Macro & Market Views

Railcar Leasing: The HALO Effect

Railcar Leasing: The HALO Effect

Though advancements in the latest technology tend to dominate the financial headlines, the US economy runs on the rails that crisscross the nation.

- Railcar leasing, in our view, offers steady, diversified, contractual income streams with risk characteristics comparable to higher grade credit alongside embedded potential upside through lease repricing, residual value realization and active asset management.

- Underpinned by long-lived physical assets that provide contractual cash flows and maintain durable residual values, railcar leasing historically has generated returns differentiated from public markets and positively correlated to inflation and interest rates.1

- As new technologies threaten margin durability across industries, rail assets represent essential physical infrastructure with limited exposure to technological disruption.

- Perpetual vehicle structures enable long-term ownership of assets, avoiding forced sales and enhancing compounding through continuous reinvestment and tax efficiency.

- We believe that scale, risk management and operational knowledge, as provided by highly experienced real assets teams, are key to successfully taking advantage of the opportunities available in railcar leasing.

Transporting food, fuel, fertilizer and countless other essential items across the US and the rest of North America, railcars, in our view, represent one of the most durable of the HALO (heavy asset, low obsolescence) sectors bridging the analog past to the digital present. Owning and leasing railcars to the industries that produce these commodities presents an attractive potential opportunity to generate a differentiated return stream that has historically exhibited low correlation to traditional financial markets while maintaining resilience across economic cycles.

Railcar leasing combines contractual, credit-like cash flows with long-lived assets that retain residual value and benefit from cyclical repricing. For investors, the result is downside mitigation we believe is comparable to high-quality credit, durability similar to infrastructure and embedded upside through lease rate resets and asset management.

Despite these appealing characteristics, railcar leasing remains a structurally underallocated asset class, often overlooked due to its classification ambiguity. As we discuss, however, there are a range of short- and long-term secular trends that we believe continue to favor railcar lessors and investment in the space.

Owning Serial Numbers, not CUSIPs

For investors, railcars represent an asset that offers a stable income profile similar to some higher grade fixed income securities combined with the total return potential of some alternative assets. Underpinned by long-lived physical assets—not securities—that provide contractual cash flows and maintain durable residual values, investments in railcars historically have generated a return profile characterized by:

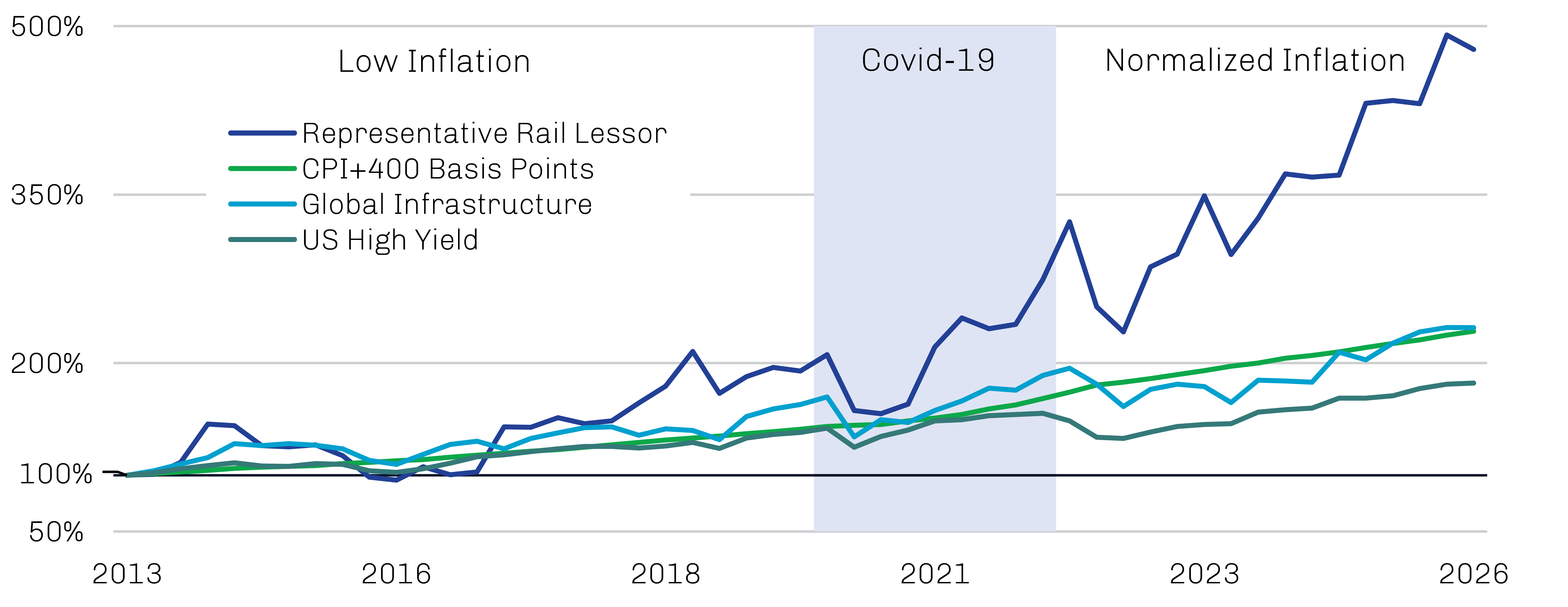

- Outperformance relative to inflation and global infrastructure benchmarks, as shown in Exhibit 1 below

- A low correlation to traditional financial markets and low sensitivity to idiosyncratic macroeconomic or geopolitical disruptions2

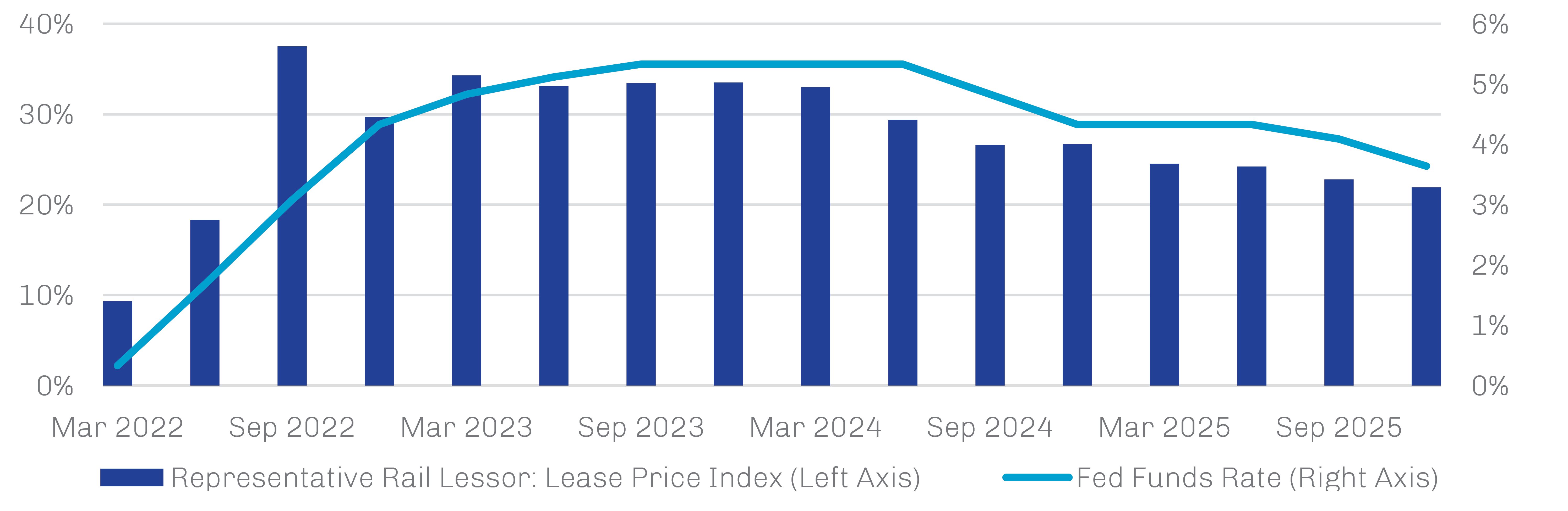

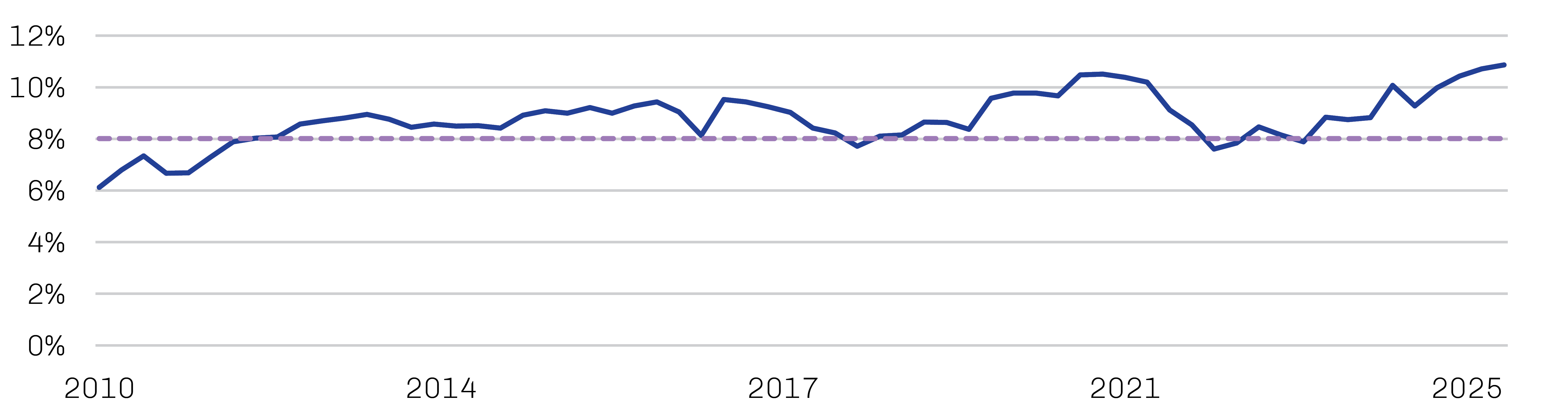

- Lease renewal rates that keep pace with changes in the federal funds rate, as shown in Exhibit 2 on page 4

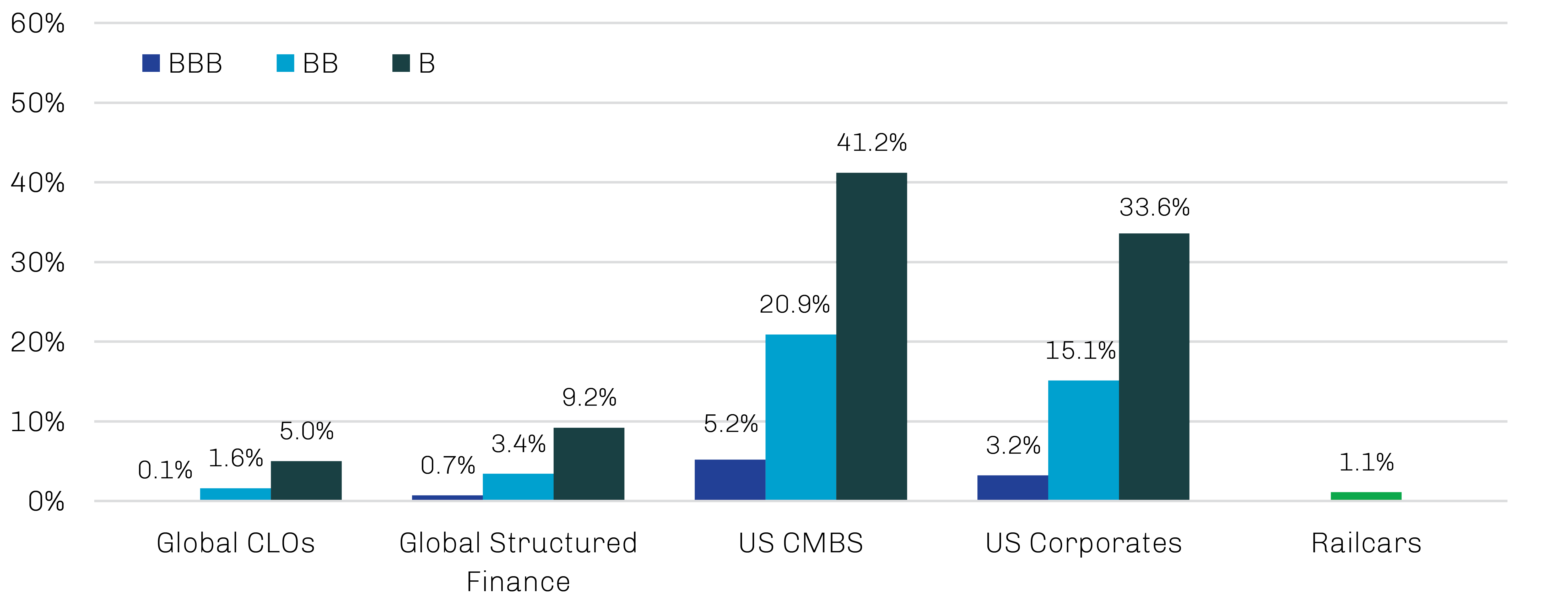

- Low railcar impairment rates comparable to investment grade assets, as shown in Exhibit 3 on page 6

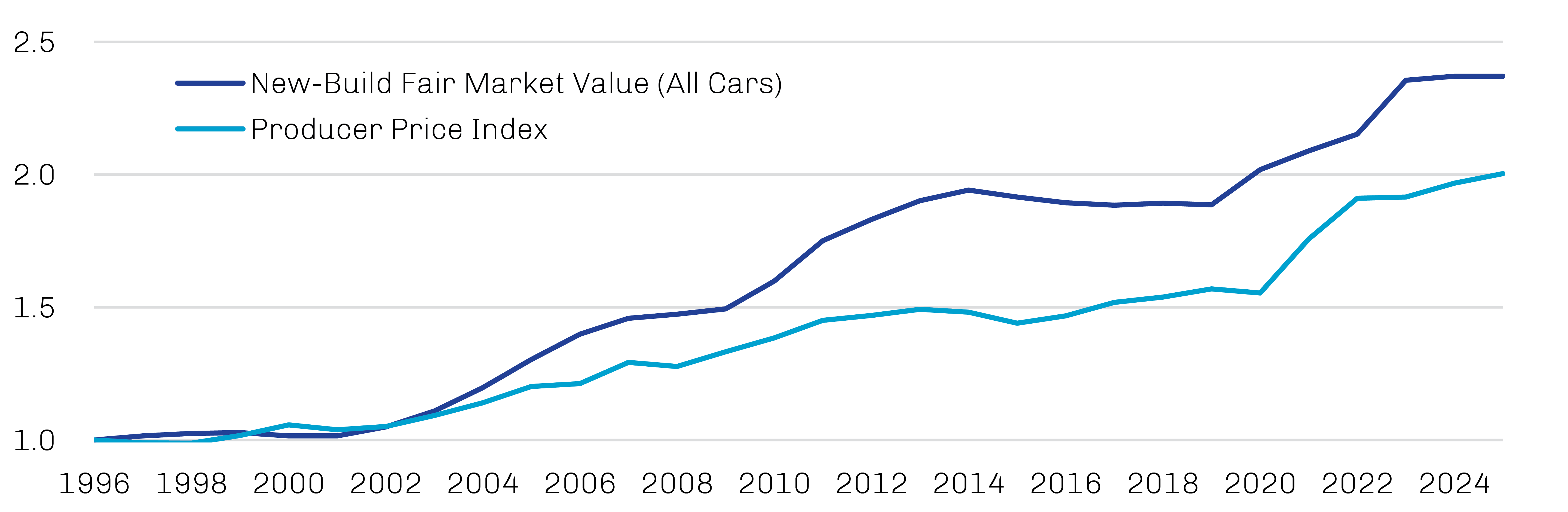

- New-build fair market value increases that exceed inflation, as shown in Exhibit 4 on page 6

- Lease-rate spreads that historically have exceeded interest rates, as shown in Exhibit 5 on page 7

- Insulation from technological trends like artificial intelligence (AI) that have buffeted other investments

Exhibit 1. Railcar Leasing Has Outpaced Inflation and Infrastructure Returns

Annual Internal Rates of Return

Note: Representative Rail Lessor = listed stock; CPI = US consumer price index; Global Infrastructure = Dow Jones Brookfield Global Infrastructure Total Return Index; US High Yield = iBoxx US Liquid High Yield Total Return.

Source: Bloomberg, company reports; data as of March 31, 2026.

Depreciation Benefits Can Bolster Returns in Diverse Portfolio Buckets

Beyond supportive fundamentals and technicals (as discussed on page 5), US taxable investors in railcars may further benefit from accelerated depreciation. Despite a railcar’s useful life of 40–50 years, the tax code allows railcars to be fully depreciated in the year they are acquired—tantamount to a zero-interest loan from the government for the duration of ownership. This rule, which was made permanent by 2025’s tax and spend bill, applies to the purchase of both new and used railcars and can be used multiple times on the same railcar as it changes hands. Certain investors may also use the upfront tax-losses generated by accelerated depreciation to offset other US tax liabilities.

Year-one depreciation— tantamount to a zero-interest loan—can enhance returns for US taxable investors.

With contractual cash flows driven by ownership of real assets, railcar leasing can be allocated to multiple segments of a diversified portfolio, including credit, alternatives or infrastructure with potential for additional benefits if accessed through a long-duration structure (as discussed on page 8). For investors with risk-based capital (RBC) limitations, such as insurance companies, railcar portfolios can be tranched to allow for RBC optimization.

The New Old Thing

For nearly 200 years, rail shipping has been a foundational component to the development of the US economy. Today, the freight network covers nearly 140,000 miles of rail across North America, efficiently hauling 1.5 billion tons of raw materials and finished goods in a typical year at a lower cost and with a lower environmental impact than the alternatives.3

While financial markets in recent years have been focused on the asset-light information economy and, more recently, the potentially disruptive impacts of advancements in AI, so-called HALO businesses have emerged as the new old thing. Rail stands out within this shift, representing infrastructure that is both essential and difficult to replace; if anything, rail networks may be enhanced by AI as it optimizes routes, improves network utilization and enables predictive maintenance.

Potential resilience in the face of AI is only one reason a real-economy investment like railcars has returned to the collective consciousness. Several structural factors also reinforce demand for rail transport. Continued US economic growth supports freight volumes, while ongoing efforts by US manufacturers to retool their supply chains—including expansions of their domestic footprints—in the aftermath of disruptive events like Covid-19 and the Trump administration tariffs have increased domestic transportation needs. 4,5 At the same time, elevated labor and materials costs have inflated new railcar prices, while higher capital costs have raised the cost of ownership, a combination that has suppressed new supply, bolstered residual values of existing cars and reinforced the appeal of leasing for shippers. And with one gallon of fuel able to move one ton of freight 500 miles by rail, rail produces 75% less greenhouse gas emissions than trucking, and its environmentally friendly profile is well-aligned with the increasing popularity of green logistics.6

With the utilization rate of lessor-owned railcar fleets already running above 95%, and averaging 96% over the last 20 years, we believe these short- and long-term secular trends, combined with more normal interest rates, bode well for railcar leasing fundamentals.7 As shown in Exhibit 2, lease renewals have historically occurred at rates above those of the expiring leases they replace, with changes generally tracking movements in the federal funds rate.8

Exhibit 2. Changes in Railcar Lease-Renewal Rates Have Tracked Movements in the Federal Funds Rate

Source: Company reports, Federal Reserve Board of St. Louis; data as of December 31, 2025.

The Enduring Role of Railcar Leasing

The current environment underpins the case for railcar leasing. The supply of railcars is constrained due to elevated manufacturing and financing costs, while demand is supported by resilient end markets, onshoring trends and the continued need for cost-efficient bulk transport. Higher interest rates have increased the cost of ownership for industrial users, making leasing more attractive and reinforcing pricing power for lessors. At the same time, rail remains one of the most cost-efficient and environmentally favorable modes of bulk transportation, supporting long-term demand.

While technological innovation continues to dominate financial headlines, the functioning of the US economy still depends on the physical infrastructure that moves essential goods across the country. Rail networks remain a critical backbone of this system, transporting food, fuel, chemicals and raw materials at scale.

In our opinion, railcars represent one of the most durable segments within what have been described as HALO sectors. These are asset classes defined by long useful lives, limited technological displacement risk and persistent real-economy demand.

Owning and leasing railcars to the industries that produce broadly needed goods enables investors to generate diversified, contractually obligated income streams from long-lived, essential-use equipment with the potential to preserve residual value over time. The end result is an income profile that combines investment grade-like risk characteristics with total return potential typically associated with higher yielding strategies. Moreover, the dynamics of railcar-market technicals historically have translated into a low correlation to other financial assets and a positive correlation to inflation and interest rates, among other attractive characteristics.9

Income from railcar leasing combines investment grade-like risk characteristics with the return potential of some higher yielding strategies.

Although the ebb and flow of next-gen technologies like AI may continue to disrupt investments across asset classes and industries, we believe railcars are structurally insulated from many of these forces—in both the short and long terms—as secular trends continue to favor railcar lessors and investment in the space. Specialized teams with decades of expertise investing in, operating and managing railcar fleets may be well-positioned to help sophisticated investors access this attractive sector of the old economy.

Market Technicals Favor Railcar Owners/Lessors

The US railcar market is dominated by lessors. These entities control about 70% of the 1.6 million rail cars in the system, with a heavy concentration (about 75%) among the five largest players.10 Lessors of railcars lease their rolling stock to the producers of raw materials or finished goods to facilitate distribution via the North American rail network. Lessors and their investors benefit from contractual cash flows, steady residual values and substantial depreciation-based tax benefits.

Rail lessors benefit from contractual cash flows, steady residual values and potential tax benefits.

Lessees—a highly fragmented group of companies participating in hundreds of industrial subsectors from agriculture and chemicals to food and energy—are able to transport their goods while keeping the very large capital outlays associated with building a fleet of railcars off their balance sheets. Further, they can do so cost-effectively, as the value of goods shipped typically is many multiples of the leasing cost; for example, a large grain car leasing for $650 per month might haul $120,000 per month in revenue.11 This also contributes to price insensitivity by lessees, and lessors typically have little difficulty passing along rising costs as contracts turn over.

The largest rail-freight shippers are North American industrials—many have strong investment grade credit ratings, and even those without public debt profiles are often of high quality.12 As shown in Exhibit 3, railcar lessors’ impairments have been extremely limited, suggesting credit risk consistent with investment grade securities despite returns comparable to higher-yielding investments.

Exhibit 3. Low Railcar Impairment Rate Is Comparable to Investment Grade Assets

Comparative Historical Impairment/Default Rates by Rating

Note: Global CLOs, Global Structured Finance and US CMBS = multiyear cumulative WR-unadjusted impairment rates by original rating from 2009-2024; US Corporates = average 10-year cumulative issuer-weighted global default rates from 1983-2024; Railcars = average multiyear cumulative North American railcar impairment rates of GATX and Trinity based on public filings from 2008-2025.

Source: BofA Global Research, Moody’s, company reports; data as of July 31, 2025.

Inflation and higher capital costs have not only bolstered demand for leased railcars but also have underpinned prices for new railcars, as shown in Exhibit 4, which has suppressed new supply of these long-lived assets. With the size of the railcar fleet having remained essentially flat over the past 30 years, supply and demand dynamics in the rail transport industry have been biased toward lessors.13

Exhibit 4. Market Value of New Railcars Has Outpaced Inflation

Note: Railcar sale price is adjusted using US PPI Final Demand: Finished Goods as of December 31, 2025.

Source: RailSolutions, Trinity Industries, Bloomberg, Federal Reserve Bank of St Louis; data as of December 31, 2025.

Railcar leasing has historically demonstrated resilience across economic cycles. Demand is supported by the transportation of essential goods, while diversified exposure across industries reduces reliance on any single sector. During periods of economic stress, lease rates may adjust—historically to levels above Treasuries, as shown in Exhibit 5—while high utilization levels and the ability to redeploy assets have historically supported continued cash flow generation.

Exhibit 5. Railcar Lease-Rates Have Exceeded Treasuries by 800 Basis Points on Average Since 2002

Freight and Tank Car Lease-Rate Spreads to Five-Year Treasuries

Source: RailSolutions, Trinity Industries, Bloomberg, Federal Reserve Bank of St Louis; data as of December 31, 2025.

Actively Managing Credit Risk Within the Fleet While Seeking to Maximize Residual Value

Railcar investments have generally demonstrated strong resilience to intermittent macro and geopolitical events, such as economic slowdowns, higher interest rates, regulatory tightening and trade conflicts. The two primary investment-risk exposures for railcar lessors—which affect both their cost of capital to finance equipment and potential risk-adjusted returns—are lease-counterparty risk and residual value risk.

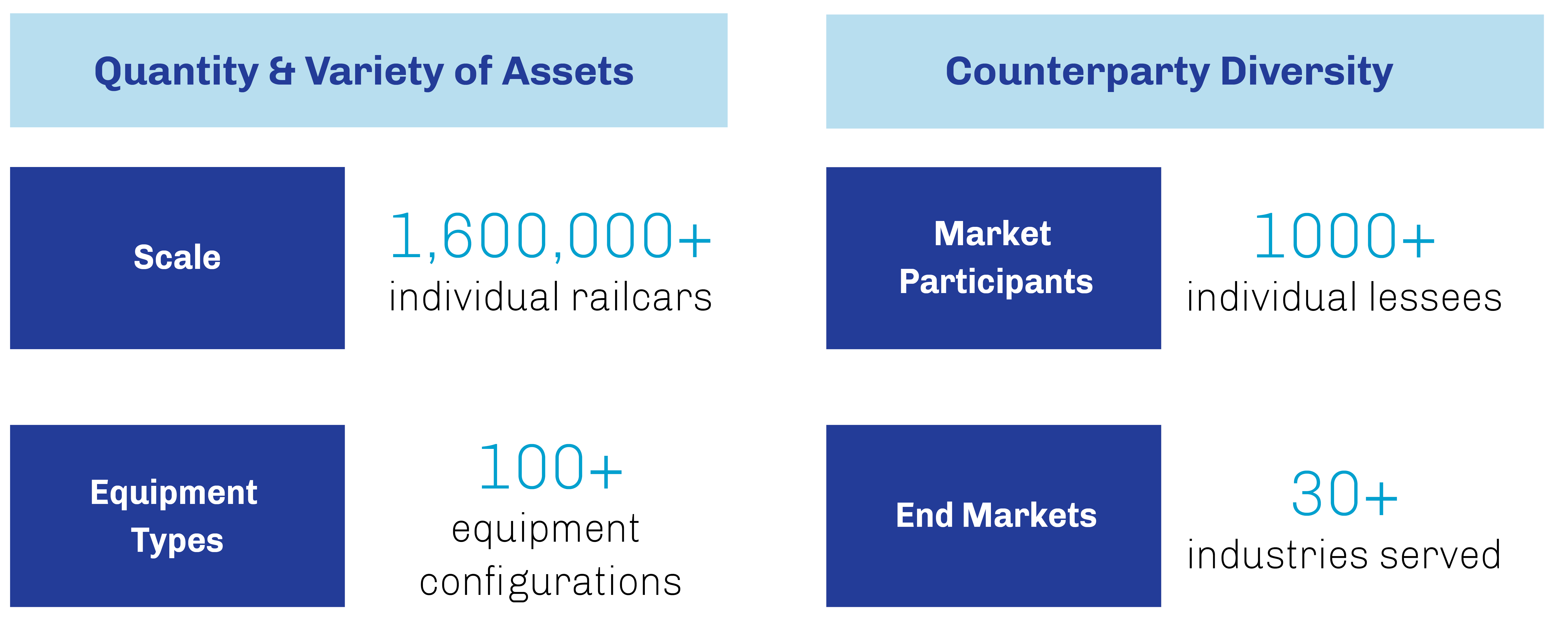

Counterparty risk can be mitigated by assessing and monitoring the creditworthiness of lessees, balancing the investment grade/sub-investment grade mix, and avoiding concentrations in any single obligor or industry —facilitated by scale and diversification—as shown in Exhibit 6. Understanding the interplay between counterparties and the potential impacts of systemic shocks on seemingly unrelated lessees is key, as is structuring lease terms to manage duration across the portfolio. With a much lower average ticket size than other transportation classes, building a diversified fleet of railcars—not only by counterparty but also industry, geography and car type—is quite achievable.14

Exhibit 6. Scale and Diversification Can Mitigate Risk in Rail Lease Portfolios

Source: Railway Age; data as of April 8, 2026.

In addition to the structural provisions of industry-standard leases to help preserve the residual value of rail assets, active fleet management can help maximize residual value potential. To this end, railcar lessors model the useful life and physical durability of their equipment to understand longevity while analyzing economic depreciation and elasticity of lease rates as assets age. Technological obsolescence, which is relatively minimal in the world of fungible railcars, is nonetheless gauged to evaluate replacement risk in the face of value-diminishing innovation. Finally, original-equipment manufacturing production capacity is monitored to understand fluctuating supply. All of this is done within the context of examining how the economics of different equipment types move together to evaluate prospective benefits of diversifying the fleet.

With a highly liquid secondary market for railcars—approximately 2-3% of the 1.6 million car fleet turns over annually—strategic opportunities for lessors to optimize fleet configurations and maximize tax benefits may prevail.15

1. Source: Preqin; data as of December 31, 2025.

2. Source: Fortune Business Insights; data as of May 11, 2026.

3. Source: Association of American Railroads; data as of February 24, 2025.

4. Source: Bureau of Economic Analysis; data as of February 20, 2026.

5. Source: McKinsey & Company; data as of December 2, 2025.

6. Source: Association of American Railroads; data as of September 30, 2025.

7. Source: IntelliTrans; data as of March 23, 2026.

8. Source: Railway Age; data as of June 12, 2025.

9. Source: BofA Global Research, Moody’s; data as of July 31, 2025.

10. Source: Fortune Business Insights; data as of May 11, 2026.

11. Source: Napier Park Global Capital estimates; data as of April 30, 2026.

12. Source: S&P Global; data as of February 6, 2026.

13. Source: Napier Park Real Assets estimates based on data from Trinity Industries; data as of March 31, 2026.

14. Source: IntelliTrans; data as of March 23, 2026.

15. Source: Railway Age; data as of March 13, 2026.

The information contained in this material is provided by First Eagle Investment Management, LLC (“FEIM”) and its global subsidiaries (collectively, “First Eagle”). FEIM is an investment adviser registered with the US Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training.

This material is for informational purposes only and reflects prevailing conditions and the judgment of the author(s) as of the date of publication, all of which are subject to change. This material should not be relied upon as investment advice; it does not constitute a recommendation to buy or sell a security or other investment; and it is not intended to predict or depict the performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or consider the specific objectives or circumstances of any investor. We consider the information in this material to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment.

Prospective investors should inform themselves and consult with an investment, tax or legal professional as to any applicable legal requirements, taxation and exchange control regulations in the countries of their citizenship, residence or domicile that may be relevant prior to investing.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

All investments involve the risk of loss of principal.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Definitions

BBB credit rating—as used by S&P Global Ratings and Fitch Ratings—is an investment grade rating on a bond considered to have adequate capacity to meet its financial commitments but that is more susceptible to adverse business, financial and economic conditions. The equivalent rating from Moody’s Investors Service is Baa.

BB credit rating—as used by S&P Global Ratings and Fitch Ratings—is a speculative-grade rating on a bond considered less vulnerable in the near term but that faces major ongoing uncertainties to adverse business, financial and economic conditions. The equivalent rating from Moody’s Investors Service is Ba2.

B credit rating—as used by S&P Global Ratings and Fitch Ratings—is a speculative-grade rating on an issue considered more vulnerable to adverse business, financial and economic conditions but currently with the capacity to meet its financial commitments. The equivalent rating from Moody’s Investors Service is B2.

Collateralized loan obligations (CLOs) are financial instruments collateralized by a pool of corporate loans.

Commercial mortgage-backed securities (CMBS) are debt securities secured by cash flows from commercial real-estate mortgages.

Consumer price index (CPI) (Price) measures inflation as experienced by consumers in their day-to-day living expenses by capturing the average change over time in the prices paid for a representative basket of consumer goods and services. A price-return index only measures price changes.

Federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis.

High yield corporate bonds are debt securities issued by companies that offer a higher rate of interest due to their perceived higher risk of default.

Structured credit is a financial instrument that pools together groups of similar, income-generating assets.

Dow Jones Brookfield Global Infrastructure Composite Index (Net) is designed to measure the performance of pure-play infrastructure companies domiciled globally. The index covers all sectors of the infrastructure market and includes Master Limited Partnerships (MLPs) in addition to other equity securities. To be included in the index, a company must derive at least 70% of cash flows from infrastructure lines of business. A net-return index tracks price changes and reinvestment of distribution income net of withholding taxes.

iBoxx USD Liquid High Yield Index (Gross/Total) measures the performance of liquid US dollar-denominated high yield bonds. A total-return index tracks price changes and reinvestment of distribution income.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The information presented does not reflect the performance of any fund, strategy or account managed or serviced by First Eagle, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this material will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

Availability of the products or services described may be restricted by law in certain jurisdictions. This material may not be distributed, published or used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

United Kingdom

Napier Park Global Capital Ltd is authorised and regulated by the Financial Conduct Authority (FRN: 541427) in the United Kingdom.

Middle East

This material is for information purposes only and has not been, and will not be, registered with or reviewed or approved by any regulator located in the Middle East. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe to or purchase, any products, strategies or other services, nor shall it, or the fact of its distribution, form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this material wishes to receive further information regarding any products, strategies or other services, it shall specifically request the same in writing from an authorized financial adviser.

Canada

Pursuant to the international adviser registration exemption in National Instrument 31-103, First Eagle Investment Management, LLC is informing you that: (i) First Eagle Investment Management, LLC. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration under National Instrument 31-103; (ii) First Eagle Investment Management, LLC’s jurisdiction of residence is New York, USA; (iii) there may be difficulty enforcing legal rights against First Eagle Investment Management, LLC. because it is a resident outside of Canada and all or substantially all of its assets may be situated outside of Canada. FEF Distributors, LLC (“FEFD”) (SIPC), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy or product.

First Eagle Investments is the brand name for First Eagle Investment Management, LLC and its subsidiary investment advisers.

First Eagle Alternative Credit and Napier Park are brand names for the two subsidiary investment advisers engaged in the alternative credit business.

© 2026 First Eagle Investment Management, LLC. All rights reserved.