Commentaries

Gold Fund Commentary

Gold Fund Commentary

Portfolio Review

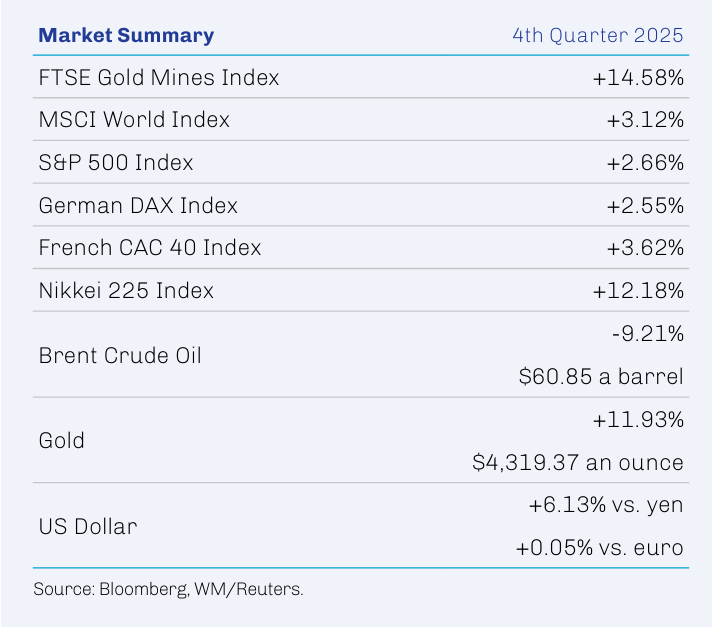

Gold Fund A Shares (without sales charge*) posted a return of 15.96% in fourth quarter 2025. Gold bullion and gold-related equities both contributed to performance. The Gold Fund outperformed the FTSE Gold Mines Index in the period.

Leading contributors in the First Eagle Gold Fund this quarter included gold bullion, DPM Metals, Inc., Barrick Mining Corporation, G Mining Ventures Corp and Newmont Corporation.

The factors driving the performance of gold bullion during the quarter were discussed in detail in the Market Overview section of this report.

DPM Metals, formerly Dundee Precious Metals, is a junior miner head quartered in Canada with assets in Bulgaria, Bosnia and Herzegovina, Serbia and Ecuador. The company reported strong financial results during the quarter. The accelerated integration of the polymetallic Vareš Mine in Bosnia and Herzegovina—which DPM acquired through its purchase of Adriatic Metals in September—and positive exploration results at Coka Rakita in Serbia further bolstered sentiment. The company has demonstrated judicious capital allocation in its successful transition from a single-asset play to the owner/operator of high-margin, concentric properties in the Baltics.

Canada’s Barrick Mining is the world’s second-largest gold producer by output. Strong gold and copper prices drove cash flows during the quarter, and operating leverage was enhanced by resumed gold production in Mali, which had been suspended in January 2025. Media reports about a potential acquisition of the company by Newmont, though unconfirmed, served as an additional boost to the stock during the quarter, as did the announcement of a stake in the company by an activist investor. As management reviews strategic actions to unlock value, including a possible initial public offering (IPO) of its North American assets, Barrick shareholders continue to benefit from stock buybacks.

The leading detractors in the quarter were Franco-Nevada Corporation, B2Gold Corp., Pan American Silver Corp Contingent Value Rights 2019-22.02.29, Agnico Eagle Mines Limited and Gold Fields Limited.

Franco-Nevada is a royalty and streaming company with a diversified portfolio of precious metal, non-precious metal and energy assets. Shares of Franco-Nevada traded down during the fourth quarter, but 2025 overall was quite strong. The company’s largest asset is Cobre Panama, a copper mine in Panama operated by First Quantum Minerals; the mine ceased production on order of the Panamanian Supreme Court in late 2023, but there are currently ongoing efforts to restart operations. Despite the issues at Cobre Panama, we continue to like Franco-Nevada’s very strong balance sheet—which has no debt—and its diversified portfolio of long-lived, cash-generative assets.

B2Gold is a Canadian mining company that owns and operates gold mines in Mali, Namibia, the Philippines and Canada. After declaring commercial production for the company’s Goose Project in Canada in October, investors were disappointed in November as management revised down full-year guidance due to crusher-capacity issues and delays accessing higher-grade ore. B2Gold has ample time to maximize economics over Goose’s nine-year reserve life. Separately, and despite persistent concerns of ongoing political risk, production at the Fekola Complex in Mali continued unimpeded throughout the quarter. We continue to value B2Gold’s strong track record of operational execution and exploration success.

Pan American Silver is a Canadian mining company with large silver endowments and a diversified portfolio of producing mines. We hold small positions in both its contingent value rights (CVRs) and equity. Rather than moves in underlying metals prices or its strong business model, price changes in the company’s CVRs reflect expectations of the prospective reopening of the company’s shuttered Escobal silver mine in Guatemala. Prospectively meaningful dialogue between the Indigenous Parliament and Guatemala’s Ministry of Energy and Mines continued during the quarter. Meanwhile, the Escobal mine remains on care and maintenance—pending compliance with Indigenous consultation guidelines—with no target date to resume operations.

We appreciate your confidence and thank you for your support.

Sincerely,

First Eagle Investments

* Performance for Class A shares without the effect of sales charges and assumes all distributions have been reinvested, and if a sales charge was included values would be lower.

1. Source: Bloomberg, FTSE Russell; data as of December 31, 2025.

2. Source: Bloomberg; data as of December 31, 2025.

3. Source: Federal Reserve; data as of December 10, 2025.

4. Source: World Gold Council; data as of October 30, 2025.

5. Source: Financial Times; data as of November 14, 2025.

6. Source: World Gold Council; data as of January 8, 2025.

7. Source: Financial Times; data as of November 25, 2025.

The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short term performance. Current performance may be lower or higher than figures shown. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than their original cost. Past performance data through the most recent month end is available at www.firsteagle.com or by calling 800-334-2143. The average annual returns are historical and reflect changes in share price, reinvested dividends and are net of expenses. “With sales charge” performance for Class A Shares gives effect to the deduction of the maximum sales charge of 3.75% for periods prior to March 1, 2000, and of 5.00% thereafter. The average annual returns for Class C Shares reflect a CDSC (contingent deferred sales charge) of 1.00% in the year-to-date and first year only. Class I Shares require $1MM minimum investment and are offered without sales charge. Class R6 Shares are offered without sales charge. Operating expenses reflect the Fund’s total annual operating expenses for the share class as of the Fund’s most current prospectus, including management fees and other expenses.

1. The annual expense ratio is based on expenses incurred by the fund, as stated in the most recent prospectus.

Investments are not FDIC insured or bank guaranteed and may lose value.

Risks

All investments involve the risk of loss of principal.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

There are risks associated with investing in securities of foreign countries, such as erratic market conditions, economic and political instability and fluctuations in currency exchange rates. These risks may be more pronounced with respect to investments in emerging markets. Investment in gold and gold-related investments present certain risks, including political and economic risks affecting the price of gold and other precious metals like changes in US or foreign tax, currency or mining laws, increased environmental costs, international monetary and political policies, economic conditions within an individual country, trade imbalances and trade or currency restrictions between countries. The price of gold, in turn, is likely to affect the market prices of securities of companies mining or processing gold and, accordingly, the value of investments in such securities may also be affected. Gold related investments as a group have not performed as well as the stock market in general during periods when the US dollar is strong, inflation is low and general economic conditions are stable. In addition, returns on gold related investments have traditionally been more volatile than investments in broader equity or debt markets. Investment in gold and gold related investments may be speculative and may be subject to greater price volatility than investments in other assets and types of companies. Funds whose investments are concentrated in a specific industry or sector may be subject to a higher degree of risk than funds whose investments are diversified and may not be suitable for all investors.

Definitions

Federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis. Exchange-traded funds (ETFs) are listed investment vehicles that seek to provide exposure to a benchmark, index or actively managed strategy.

MSCI World Index (Net) measures the performance of large and midcap equities across developed markets countries. A net-return index tracks price changes and reinvestment of distribution income net of withholding taxes. FTSE Gold Mines Index (Price) measures the performance of gold mining companies worldwide that have a sustainable, attributable gold production of at least 300,000 ounces a year and that derive 51% or more of their revenue from mined gold. A price-return index only measures price changes. S&P 500 Index (Gross/Total) measures the performance of 500 of the top companies in the leading industries of the US economy and is widely recognized as a proxy for the US market as a whole. A total-return index tracks price changes and reinvestment of distribution income. Nikkei 225 is a price-weighted index composed of 225 stocks in the Prime Market of the Tokyo Stock Exchange. It is widely recognized as a proxy for the Japanese equity market as a whole. German DAX® Index measures the performance of the 40 largest companies listed on the Frankfurt Stock Exchange that fulfil certain minimum quality and profitability requirements. It is widely recognized as a proxy for the German equity market as a whole. CAC 40® Index is a free-float market capitalization-weighted index that measures the performance of the 40 largest and most actively traded shares listed on Euronext Paris.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The holdings mentioned herein represent the following total assets of the First Eagle Gold Fund as of 12/31/2025: gold bullion 23.76%; DPM Metals, Inc. 5.73%; Barrick Mining Corporation 5.35%; G Mining Ventures Corp 4.01%; Newmont Corporation 7.22%; Franco-Nevada Corporation 3.94%; B2Gold Corp. 0.78%; Pan American Silver Corp Contingent Value Rights 2019-22.02.29 0.06%; Agnico Eagle Mines Limited 6.45%; Gold Fields Limited 2.71%.

Additional Disclosures

This commentary represents the opinion of the First Eagle Gold Fund portfolio managers as of the date noted and is subject to change based on market and other conditions. The opinions expressed are not necessarily those of the entire firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed.

The Fund may invest in gold and precious metals through investment in a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). Gold Bullion and commodities include the Fund’s investment in the Subsidiary.

The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof.

Third-party marks are the property of their respective owners.

FEF Distributors, LLC (“FEFD”) (SIPC), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy or product.

Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about our funds and may be obtained by visiting our website at www.firsteagle.com or calling us at 800-334-2143. The prospectus or summary prospectus should be read carefully before investing.

First Eagle Funds are offered by FEF Distributors, LLC, a subsidiary of First Eagle Investment Management, LLC, which provides advisory services.