Stay Gold

Stay Gold

Financial markets were rattled by a litany of interlocked challenges during 2022, including war, high inflation, rising interest rates and fears of recession. Gold’s decline in the face of these uncertain conditions—when many likely expected the metal to live up to its reputation as a safe haven—had some commentators asking, “Why bother?”

As Thomas Kertsos, co-portfolio manager of the Gold strategy, and Max Belmont, associate portfolio manager of the strategy, discuss below, gold behaved as we expected it would—if not better—in 2022 given the year’s conflicting dynamics. Ultimately, Thomas and Max believe the year underscored why a number of First Eagle’s portfolios “bother” with a strategic allocation to gold; namely, because its reputation as a potential hedging tool for capital preservation is unparalleled, if perhaps misunderstood.

Living in the Real World

In 2022, no-longer-transitory inflation become a meaningful concern in developed market economies for the first time in many decades. Since gold is widely viewed as a potential hedge against inflation, its price should benefit from multi-decade-high inflation levels, right? Well, it’s not quite as simple as that. While inflation can help influence movements in the price of gold, it’s not the primary catalyst.

Consider gold in 2022. Gold rallied early in the year as investors flocked to perceived safe havens in the weeks leading up to and immediately following Russia’s invasion of Ukraine. However, it wasn’t long before markets turned their attention to the likelihood that the Fed would soon act to combat unflagging inflation, and gold’s 2022 peak was established only days before the central bank launched one of its most aggressive rate-hike cycles in decades. Signs that the Fed may be prepared to slow its pace of tightening prompted a November rebound in gold, and the metal finished the year-to-date through November down only 2.3% despite significant intra-period swings in both directions.1

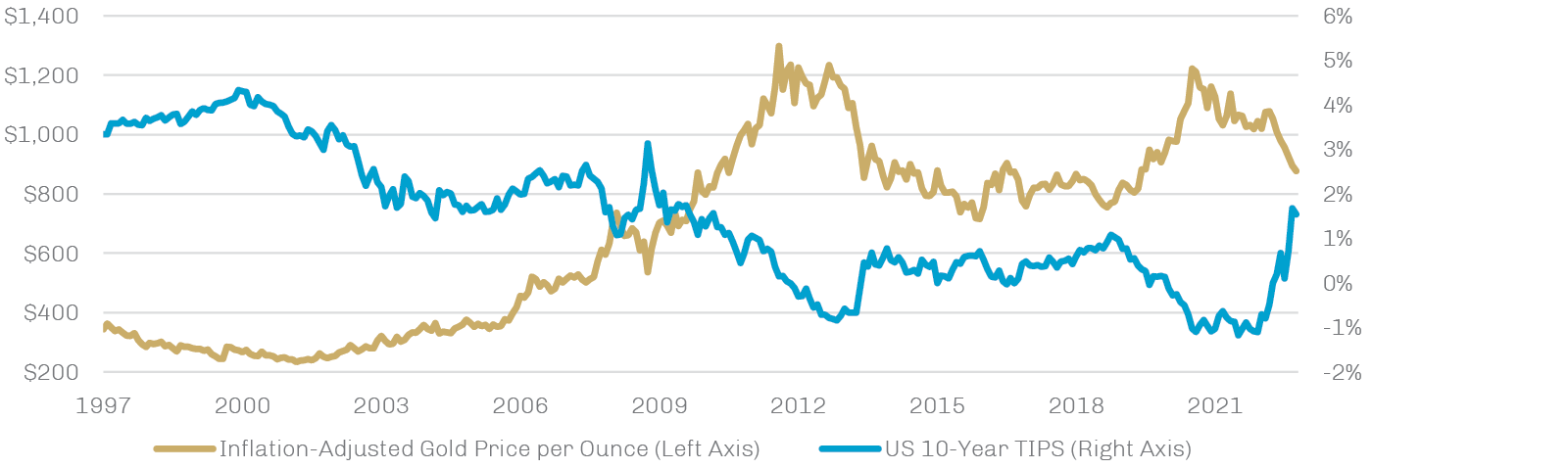

While multiple factors can affect the price of gold, we believe changes in real interest rates—i.e., the difference between nominal interest rates and inflation—are the most important driver over the medium and long terms. Real interest rates represent the opportunity cost of owning gold; since it pays neither dividends nor interest, gold is relatively expensive to hold when real interest rates are high and relatively inexpensive to hold when they are low. Thus, real interest rates and the price of gold historically have been negatively correlated; as shown below, when real interest rates have moved lower, the gold price, despite some lead/lag effects, has generally moved higher and vice versa.

Real Interest Rates Historically Have Been the Key Driver of the Gold Price

January 1997 through November 2022; Consumer Price Index, 1982–84 = 100

Source: Bloomberg data as of November 30, 2022.

Looking specifically at 2022, stubbornly high inflation prints prompted the Fed to raise its federal funds target rate by 375 basis points between March and November while maintaining steadily hawkish rhetoric.2 The real interest rate—as represented by the yield on 10-year Treasury inflation-protected securities (TIPS)—trended decidedly upward in response, climbing from around -1% in March to an early-November peak above 1.7%, the largest spike in real rates since the global financial crisis.3That the price of gold fell about 18% during the trough-to-peak period in real rates during 2022 doesn’t come as a surprise. It’s worth noting, however, that the gold price’s year-to-date decline of 2.3% handily outpaced most risk assets—including equities (S&P 500 Index: -13.1%) and long-term bonds (Bloomberg US Long Treasury Index: -28.0%)—and provided the ballast we seek.4

Despite the market, macro and geopolitical trends pointing to the contrary, the behavior of real and nominal interest rates thus far in 2022 suggests the Fed has convinced the market that it will be successful in its efforts to get prices under control without tipping the economy into a protracted decline. The yield on 10-year TIPS, our proxy for real interest rates, is composed of the current nominal 10-year Treasury rate plus market expectations for average inflation over the security’s tenor (termed the “breakeven inflation rate”). As shown below, the breakeven inflation rate peaked in March and has been biased lower since, implying that inflation expectations remain anchored. It also implies that the increase in real interest rates during 2022 has been fueled primarily by higher nominal rates, whose path to levels not seen since 2008 indicates confidence that significant rate cuts will not be needed to stimulate a flagging economy.

Fed Tightening in 2022 Appeared to Cool Inflation Expectations

January 1, 2022, through November 30, 2022

Source: FactSet; data as of November 30, 2022.

A Potential Hedge for All Seasons

The market appears optimistic about the Fed’s ability to tame inflation. But what if the Fed fails? What if its aggressive intervention amid a backdrop of massive federal debt prompts the kind of deflationary shock we saw in 2008? Or what if any number of potential black swan events emerge to waylay the journey back toward normalization and force the Fed to intervene? As students of history, we are inclined to prepare for a range of potential outcomes; we believe doing so includes a strategic allocation to gold—an allocation that has been beneficial during such recent challenges as Russia’s invasion of Ukraine (2022), the outbreak of Covid-19 (2020) and the global financial crisis (2008).

Our view is that of all the available potential hedging options, both real and financial, gold’s differentiated risk-return characteristics could promote long-duration resilience across the widest variety of adverse circumstances. Over the past two centuries alone, gold has withstood inflationary episodes and deflationary spirals, political revolutions and rapid technological evolution, localized conflicts and world wars, pandemics and treatments for them.5

Take the disinflationary impulse of the global financial crisis, for example. As depicted below, gold initially spiked higher when Lehman Brothers declared bankruptcy in September 2008, only to collapse alongside equities, oil, real estate, copper and most other risk assets as liquidity breakdowns across markets paradoxically pushed real yields higher.6 While gold ultimately shed more than 20% to reach its mid-November trough, the potential hedge value of gold reasserted itself as other risk assets continued to founder. By the end of 2008, gold’s 5.8% gain historically made it one of the very few assets to deliver a meaningful return in 2008. By the time equity markets reached their cyclical nadir in March 2009, gold was more than 20% higher than its pre-Lehman price.7

Gold Has Weathered a Range of Historical Challenges, Including the Global Financial Crisis

September 15, 2008, through April 30, 2009; September 15, 2008 = 100

Source: Bloomberg; data as of November 30, 2022.

The 1970s—a decade that offered not only high inflation but also high unemployment, sluggish economic growth and freeform turmoil—provide a contrasting example. Throughout history, gold prices have tended to be at their highest—and real interest rates at their lowest—when the economy was weak and/or experiencing inflation, periods that have tended to coincide with low levels of confidence in the economy and government, and thus a greater inclination among investors to hold a universal currency like gold rather than its manmade substitute. Trading freely following the collapse of the Breton Woods system in 1971, gold’s price grew 25-fold by 1980, bolstered in part by its lack of industrial utility, a trait that can make the prices of other real assets like base metals sensitive to economic activity and serve as a headwind during periods of stagflation, such as we saw in the late 1970s.

While the Fed’s gravitational pull on the gold price during 2022 was unusual given the combination of war in Europe and high inflation, it served as a good reminder of why we don’t maintain a directional view on price. Instead, we value gold for its attributes as a potential hedge that may help mitigate the risk of permanent impairment of capital.

1. Source: Bloomberg; data as of November 30, 2022.

2. Note that publication deadlines preceded the Fed’s mid-December meeting, at which it was expected to announce a 50 basis point hike.

3. Source: Bloomberg; data as of November 30, 2022.

4. Source: FactSet; data as of November 30, 2022.

5. Source: World Gold Council, data as of November 30, 2022.

6. Source: FactSet; data as of November 30, 2022..

7. Source: Bloomberg; data as of November 30, 2022.

8. Source: Bloomberg; data as of November 30, 2022.