Commentaries

Small Cap Opportunity Fund Commentary

Small Cap Opportunity Fund Commentary

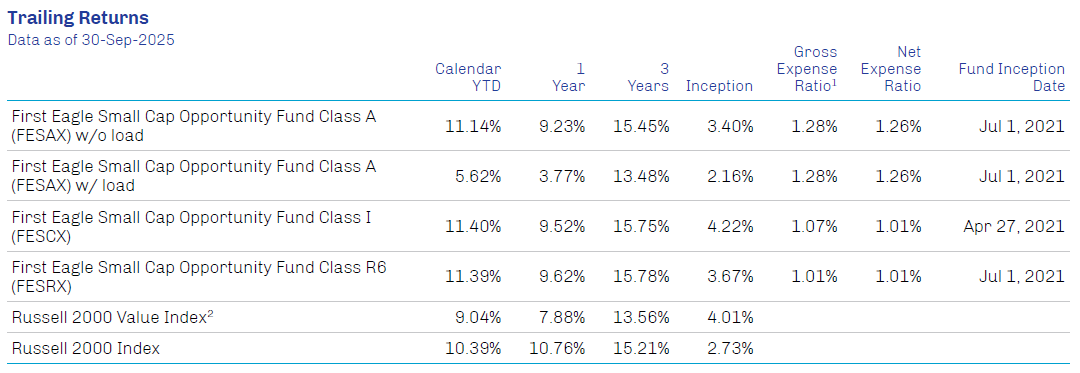

* Performance for Class A shares without the effect of sales charges and assumes all distributions have been reinvested, and if a sales charge was included values would be lower.

1. Source: FactSet; data as of September 30, 2025.

2. Source: LSEG I/B/E/S; data as of October 3, 2025.

3. Source: CME FedWatch; data as of October 9, 2025.

4. Source: Bloomberg; data as of September 30, 2025.

The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short term performance. Current performance may be lower or higher than figures shown. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than their original cost. Past performance data through the most recent month end is available at www.firsteagle.com or by calling 800-334-2143. “With load” performance for Class A Shares gives effect to the deduction of the maximum sales charge of 5.00%. Class I Shares require $1mm minimum investment, and are offered without sales charge. Class R6 is offered without sales charge.

1. First Eagle Investment Management, LLC (the ‘‘Adviser’’) has contractually agreed to waive and/or reimburse certain fees and expenses of Classes A, I and R6 so that the total annual operating expenses (excluding interest, taxes, brokerage commissions, acquired fund fees and expenses, dividend and interest expenses relating to short sales, and extraordinary expenses, if any) (‘‘annual operating expenses’’) of each class are limited to 1.25%, 1.00% and 1.00% of average net assets, respectively. Each of these undertakings lasts until 28-Feb2026 and may not be terminated during its term without the consent of the Board of Trustees. The Fund has agreed that each of Classes A, I and R6 will repay the Adviser for fees and expenses waived or reimbursed for the class provided that repayment does not cause annual operating expenses (after the repayment is taken into account) to exceed the lesser of: (1) 1.25%, 1.00% and 1.00% of the class’ average net assets, respectively; or (2) if applicable, the then-current expense limitations. Any such repayment must be made within three years after the year in which the Adviser incurred the expense.

2. Primary index.

Investments are not FDIC insured or bank guaranteed and may lose value.

The annual expense ratio is based on expenses incurred by the Fund, as stated in the most recent prospectus.

Risk Disclosures

All investments involve the risk of loss of principal.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

There are risks associated with investing in foreign investments (including depositary receipts). Foreign investments, which can be denominated in foreign currencies, are susceptible to less politically, economically and socially stable environments, fluctuations in the value of foreign currency and exchange rates, and adverse changes to government regulations. The value and liquidity of portfolio holdings may fluctuate in response to events specific to the companies or markets, as well as economic, political or social events in the United States or abroad. During periods of market volatility, the value of individual securities and other investments at times may decline significantly and rapidly. The securities of small and micro-size companies can be more volatile in price than those of larger companies and may be more difficult or expensive to trade. A principal risk of investing in value stocks is that the price of the security may not approach its anticipated value or may decline in value. “Value” investments, as a category, or entire industries or sectors associated with such investments, may lose favor with investors as compared to those that are more “growth” oriented. Strategies whose investments are concentrated in a specific industry or sector may be subject to a higher degree of risk than funds whose investments are diversified and may not be suitable for all investors.

Definitions

Federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis.

Gross domestic product (GDP) measures the total value of all economic output in goods and services for an economy.

A floating interest rate adjusts periodically based on movements in an underlying reference

Russell 2000® Value Index (Gross/Total) measures the performance of the small cap value segment of the US equity universe. It includes those Russell 2000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (two-year) growth and lower sales per share historical growth (five-year). A total-return index tracks price changes and reinvestment of distribution income.

Russell 2000® Index (Gross/Total) measures the performance of the small-cap segment of the US equity universe. It includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership. A total-return index tracks price changes and reinvestment of distribution income.

Russell 2500™ Index (Gross/Total) measures the performance of the small to midcap segment of the US equity universe, commonly referred to as “smid” cap. It includes approximately 2,500 of the smallest securities in the Russell 3000® based on a combination of their market cap and current index membership. A total-return index tracks price changes and reinvestment of distribution income.

S&P 500 Index (Gross/Total) is a widely recognized unmanaged index including a representative sample of 500 leading companies in leading sectors of the US economy. Although the S&P 500 Index focuses on the large cap segment of the market, with approximately 80% coverage of US equities, it is also considered a proxy for the total market. The S&P 500 Index includes dividends reinvested. A total return index tracks price changes and reinvestment of distribution income.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The holdings mentioned herein represent the following total assets of the First Eagle Small Cap Opportunity Fund as of 30-Sep-2025: Coeur Mining, Inc. 1.57%; Ameresco, Inc. Class A 1.21%; CECO Environmental Corp. 1.12%; Hecla Mining Company 1.07%; Performant Healthcare, Inc. 0.27%; FTAI Infrastructure Inc. 0.48%; Portillo’s, Inc. Class A 0.00%; Tronox Holdings Plc 0.00%; Intrepid Potash, Inc. 0.42%; Goodyear Tire & Rubber Company 0.28%.

Additional Disclosures

The commentary represents the opinion of the Small Cap team as of the date noted. The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation or an offer to buy, hold or sell or the solicitation of an offer to buy or sell any fund or security.

The Fund’s portfolio is actively managed and holdings can change at any time. Current and future portfolio holdings are subject to risk.

The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof.

Third-party marks are the property of their respective owners.

FEF Distributors, LLC (“FEFD”) (SIPC), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy or product.

Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about our funds and may be viewed at www.firsteagle.com. You may also request printed copies by calling us at 800-747-2008. Please read our prospectus carefully before investing.

First Eagle Funds are offered by FEF Distributors, LLC, a subsidiary of First Eagle Investment Management, LLC, which provides advisory services.