Macro & Market Views

Digging Deep: Lower Middle Market Direct Lending

Digging Deep: Lower Middle Market Direct Lending

The direct lending industry has evolved alongside the shifting dynamics of the marketplace.

- A volatile interest rate environment in recent years has weighed on M&A activity, the primary driver of demand for middle-market loans. While the start of a Fed rate-cut cycle may serve as a tailwind for direct lending in general, First Eagle Alternative Credit believes the sweet spot of opportunity remains with smaller, sponsored borrowers.

- With deal volumes sluggish, some larger alt credit vehicles have targeted the very large deals that in the past had been the province of broadly syndicated loans. We believe such an approach may introduce additional risks.

- First Eagle Alternative Credit believes the lower middle market continues to offer private lenders and their investors the most attractive combination of yield, leverage and structure at deal sizes that facilitate diversification across multiple borrowers and industries.

- In our view, asset-based lending facilities—rigorously underwritten and secured by specific assets of the borrower—represent an attractive complement to traditional middle-market loans backed by cash flows.

Nonbank lenders emerged in earnest in the aftermath of the global financial crisis, as a stricter regulatory environment limited the ability of banks to provide liquidity to middle-market corporate borrowers. While continuing to serve this cohort, alternative lenders have remained attuned to other needs going unmet by traditional providers; notably, some private credit firms in recent years have targeted their bulging capital stores on large deal sizes more typically associated with broadly syndicated loans.

Though merger and acquisition (M&A) activity—the lifeblood of the direct lending pipeline—has been sluggish amid the volatile interest rate environment of the past two years, First Eagle Alternative Credit believes the lower middle market continues to offer private lenders and their investors the most attractive combination of yield, leverage and structure, at deal sizes that facilitate investor diversification across borrowers and industries. Whether or not deal activity accelerates in the near term, we believe it’s likely there will still be opportunities to generate good risk-adjusted returns in the lower middle market when the right borrower, sponsor and lender converge.

High and Volatile Interest Rates Have Curtailed Private Credit Origination

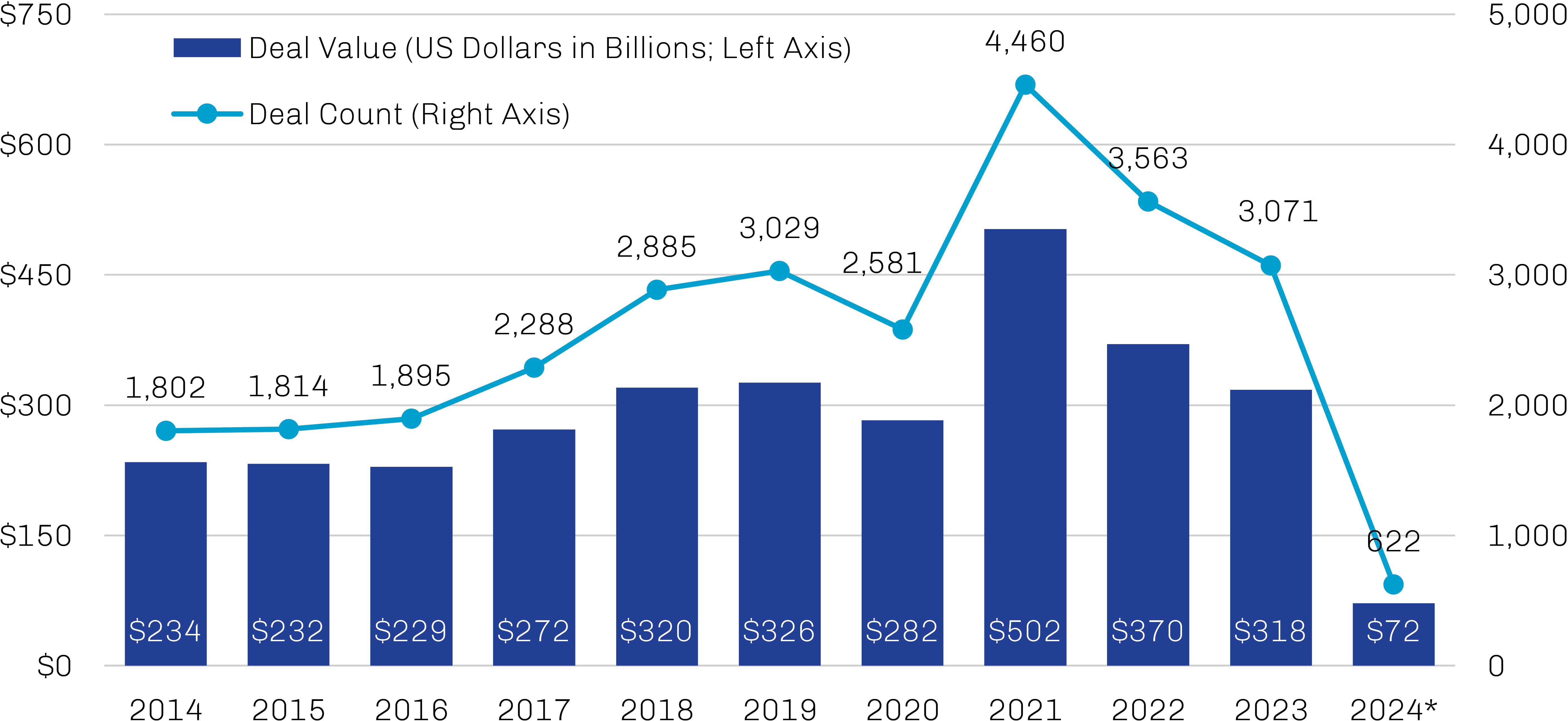

Significant rate volatility has prevailed since the Federal Reserve began its aggressive rate-hike cycle in 2022, as markets have sought to divine the duration and trajectory of Fed tightening and the odds that the central bank would be able to tame inflation without tipping the economy into recession (the much-desired “soft landing”). Not surprisingly, this uncertain rate backdrop has not been conducive to the M&A activity that serves as a major feeder to the direct lending pipeline. Private equity dealmaking, by both count and value, has declined sharply from its 2021 peak, as shown in Exhibit 1.

Exhibit 1. Weak Private Equity Deal Flow Has Weighed on Direct Lending Volumes

US Private Equity Middle-Market Deal Activity, 2014 through June 2024

* Year-to-date through June 30, 2024.

Source: Pitchbook | LCD; data as of June 30, 2024.

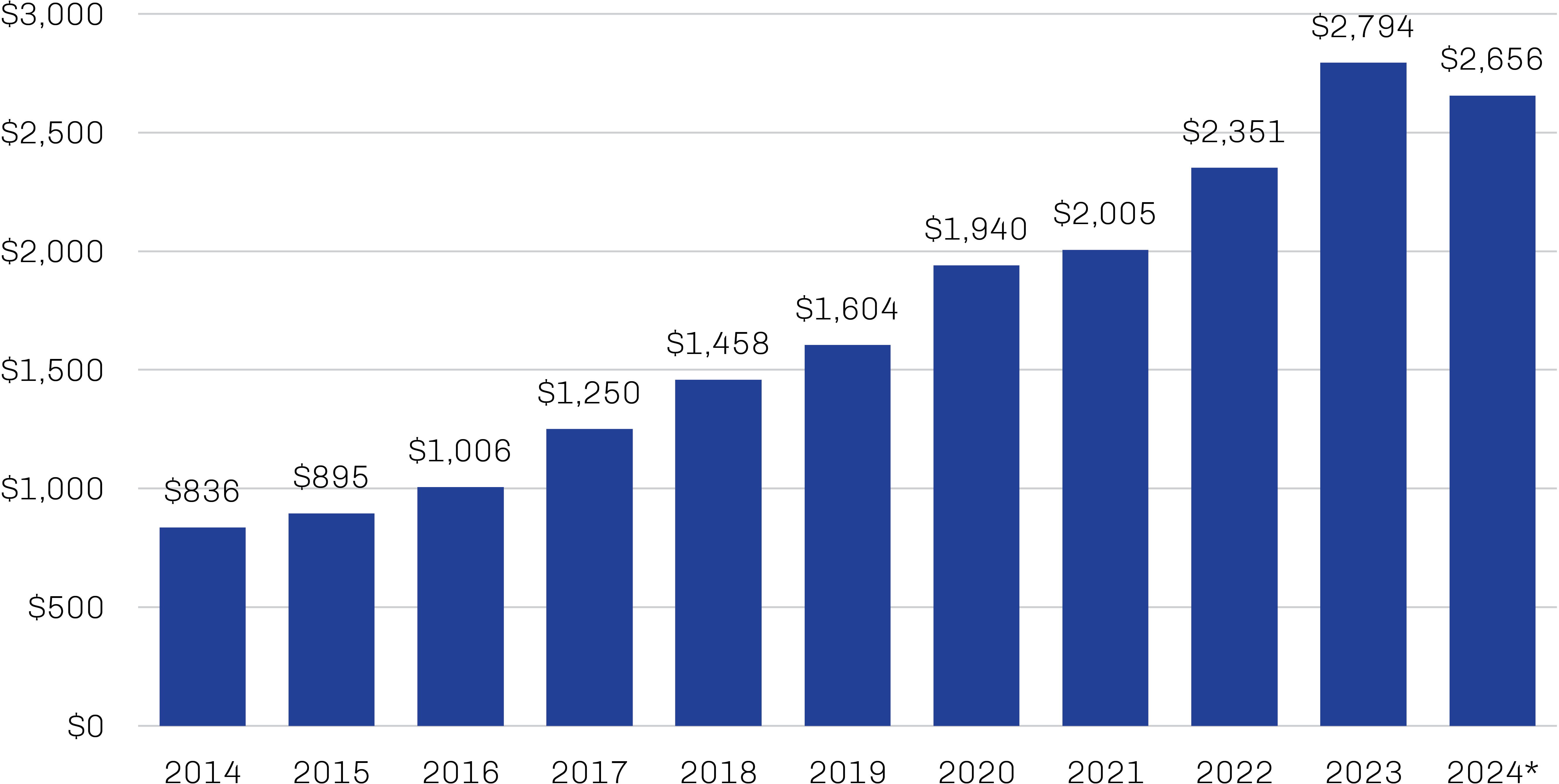

With the Fed having begun to lower its policy rate in September 2024 amid cooling inflation and a stillstable economy, however, a dealmaking inflection point may be at hand. The potential release of pent-up M&A energy bodes well for new-loan volumes ahead, especially given the amount of dry powder waiting for a target. As illustrated in Exhibit 2, deploying the current level of private equity dry powder to fund buyouts—at a conservative loan-to-value ratio of 50%—could unlock $2.7 trillion of private credit demand.

Exhibit 2. Massive Stores of Private Equity Dry Powder May Support Direct Lending Pipeline

US Private Equity Dry Powder in Billions of US Dollars, 2014 through June 2024

* Year-to-date through June 30, 2024.

Source: Preqin; data as of June 30, 2024.

The Lower Middle Market Trifecta: Yield, Leverage and Structure

Unrated and lacking a secondary market, middle market loans offer investors complexity and illiquidity premia alongside credit premia, risks that can be mitigated through vigorous underwriting and structuring. Typically positioned at the top of the borrower’s capital structure, these senior-secured loans provide lenders first recourse on the borrower’s assets in case of default/restructuring, and a conservative loan-to-value ratio—often 30–50%—provides a substantial equity cushion. Strong documentation and traditional financial covenants are standard, and a floating interest rate minimizes duration risk. Additionally, directly originated senior-secured loans historically have exhibited low to negative correlations with traditional fixed income and only moderate correlation to equities, potentially offering portfolio diversification benefits.1

Notably, the substantially lower transaction volumes of the past two years have inspired a number of larger private lenders to put their ample capital stores to work by moving into deal sizes usually associated with broadly syndicated loans. These lenders have been able to take market share primarily by offering speed and certainty of funding during periods when more complicated financing structures have been bogged down in disruptions, such as the onset of Covid-19 in 2020 or the regional bank crisis in 2023.

We think this approach holds risk for investors. In effect, these transactions refinance public debt as private debt, with the attendant decrease in liquidity for lenders but little or no change in the credit profile of the borrower. Moreover, the overwhelmingly covenant-lite nature of the syndicated loan market may creep into private structures as larger private lenders compete for these deals, undercutting what we view as one of the most appealing features of private lending.

While competitive pressures erode lenders’ negotiating power on larger loans, we believe the lower middle market continues to offer private lenders and their investors a more attractive combination of yield, leverage and structure, at deal sizes that facilitate investor diversification across borrowers and industries.

Within the lower middle market, we believe a sweet spot may be found among smaller sponsored loans to companies with annual EBITDA (earnings before interest, taxes, depreciation and amortization) of $5–50 million. In addition to sidestepping the competitive dynamics that erode pricing and structuring power in larger transactions, smaller loans tend to facilitate greater access to management teams, allowing for more comprehensive due diligence by lenders. Moreover, they encourage lender/borrower/sponsor relationships that are more collaborative than mercenary, an aspect that may encourage prompt remedial action—such as additional equity infusions from the sponsor or concessions from the lender in challenging times—adding another layer of downside mitigation.

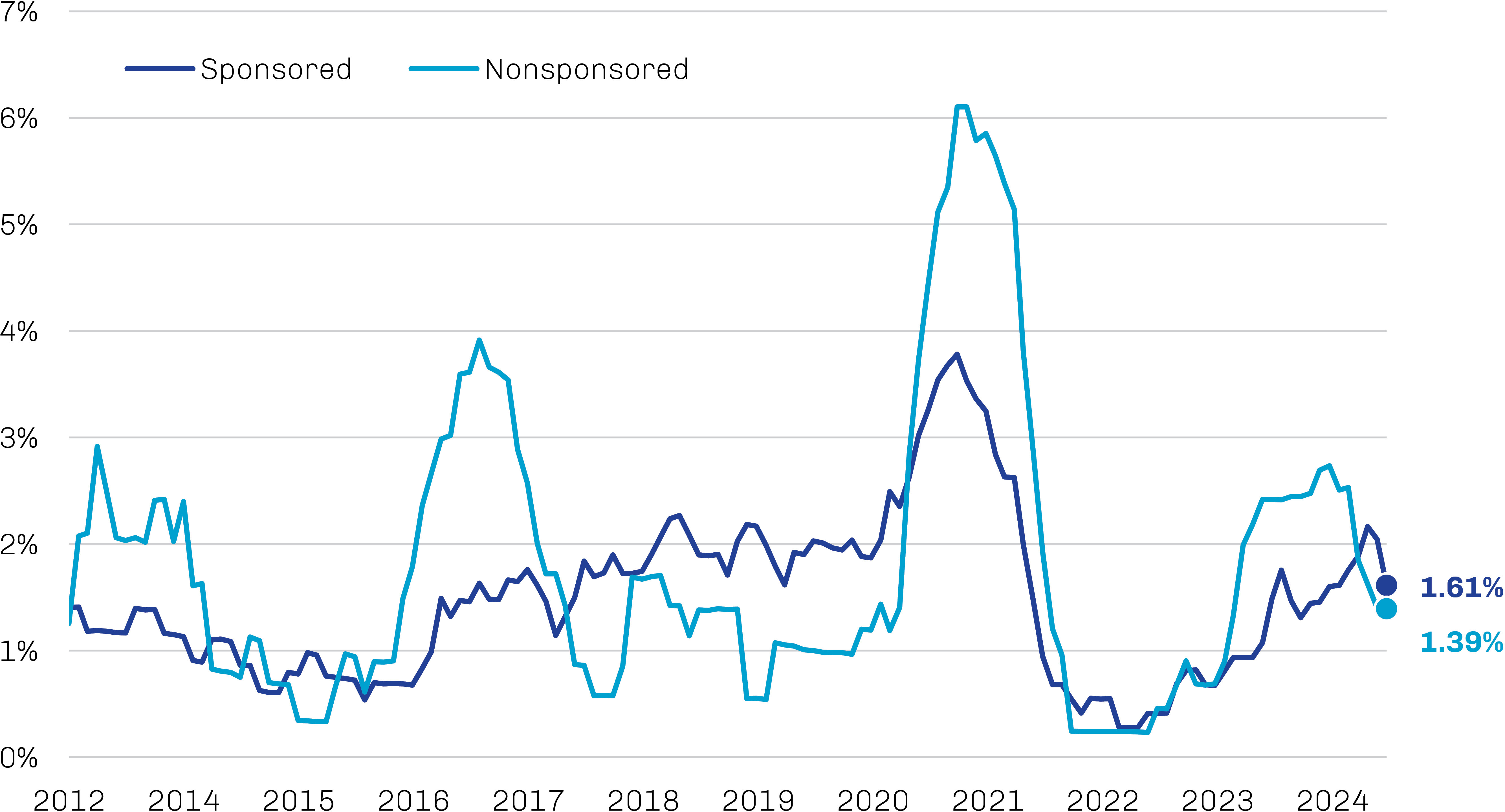

All in, sponsored loans historically have had significantly lower default rates during periods of stress (as shown in Exhibit 3) and higher recovery rates than nonsponsored deals.

Exhibit 3. Sponsored Loans Have Been Resilient During Periods of Stress

Sponsored and Nonsponsored Loan Default Rates by Issuer Count, January 2012 through June 2024

Source: Pitchbook | LCD, Morningstar; data as of June 30, 2024

Rigorous Underwriting and Strong Relationships Underpin Success

As rates decline and dry powder is unleashed, rebounding M&A activity could be a tailwind for direct lending to the lower middle market, particularly as private equity sponsors continue to look toward the space for more cost-effective platform opportunities in the face of rising valuations. In our view, the lower middle market currently has a more balanced supply/demand dynamic, providing managers greater opportunities for diversification on behalf of clients.

While we believe the lower middle market offers inherent advantages for nonbank providers of capital, success ultimately comes down to quality underwriting, structuring and portfolio construction. For us, that has meant targeting borrowers with stable historical earnings, strong cash flows and private equity sponsorship, often in growth industries with resilient businesses and deep management insights into broader industry trends. A first-lien position in the borrower’s capital structure—complemented by at least one financial covenant and/or liquidity test—is one source of potential idiosyncratic risk mitigation. Another is constructing broadly diversified portfolios comprised of a large number of smaller loans, which we believe is vital given the illiquidity of these assets.

In the end, direct lending is a relationship business. A lender’s ability to provide flexible financing solutions for sponsors without compromising its underwriting standards is among the ways it can add value to these relationships, supporting consistent deal flow over time.