Macro & Market Views

There’s No Place Like Home

There’s No Place Like Home

Key Takeaways

Continued strong dynamics in the US housing market combined with regulatory headwinds for conventional lenders have generated opportunities to invest in real estate specialty lending with attractive risk-adjusted return potential.

With attractive yields, robust cash flows and short durations, we believe residential transitional loans and land banking appear to be especially compelling segments among private assets.

Publicly traded real estate-linked credits—including agency mortgage-backed and credit-risk transfer securities and higher yielding opportunities linked to mortgage insurance and non-qualifying mortgages—may provide attractive complements to private credit investments.

Investors with the flexibility to opportunistically manage exposures may capture the benefits offered within private and public real estate debt while exploiting the relative-value discrepancies that periodically emerge between them.

Even as a yawning gap between housing supply and demand has provided a tailwind for US residential real estate values, regulatory changes since the global financial crisis have reduced the availability of bank financing for certain types of real estate activities. The resulting disconnect has created an opportunity for a new cohort of private lenders to step in as liquidity providers—and potentially generate attractive, long-term returns for themselves and their investors.

This has included participation in such private-market segments as residential transitional loans and land banking, where yields offer attractive complexity and illiquidity premia over traditional credit assets like leveraged loans and high yield bonds, alongside short durations and robust cash flows. Certain public-market assets, meanwhile, may complement these private investments. High-yielding opportunities may potentially be found in credit-risk transfer securities issued by agencies such as Fannie Mae and Freddie Mac, for example, or in instruments linked to mortgage insurance and non-qualifying mortgages.

While we believe supply/demand dynamics in the US residential real estate market are likely to support durable investment opportunities in real estate specialty lending, these investments tend to have high barriers to entry. Experience sourcing, underwriting and structuring such deals may be a prerequisite for success.

US Housing Market Has Cooled but Remains Significantly Undersupplied…

The US hasn’t built enough homes in recent decades, leading to a significant gap between housing supply and demand, estimates of which vary from 1.6 million to 5.5 million units.1 The lack of affordable homes highlights the need for increased supply in both the new- and existing-home markets. We believe the motivation to close the supply/demand gap represents a strong and durable tailwind for residential new construction and the renovation of existing homes as well as demand for the capital needed to fund these projects.

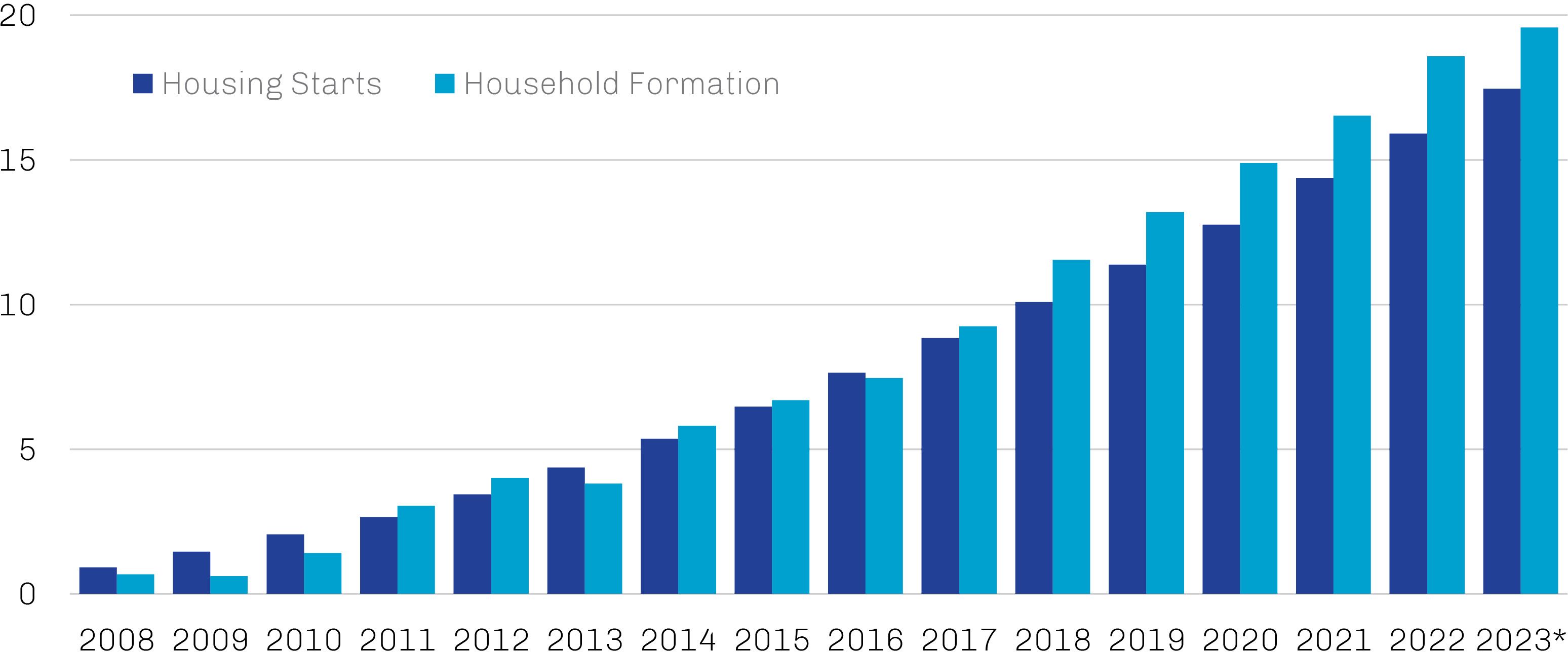

The current housing shortfall can be traced back to the global financial crisis, as the pullback in consumer credit at the time prompted a sharp decline in housing starts from which the industry has yet to recover.2 Household formation (that is, growth in the number of families), meanwhile, has continued nearly unabated, and the resulting gap between housing supply and demand has widened further, as shown in Exhibit 1. The impact of new-housing underbuilding has been exacerbated by the limited supply of existing homes for sale, partially due to the “lock-in effect” that serves as a disincentive for homeowners to sell. To illustrate, 81% of outstanding mortgages carry an interest rate below 5%, 61% are below 4%, and 23% are below 3%;3 the 2023 high for the Freddie Mac 30-year fixed was 7.79%.4 And with a median age of owner-occupied homes at 40 years, the homes that do come to market likely will need remodeling to maximize their value.5

Exhibit 1. The US Housing Gap Has Worsened in Recent Years

Cumulative in Millions, 2008 through November 2023

*Year to date through November 30, 2023.

Source: Source: Federal Reserve Bank of St. Louis; data as of November 30, 2023.

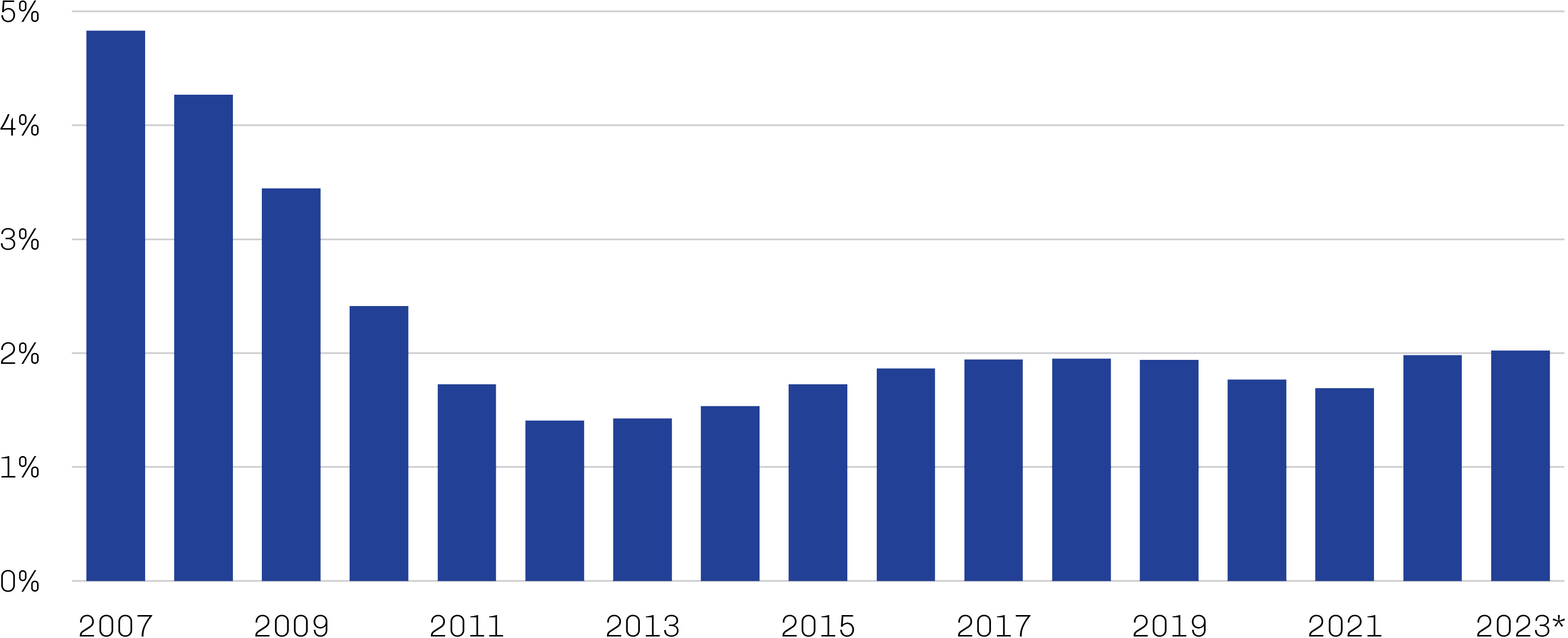

While housing supply has grown increasingly strained over the past 15 years, regulatory changes in the wake of the global financial crisis have hampered banks’ ability to finance certain types of real estate activities, including acquisition, development and construction lending. As shown in Exhibit 2, for example, construction loans as a percentage of bank total assets today are less than half of what they were in 2007. Effectively, the banks have been replaced by a highly fragmented set of lenders across the country that lack institutional capital, which has presented an opening for asset managers to become liquidity providers in the space at attractive terms.

Exhibit 2. Traditional Banks Have Pulled Back from Certain Types of Real Estate Lending

Construction Loans as a Percentage of Total Bank Assets, 2007 through March 2023

*Year to date through March 31, 2023.

Source: Federal Deposit Insurance Corporation; data as of March 31, 2023.

Despite the adverse impacts of inflation and tighter financial conditions, US consumers remain in good financial shape, suggesting near-term demand for housing should remain strong. At the end of the second quarter of 2023, the total value of the US single family housing market increased to an all-time high of $44.5 trillion, 84% above the 2006 peak.6 A large portion of this growth came from the increase of homeowners’ equity, which rose 123% over this period, while outstanding mortgage debt only increased 29% to $12.9 trillion.6 Given the dramatic increase in equity relative to mortgage debt, the rate of aggregate residential mortgage debt to value has declined to 29% today from more than 50% in second quarter 2013.6 Households with low-rate mortgages secured before the recent hikes, in particular, have benefitted from this deleveraging and maintain strong debt-service ratios even as other forms of credit have grown more expensive.

…Creating Durable Opportunities for Providers of Capital to the Real Estate Industry

The increase in benchmark rates since the Federal Reserve began its rate-hike cycle in early 2022 has pushed yields across public credit investments in general to levels not seen in decades, while yields on more complex private credit assets also rose, albeit at a slower pace. In light of our constructive view on US residential real estate, the yields available in market segments like residential transitional loans and land banking appear particularly compelling to us. In addition to offering complexity and illiquidity premia of 200–300 basis points over traditional market options like leveraged loans and high yield bonds, the short durations and robust cash flows typical of these assets enable frequent reinvestment of proceeds.7

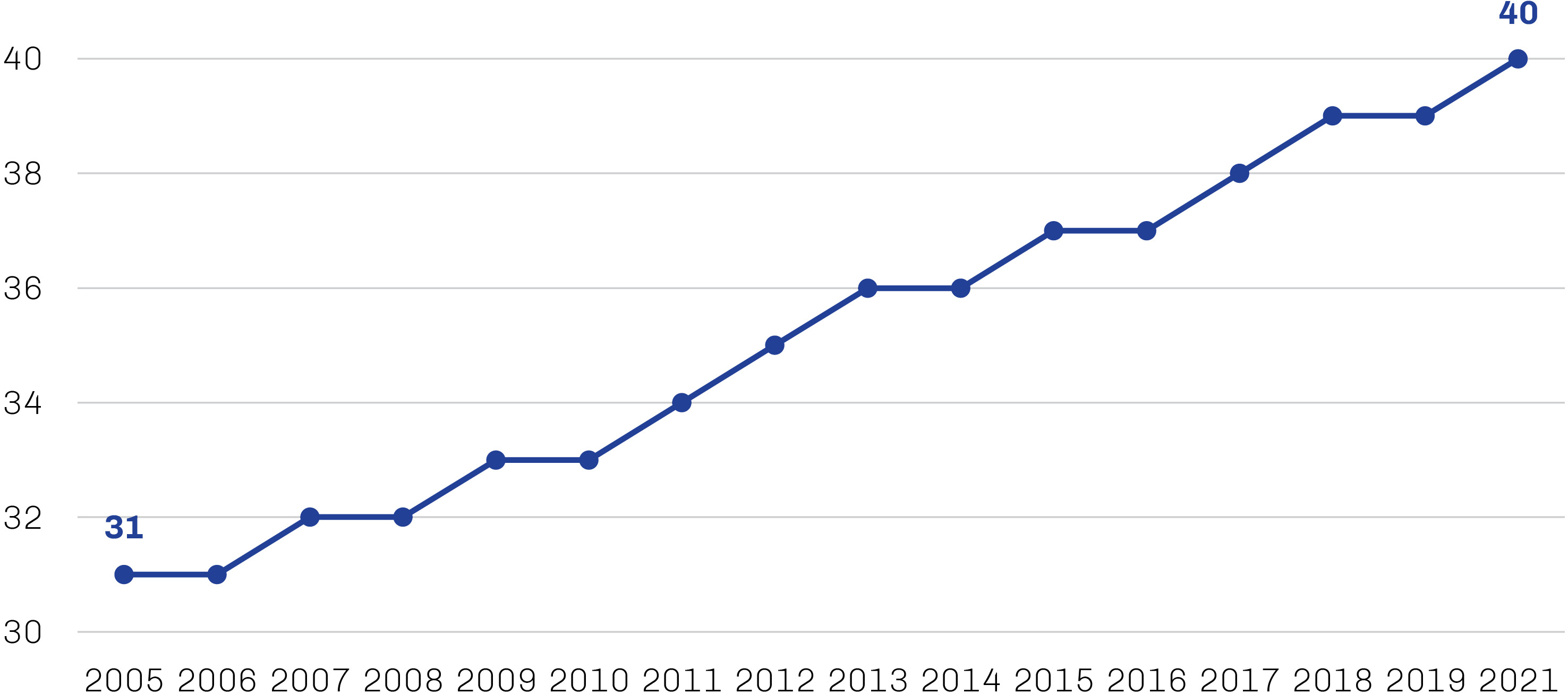

Residential transitional loans. To many buyers, a refurbished home in an established neighborhood can be more desirable than a new home in a new area, allowing them to tap into proven infrastructure like schools, parks and retail, potentially at a better price. This demand combined with the aged US housing stock shown in Exhibit 3 has fueled a surge in “fix and flip” activity in which real estate developers buy single-family residences with the intent of renovating and reselling at a profit within a short period of time. There is a similar dynamic evident in the multifamily space, as real estate investors seek to upgrade existing rental properties to standards that can command higher rents.

Of course, all of this requires capital. As commercial banks have pulled back from providing this type of financing, a fragmented group of specialty lenders has stepped in to fund these short-duration value-add renovation loans. The majority of these lenders lack the capital to underwrite and hold these loans at meaningful scale, however, and asset managers have been able to provide necessary liquidity to the real estate industry by purchasing individual loans to construct diversified portfolios with attractive risk-adjusted return potential.

Exhibit 3. Aging US Housing Supply May Drive Demand for Renovation Capital

Estimates of Median Age in Years of US Owner-Occupied Housing, 2005 through 2021

Source: US Census Bureau, American Housing Survey; data as of December 31, 2021.

Land banking. Another byproduct of post-crisis US housing market dynamics is a shortage of permitted, build-ready lots for single-family construction, as the ownership of such lots can substantially tie up capital on a homebuilder’s balance sheet. The top homebuilders are increasingly moving toward a “land light” business model, and off-balance-sheet financing solutions like land banking have become a staple of their land inventory-management strategies.

In an example land-banking deal, a lender may acquire an entitled, permitted and improved property while simultaneously entering into an agreement with a homebuilder giving it the option to acquire lots over time in exchange for a nonrefundable fee. The two parties commonly enter into a construction agreement whereby the builder is paid by the land banker to develop the land, and a “takedown schedule” governs the pace at which the homebuilder must acquire individual lots on that property. Homebuilders typically are willing to pay a significant spread over benchmark interest rates for the optionality and off-balance-sheet treatment a land-banking arrangement affords. Given their financial strength and long operating histories, large public homebuilders have the capacity to furnish significant upfront deposits and completion guarantees that smaller private homebuilders are unable to offer.

Public securities. The opportunity we see in US real estate debt is not limited to private deals, however; real-estate-linked publicly traded structured credit, for example, may also provide attractive potential yields and serve as a complement to private deals. In fact, investors able to opportunistically manage their exposures to both public and private real estate debt markets may be well-positioned to capture not only the benefits of each but also the relative-value discrepancies that periodically emerge between them.

Agency mortgage-backed securities (MBS)—issued and guaranteed by US government-sponsored enterprises (GSEs) Fannie Mae and Freddie Mac—are one of the largest and most active of the structured credit asset classes.8 The largest holders of high-quality MBS risk, GSEs have the implicit backing of the US government; as a result, agency MBS present very limited credit risk to investors and pay relatively low yield spreads as compensation for interest rate risk. GSEs mitigate their own credit risk exposure through the issuance of non-guaranteed credit-risk transfer (CRT) securities referencing pools of mortgages they own; as CRTs bear both credit risk and interest rate risk, they offer wider spreads than agency MBS. CRTs are issued in tranches of different seniorities and risk/return profiles, enabling investors to tailor their exposure across junior, more credit-intensive segments of these securitizations. Similar high-yielding opportunities also can potentially be found outside the agencies, such as through instruments linked to mortgage insurance and non-qualifying mortgages.

Since GSEs issue these securities primarily to mitigate risk, they tend to do so programmatically rather than strategically based on market conditions. This sometimes gives rise to pricing inefficiencies that can be exploited, especially as programmatic buyers like the Fed have pulled back from the market. Moreover, the reduced capital flows that accompany periodic market dislocations—such as the outbreak of Covid-19 in 2020 or the regional bank crisis in early 2023—can drive spreads significantly wider even if the underlying fundamentals of the mortgages backing the securities are little changed.

Getting the House in Order

While the US housing market today presents both challenges and opportunities, we believe its technical and fundamental dynamics reflect a persistent structural trend that will be supportive of mortgage credit in the near term. The fragmented specialty-lending segments discussed above tend to have high barriers to entry, however, highlighting the importance of sourcing, underwriting and structuring experience for those looking to leverage the ample opportunities we believe exist in residential real estate credit.