Macro & Market Views

Municipal Bonds: Unrated ≠ Uninvestable

Municipal Bonds: Unrated ≠ Uninvestable

With more than $4.3 trillion distributed across more than one million distinct municipal bonds and 50,000 issuers, the municipal bond market is large and highly fragmented.1

- We believe unrated municipal bonds—whether newly issued or trading in the secondary market—represent a particularly attractive opportunity for investment managers to identify potential value through skilled credit analysis.

- Municipal issuers often forego bond ratings due to cost. For unrated bonds, the investor is solely responsible for assessing a bond’s creditworthiness, a complexity that is typically accompanied by higher interest rates.

- While unrated bonds are not necessarily risker than rated bonds, the significant dispersion of yields and prices among this cohort offers opportunity for active managers to identify bonds with favorable yields relative to credit quality and default risk.

Historically, this fragmentation has resulted in significant dispersion of yields and prices for similar bonds2, a dynamic that has provided skilled credit managers with ample opportunity to leverage their underwriting acumen to identify potential mispricings in the market. And, based on our research, nowhere has this opportunity been more abundant than within the large cohort of unrated bonds.

While unrated bonds have not been subject to the proprietary scrutiny of nationally recognized statistical rating organizations (NRSRO) like Moody’s or S&P Global Ratings, we don’t believe their lack of credit rating should be interpreted as a reflection of the borrower’s capacity to meet its financial commitments. In fact, it’s been our experience that the universe of unrated municipal bonds represents a particularly attractive hunting ground for managers in search of favorable yields relative to credit quality and default risk.

Ratings Aren’t Everything

Though not required by law, many bond issuers, including municipalities, seek the imprimatur of an NRSRO before issuing bonds to the public. In these instances, one or more rating agencies will be tasked with evaluating the creditworthiness of the debt issue and opine on the issuer’s ability to meet its financial obligations in full and on time. Upon the completion of its analysis, the agency will assign the bond a rating—generally from AAA (highest) to D (lowest), with many increments in between—reflecting its likelihood of default relative to the broad universe of credit risk.

Credit ratings not only provide investors with an independent assessment of a bond’s relative risk, they also influence the interest rate the issuer would need to pay to attract investors to the offering. Generally speaking, a higher rating implies deeper financial resources on the part of the issuer and a higher probability of loan repayment, which translates into a wider and deeper market for its debt and a lower interest rate for investors. Bonds further down the ratings spectrum are perceived as riskier and thus tend to pay a higher interest rate.

Unrated bonds are not necessarily riskier than a rated bond.

Unrated bonds are not so easily classified. Though considered speculative for most practical purposes—any investor prohibition against holding high yield bonds, for example, would typically extend to unrated paper— unrated bonds are not necessarily riskier than a rated bond. The only conclusion that can definitively be drawn from the lack of a rating is that the investor is solely responsible for assessing the bond’s creditworthiness. To compensate for greater complexity and information risk involved with these bonds, however, they typically pay investors a higher yield compared to rated issuers of similar quality.

Many financially healthy municipalities may choose to forego a credit rating at time of bond issuance. In fact, 34% of the 200,000 municipal bonds issued from 1998 to 2017—or 14% of the $3.7 trillion in par value—did not obtain a credit rating from an NRSRO.3 On the secondary market, unrated bonds, which by definition are considered noninvestment grade, currently comprise approximately two-thirds of the S&P Municipal Bond High Yield Index based on number of constituents.4

Issuers may forego ratings for a number of reasons, with cost often the predominant consideration. Issuers must pay a fee to the agency for its rating and also typically incur additional costs associated with preparing information for the agency. Small offerings—which are not unusual in the muni space—may find the expense of a rating prohibitive relative to the proceeds raised.

Additionally, as financed projects develop and progress and municipalities generate higher revenues from a diversified tax base, risk often recedes and issued bonds may appreciate in price. Moreover, upon achieving certain development and revenue milestones, issuers may be able to refinance (or “refund” in muni parlance) the bonds, potentially with an NRSRO rating, and at a lower interest rate.

Unrated Bonds May Offer Opportunities for Skilled Investors

Not all speculative bonds are created equal, and the differentiated risk/reward profile of unrated bonds may offer opportunity for investors willing to undertake deep credit analysis. While a typical unsecured corporate bond is backed only by the issuer’s creditworthiness and a contractual obligation to repay, municipal bonds—including unrated issues—generally include structural enhancements to bolster risk profiles. General obligation bonds, for example, are backed by the full faith and credit of the issuing municipality, which includes its taxing power. Revenue bonds are linked to income streams generated by specific projects or public works, such as those generated by a toll road or hospital.

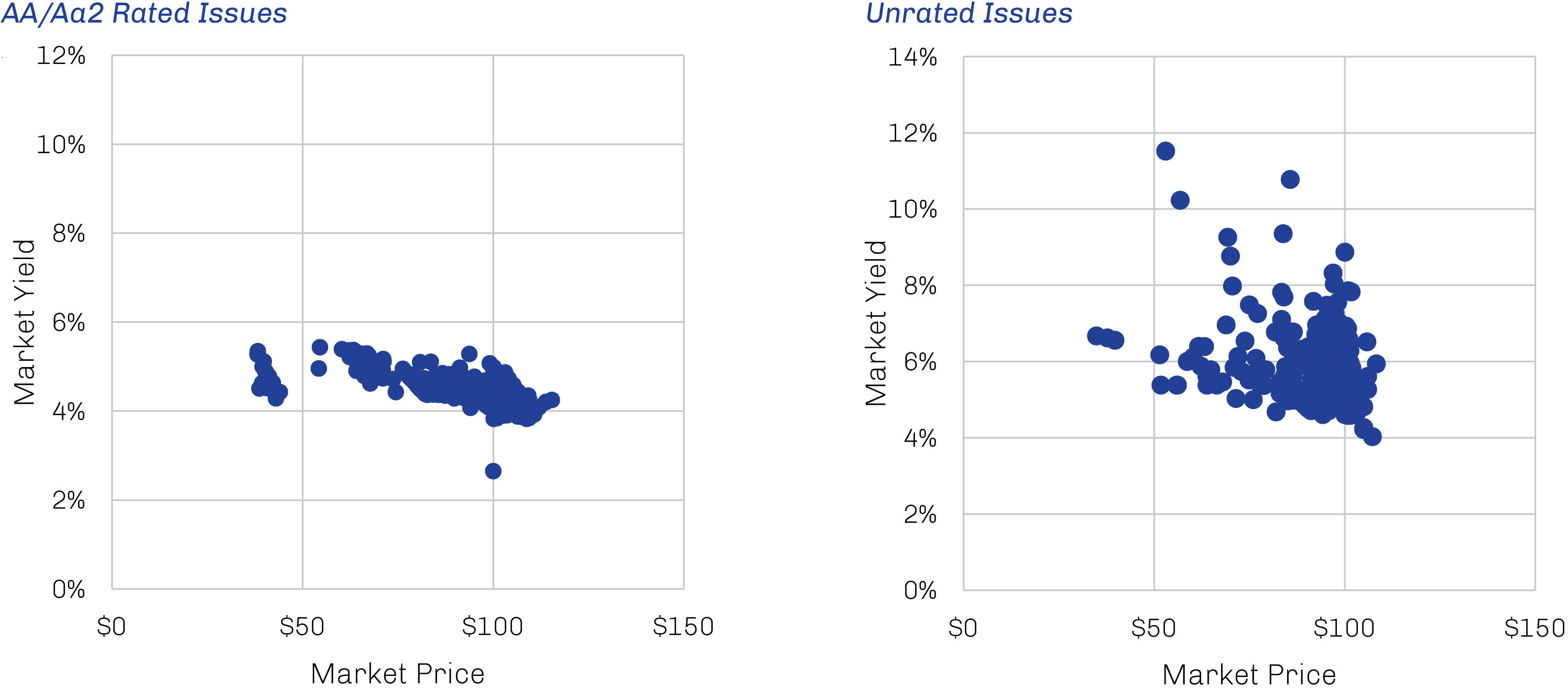

Dispersion presents potential to identify unrated bonds with favorable yields relative to credit quality and default risk.

Reflecting the deeper financial resources of their issuers, high yield municipal bonds have a far lower historical default rate than comparable corporate issues: just 0.9% for the period 1970 through 2024 on a trailing 12-month basis compared to 2.4% for similarly rated corporates.5

In light of historically low default rates and often attractive risk-return profiles, independent credit work on nonrated munis may be especially rewarding. Further enhancing the value proposition is the significant dispersion of yields and prices for similar unrated bonds—as demonstrated in Exhibit 1—which presents skilled credit managers with ample potential to identify bonds with favorable yields relative to credit quality and default risk.

Exhibit 1. Significant Price and Yield Dispersion Exists Among Individual Credits

Comparison of Bonds in the S&P Municipal Yield Index with 2044 Maturities

Source: Perform; data as of September 30, 2025.