BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

BLOGThe Bird's Eye View

Timely Perspectives, Unconventional Thinking

We’re excited to share timely market insights, thoughtful perspectives and expert commentary as part of our commitment to providing modern investment solutions to modern challenges.

Taxable Fixed Income Markets Update: April 2026

Client Portfolio Manager, Diamond Hill Capital Management

The war with Iran continued to dominate fixed income markets in April, with asset prices moving in conjunction with waxing and waning hopes for a swift end to the conflict. Though the month ended with the combatants in an extended cease-fire, a peace agreement has been elusive and the Strait of Hormuz remains effectively closed. Markets appeared to grow accustomed to this new normal, however, and spread assets in general delivered returns in excess of Treasuries.1

Treasuries and rates. The specter of a prolonged conflict with Iran weighed on Treasuries and sent yields higher across the curve. Given the war’s potential inflationary impact, longer-maturity bonds were the most effected; yields on 10- and 30-year Treasuries, for example, both moved to levels not seen consistently since the first half of 2025.2 Meanwhile, futures markets, which entered the year pricing in two or three fed rate cuts during 2026, now expect no policy rate action by the central bank.3

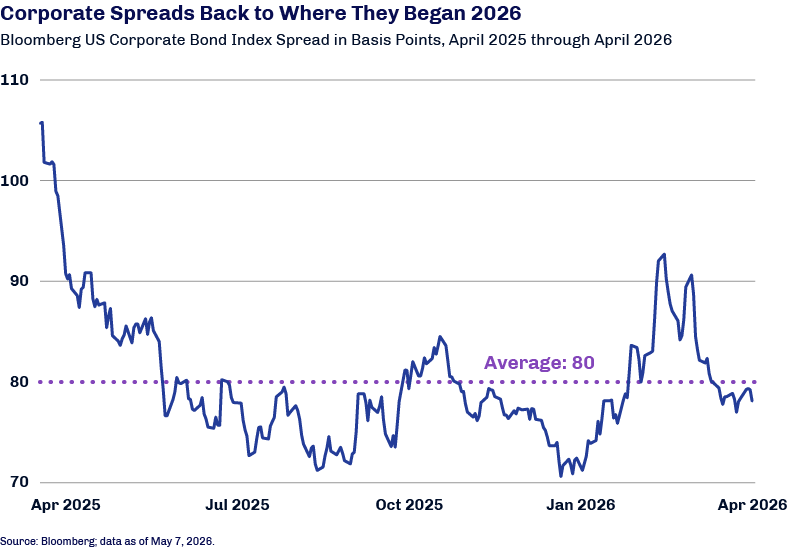

Corporate credit. Having spiked with the outbreak of hostilities with Iran, investment grade and high yield corporate spreads tightened to end-2025 levels during April as markets brushed off the challenging geopolitical environment. Both delivered strong excess returns relative to comparable-duration Treasuries.4 Corporate issuance across the credit spectrum remained robust during the month and is running more than 28% higher compared to year-to-date 2025.5

Securitized credit. As they did in other credit segments, securitized credit spreads tightened throughout April. Unlike other areas of the market, however, securitized credit spreads now sit tighter than end-2025 levels. Index-level performance returned to positive territory in April, helped by shorter-duration asset-backed securities. Though not part of the Bloomberg family of indexes, collateralized mortgage obligations were the top-performing sector of the securitized market.6

While central bank policy remained unchanged at Jerome Powell’s last meeting as chair of the Federal Open Market Committee on April 29, it drew dissents from four of the 12 voting members—the most since 1992. Three regional Fed presidents approved of the decision to hold rates steady but wanted to remove language they believe suggested an easing bias. Governor Stephen Miran, as usual, called for a rate cut.1

With the economy facing stagflationary pressures from the Iran war, tariffs and immigration policy, Powell hands over the reins of the central bank at a particularly challenging time.

Powell hands over the reins of the central bank at a particularly challenging time.

His successor Kevin Warsh, though widely viewed as a mainstream pick for the job, raised eyebrows during his recent hearings before Senate Banking Committee when he testified about his desire to promote “regime change” at the Fed. Details on his objectives were scarce, however, and many are contradictory. My expectation is that any operational changes under Warsh, whose term begins May 15, are likely to be gradual.

In a noteworthy break from historical precedent, Powell announced that he would stay on the Fed board as a governor when his term as chair ends. While chairs tend to resign in order to avoid overshadowing their replacements, Powell stated the he will leave the board only when the investigation into his handling of the Fed headquarters’ renovation, which now sits with the Fed’s inspector general, is “well and truly over, with finality and transparency.”2 I would not be surprised if Powell remained though year end—i.e., past the midterm elections.