Macro & Market Views

Why Munis Now?

Why Munis Now?

Risk appetites, for the most part, have remained intact thus far in 2024, even as the potential trajectory of interest rates has grown increasingly murky. Persistently sticky inflation readings and more recent signs of economic weakness have markets reconsidering how many federal funds rate cuts will happen this year—or if any will happen at all.1

- Though recent macroeconomic readings have tempered expectations about the timing and magnitude of interest rate cuts, current conditions in the municipal bond market—notably, its unusual U-shaped yield curve—suggest an opportunity to lock in yields at levels not seen in many years.

- Market technicals remain supportive, as both demand and supply show signs of renewed energy after a sluggish couple of years.

- In contrast with the US federal government, fiscal positions of state and local governments are strong overall, which we expect will support the muni market’s historically low default rate as well as high recovery rate in the event of default.

- Certain sectors of the municipal market that appear to be unloved or overlooked—such as health care, charter schools and not rated—may offer particularly fertile ground for fundamental managers focused on rigorous underwriting.

With interest rates retracing much of their late-2023 rally, longer-duration fixed income assets for the most part have lost ground, and the bond market in general continues to be marked by minimal term premia for government paper and very tight spreads on credit, suggesting underwhelming compensation for incremental risk. Municipal bonds—and high yield munis, in particular—have held up relatively well in a market not terribly supportive of fixed-rate assets, and we believe conditions continue to underpin investment in fixed-rate, tax-exempt bonds.

Both market technicals and issuer fundamentals should bolster muni bond prices in the short term, while the unusual U-shape of the muni bond yield curve—with elevated yields on the short and long ends of the curve bookending a deep sag in the belly—may offer the opportunity to lock in long-term income streams at levels not seen in many years. We think particular value may be found in certain unloved sectors of the high yield muni market—healthcare and charter schools, for example, as well as unrated bonds—for managers willing to do the fundamental research to uncover them.

Current Dynamics Support Muni Bond Investment

Evolving interest rate expectations—as they were in 2023—have been a prime driver of risk assets thus far in 2024. While confidence in a potential Fed pivot fueled rallies across a range of assets beginning in late 2023, “higher for longer” has reemerged as the dominant policy narrative in 2024 as macroeconomic readings have tempered expectations around the timing and magnitude of federal funds rate cuts. Swaps traders entered the year expecting six cuts totaling 150 basis points during 2024 but now see only one 25 basis point cut.2 With rates rising across maturities year to date, the Treasury yield curve remains inverted, as it has been since July 2022.3

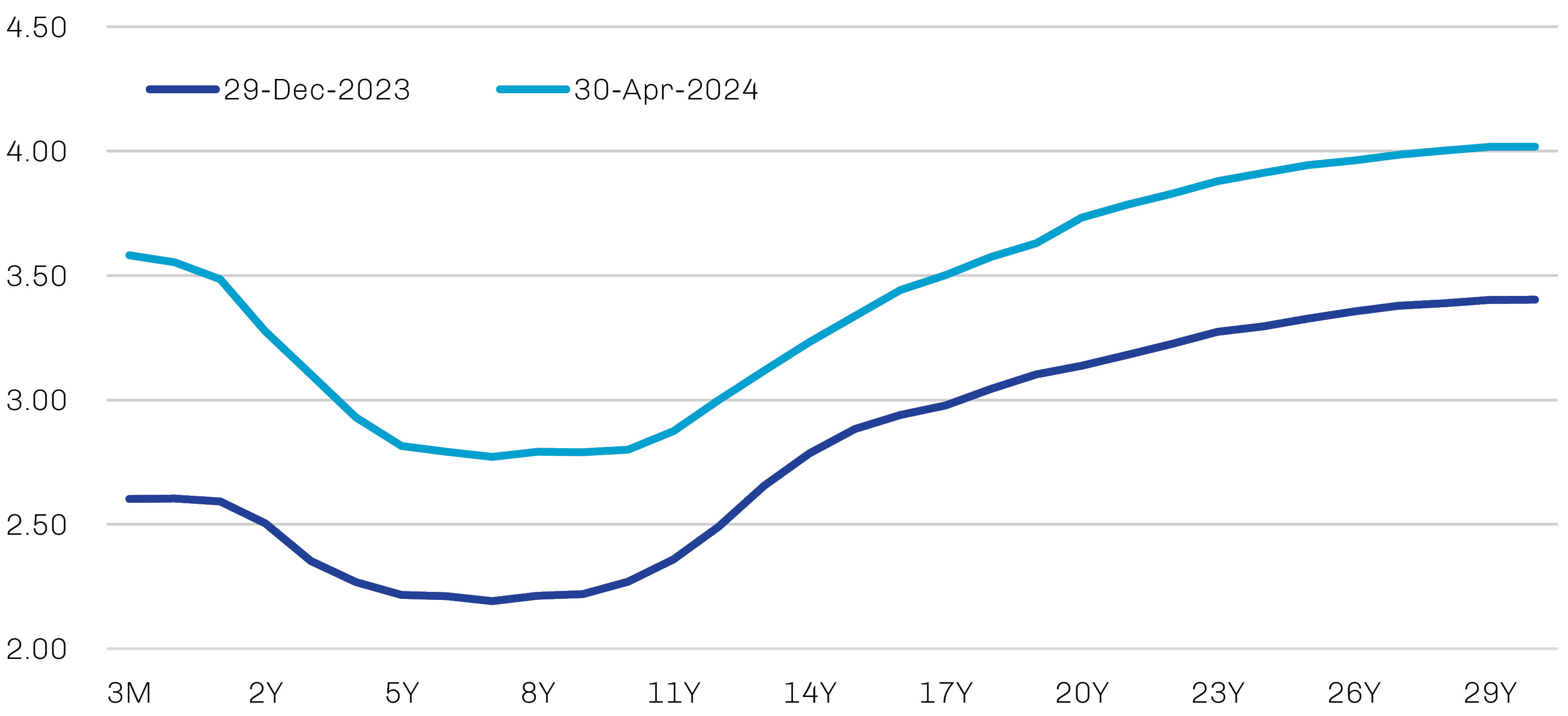

Unlike the downward-sloping Treasury curve, the municipal bond yield curve exhibits a pronounced U shape, which presents investors with a different set of positioning dynamics to consider. As shown in Exhibit 1, high yields at the short end of the curve slope downward until 10 years, suggesting investors are not being compensated for the additional duration risk across the belly of the curve. The curve turns upward at the 10-year mark, however, and the steepness at the long end of the curve points to an opportunity to capture significant additional yield per unit of duration risk in longer-maturity issues. Though off the highs of October 2023, long municipal bond yields persist at levels not seen in many years.

Exhibit 1. The Long End of the Muni Curve Appears to Offer More Attractive Risk-Reward Profile

AAA Municipal Bond Yield Curve

Source: FactSet; data as of April 30, 2024. Chart is for illustrative purposes only.

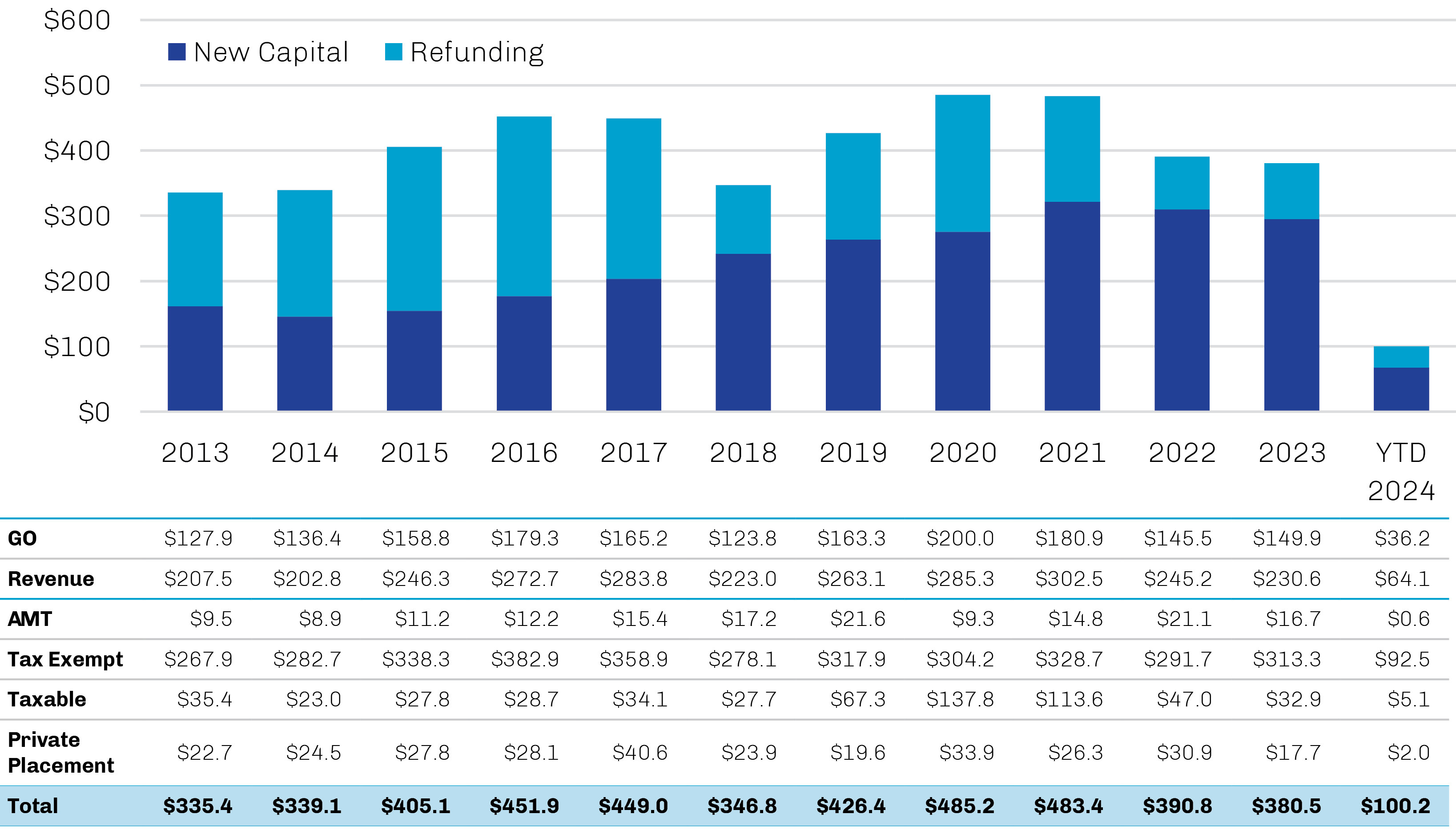

Market technicals and healthy fundamentals have promoted resilience in the muni bond space even as yields have risen. Muni issuance, as it has been in the corporate debt space, has been sluggish since the Fed began raising rates in early 2022.4 State and local coffers generally were well-funded entering the tightening cycle—post-Covid economic reopenings drove a large rebound in tax revenues, while balances were bolstered further by significant federal Covid relief—and there was limited need to issue debt in the face of much higher borrowing costs. As a consequence, there has been an overall decline in tax-exempt muni bonds outstanding, and the resulting supply-demand imbalance has helped support prices.5

While supply could rebound as the benefit of federal support wanes and interest rates stabilize, we think there is sufficient pent-up demand for municipal bonds to absorb any uptick in issuance. For example, after two years of significant outflows amid rising interest rates, tax-exempt muni bond mutual funds have attracted more than $11 billion of inflows this year; while this is encouraging, we’d caution that demand also started strong in 2023 before fading as the year progressed.6

Exhibit 2. Municipal Bond Issuance Faded Post-Pandemic

Annual Issuance in Billions of Dollars

Source: FactSet, data as of April 30, 2024. Charts are for illustrative purposes only.

Searching for Diamonds in the Rough

While we are constructive on the municipal market as a whole, we believe there are a number of unloved, overlooked or contrarian sectors in which fundamental, research-driven investment managers may be able to uncover particularly attractive opportunities.

Healthcare. The healthcare sector, which includes both hospitals and senior living, has long been out of favor among muni buyers. Hospital bonds came into 2024 continuing to bear the stain of the financial stresses faced during the Covid-19 period, but we believe the worst is behind these issuers. During the height of Covid, hospitals deferred high-margin elective procedures in favor of providing less-profitable pandemic care; once Covid began to wane and activity normalized, surging wage inflation—particularly for nurses—weighed heavily on margins.

The lack of attention paid to the hospital sector by muni investors has resulted in what we view as a particularly inefficient market, and we believe this inefficiency is a good target for First Eagle’s fundamentally driven security-selection process. Hospital operators today are rebounding from the dislocations of Covid at different rates, in our view, and our goal is to take advantage of the improving credit stories before they are recognized by the market. Bond features like a first mortgage lien on property plant and equipment, as well as a gross revenue pledge, rate covenants and debt-service reserve funds serve as a measure of risk mitigation.

Senior living facilities are perhaps the most contrarian area of the muni market. While relatively small in par value, senior living facilities have accounted for nearly half of all municipal bond defaults over the last several years.7 Given their need to constantly maintain and improve their facilities in order to preserve high occupancy levels, operators of nursing homes and continuing care retirement communities tend to be highly levered with limited equity cushions in their capital structures. Covid-19 weighed heavily on this sector, and it unsurprisingly entered 2024 with very wide credit spreads. Caution is still warranted in the space, but we believe rigorous underwriting can uncover what we consider to be hidden gems that are well-managed and well-positioned in their markets while offering the potential for favorable yields and dollar prices that may adequately compensate for the risks

Charter schools. This is one of the most idiosyncratic municipal sectors; while individual issues tend to be highly fragmented and small—typically only about $25 million—they collectively comprise a multibillion-dollar space. Bonds are issued to build and acquire new schools and campuses, and bondholders usually have liens on property and gross revenue, which come from the state. Notably, state general obligation ratings are investment grade, but most charter school bonds are either BB rated or not rated. State school budgets have a large influence on charter schools, which were also supplemented with federal government aid during the pandemic.

As federal pandemic aid begins to end, we have begun to see more distressed charter schools, although the total number of defaults remains low. Accordingly, rigorous underwriting and due diligence are still necessary. We look for well-managed schools in good locations with growing demographics that are desirable for families and provide competitive offerings relative to local public schools. Because of the idiosyncratic nature of charter schools, attractive credit spreads may be identified by managers able to do the analysis.

Unrated bonds. Unrated bonds are another area where credit managers that take a fundamental approach to underwriting and evaluating credits may find favorable yields relative to credit quality and default risk. We estimate about one-third of all municipal bonds—and the majority of high yield bonds—are not rated by a nationally recognized statistical rating organization (NRSO). We don’t believe the lack of a rating should be interpreted as a reflection of a muni bond’s credit quality, however. Many unrated issues are smaller and less liquid than investment grade deals, and issuers often forgo ratings to avoid the associated expenses. To compensate for greater complexity and information risk, these bonds typically pay investors a higher yield compared to rated issuers of similar quality.

Exploiting Inefficiencies in a Large but Fragmented Muni Market

We believe the muni bond market remains robust from a fundamental perspective. Unlike the US federal government, the fiscal positions of state and local governments are strong overall. Total financial assets for state and local governments ended 2023 at an all-time nominal high, and expenditures, while above trend, have begun to moderate.8 Municipal bond defaults are far less common than defaults by corporate issuers—issuers have multiple levers that can be pulled to help service their debt, including tax increases, spending cuts and drawing on reserves—and current fiscal dynamics should support historically low default rates as well as high recovery rates in the event of default.

With about $4 trillion distributed across more than one million distinct municipal bonds and 50,000 issuers, the municipal bond market is large but highly fragmented, which historically has resulted in pricing inefficiencies and opportunities for skilled active investors to add value. Through rigorous underwriting we seek to uncover what we consider to be hidden gems that are well-managed and well-positioned in their markets while offering the potential for favorable yields and dollar prices that may adequately compensate for the risks.