Macro & Market Views

A New Dawn for Healthcare Credit

A New Dawn for Healthcare Credit

While many of the dynamics that battered the healthcare industry in the aftermath of the Covid-19 pandemic have eased, new challenges with highly uncertain impacts have emerged. First Eagle Alternative Credit’s (FEAC’s) Garrett Stephen, senior managing director and co-head of origination on the Direct Lending team, and Jeff Kovanda, managing director and sector portfolio manager on the Tradable Credit team, leverage nearly 40 years of combined experience to offer their outlooks for the healthcare sector and where they see opportunities and risks for credit investors in the space.

Q: How would you characterize the current macroeconomic environment for healthcare companies?

Jeff: While it seems cavalier to summarize an outlook for so disparate an industry—we organize our healthcare analysis around a broad range of distinct subsegments—the overall environment for healthcare remains generally positive, in my view, as the negative impacts from higher interest rates and escalating labor costs that emerged in 2022 have continued to subside.

Higher utilization rates and reduced dependence on expensive temporary labor, alongside better reimbursement rates negotiated with insurers, have enabled healthcare companies to report steadily improving margins. While economic uncertainty prevails, healthcare historically has been a defensive sector and thus could outperform more cyclical segments of the economy if tariffs and renewed inflation weigh on growth. People don’t stop getting sick because of a poor GDP print, and structural demand for health services is supported by the country’s aging demographics.

That said, pharmaceuticals stands out as a subsector that is facing outsized regulatory and legislative risk over the next 12 months. Pharmaceuticals are currently exempt from the tariff policy announced by the Trump administration in April, but it seems likely that a tariff on drugs will be introduced in the second half of the year. The baseline assumption is 25%, but the true impact will depend on how the tariff is implemented. A tariff that includes active pharmaceutical ingredients used in domestic drug production would be more far-reaching than one that applies only to finished products. Our relationships with sponsors and borrowers in the direct lending market enable us to structure loan terms with the provisions we need to feel comfortable extending credit.

Pharma companies also face challenges from headcount reductions at the FDA, which could delay the approval of new products, as well as uncertainty around an executive order signed by Trump in May that would implement most-favored nation (MFN) pricing. MFN pricing would prohibit pharma companies from the common practice of charging more for drugs in the US than they do in other countries. Whether MFN pricing would be applied to all drugs or just certain Medicare drugs is still to be determined. If implemented, MFN pricing could potentially be a significant negative for branded pharma with less impact to generics. It’s worth noting, however, that Trump’s prior attempt to implement MFN pricing late in his first administration was struck down by the courts.

Garrett: Legislative risk for healthcare companies of all types is higher than we expected going into the 2024 elections. A number of provisions in the recently signed tax, spending and policy bill seems likely to have a negative impact on the healthcare industry broadly, particularly the proposed cuts to Medicaid.

In fiscal 2023, Medicaid provided healthcare to 96 million Americans at a total cost of nearly $900 billion and represented 18% of national health expenditures.1 The new tax bill could increase the number of uninsured by around 16 million by 2034.2 Medicaid cuts would negatively impact sub-sectors within healthcare exposed to government reimbursements, though providers focused on certain patient populations—such as children and the disabled—should be relatively insulated. An increase in the number of uninsured is a long-term negative for healthcare broadly.

Our thesis is that the strongest companies will manage through macro and regulatory headwinds to preserve their margins. They’ll right-size their cost structures and/or negotiate higher reimbursement rates from commercial payors. In the long run, they may have the ability to optimize their geographic footprints in provider-friendly jurisdictions if necessary.

Q: How do you evaluate potential investments and manage risk within healthcare?

Jeff: Though each investment decision is unique, especially given the many differences between investing in broadly syndicated loans and direct lending, all of us at First Eagle Alternative Credit are focused on the same thing: consistently applying a disciplined underwriting process that seeks to identify value through rigorous fundamental analysis with particular attention on mitigating downside risk. This effort is bolstered not only by our ability to go deep into the various subsectors of the market in search of opportunities but also through collaboration with our colleagues across the capital stack to raise the bar for the platform as a whole.

In addition to the usual metrics of a corporate borrower’s creditworthiness like profitability, margins, liquidity and leverage, there are a number of healthcare-specific factors to consider. For example, a provider’s payor mix—the ratio of its revenues attributable to government programs like Medicare and Medicaid, private insurance coverage and direct consumer payment—can have a significant impact on profitability and margins. While the government dictates the reimbursement rates it will pay for healthcare, providers negotiate directly with private insurers to establish reimbursement rates that are typically much higher.

Geographic exposure is another consideration. Demand for healthcare at the national level is strong, but there are regional, demographic-based variations. Healthcare providers located in prosperous, growing areas of the country with favorable supply/demand dynamics are more likely to benefit from enhanced pricing and an expanding addressable market.

Garrett: On the direct lending side, we consider the same factors Jeff mentioned but perhaps with even greater intensity given that we lend to niche companies. While the borrower in a syndicated loan deal might be diversified across 10–20 states and multiple product lines, a lower middle market company is likely more concentrated in both regards. The narrower focus of a smaller company—with us often the sole lender—induces us to thoroughly underwrite size and concentration relative to the large cap market in search of favorable structural and business- specific characteristics, including density in affluent metropolitan statistical areas (MSA) that may enrich the payor mix.

Across our many years of experience providing capital to borrowers in the middle market, we have learned that risks can be mitigated through quality underwriting and rigorous structuring. This often has meant a focus on best-of-breed healthcare players with well-aligned private equity sponsors pursuing growth strategies. Rollups—in which a larger, established company or a private equity sponsor buys and combines smaller companies—are a common way to achieve economies of scale, take market share and improve revenue and profitability in the large and mostly fragmented healthcare industry.

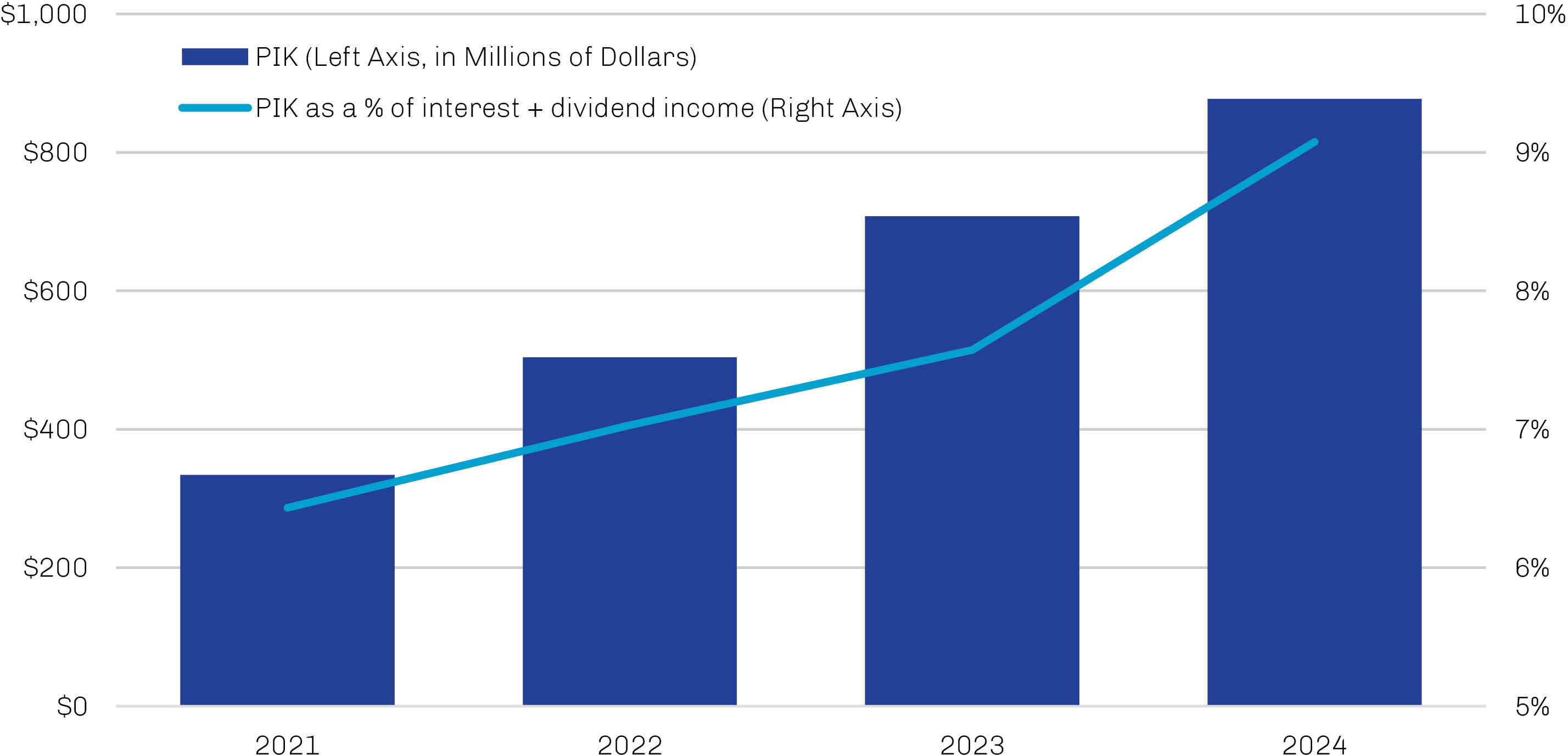

Our relationships with sponsors and borrowers in the direct lending market enable us to structure loan terms with the provisions we need to feel comfortable extending credit. A first-lien position in the borrower’s capital structure is a source of potential idiosyncratic risk mitigation, as is a rigorous loan structure. Syndicated loans have grown increasingly covenant lite over the years, and the larger end of the middle market direct lending universe has followed suit. One example of this is the growing popularity, depicted in Exhibit 1, of payment-in-kind (PIK) structures that enable borrowers to pay lenders with additional debt or some combination of debt and cash (a PIK toggle). Within our segment of the market, however, lenders generally maintain the ability to negotiate terms. For us, these generally include at least one maintenance covenant and coupon payments that must be made in cash.

Exhibit 1. Payment-in-Kind Structures Have Gained Sway in Direct Lending, but We Prefer Cash

Source: Pitchbook | LCD, company reports; data as of December 31, 2024.

Jeff: As a direct lender, Garrett can influence loan terms in a way I can’t. The structure and pricing of a new broadly syndicated loan are primarily determined by the deal’s arranger, and as an investor I can pretty much take it or leave it. And if I don’t believe the loan’s price provides adequate compensation for its risk, I’ll leave it. Same goes with opportunities in the secondary market. So, risk mitigation in syndicated loan portfolios starts with a disciplined, research-driven underwriting process informed by deep industry knowledge.

Q: What are your favorite and least favorite subsectors within healthcare?

Garrett: My top pick in direct loans is revenue cycle management and payor services/cost containment. Companies in this sector provide healthcare organizations with billing and collection services, helping maximize a practice’s revenue while enabling clinicians to focus on patient care. Healthcare in the US is inherently complicated and seemingly grows only more so. The increasing complexity of the reimbursement environment favors businesses that can relieve practices of administrative burdens. These companies generally generate strong margins and highly recurring revenue streams and are largely insulated from tariff and legislative risks. While recognizing strengths, we constantly evaluate each business model to ensure it’s properly preparing for evolving technologies. We favor companies investing to improve processes, targeting a positive return on investment driven by increased accuracy, quality and margins.

Behavioral health is another attractive subsector. Mental health services benefit from a favorable supply/demand imbalance and therefore pricing power, partially driven by increased attention on overall emotional, psychological and social well-being, including heightened focus on autism.

I’m avoiding branded pharmaceuticals. Besides the regulatory risk we discussed earlier, lower middle market pharma companies tend to depend on a single product, making their outlooks quite binary. I’d note, though, that within pharma, outsourced service companies—including contract research organizations that help pharmaceutical companies become more efficient, improving their margins and cash flow—can be interesting.

I’m not excited about nursing homes, as margins in this business are thin, exacerbated by exposure to Medicaid/ government reimbursements. Similar to pharma, however, outsourced services in this space—companies providing everything from specialized ancillary/nursing services to remote patient monitoring to outsourced food prep, laundry and housekeeping services—may hold more appeal. The asset-lite nature of these outsourced providers takes the burden off nursing homes to coordinate care, increase the quality of care and ultimately control costs to payors by preventing higher-cost emergency room visits—thus improving quality, increasing patient satisfaction and reducing costs across the healthcare system.

Jeff: In the syndicated loan market, I share Garrett’s enthusiasm for revenue cycle management companies. I also like outpatient surgery/ambulatory care centers, which provide same-day surgical and diagnostic procedures outside of a traditional hospital setting. These services provide ample exposure to an aging demographic with a favorable private-pay revenue mix and a lower cost structure than hospitals/acute care facilities.

Hospital fundamentals remain strong, as operators are seeing strong volumes, above-average commercial rates and improved labor and wage dynamics. Rural hospitals would be negatively affected by changes to Medicaid given their payor mix, but we expect these cuts to be manageable. We’ve been focused on hospitals with ample liquidity, tolerable secured leverage and enough hard-asset collateral to cover first-lien debt in the event of negative outcomes.

I generally steer away from post-acute care—transitioning patients from hospitals to home or long-term care facilities with rehabilitation, skilled nursing and/or palliative care—as these companies can be highly reliant on government reimbursements. I’m also down on physical therapy, where high labor costs persist due to a shortage of physical therapists amid structurally rising demand for their services.

Q: What is the value proposition of alternative credit in today’s investment environment?

Jeff: Though yields across fixed income are still elevated relative to post-global financial crisis history, the five-handle on the Bloomberg US Corporate Bond Index should be taken with a grain of salt. Much of the improvement in coupons can be traced to the rising base rates prompted by the Federal Reserve’s 2022–23 hiking cycle. Option-adjusted spreads on investment grade corporate credit are well below their five-year average, suggesting that compensation for credit risk has remained relatively stingy even as the economic backdrop—and thus future credit fundamentals—have deteriorated. As the potential for renewed inflation and the persistently higher cost of capital weigh on corporate fundamentals, it seems likely that credit profiles could weaken further before they get better, especially if the economy slips into recession.

Syndicated loans and direct lending historically have offered a consistent and healthy premium to core fixed income assets as compensation for their more limited liquidity and lack of investment grade ratings. And while credit spreads remain tight in the investment grade space, spreads in the alt credit space are well off cyclical lows. Alternative credit assets also offer certain durable advantages relative to traditional fixed income, such as floating-rate coupons to help mitigate duration risk and, in First Eagle’s case, a focus on senior-secured, first-lien loans to help mitigate default risk.

Garrett: In uncertain macroeconomic environments like these, lenders without experience in difficult market conditions across cycles and/or those positioned too aggressively can be at a competitive disadvantage should a downturn materialize. First Eagle Alternative Credit’s research-driven process—enhanced by inter-team collaboration across sectors and the capital stack—is rare within the industry, and we believe our shared insights into a borrower’s lifecycle can enhance our effectiveness as underwriters across the platform.

Direct access to management, strong sponsor support and robust credit analysis—in addition to tailwinds for the sector themes we favor—underpin our rationale for investing in core middle market healthcare loans. This underpinning—coupled with thematic investing across our tradable credit and direct lending platforms—helps us prudently deploy capital despite broader challenges and risks in the marketplace.