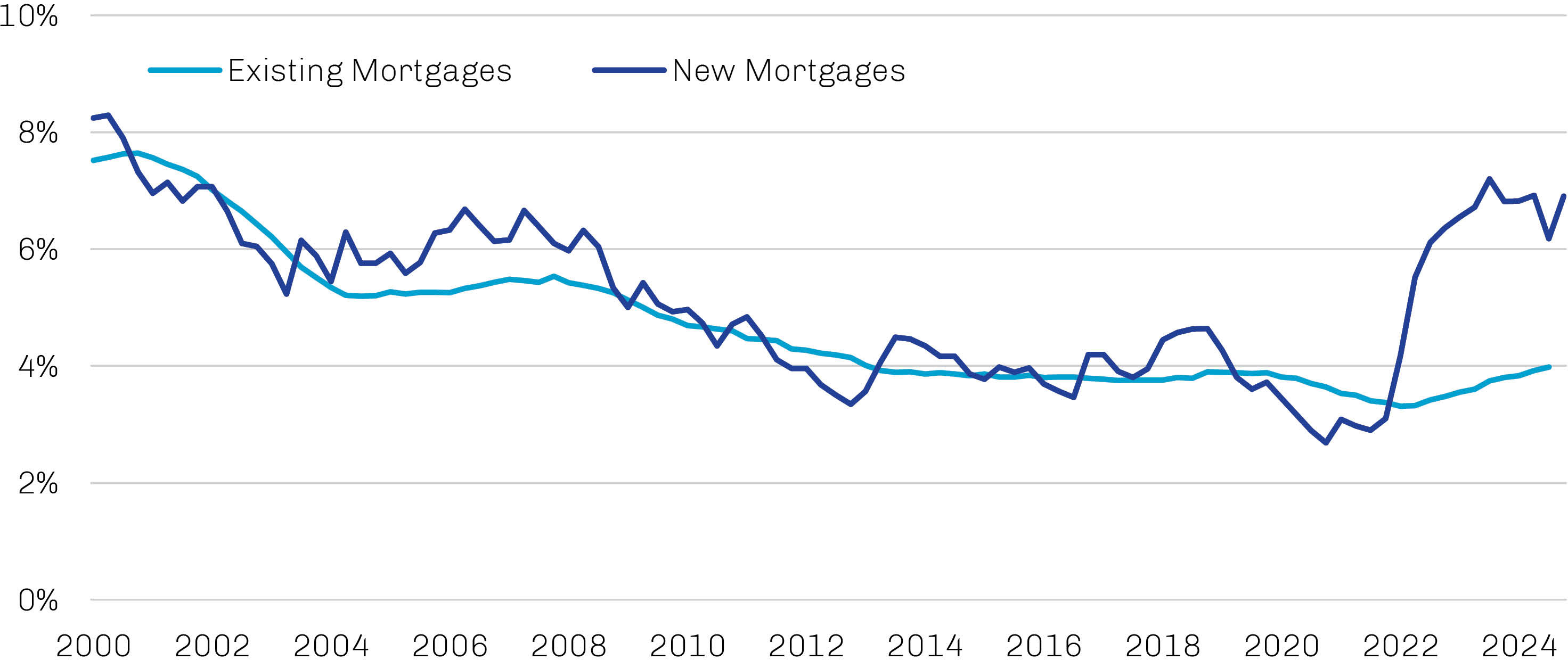

The impact of new-home underbuilding has been exacerbated by the limited supply of existing homes for sale. This is primarily due to the “lock-in effect” of the higher mortgage rate regime, as demonstrated in Exhibit 2. Though the 30-year fixed-rate mortgage ended 2024 down from 2023’s peaks, it far exceeds the 4% average on existing mortgages and remains a significant disincentive to sell.1 This locked-in cohort includes many of the country’s 65 million baby boomers, who account for 36% of homeowner households in the US; a recent survey found that nearly 70% of this group plan to age in place in their current homes.2

Exhibit 2. Much Higher Interest Rates on New Mortgages Have “Locked In” Current Homeowners

30-Year Fixed-Rate Mortgage Average, January 2000 through December 2024

Source: Morgan Stanley Research, National Association of Realtors, Freddie Mac, US Census Bureau, Bureau of Labor Statistics; data as of December 26, 2024. Reflects latest available data for each series.

Housing demand remains well supported by consumer fundamentals, which, together with a shortage in supply, have buoyed home prices. Household net worth stands at a record high, debt levels remain manageable even off Covid-19-era lows, and indicators of consumer confidence have been biased higher.3 This is evidenced in Exhibit 3 by Fannie Mae’s Home Purchase Sentiment Index, which has reclaimed levels consistent with pre-tightening trends as consumers acclimate to the environment of higher home prices and higher mortgage rates.

Exhibit 3. Consumer Housing Sentiment Has Rebounded from All-Time Lows

Fannie Mae Home Purchase Sentiment Index, December 2019 through December 2024

Source: Fannie Mae; data as of January 7, 2025.

Such acclimation may continue to be necessary. Mortgage rates have been on the rise since the Federal Reserve began cutting its policy rate in September, contrary to what many observers may have expected. This is because mortgage rates are based on long-term Treasury yields, which in turn are impacted by expectations for future short-term interest rates rather than their current levels. Due in large part to persistent inflation, expectations for future rates have been biased higher, pulling long Treasury and mortgage rates along with them.

But while improved affordability could drive additional demand, supply is likely to remain the US housing market’s main problem.

Credit Risk Premia in Public Markets Has Shrunk…

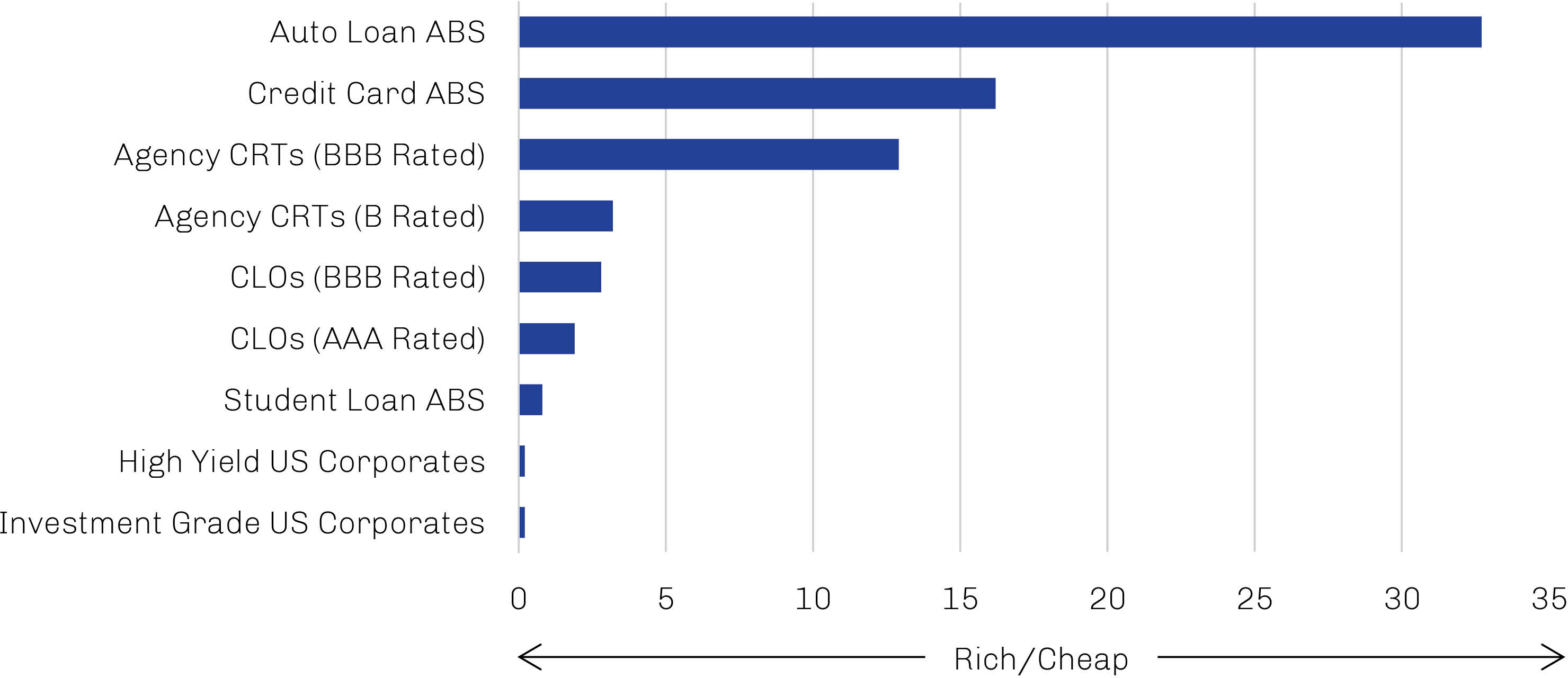

The strong performance of credit over the last 18 months has driven spreads for most public securities markets well below their long-term averages. This is particularly true of traditional public fixed income products, which enter 2025 facing the most severe valuation constraints seen in more than two decades, as shown in Exhibit 4.

Exhibit 4. Valuations Are Constrained Across Many Public Credit Segments

Spread Percentile Ranks, January 2010 through December 2024

Note: Auto Loan ABS = ICE BofA AA-BBB US Fixed Rate Automobile ABS Index; Credit Card ABS = ICE BofA AA-BBB US Floating Rate Credit Card ABS Index; Agency CRTs (BBB Rated) and Agency CRTs (B Rated) = Goldman Sachs Global Investment Research calculations using outstanding prices; CLOs (BBB Rated) = Palmer Square CLO BBB Index; CLOs (AAA Rated) = Palmer Square CLO AAA Index; Student Loan ABS = ICE BofA AA-BBB US Floating Rate Student Loan ABS Index; High Yield US Corporates = Bloomberg US Corporate High Yield Index; Investment Grade US Corporates = Bloomberg US Corporate Index.

Source: PitchBook | LCD, Goldman Sachs Global Investment Research; data as of December 3, 2024.

There are a range of real estate-backed structured credit products that trade publicly. In addition to the spread pressures felt across the fixed income complex, many of these products have been further squeezed by the “technical” bid for absolute yield as well as the resilient macro backdrop for US residential real estate. Credit risk transfer (CRT) securities—non-guaranteed mortgage-backed securities issued by US government sponsored enterprises Fannie Mae and Freddie Mac—are one such example.

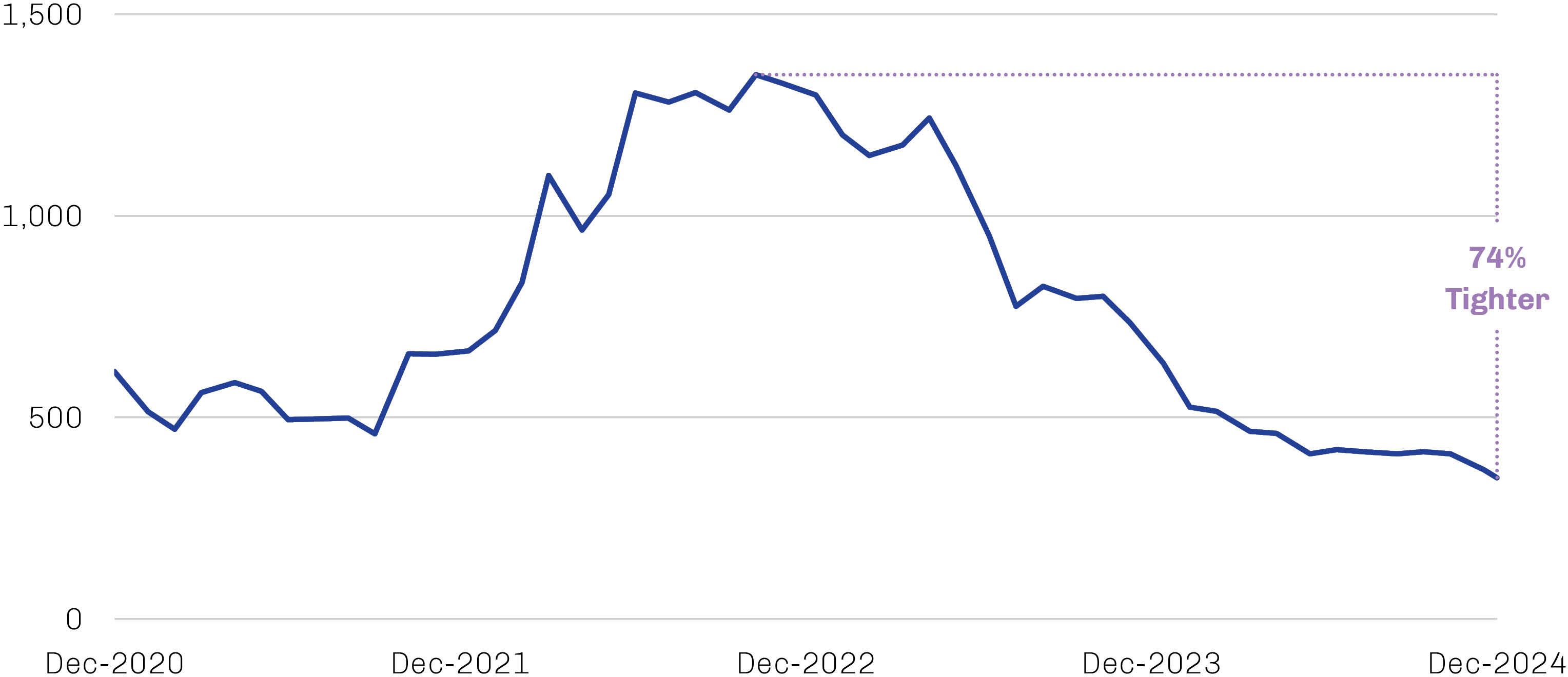

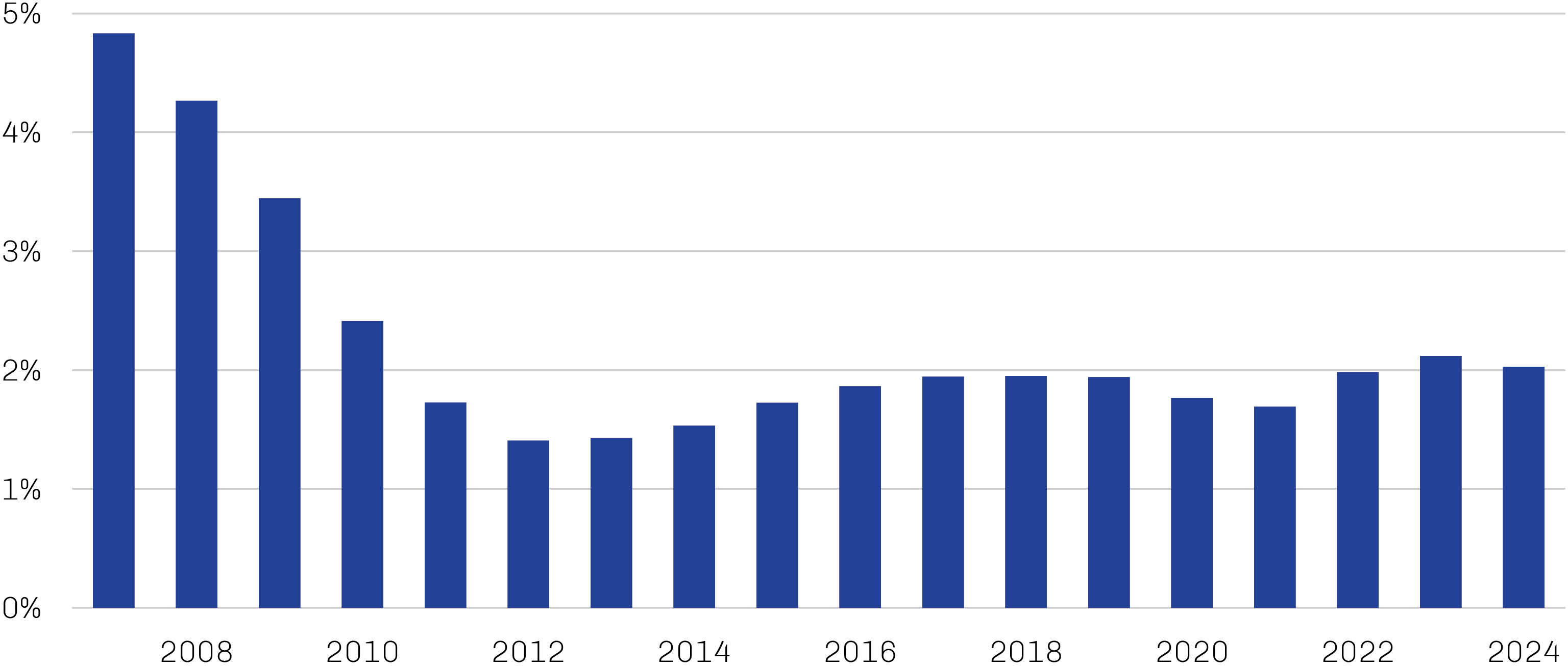

CRTs have been particularly successful of late. CRTs pay a fixed spread over 30-day SOFR (Secured Overnight Financing Rate), which is highly sensitive to changes in the federal funds rate and rose from near zero to well above 5% during the Fed’s 2022–23 hiking cycle.4 CRT spreads to SOFR widened significantly on concerns that central bank tightening would trigger a recession and an associated increase in mortgage delinquencies. As a result of higher rates and wider spreads, these securities offered very high yields despite containing attractive structural provisions; through the Covid-19 dislocation, for example, no CRT transaction experienced a loss greater than two basis points.5 With the US economy proving resilient despite tighter financial conditions, risk appetites soon returned and CRT spreads have tightened by about 1,000 basis points since late 2022, as shown in Exhibit 5. This tightening provided CRT investors with robust returns, but we believe the current entry point for these vehicles appears less attractive at current levels.

Exhibit 5. Credit Risk Transfer Spreads Have Tightened Meaningfully Over the Past Two Years

CRT B2 Spread to 30-Day SOFR in Basis Points, December 2020 through December 2024

Source: Citi Research; data as of December 13, 2024.

…but We Believe Opportunities in Private Residential Real Estate Debt Remain Attractive

With public credit spreads near all-time tights entering 2025, the returns on residential mortgage securities like CRTs are likely to be more modest in the months ahead.6 At this time, we believe there are more attractive opportunities to be found on the private side of the real estate debt market, including residential transitional loans and land banking. Private markets tend to have a delayed and lagged response to changes in lending costs, and their structural complexity and illiquidity typically provide an additional boost to yields. Further, the short durations and robust cash flows typical of these assets enable the frequent reinvestment of proceeds, providing investors optionality to migrate into public credit opportunities should market conditions shift.

While high home prices and strong demand would seem to be powerful motivators for homebuilders to aggressively fill the housing gap, significant headwinds persist. Notably, rising construction costs have weighed on builders’ profit margins and put further upward pressure on home prices. Materials, equipment and labor costs are all up sharply post-Covid, and the price of land has outstripped the rise in housing prices nationally.7 The explicit and/or implicit costs of regulatory compliance in order to develop buildable lots—which include a range of requirements from zoning approval to permitting to environmental studies—have remained high as well; a study from 2021 found that regulations imposed by all levels of government account for nearly 24% of the final price of a new single-family home.8

Given high costs and lengthy timelines, homebuilders have long relied heavily on credit to finance new construction or the renovation of existing properties for resale. But commercial banks, their traditional source of funding, have pulled back from certain types of real estate activities—including acquisition, development and construction lending—due to regulatory changes enacted in the wake of the global financial crisis. As shown in Exhibit 6, construction loans as a percentage of bank total assets today are less than half of what they were in 2007.

Exhibit 6. Traditional Banks Have Pulled Back from Certain Types of Real Estate Lending

Construction Loans as a Percentage of Total Bank Assets, 2007 through 2024

Source: Federal Deposit Insurance Corporation; data as of December 31, 2024.

As commercial bank activity has receded, a fragmented collection of specialty lenders have stepped in. The majority of these lenders lack the capital to underwrite and hold these loans at meaningful scale, however, which has presented an opportunity for asset managers to provide necessary liquidity to the real estate industry at attractive terms.

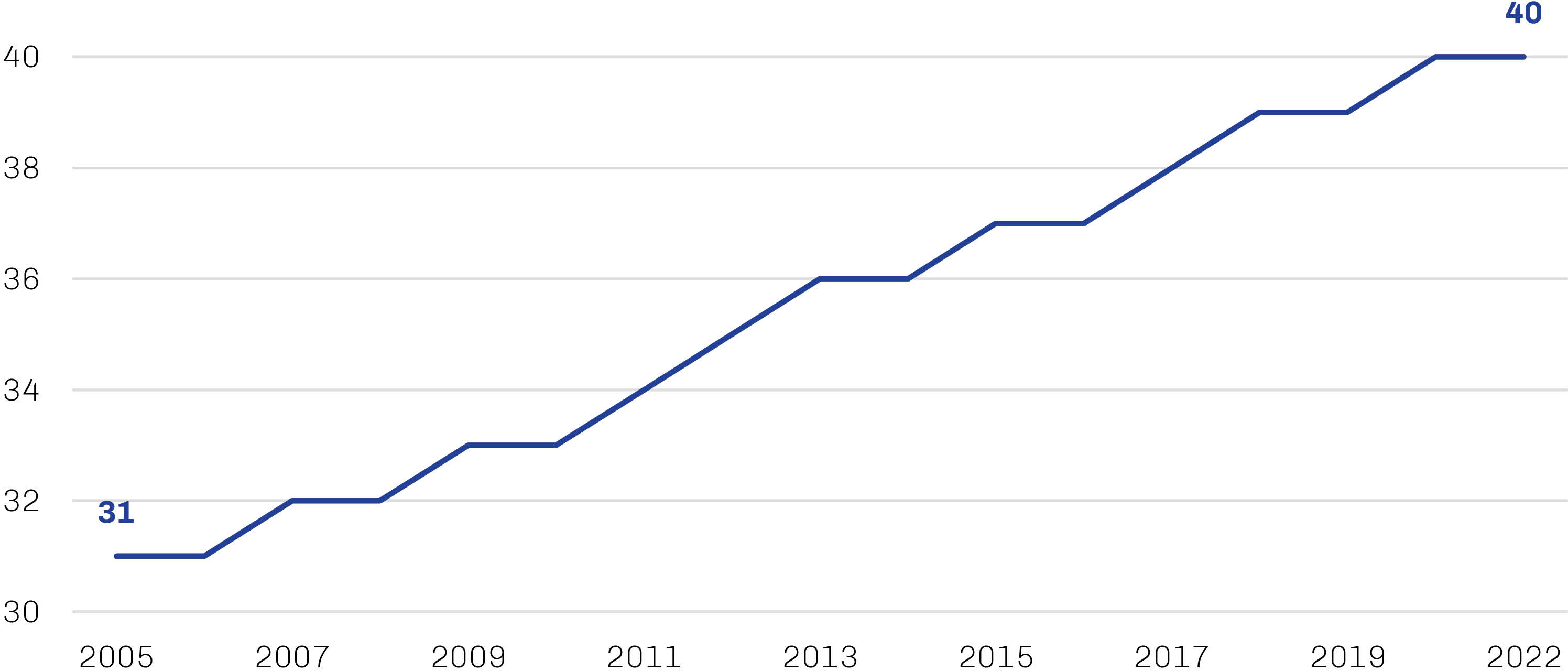

Residential transitional loans are an example of one such opportunity. To many buyers, a refurbished home in an established neighborhood with proven infrastructure like schools, parks and retail is more desirable than a new home in a new area. As could be inferred from the aged state of the US housing stock depicted in Exhibit 7, not every legacy property is in turnkey condition, which has fueled the proliferation of “fix and flip” activity. Real estate developers purchase single family residences with the intent of renovating and reselling them at a profit within a short period of time. There is a similar dynamic evident in the multifamily space, as existing rental properties are upgraded to standards that can command higher rents.

Exhibit 7. Aged US Housing Stock Fuels Demand for Renovation Capital

Estimates of Median Age in Years of US Owner-Occupied Housing, 2005 through 2022

Note: The Census Bureau did not release the standard American Community Survey in 2020 due to data-collection disruptions experienced during the Covid-19 pandemic.

Source: US Census Bureau, American Community Survey; data as of December 31, 2022. Reflects latest data available.

Residential transitional loans provide the capital for these rehabs. These loans are typically 12 to 18 months in tenor and secured by a first lien on the property, with interest-only payments until the principal is due at maturity. Frequently, these loans are originated by small, regional private lenders focused exclusively on this type of financing and related services. Lacking the scale to hold these loans to maturity, originators often sell them to large, nonbank asset managers looking to build diversified portfolios of residential transitional loans they believe will generate compelling risk-adjusted long-term returns.

Land banking is another area where we see opportunity. The limited supply of buildable land is among the factors constraining the rebound in US new-home construction, a fact often overlooked in a country with a land area in excess of 3.5 million square miles.9 Beyond the limitations of local zoning laws, the process of preparing raw land for construction—from design to infrastructure build—often takes two years or more as a result of significant local, state and national regulations.10

This lag can be a challenge for homebuilders trying to maintain robust development pipelines without compromising liquidity and financial flexibility, and many have moved toward “land-light” business models in response. As such, off-balance-sheet financing solutions like land banking—in which a capital provider, in exchange for a fee, acquires and holds property on behalf of a builder that has agreed to purchase lots on the property at a predetermined schedule—have become a staple of builders’ land inventory-management strategies. Large public homebuilders, in particular, have demonstrated a willingness to pay a significant premium to the prevailing interest rate on corporate debt for the benefits of such an arrangement.

Staying Nimble Within a Secular Growth Story

While dynamics remain supportive of the US housing market as a whole, we believe current return prospects favor private lending opportunities. However, history has shown that public markets can quickly grow volatile, especially in an environment of tight credit spreads; it would not be surprising to see spreads widen significantly should some sort of near-term dislocation occur. We believe investors able to nimbly adjust their public and private exposures and seize upon unique opportunities as they emerge may be well positioned for success in the residential real estate debt space.