BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

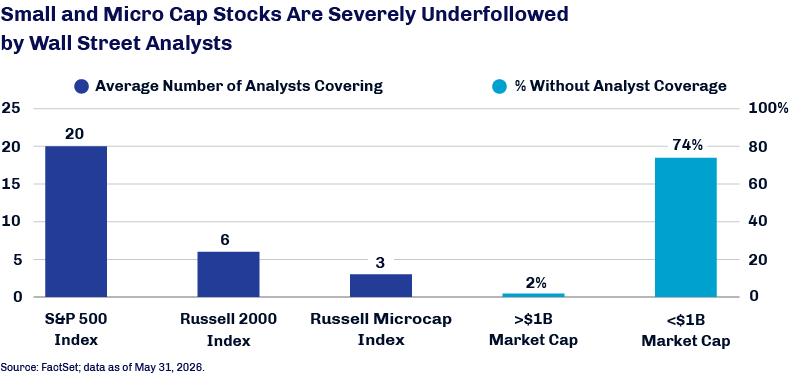

Boring Is Beautiful: Opportunities in Small Companies

Portfolio Manager, Diamond Hill Capital Management

Everyone wants to admire the cathedral. Nobody wants to talk about the quarry.

We remember the soaring ceilings, stained glass and architect’s genius. We rarely celebrate the people extracting stone, hauling it across mud and doing the unglamorous work that makes grandeur possible. Markets behave similarly. They celebrate the glamorous endpoint and ignore the grubby prerequisites. Yet the quarry owner, not the dreamer with a sketchpad, is often closer to the cash flow.

In small and micro cap investing, many of the most compelling opportunities exist far upstream from where attention naturally concentrates. However, markets frequently reward narratives before economics, directing attention toward businesses tied to disruption, rapid growth or a compelling story that often attract disproportionate investor attention. Wall Street has always preferred the chandelier to the invoice for concrete.

Often found in industries viewed as mundane—limestone, coatings, cement or industrial minerals—these businesses may be overlooked precisely because they sound ordinary. Yet businesses built around scarce physical assets, regional scale, regulatory barriers or operational discipline can possess exactly the qualities long-term investors should value: durable competitive positions, rational industry structures and opportunities to reinvest capital over many years. A mineral reserve, terminal network, processing facility or regional service footprint may not inspire excitement, but when it is difficult to replicate, essential to customers and positioned in markets with steady demand, it can become a powerful economic advantage.

The cathedral may attract admiration. But over time, the quarry, the rail terminal and the mineral reserve may prove to be more durable economic assets.

In small and micro cap investing, that is often where long-term compounding begins.

After underperforming for what, to us, seemed like forever, small caps have finally demonstrated what consistently strong earnings can do for equity returns. The Russell 2000 Index has outperformed the S&P 500 Index by approximately 1,000 basis points year to date and is in what we hope is only the early stages of an extended redemption tour.1

While the macroeconomic and geopolitical backdrop remains unsettled, we believe there are a number of bright beacons to help guide small caps to success.

Continued earnings upswing. For the first time in a while, Russell 2000 Index earnings growth is projected to outstrip that of the S&P 500 Index for at least the next two years.2

Software-enabled efficiencies. Outsourced software and servicing solutions may provide resources for small companies to scale their operations, improve efficiency and facilitate the conversion of some costs from fixed to variable, easing the need for working capital.

AI-driven growth. Artificial intelligence (AI) may enable some small cap companies—including suppliers to infrastructure and data-center construction—to expand their customer bases without incremental spending on research and development, underpin¬ning both top-line growth and margin expansion. Healthcare and consumer goods companies could conceivably see even greater benefits from AI through enhanced development of premium products that drive pricing power.

Policy and economic tailwinds. A more benign regulatory environment may spur mergers and acquisitions activity, while reindustrialization and reshoring trends could be of benefit to smaller domestic-focused businesses.

A resurgent IPO market. With free money a thing of the past, private equity sponsors may be incentivized to monetize their investments through initial public offerings (IPOs). Increased liquidity and investor focus on private-to-public marks could more broadly enhance valuations and performance for publicly traded small cap companies overall.