Macro & Market Views

Supporting a Solid Foundation for Insurance Portfolios

Supporting a Solid Foundation for Insurance Portfolios

Only introduced a few decades ago, structured credit—marketable fixed income securities collateralized by pools of similar, income-generating assets—has evolved into one of the largest segments of the US fixed income market. Assets eligible for securitization represent a broad range of cash streams, from the traditional (such as residential mortgages and corporate loans) to the more esoteric (such as airplane leases and music licensing revenues) and even to derivatives (such as swaps and options).

From a macroeconomic perspective, the securitization process effectively transfers the risk of a large amount of mostly illiquid debt from the original provider of capital—typically, banks or specialty finance companies—to investors, providing the seller with term, nonrecourse financing while also increasing the supply of credit in the system and promoting broader price discovery. For insurers, structured credit offers the potential for higher returns, portfolio diversification and tailored credit-risk exposure, serving as an attractive complement to an insurer’s corporate credit exposure with, in many cases, a similar risk-based capital factor and lower historical default risk.

While the greater complexity, reduced liquidity and pronounced price volatility of structured credit can be daunting to some, historical default rates point to durable opportunities for investors experienced in the asset class. We believe First Eagle’s expertise in the space combined with our dedicated insurance team can help insurers generate meaningful incremental yield with manageable incremental risk while leveraging key diversification benefits.

Insurers Continue to Tap into Credit Alternatives

The most recent report from the National Association of Insurance Commissioners (NAIC) showed that US insurers held nearly $9 trillion in cash and invested assets as of year-end 2024, a 5.3% increase from 2023 driven by investment gains and the strong underwriting environment.1 While corporate bonds and Treasuries continue to attract the lion’s share of assets, various types of structured credit instruments have continued to make inroads.

Structured credit—including asset-backed securities (ABS), collateralized loan obligations (CLOs) and various forms of residential and commercial mortgage-backed securities (RMBS and CMBS)—accounted for 27% of US insurers’ fixed income exposure at year-end 2024, up from 22% at year-end 2017. Most notable has been the increase in NAIC’s “ABS and Other Structured Securities” category, which climbed to 12.9% from 7.6%.2 While the shift was instigated by the search for yield in a prolonged environment of ultra-low interest rates, the appetite for the improved marginal rates of return, structural advantages and potential diversification benefits offered by what are perceived to be more complex holdings has persisted even as yields on traditional credit instruments returned to more attractive levels.

In our view, structured credit continues to represent a compelling option for insurers seeking a capital-efficient way to enhance return potential.

In our view, structured credit continues to represent a compelling option for insurers seeking a capital-efficient way to enhance return potential without significant marginal risk of default. Not only has structured credit historically offered higher risk-adjusted yields than corporates, the credit exposures underlying these securities provide insurers a way to enhance portfolio diversification.

The Large and Diverse World of Structured Credit

Structured credit instruments most commonly start with the bundling of income-producing credit assets and subsequent issuance of multiple debt securities collateralized by their cash flows. Synthetic structured credit has also grown in popularity in recent decades; in this instance, a basket of derivative contracts like credit default swaps (CDS) are grouped together and issued as an exchange-traded security (the credit default swap index, or CDX).

Claims on the cash flows from these asset pools are packaged into tranches that stratify credit risk based on seniority, providing investors the opportunity to target a range of risk/return profiles. Investors at the top of the capital structure have a priority claim on the cash flows and receive a relatively modest yield as a result. Tranches below the AAA rated senior paper pay higher coupons in exchange for subordination to the senior paper. At the bottom of the capital stack is a first-loss equity tranche—often owned in part by the originator to promote an alignment of interests—that has a claim on all residual cash flows once interest and principal is paid in full to all debtholders.

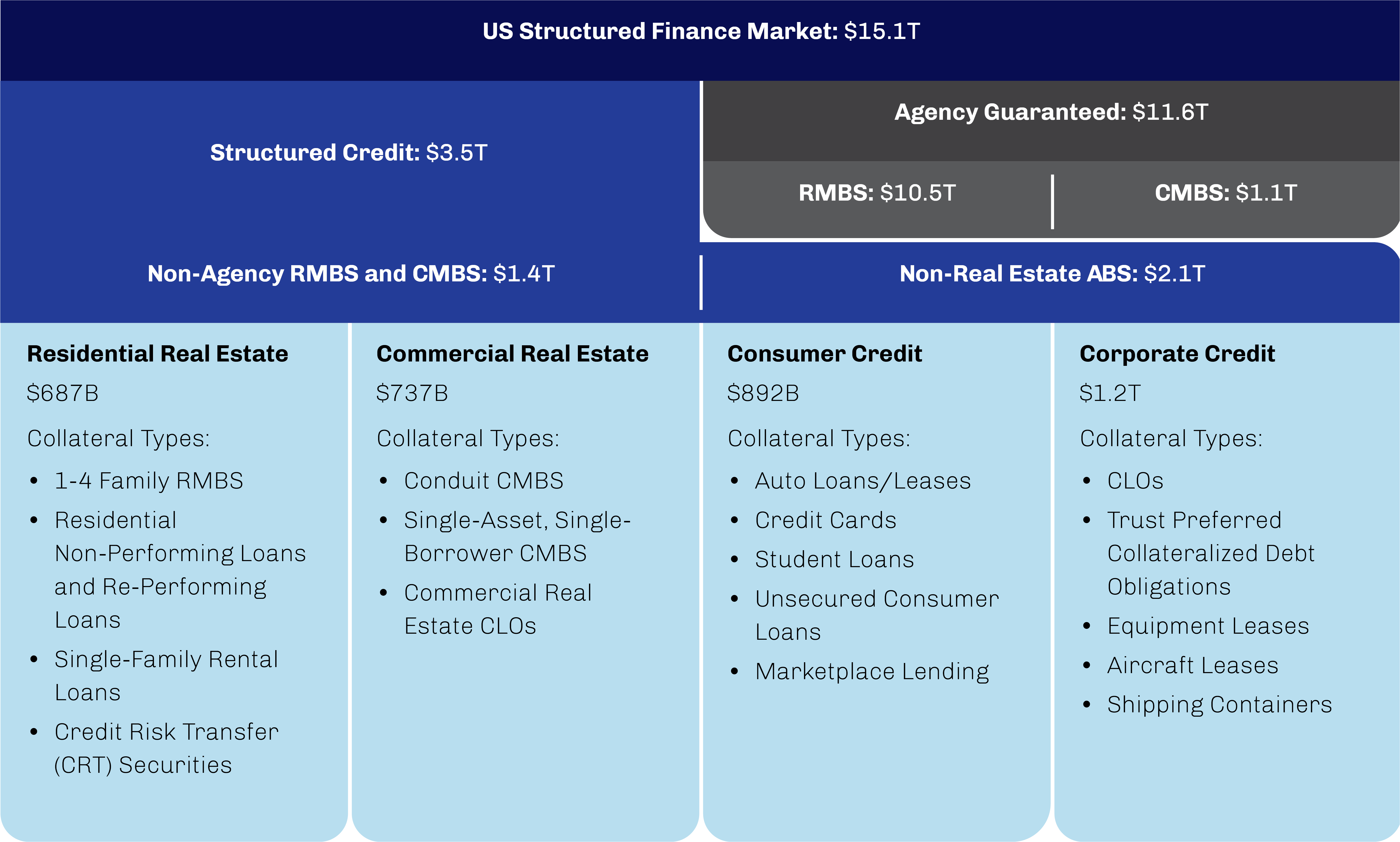

The market for structured credit is vast and varied. Structured credit outstanding in the US alone amounts to more than $15 trillion across a range of instruments and backed by a variety of collateral; this represents about 20% of all debt outstanding in the US, second only to Treasuries.3 Highlighted in shades of blue in Exhibit 1, the $3.5 trillion of securitized debt outstanding in the non-agency-guaranteed structured credit market is divided between securities backed by loans on real estate (both residential and commercial) and those backed by other forms of consumer and corporate credit. Most prominent in the latter category are CLOs, which are backed primarily by pools of broadly syndicated corporate loans, and ABS, which are backed by consumer debt such as student loans and credit card balances. More esoteric assets, with cash flows backed by everything from aircraft and shipping containers leases to music royalties and athletes’ earnings, have also become more prevalent in recent years.

Exhibit 1. Structured Credit Is a Large and Diverse Subset of the US Bond Market

Source: BofA Global Research; data as of August 31, 2025.

The growth in structured credit since its emergence in the 1980s should not come as a surprise. For banks and other originators, securitization provides a conduit through which they can manage credit risk and serves as an efficient alternative source of term, nonrecourse financing for a wide range of commercial and consumer loans. For investors, structured credit offers a number of features potentially beneficial to diversified portfolios, not the least of which is an attractive risk-adjusted yield.

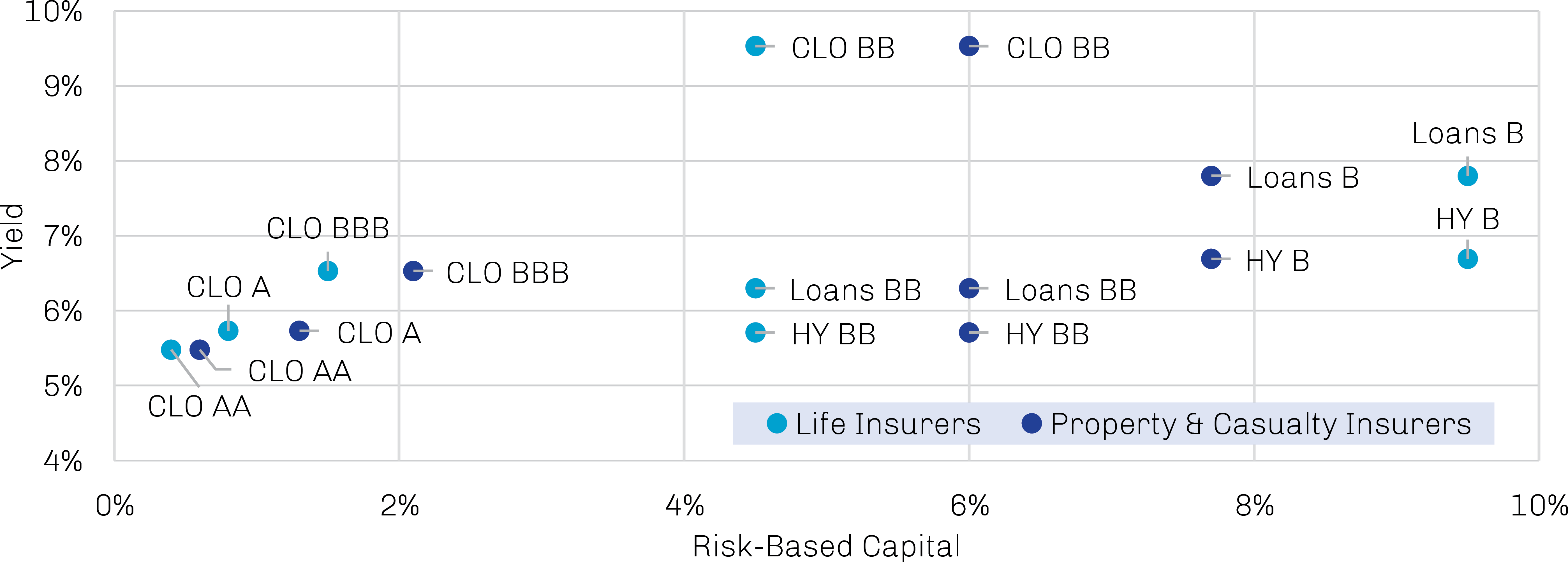

As shown in Exhibit 2, current yields on CLOs are very appealing thanks to normalized base rates and attractive spreads, and the pickup they offer relative to traditional corporate debt instruments is not a historical anomaly. For insurers, structured credit also represents an advantaged investment when adjusted for risk-based capital (RBC) requirements, as shown in Exhibit 3.

Exhibit 2. CLOs Currently Offer Attractive Yields on an Absolute Basis

Yields by Rating

Source: BofA Global Research, Markit, ICE Data Indices, PitchBook | LCD; data as of October 3, 2025.

Exhibit 3. and When Adjusted for Insurers’ Risk-Based Capital Requirements

Return per Unit of Risk-Based Capital

Source: BofA Global Research, Bloomberg, Citi, National Association of Insurance Commissioners; data as of September 30, 2025.

Yield Premia of Structured Credit Belies a Track Record of Limited Defaults

While there are a number of valid reasons for the structured credit premium—including the perception of greater complexity, potential reduced liquidity and potential price volatility, as we will discuss—we do not believe greater credit risk is one of them.

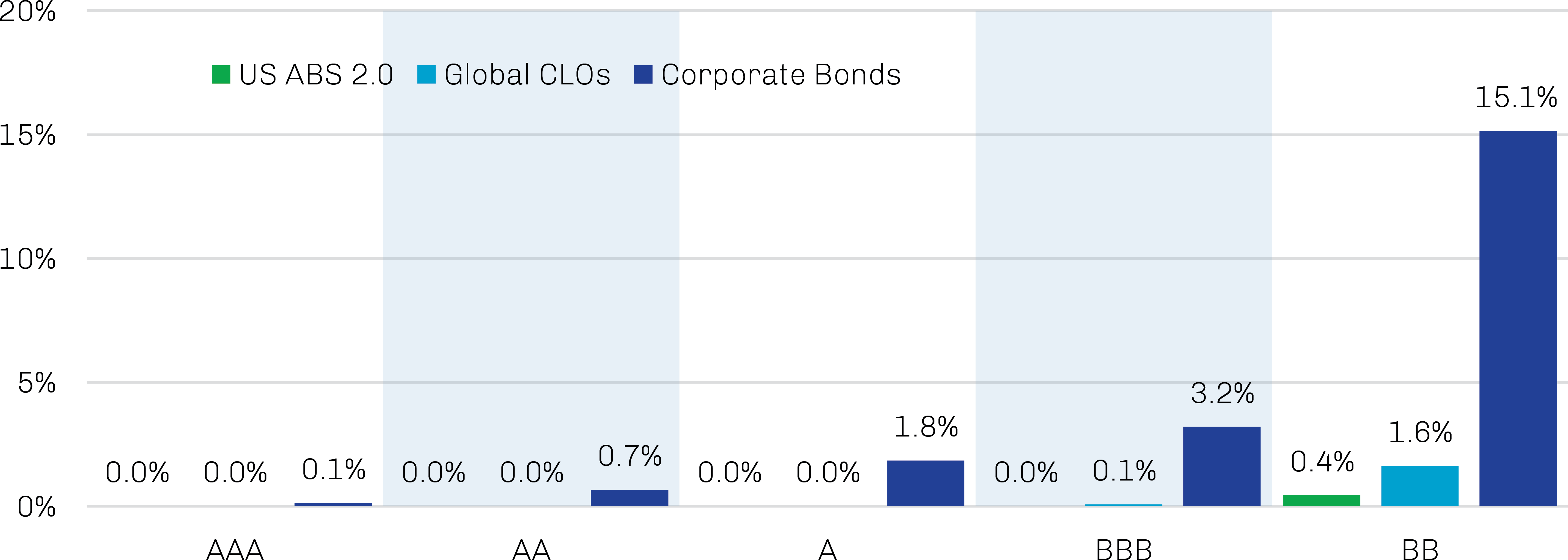

In fact, as depicted in Exhibit 4, certain structured products historically have realized significantly lower defaults than their like-rated traditional counterparts—including, in many cases, none at all. The difference is stark across the ratings spectrum; for example, the 15.1% default rate on BB rated corporate bonds is more than nine times greater than the 1.6% default rate of BB rated CLOs and significantly greater than the near-zero default rate of same-rated ABS. Meanwhile, there has only been one potential impairment globally among investment grade CLO 2.0 issues since the structure was introduced in 2009. The fact that corporate bonds pay a significantly lower yield despite much higher levels of historical default suggests to us a persistent mis-rating of structured credit by the ratings agencies—one that has promoted an ongoing yield premium in the markets and a potential corresponding opportunity for investors experienced in the space to generate attractive risk-adjusted returns over the long term.

Exhibit 4. Despite Meaningfully Lower Default Rates

Cumulative 10-Year Impairment/Default Rate by Original Rating

Note: US ABS 2.0 and Global CLOs reflect originations over 2009–24 and are not adjusted for issuers whose ratings were withdrawn. US ABS 2.0 data exclude home equity loans. Corporate bonds data reflect issuer-weighted defaults over 1920–2024.

Source: BofA Global Research, Moody’s Investors Services; data as of July 30, 2025.

Though often collateralized by the cash flows of the noninvestment grade and unrated debt that comprise their reference pools, as mentioned previously, structured credit securities are issued with ratings across the capital stack, from AAA to equity. There are several key—and, in our view, generally underappreciated—elements in these securities’ design that contribute to this transformation and have been factors behind their lower default rates:

Diversification. By design, each structured credit asset is backed by a pool of hundreds or even thousands of individual credits, spreading out the risk of any single default. We believe such broad diversification helps cushion the impact of potential losses, assuming the underlying assets are somewhat independent of each other.

Subordination. As noted earlier, cash flows from the collateral pool are divided into different levels of priority, with senior tranches receiving payments before junior ones. This “waterfall” structure means that junior tranches are the first to absorb losses in case of defaults, while senior tranches have a larger cushion.

Overcollateralization. Typically, the value of the underlying pool of assets exceeds the debt issued by the securitization, which serves as a cushion for investors. Regular checks are also conducted to ensure this cushion remains sufficient, and a failure to meet minimum levels may result in cash flows being redirected to more senior securities from junior ones.

Excess spread. Structured credit assets are usually designed such that the income generated by the assets exceeds the obligations to debtholders. This surplus (i.e., excess spread) serves as another buffer against defaults. While often distributed to equity investors, it can be diverted in support of the debt tranches if necessary.

Amortization. Many structured assets benefit from amortization through the distribution of excess spread during the life of the securitization. This results in a steady reduction of exposure and leverage, which can lead to credit rating upgrades for the issue’s mezzanine bonds as its senior debt is retired.

Guilt by Association

So if credit risk is not driving the yield differential between structured credit and traditional corporate bonds and loans, what is? While there are a number of concrete reasons why investors might demand additional compensation for investing in a structured credit product, as we will discuss below, we cannot help but think the reputation of these acronymic products has been tarnished by their perceived association with the global financial crisis.

The swiftly growing popularity of structured credit during the early 2000s may have proved a double-edged sword for the instruments. While the ability to decouple lending from risk inspired considerable innovation and the development of new and useful financial instruments, it also fostered an environment of lax oversight, deteriorating underwriting standards and the mis-assessment of risk—factors that many believe helped stoke the global financial crisis.

Certain types of structured assets that emerged in this period were consigned to history just as fast as they were created; this included products that purchased and re-securitized the lower-rated tranches of outstanding subprime mortgage-backed securities, which are often identified as being among the key archetypes of the crisis.4 Others, however, like CLOs, performed very well when held to maturity even while displaying extreme interim price volatility. And while the post-crisis regulatory overhaul—most notably through provisions within the Dodd–Frank Act of 2010—further bolstered investor safeguards embedded in structured assets, many market participants, both investors and ratings agencies, continue to approach all structured credits with trepidation.

This is not to say there are not a number of potential risks that are more pronounced in a structured credit investment relative to a similarly rated bond or loan. These risks are the primary source of incremental return, and experienced asset managers can seek to mitigate them as part of an active portfolio strategy. Perhaps most notable among the risks of structured credit are complexity and illiquidity.

Complexity. While the structural characteristics described earlier in this paper have helped support the strong performance of these assets over time, they also introduce a level of complexity that many investors find daunting. A structured credit asset comprised of hundreds or even thousands of individual collateral line items and subject to a range of idiosyncratic deal terms and contractual obligations is far more difficult to underwrite than a traditional bond of a single corporate issuer. The required investment of time, resources and technology, not to mention the necessary real-world expertise needed to invest successfully, serves as a hurdle for many institutional investors and constrains the buyer base for structured credit despite the large size of these markets. As a result, many insurers choose dedicated third-party investment managers, such as First Eagle, to manage their structured credit exposure.

Liquidity. With an active investor base already narrowed by the inherent complexity of structured products, particularly for noninvestment grade or mezzanine issuance, liquidity has been further impaired by regulatory changes following the global financial crisis that forced banks to curtail their market-making activities. Of course, these rules have not been limited to structured credit, and trading activity across fixed income markets at the onset of the Covid-19 pandemic in 2020 serves as a good example of how even assets viewed as conservative can be impacted by liquidity concerns when turmoil strikes.

Illiquidity in any asset tends to amplify its price movements to both the upside and downside. While the volatility in structured credit can be disquieting for some investors in challenging markets, it historically has proven transitory. Not only has the impairment of principal in structured credit been infrequent, but market price dislocations often have been followed by meaningful recoveries. Structured credit drawdowns in response to adverse events since the global financial crisis typically have been around double that of same-rated high yield bonds, though recoveries have been far more substantial.5 We believe this price action creates periodic opportunities for active managers like ourselves to acquire assets at a discount and potentially generate alpha through active portfolio rotation.6

Structured Credit Has Continued to Grow in Popularity with Insurers

While the complexity of the structured credit opportunity set can be daunting to some, insurance companies over time have found the juice to be worth the squeeze. For example, US insurers’ investment in CLOs has increased at a double-digit rate since 2018, and CLOs represented about 6% of life insurers’ portfolios by the end of 2024. In fact, insurance companies have become a key part of the CLO ecosystem, owning about 27% of outstanding CLOs and serving as anchor investors in a significant percentage of new-issue volume.7

Helping support the increasing popularity of CLOs and other structured credit assets among insurance investors has been their risk-based capital treatment and resulting capital efficiency. Insurers generally have exposure to noninvestment grade issuers both directly through broadly syndicated loans and high yield bonds and indirectly through CLOs. Despite being collateralized by noninvestment grade issues, investment grade tranches of a CLO—those with NAIC 1 or NAIC 2 designations—carry RBC factors similar to like-rated corporate bonds rather than the higher factors assigned to leveraged credits. For tightly regulated insurance investors, higher ratings hold great appeal; to wit, more than 95% of the industry’s total bond holdings at year-end 2024 were rated NAIC 1 or 2.8

There are reasons to believe that insurers will continue to look toward structured credit as an effective way to enhance the return potential of their fixed income portfolios, potentially without adding significant marginal risk. Not only has structured credit historically offered higher yields than traditional fixed income assets, the collateral assets underlying these securities provide an avenue to diversify the corporate credit risk that dominates traditional fixed income portfolios while floating rate coupons take the sting out of interest rate risk.

Meanwhile, concerns that upcoming adjustments to the NAIC’s risk-based capital framework would significantly impact the capital efficiency of structured assets like CLOs appear misplaced at this stage. Since first implementing RBC requirements in 1993, the NAIC has regularly updated its framework to promote insurer solvency amid a dynamic financial environment. Recent years has seen the standard-setting organization look to modernize its RBC framework in light of insurers’ increasingly complex portfolios. A key element of NAIC’s effort is eliminating the potential for “regulatory arbitrage” in structured securities, which occurs when the weighted- average risk factor of a structure is less than that of its underlying collateral; CLOs are its initial focal point.9

While the NAIC’s final guidelines are not scheduled to be implemented until year-end 2026,10 Moody’s research on preliminary risk distribution models suggest that the updated RBC framework is likely to further incentivize investment in highly rated CLO tranches while making mezzanine tranches less compelling from a capital-efficiency standpoint. In fact, most insurers with meaningful CLO holdings would see their RBC charges fall based on these projections. (Note that the NAIC had already increased the RBC factor on residual interests in 2024.)11

Structured Credit Is not Limited to Public Markets

Private structured credit is increasingly viewed as a valuable complement to traditional fixed income allocations, particularly for insurers seeking to enhance yield, diversify exposures and better align assets with liabilities. We focus on opportunities across core business finance, consumer credit and residential real estate, sectors in which regulatory and capital constraints have limited traditional bank lending. Typically negotiated directly between issuer and investor, these transactions allow for customized structures with strong collateral backing, shorter durations and compelling spreads relative to public market alternatives.

Private credit can offer a range of benefits that are well aligned with insurers’ portfolio objectives, including the potential for higher and more stable yields, predictable income streams and tailored structures that support liability matching. Robust covenants and asset-based collateral, meanwhile, help mitigate downside risk. While many investments fall outside the investment grade universe, options exist across the credit ratings spectrum for insurers with ratings-sensitive mandates. When managed by experienced teams with deep structuring and underwriting expertise, private structured credit can serve as a resilient, capital-efficient allocation that supports long-term performance and risk management goals.

First Eagle Offers Structured Credit Expertise and Dedicated Client Service for Insurers

Given attractive returns relative to traditional fixed income instruments on both an absolute basis and adjusted for statutory capital requirements, structured credit, in our view, may represent a compelling strategic allocation for insurance portfolios, as appropriate. While certain risks typical of structured credit such as complexity, illiquidity and volatility suggest a yield premium over traditional credit investments is warranted, historical default rates point to durable opportunities to harvest meaningful incremental yield with manageable incremental risk. However, these risks also represent barriers to entry into this market—even for large investors—and make the case for outsourcing the management of structured credit to a highly experienced, well-resourced investment manager.

Napier Park Global Capital, First Eagle’s global credit management platform, is one such manager. Led by structured credit pioneer Jon Dorfman—who was among the innovators and early risk takers in the credit-default swap, credit index and tranched-risk credit markets—our team brings extensive experience across a range of both public and private structured credit products and markets in the US and Europe. Consistently applying a time-tested, disciplined approach across market cycles, the team seeks to realize yield, avoid defaults and mitigate downside exposure on behalf of our clients.

We have been managing assets on behalf of insurance clients for more than 15 years. Our dedicated insurance team is focused on the development of 1) strategic relationships with our insurance partners, and 2) bespoke solutions that complement their portfolio asset allocation and liability profiles. With regulations in flux and markets ever-changing, the insurance specialists at First Eagle stand ready to evolve alongside the needs of our insurance clients globally. We are continually evaluating our product suite, and our size promotes a bespoke approach to tailoring custom investment solutions across asset classes and structures for insurers.

With a heritage dating back to 1864, First Eagle has served as a prudent steward of client capital across market cycles, varying macroeconomic conditions and numerous disruptive events. Distinguished by disciplined and unconventional thinking, a global perspective and the long-term alignment of interests, our actively managed strategies—which include alternatives, fixed income and equities—offer insurers a wide range of differentiated risk-return profiles backed by a shared emphasis on mitigating downside risk and preserving capital.