Macro & Market Views

Liquid Real Assets: Powering the Pursuit of Real Returns

Liquid Real Assets: Powering the Pursuit of Real Returns

First Eagle’s commitment to seeking absolute, long-term returns across market cycles, disparate economic regimes and disruptive events often leads us to differentiated and overlooked areas of the investment universe.

- We find liquid real assets—a range of public companies involved with tangible assets as well as businesses that service the real economy—to be an underappreciated segment of the investment universe offering vaious potential benefits as a strategic portfolio allocation.

- Given their scarcity and critical role in the function of the global economy, real assets have demonstrated a measure of durability across cycles despite sensitivity to near-term cyclicality.

- We think potential structural trends like re-industrialization, the housing gap in the US and the energy transition may serve as a tailwind for certain businesses in the real asset space.

- It’s been our experience that the gold market sometimes serves as the metaphorical canary in the coalmine, sussing out potential dangers before they manifest in asset prices more broadly.

- Companies that own scarce, durable real assets and have competitive advantages may contribute to portfolio diversification while also generating relatively stable yields, helping reduce return volatility and potentially mitigating downside risk.

Among the more curious developments during first quarter 2024 was the concurrent new highs established by both equity markets and gold prices despite interest rates—both nominal and real—that persist at levels not seen since before the global financial crisis. High interest rates generally would be expected to weigh on equity valuation multiples, while the price of gold historically has been inversely related to changes in the real interest rate. Perhaps the most plausible explanation for this phenomenon is a fundamental shift to a higher rate of nominal drift in the global economy, the cause of which can be traced to the very large primary deficits currently facing many of its largest participants. In our view, the persistence of higher levels of nominal drift ultimately may result in multiple expansion for the resilient businesses well-positioned to benefit from it.

Imbalances Reveal Opportunities in an Underappreciated Space

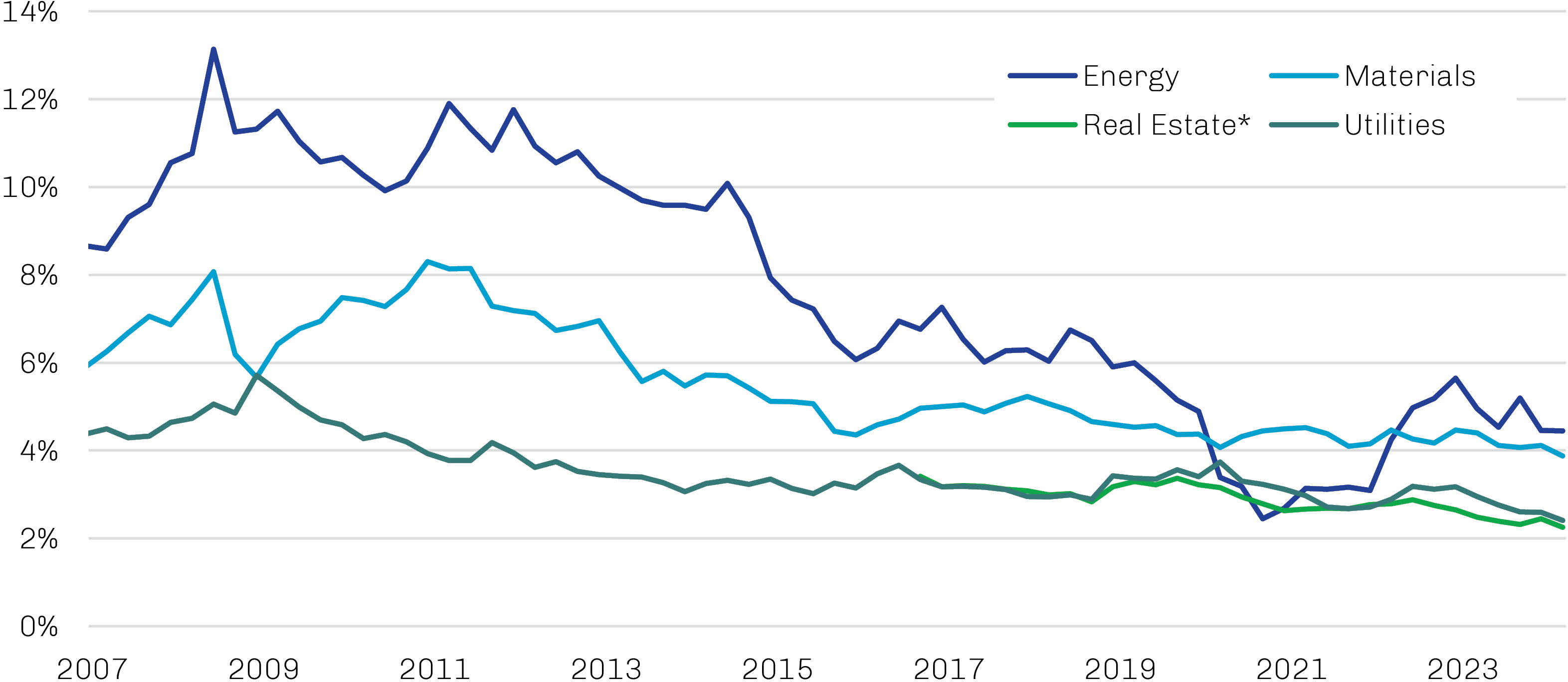

Encompassing a range of businesses in the energy, materials, real estate and utilities sectors of the equity market, real assets underpin the functioning of the real economy. So, it is perhaps not surprising that changes in the market valuations of these companies tend to ebb and flow with business cycles. The low inflation and interest rates and middling GDP growth that prevailed for most of the post-global financial crisis era weighed on the relative performance of these sectors, eating into their share of total equity market capitalization, as shown in Exhibit 1. Real assets sectors accounted for 13% of the MSCI World Index as of March 2024, down from more than 26% in June 2008.

Exhibit 1. The Contribution of Real Assets Sectors to Economic Growth Is Underappreciated by Equity Markets

Sector Weightings in MSCI World Index, January 2007 through March 2024

* Real estate became a headline GICS sector on August 31, 2016; previously, it had been part of the financials sector.

Source: MSCI; data as of March 31, 2024

Despite their shrinking presence in major equity indexes, real assets remain a key driver of global economic activity. For example, global gross capital formation—which measures additions to the fixed assets of the economy (like machinery, equipment, infrastructure and construction) plus net changes in inventories—stood at a modern-era high of around 28% of GDP at end-2022, up from a crisis-era bottom of 23%. In the US and much of the developed world, however, this metric remains below mid-2000s levels, as investment spending in certain “old economy” sectors that comprise much of the real asset space has lagged.1 This underinvestment may take years to correct in some cases, further bolstering the durable investment opportunities we discuss below.

Equity valuations for real asset businesses often track the nearer-term cyclicality of supply and demand, which can cause them to become disconnected from long-term equilibrium cash flows and replacement costs. We believe this dynamic presents opportunities to acquire attractive companies before the market fully appreciates the potential for periods of structural improvement. We explore three such disconnects below, noting the importance of a selective approach to investment within each; it’s been our experience that incumbent businesses typically are in an advantaged position to benefit from structural tailwinds, as physical scarcity anchors long-term cash flows while high and rising replacement costs and barriers to entry further support their long-term viability.

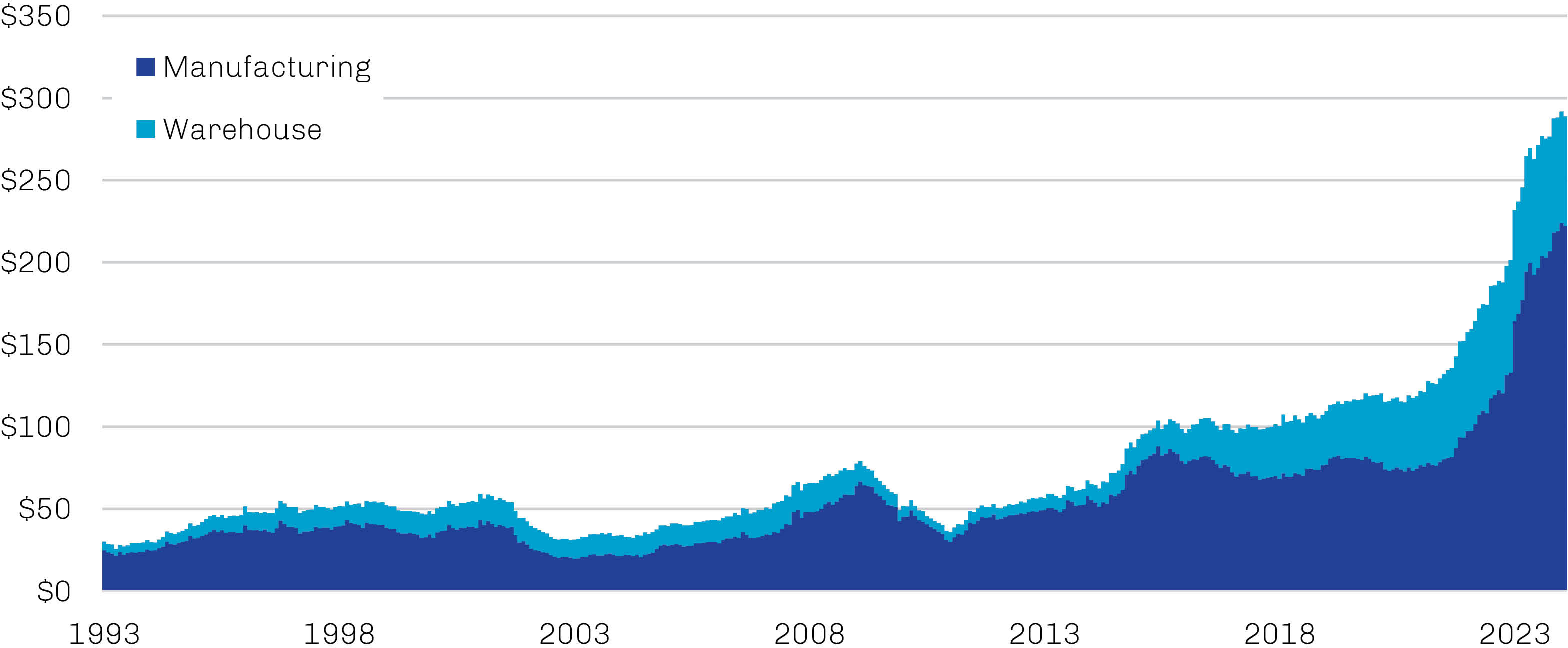

Reindustrialization in the West. The supply constraints that developed during the Covid-19 pandemic sparked a reevaluation of globalization’s risk/reward tradeoffs, with many governments and businesses in the Western world—particularly in North America—opting to diversify supply chains, including into locations closer to home. Meanwhile, increasing demand for high-intensity computing, with a focus on latency and data security, has driven a new wave of large-scale tech-infrastructure development and funding from government programs.2 This form of modern industrial activity is unique in its tendency to strategically locate in or close to end-markets. This near-shoring trend is evident in Exhibit 2, which depicts a spike in expenditures on US manufacturing and warehouse facilities over the past several years. We’ve also seen a pronounced uptick in such activity immediately south of the US border—highlighting a distinct reversal relative to prior decades—as vacancy rates in Mexican industrial properties have continued to decline, as shown in Exhibit 3.

Exhibit 2. Construction of Industrial Properties in the US Has Increased Dramatically Since the Onset of Covid-19

US Private Expenditures on Manufacturing and Warehouse Facilities in Billions of Dollars, Seasonally Adjusted,

January 1993 through February 2024

Source: US Census Bureau, Haver Analytics; data as of February 29, 2024.

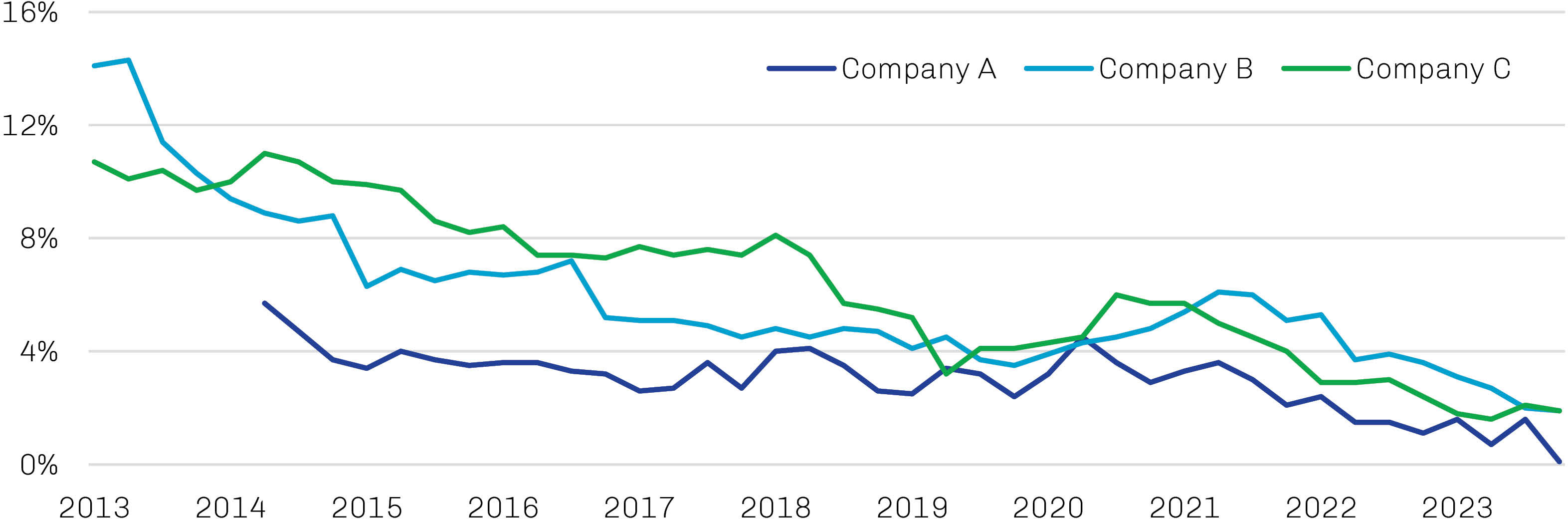

Exhibit 3. Domestic and Near-Shoring Demand in Mexico Has Spurred a Decline In Industrial Vacancy Rates South of the US Border

Industrial Portfolio Vacancy Rates of Select Mexican Property Companies, April 2013 through December 2023

* Real estate became a headline GICS sector on August 31, 2016; previously, it had been part of the financials sector.

Source: MSCI; data as of March 31, 2024

The primary beneficiaries of accelerated industrial infrastructure development include providers of building materials, especially those companies that dominate local markets with strong volumes and pricing power.

Distributors, processors and other service businesses— including metals processors and equipment rental companies—may also benefit from demand for the inputs needed to develop, operate and/or maintain new industrial capacity. Additionally, owners of better located incumbent industrial properties with lower cost bases and/or acquisition costs may be especially well-positioned as new structures are developed in inferior locations at higher costs. Increased user demand along with higher replacement values typically drive higher stabilized rents and cash flows to owners, as is the current dynamic in the southern US and in northern Mexico. Finally, the heavy energy requirements for new semiconductor production and computing capacity may require growth in energy infrastructure investments, benefiting service providers to those build-outs and select utilities with attractive regulatory frameworks.

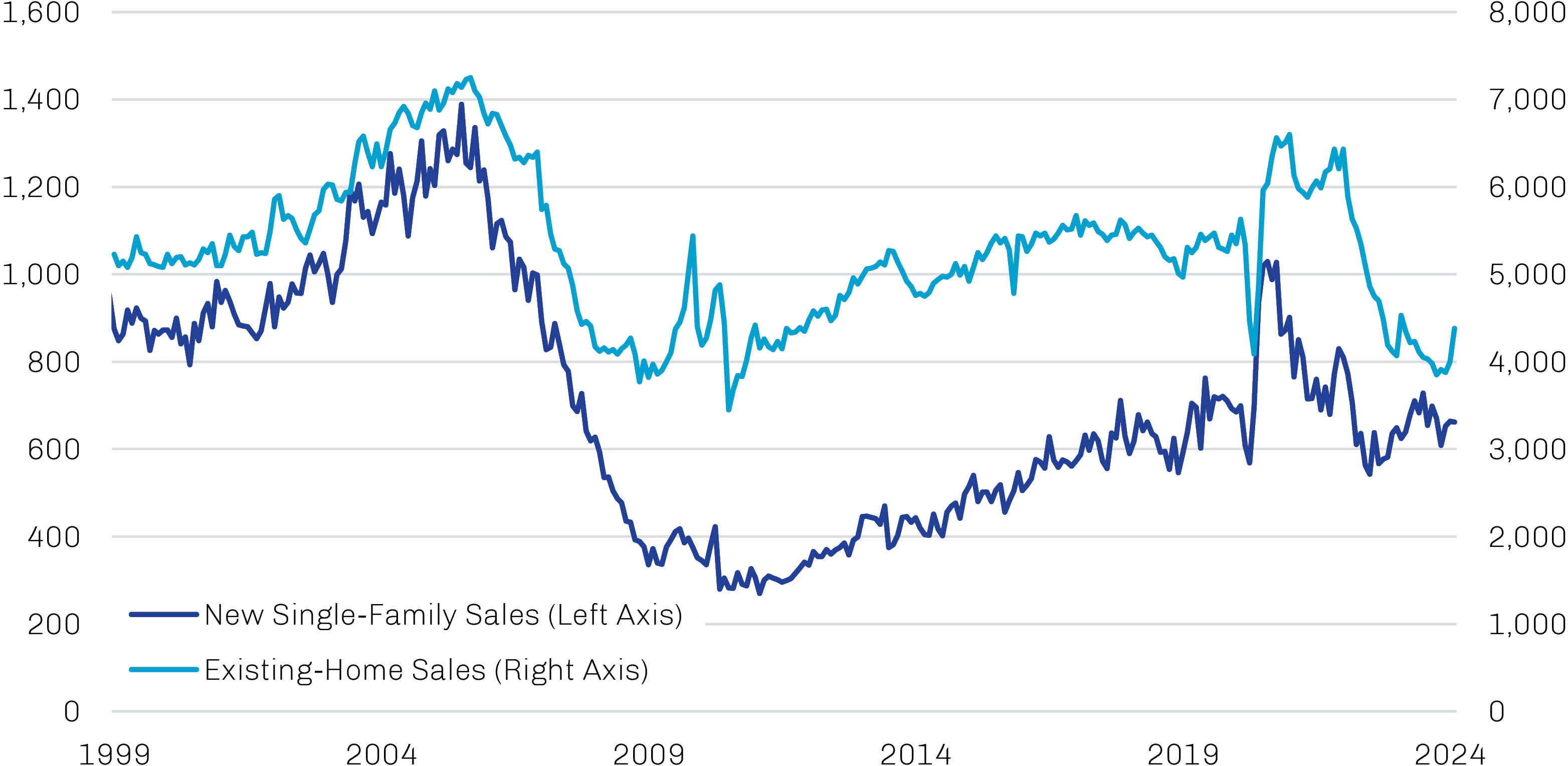

Housing shortages in select US markets. The US housing market continues to suffer from the aftershocks of the global financial crisis, and years of underbuilding relative to household formation has left the country with a sizable deficit of available single-family homes. This housing gap has only worsened in the years following Covid-19; as shown in Exhibit 4, a pickup in demand ultimately was stymied by supply-chain challenges that weighed on new-home construction and a subsequent sharp rise in mortgage rates that incented existing homeowners to stay put. New-construction costs remain high, and the stock of permitted, build-ready lots is low.

Exhibit 4. The US Housing Market Remains Undersupplied

US Housing Transactions in Thousands, Seasonally Adjusted, February 1999 through February 2024

Source: US Census Bureau, National Association of Realtors, Bloomberg; data as of February 29, 2024.

Limited single-family housing supply combined with high replacement costs and continued demand may provide potential opportunities for real asset investors. Construction-related businesses—including both homebuilders and the companies that provide products and services to them—are obvious beneficiaries of the need for additional housing, and the latter also may see increased activity from the renovation and maintenance of the existing stock of homes. Additionally, businesses that own and operate single-family housing portfolios may see the value of their underlying assets benefit directly from inflationary tailwinds. Multifamily operators may also benefit over time, though the heightened wave of supply ignited by Covid-19 and financing issues created by a combination of oversupply and higher interest rates may dampen their near-term prospects, particularly in lower-barrier markets in the southern US. Some of these multifamily owner-operators can further enhance value through active portfolio management while taking advantage of valuation gaps between public and private markets as they occur.

In contrast with the above, depressed housing-transaction activity may temporarily weigh on the revenues of self-storage facilities, for whom aggregate household movement is a meaningful driver of marginal demand.

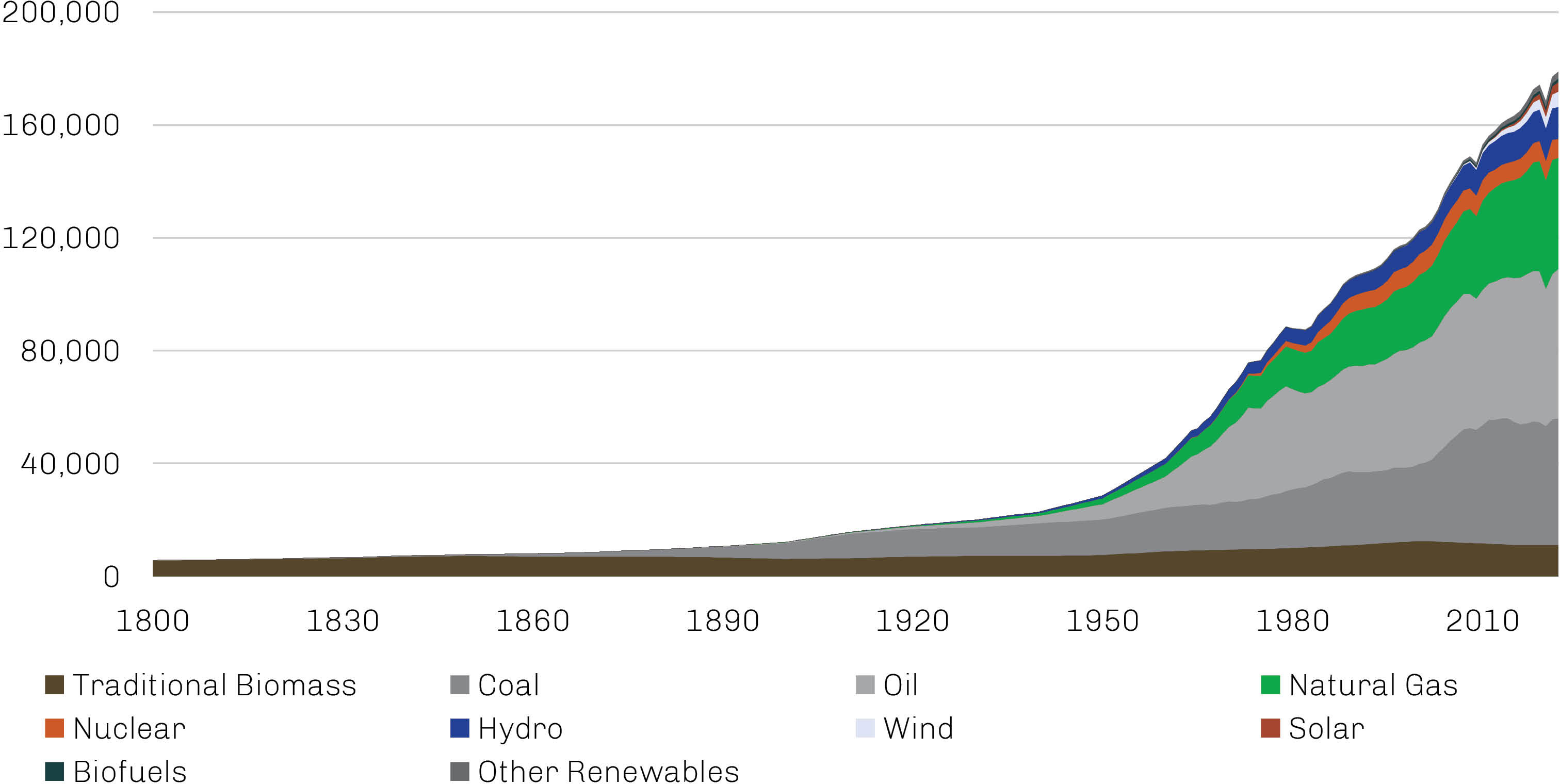

Decarbonization efforts globally. Energy transitions historically have been very long-duration events, as shown in Exhibit 5, and there’s no evidence to suggest the current transition from carbon-based fuels to renewable energy sources will be any different. As global energy consumption continues to expand with population growth and increased economic activity, especially in developing economies, it seems likely the world will need to balance the availability of both traditional and renewable forms of energy. Such a scenario suggests that fossil fuels may be needed to bridge the gap to a greener future and that fade risk for legacy producers may be over-discounted by markets.

Exhibit 5. Past Energy Transitions Have Evolved Over Decades

Global Energy Consumption by Source in Terrawatt Hours, 1800 through 2022

Source: Thunder Said Energy, BP Statistical Review, Vaclav Smil; data as of December 31, 2021.

Ongoing demand for fossil fuels for decades to come likely will benefit legacy energy businesses in possession of scarce, vital assets that are well positioned on the cost curve. This includes majors that are the primary suppliers of liquefied natural gas; midstream companies with infrastructure essential to the processing, transportation and storage of oil, gas and natural gas liquids; and service businesses helping to maximize productivity, detect and minimize methane emissions, and equip the energy industry with the latest emerging technologies. These legacy companies may be further bolstered by industry consolidation, which can offer opportunities for improvements in operational efficiency across the energy value chain.

Even as demand for traditional fossil fuels may continue, the global shift from internal combustion engines to battery-powered electric vehicles could require a significant increase in the long-term production of minerals essential to their production, such as copper, lithium and nickel. A selective approach to evaluating operators of established, low-cost mines in possession of the future’s key bottleneck materials may be rewarding, especially if rising social and regulatory barriers to new capacity increase its incremental cost.

Another long-term beneficiary of decarbonization may be businesses focused on improving the energy efficiency of buildings, which are responsible for a material portion of aggregate energy consumption (including, for example, 40% of all energy use in the US).3 Opportunities could include manufacturers of advanced temperature control devices and electrical systems as well as manufacturers and service providers of insulation materials. Increased socially driven conservation efforts combined with tightened regulatory standards could be an additional tailwind for these businesses.

Liquid Real Assets May Provide Durable Resilience at an Attractive Price

Though equity market indexes established a series of new record highs in recent months on expectations of a Federal Reserve pivot, we remain cautious about the soft-landing narrative. Further, there are a number of other factors—including ongoing fiscal profligacy and geopolitical discord—that may at some point inspire a significant recalibration of risk appetites in the markets and promote increased interest in assets with a track record of cross-cyclical resilience.

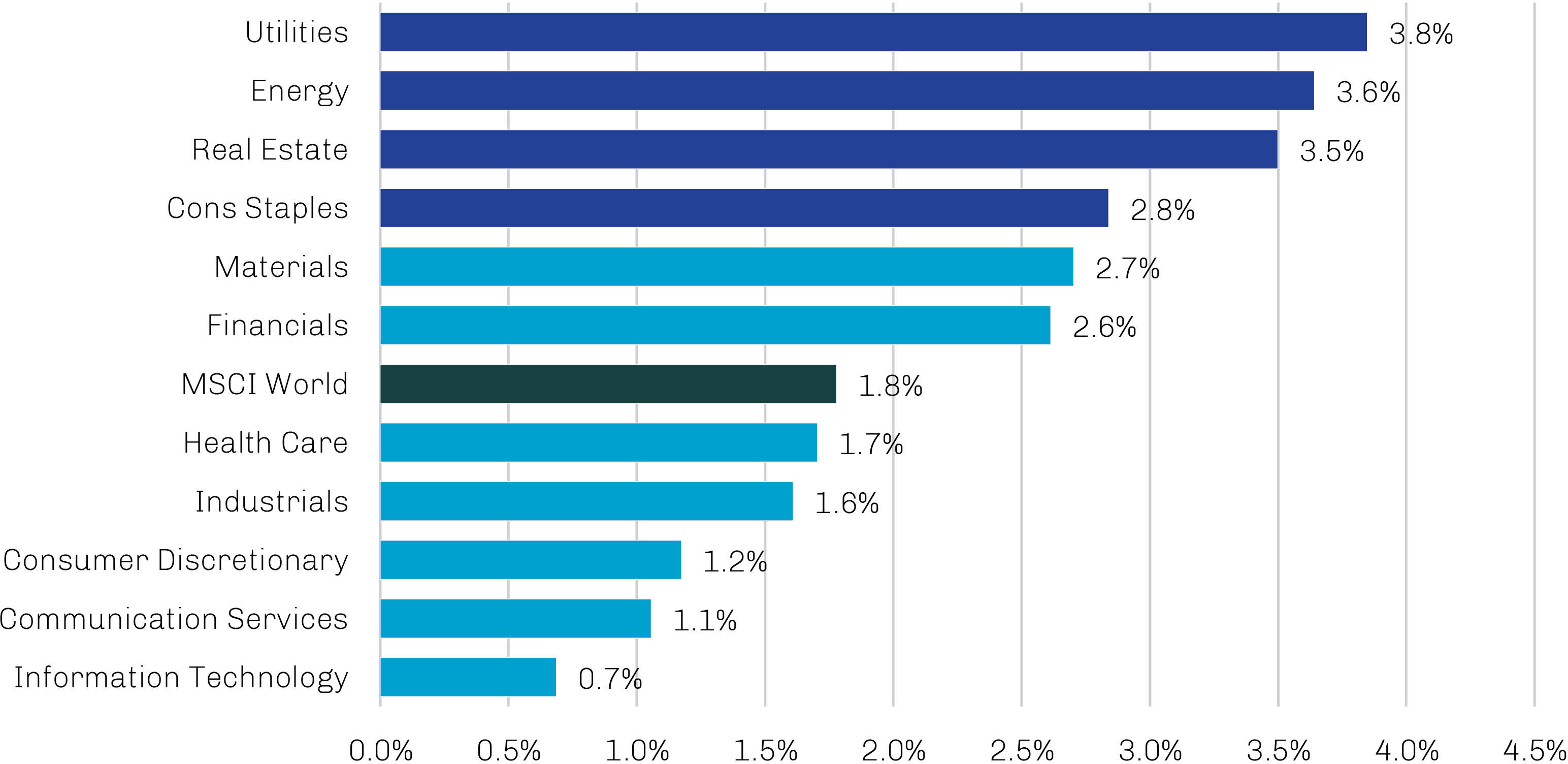

In such an environment, we continue to believe that real assets represent an attractive strategic allocation. The importance of physically scarce hard assets to the real economy anchors their intrinsic replacement value and supports the long-term cash flows of the companies that control them. Historically, this has promoted relatively low correlations to broad equity markets alongside relatively attractive yields, which may help reduce volatility of return and potentially mitigate downside risk, as shown in Exhibits 6.

Exhibit 6. Real Assets Offer Enhanced Potential for Attractive Real Yields

Dividend Yield of MSCI World Index Sectors

Source: FactSet, MSCI, S&P Dow Jones, FTSE, Bloomberg; data as of March 31, 2024.

Further, we think targeting high-quality publicly traded real assets companies may represent the most effective way to gain exposure to these assets at attractive prices. It’s been our experience that the best incumbent businesses in the real asset space typically exist in the public, rather than private, markets, as some are too large to be practically owned in nonpublic format or are simply constrained by the scarcity of the underlying real asset. This includes, for example, companies involved in infrastructure (e.g., major railroad networks), natural resources (e.g., owners of very large and low-cost mines and oilfields) and property (e.g., highly scaled real estate operating platforms). Enhanced access to capital for publicly traded companies also allows many listed real asset businesses to maintain more conservative levels of financial leverage than some private companies. An active approach to publicly traded real asset companies affords investors the potential to purchase interests in these businesses at times when they trade at a discount to “intrinsic value” and potentially achieve sound risk-adjusted returns over time.4