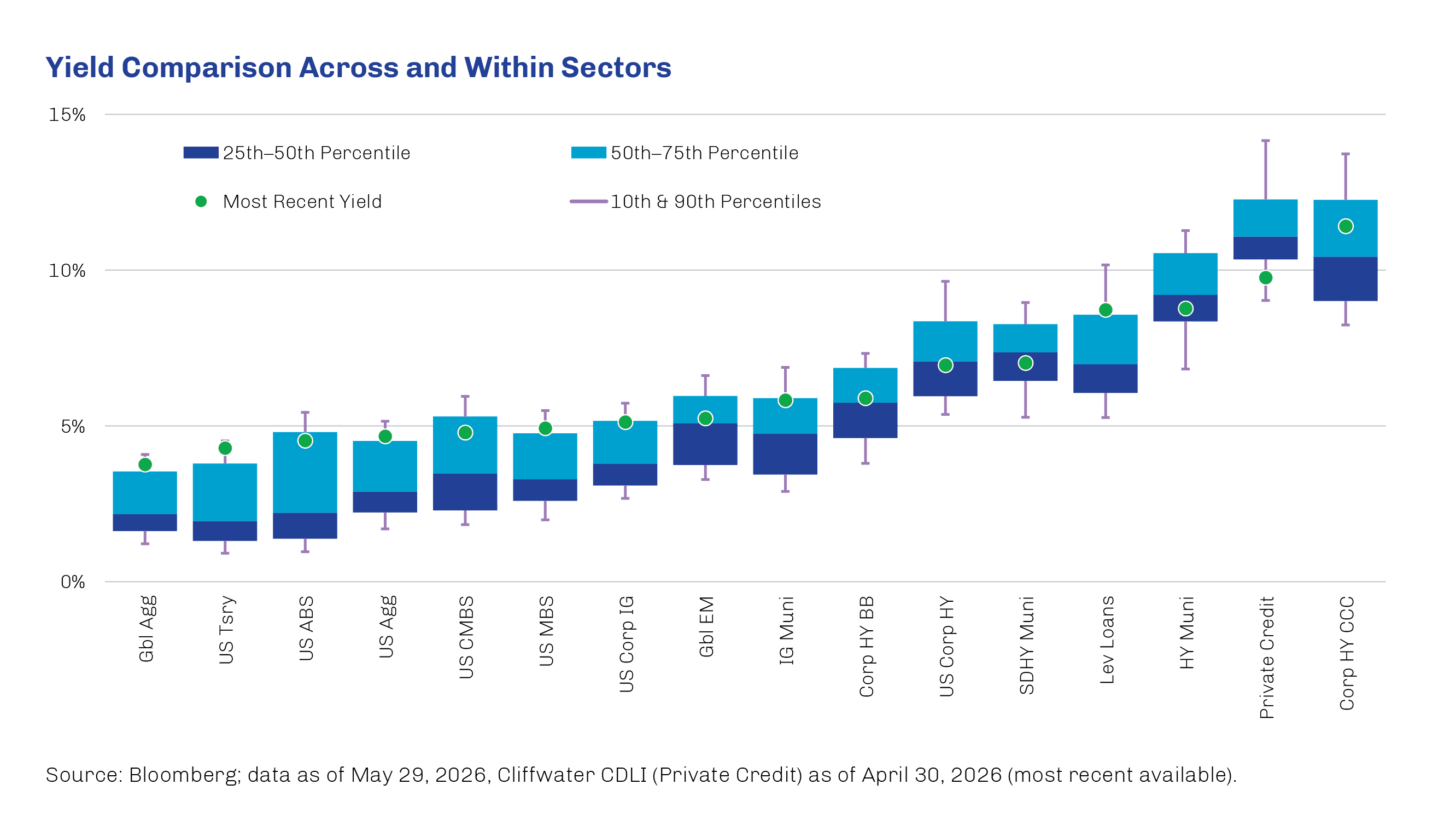

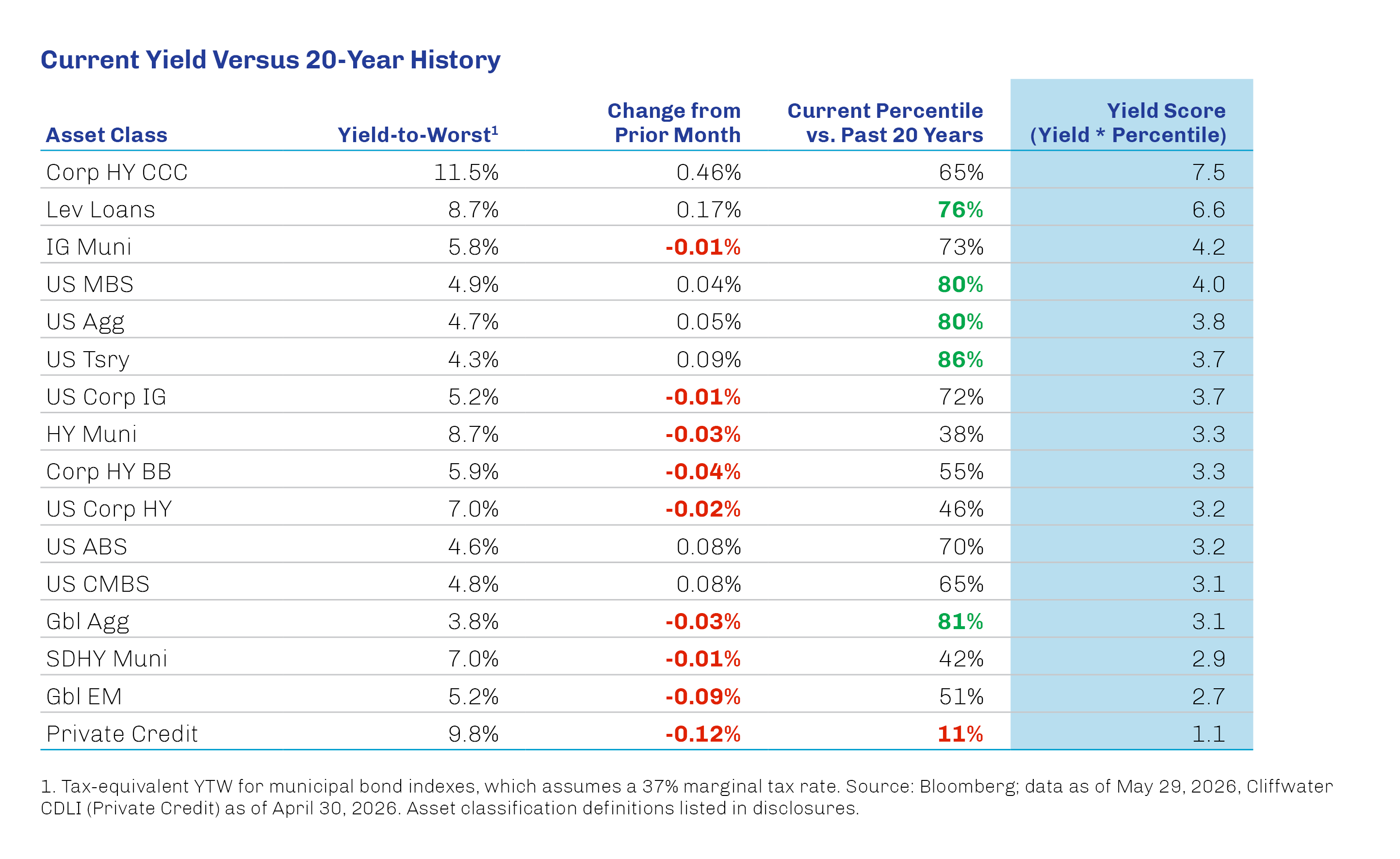

1, 2, 3, 4, 5 Bloomberg; data as of May 29, 2026.

The information contained in this material is provided by First Eagle Investment Management, LLC (“FEIM”) and its global subsidiaries (collectively, “First Eagle”). FEIM is an investment adviser registered with the US Securities and Exchange Commission (SEC). Registration with the SEC does not imply a certain level of skill or training.

This material is for informational purposes only and reflects prevailing conditions and the judgment of the author(s) as of the date of publication, all of which are subject to change. This material should not be relied upon as investment advice; it does not constitute a recommendation to buy or sell a security or other investment; and it is not intended to predict or depict the performance of any investment. This material is not being provided in a fiduciary capacity and is not intended to recommend any investment policy or investment strategy or consider the specific objectives or circumstances of any investor. We consider the information in this material to be accurate, but we do not represent that it is complete or should be relied upon as the sole source of appropriateness for investment.

Prospective investors should inform themselves and consult with an investment, tax or legal professional as to any applicable legal requirements, taxation and exchange control regulations in the countries of their citizenship, residence or domicile that may be relevant prior to investing.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

All investments involve the risk of loss of principal.

Municipal bonds are subject to credit risk, interest rate risk, liquidity risk, and call risk. However, the obligations of some municipal issuers may not be enforceable through the exercise of traditional creditors’ rights. The reorganization under federal bankruptcy laws of a municipal bond issuer may result in the bonds being cancelled without payment or repaid only in part, or in delays in collecting principal and interest.

Investments in bonds are subject to interest-rate risk and can lose principal value when interest rates rise, while they typically increase their principal values when interest rates decline. Bonds are also subject to credit risk, in which the bond issuer may fail to pay interest and principal in a timely manner, or that negative perception of the issuer's ability to make such payments may cause the price of that bond to decline.

Investments that are concentrated in a specific industry or sector may be subject to a higher degree of risk than funds whose investments are diversified and may not be suitable for all investors.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Asset-backed securities (ABS) are debt securities whose payments of principal and interest are backed by the cash flow generated by pools of income-producing credit assets.

CCC credit rating—as used by S&P Global Ratings and Fitch Ratings—is a speculative-grade rating on a bond considered vulnerable and dependent on favorable business, financial and economic conditions to meet its financial commitments. The equivalent rating from Moody’s Investors Service is Caa.

Commercial mortgage-backed securities (CMBS) are debt securities whose payments of principal and interest are backed by the cash flow generated by pools of commercial real-estate mortgage loans.

A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of credit worthiness of an issuer with respect to debt obligations, including specific securities, money market instruments, or other bonds. Ratings are measured on a scale that generally ranges from AAA/Aaa (highest) to D/RD (lowest); ratings are subject to change without notice. Not Rated (NR) indicates that the debtor was not rated and should not be interpreted as indicating low quality.

Duration is a measure of a bond price's sensitivity to changes in interest rates.

High yield bonds (also called junk bonds) are bonds deemed by rating agencies to have a higher risk of default and thus offer investors a higher interest rate than investment grade bonds.

Investment grade bonds are bonds deemed by rating agencies to have a relatively low risk of default.

Leveraged loans typically refer to floating-rate commercial loans provided by a group of lenders to a noninvestment grade borrower.

Mortgage-backed securities (MBS) are debt securities whose payments of principal and interest are backed by the cash flow generated by pools of mortgage loans.

Private credit refers to a loan agreement between a borrower and single or small group of nonbank lenders. Private credit can also be referred to as “direct lending” or “private lending.”

Securitized credit refers to bonds backed by pools of individual loans.

Taxable equivalent yield (TEY) reflects the pretax yield that a taxable fixed-income investment would need to offer to produce the same after-tax yield as tax-exempt security. The TEY shown is calculated based on the most common federal tax bracket(s).

US Treasury securities are debt instruments backed by the full faith and credit of the US government.

A yield curve is a graphical representation of interest rates on debt of equal credit quality across a range of maturities.

Yield to Worst (YTW) is a financial metric that helps investors assess the minimum yield they can expect from a bond under various scenarios. It accounts for the bond’s yield in the worst-case scenario, considering factors like call provisions, prepayments, and other features that may affect the bond’s cash flows.

Bloomberg Municipal Bond Index Total Return Index (Gross/Total) measures the performance of the US dollar-denominated long-term tax-exempt bond market, inclusive of state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg Muni High Yield Total Return Index (Gross/Total) measures the performance of non-investment grade US municipal bonds. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg Municipal High Yield Short Duration Index (Gross/Total) measures the performance of US high-yield municipal bonds with shorter maturities. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Treasury Total Return Index (Gross/Total) measures the performance of the US Treasury market. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg Global Aggregate Index (Gross/Total) measures the performance of investment grade debt from local currency markets worldwide. The multi-currency benchmark includes treasury, government-related, corporate and securitized fixed rate bonds from both developed and emerging markets. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Corporate Total Return Index (Gross/Total) measures the performance of investment grade, fixed-rate, taxable corporate bond market and is inclusive of US dollar-denominated securities publicly issued by US and non-US industrial, utility and financial issuers. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Corporate High Yield Total Return Index (Gross/Total) measures the performance of US dollar-denominated, high yield, fixed-rate corporate bond market. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg Ba US High Yield Total Return Index (Gross/Total) is a subset of the broader high yield index and measures the performance of bonds with a rating of Ba1/BB+. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg Caa US High Yield Total Return Index (Gross/Total) measures the performance of the lowest rated (Caa/CCC or lower) segment of the US high yield corporate bond market. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg Global Emerging Markets Sovereign Index (Gross/Total) measures the performance of sovereign debt issued by emerging market countries in hard currencies. A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US Agg ABS Total Return Index (Gross/Total) tracks US investment-grade asset-backed securities (ABS). A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg US MBS Index Total Return Index (Gross/Total) measures the performance of agency mortgage-backed securities (MBS). A total-return index tracks price changes and reinvestment of distribution income.

Bloomberg CMBS: Erisa Eligible Index (Gross/Total) measures the performance commercial mortgage-backed (CMBS) that are compliant with ERISA investment guidelines. A total-return index tracks price changes and reinvestment of distribution income.

S&P UBS Leveraged Loan index (Gross/Total) formerly named the Credit Suisse Leveraged Loan Index, measures the performance of the investable universe of the US dollar institutional leveraged loans. A total-return index tracks price changes and reinvestment of distribution income.

Cliffwater Direct Lending Index (Gross/Total) is an asset-weighted index of US middle-market direct loans. A total-return index tracks price changes and reinvestment of distribution income.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The information presented does not reflect the performance of any fund, strategy or account managed or serviced by First Eagle, and there is no guarantee that investors will experience the type of performance reflected. There is no guarantee that any market forecast set forth in this material will be realized. There is no guarantee that any historical trend referenced herein will be repeated in the future, and there is no way to predict precisely when such a trend will begin. The mention of specific securities is not a recommendation or solicitation to buy, sell or hold any particular security and should not be relied upon as investment advice.

Availability of the products or services described may be restricted by law in certain jurisdictions. This material may not be distributed, published or used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

United Kingdom

Napier Park Global Capital Ltd is authorised and regulated by the Financial Conduct Authority (FRN: 541427) in the United Kingdom.

Middle East

This material is for information purposes only and has not been, and will not be, registered with or reviewed or approved by any regulator located in the Middle East. It does not constitute or form part of any marketing initiative, any offer to issue or sell, or any solicitation of any offer to subscribe to or purchase, any products, strategies or other services, nor shall it, or the fact of its distribution, form the basis of, or be relied on in connection with, any contract resulting therefrom. In the event that the recipient of this material wishes to receive further information regarding any products, strategies or other services, it shall specifically request the same in writing from an authorized financial adviser.

Canada

Pursuant to the international adviser registration exemption in National Instrument 31-103, First Eagle Investment Management, LLC. is informing you that: (i) First Eagle Investment Management, LLC. is not registered in Canada and is advising you in reliance upon an exemption from the adviser registration under National Instrument 31-103; (ii) First Eagle Investment Management, LLC’s jurisdiction of residence is New York, USA; (iii) there may be difficulty enforcing legal rights against First Eagle Investment Management, LLC. because it is a resident outside of Canada and all or substantially all of its assets may be situated outside of Canada.

FEF Distributors, LLC (“FEFD”) (SIPC), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy or product.

First Eagle Investments is the brand name for First Eagle Investment Management, LLC and its subsidiary investment advisers.

First Eagle Alternative Credit and Napier Park are brand names for the two subsidiary investment advisers engaged in the alternative credit business.

© 2026 First Eagle Investment Management, LLC. All rights reserved.