BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

Following a strong 2025 for credit markets broadly, mounting headwinds in early 2026 prompted a sharp increase in volatility and a repricing of risk. Conditions during the first quarter were reminiscent of second quarter 2025, with concerns about the potential disruption of artificial intelligence (AI) and the war with Iran replacing tariffs as the primary headwinds and sources of uncertainty.

While spending and earnings growth appear to be resilient in the face of ongoing economic uncertainty and spiking energy prices—perhaps due in part to outsized tax refunds paid out this year1—we remain wary of the K-shaped economy in which activity increasingly becomes dependent upon upper-income households, as well as tech-oriented businesses. In corporates, we see meaningful bifurcation between higher and lower quality names and a similar story in the consumer segment where strain exists amongst the lower-income consumers, such as the growing use of credit cards to cover essential expenses and troublingly high auto loan and lease delinquency rates.2, 3

We continue to see signs of strain among lower-income consumers and lower-quality credits.

We believe caution remains appropriate. By prompting what appears to be the largest-ever physical supply disruption to world oil markets, the war with Iran has sent a stagflationary impulse to the global economy that, the longer it persists, is likely to weigh on economic growth while adding to inflationary pressures facing consumers. And while spreads in many credit assets are wider than where they began the year, spread compensation remains compressed on a historical basis, particularly for the good-quality credits we seek in today’s highly uncertain environment.4

Is Energy Volatility the New Normal?

Portfolio Manager and Senior Research Analyst

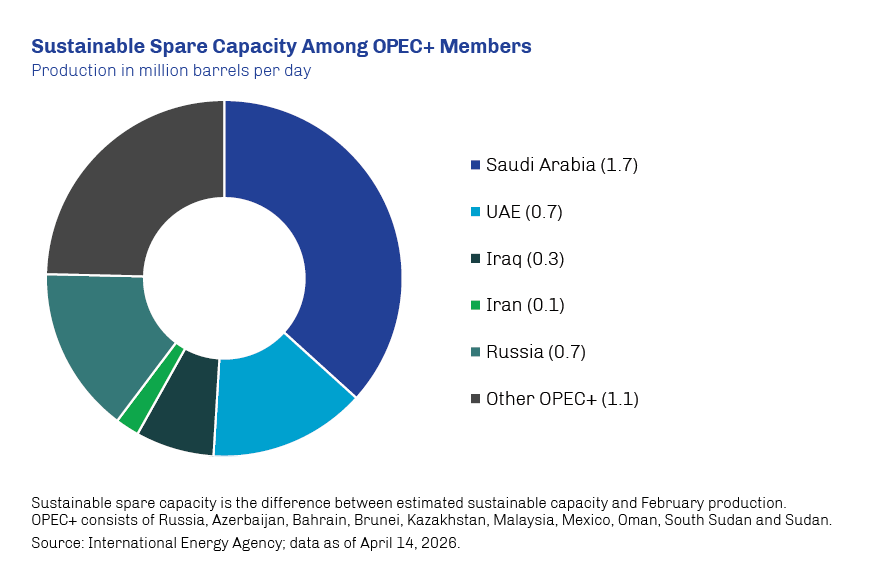

The recent announcement from the United Arab Emirates (UAE) that it will exit the Organization of Petroleum Exporting Countries (OPEC) on May 1 highlights the growing supply vulnerability and persistent volatility of the global oil market.

Founded in 1960 by Iran, Iraq, Kuwait, Saudi Arabia and Venezuela, OPEC was created to coordinate production and manage global oil prices. Driven by strategic national interests and a desire to increase production, the UAE’s departure will reduce the cartel’s ability to steady the global oil market, in our view. In addition to having meaningful spare production capacity, the UAE is also able to reroute oil transportation through the Abu Dhabi Crude Oil Pipeline directly to the Port of Fujairah on the Gulf of Oman, thereby bypassing the blockages at the Strait of Hormuz.1

We believe this latest development is a reminder why oil, the world’s most consumed commodity, has value as a potential geopolitical hedge and why energy security is paramount to government interest as geopolitical tensions escalate.2 The recent string of geopolitical shocks shows that volatility is not just a short-term event risk. With numerous geopolitical conflicts since the formation of OPEC, we think ongoing disruptions—such as attacks on infrastructure and disrupted transportation routes—are likely to persist. This ongoing risk reinforces the critical importance of reliable and secure sources of energy. While not immune to the impact of global oil prices, we believe recent events highlight the value of energy production in the US and Canada, which are linked by dozens of pipelines and transportation routes.

Within the energy sector, we continue to favor global integrated energy companies and service businesses that operate across stable jurisdictions and have the logistics scale to keep product moving when trade routes are disrupted. In our view, these companies are better positioned to maintain production and distribution in an increasingly uncertain landscape.