Macro & Market Views

Summertime Observations

Summertime Observations

First Eagle over time has deliberately sought to nurture an investment-led culture supported by a set of core investment tenets that encourages philosophical autonomy among our portfolio management teams in pursuit of client goals. While our four investment teams operate independently, we strongly believe each can benefit from the disciplined, unconventional thinking the others bring to bear in their areas of expertise. To share such insights broadly across the organization, we periodically assemble the senior members of our investment teams; below is an overview of some of the key issues raised at our midyear 2023 gathering.

Matt McLennan

Co-Head of Global Value Team

Looking at a variety of market indicators, it might be easy to get the impression that the world returned to normal during the first half of 2023. The S&P 500 Index was up nearly 17%, implied stock market volatility receded to pre-Covid levels, bond yields moderated and inflation expectations continued to ease.1 Ironically, the signs of cyclical improvements in US inflation data that have supported these sanguine developments may also be distracting markets from the emergence of more-worrying secular concerns—perhaps most notably, rising sovereign risk due to an erosion of the country’s fiscal position.

It’s possible that the regional bank failures we saw earlier in the year were the proverbial canaries in the coal mine warning us of hazardous conditions. Though each failure was idiosyncratic in nature, they all appeared to grow from a common root: the massive fiscal stimulus rolled out in response to the disruptions from Covid-19.

The expansion of the US money supply—M2 grew by about 40% from March 2020 to its peak in April 2022—led to a surge in commercial bank deposits.2 With loan activity off its peaks and interest rates near zero, banks sought profitable applications for these deposits. Many tried to scratch out marginal yield by increasing exposure to long-dated Treasuries. Given the government’s ability to print money, the risk of credit losses on US Treasuries is minimal; as such, bank capital guidelines assign US government securities a risk weighting of zero, meaning that banks are not required to hold a multiple of capital against these exposures as they are with risk assets. And though the duration risk of these Treasuries was no secret, many banks likely deemed the risk/reward acceptable given the 40-year downtrend in interest rates. They were wrong, of course, and paid dearly. Treasury yields picked up in late 2021 as inflation prints continued to rise, and the onset of aggressive Fed tightening—which came at a lag given the average inflation-targeting policy framework adopted by the central bank in 2020—accelerated their move higher.

So where did this unexpectedly strong surge in inflation come from? Economist John Cochrane has posited a theory of inflation that to me seems particularly well aligned with today’s dynamics. His “fiscal theory of the price level” states that “inflation adjusts so that the real value of government debt equals the present value of primary surpluses.” In essence, fiat money only has value because it’s required for the payment of taxes; thus, a government bond denominated in fiat only has real value if there is an expectation that there will be sufficient budget surpluses in the future such that the bond can be repaid in real terms. If such surpluses fail to materialize, additional bonds must be issued—which for existing holders of sovereign paper act as the equivalent of a share split. He goes on to point out that debt and deficits are not necessarily highly correlated with inflation if government credibility remains intact. If investors lose faith in the government’s ability to generate the necessary surpluses to repay the outstanding deficit, however, new debt can be inflationary.3

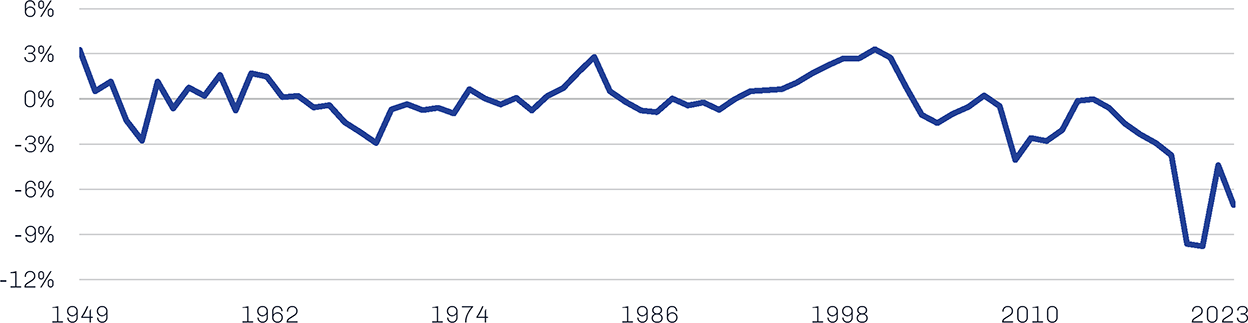

Exhibit 1 depicts the US government’s cyclically adjusted primary fiscal balance—the difference between federal non-interest spending and receipts—going back to World War II. Until about 2000, the government tended to run a small surplus on average, suggesting credibility as an issuer. Since then, however, there has been a meaningful erosion in the country’s fiscal picture, as crises have been met with deeper and deeper deficits while productivity improvements lag. At some point, it’s possible that market participants perceive the resumption of fiscal surpluses to be further into the future than had been typical in the twentieth century, leading to persistently above-target price increases amid sluggish economic growth—i.e., stagflation.

Exhibit 1. US Federal Deficit Has Increased with Each Successive Crisis in the Twenty-First Century

Primary Fiscal Balance as a Percentage of GDP, Adjusted for Output Gap; January 1949 through June 2023

Note: Primary deficit adjusted for output gap is primary deficit plus unemployment rate minus the noncyclical rate of unemployment (formerly called NAIRU). Primary balance calculated using interest outlays.

Source: Bureau of Economic Analysis, US Treasury, Federal Reserve Bank of St. Louis; data as of June 30, 2023.

The emergence of stagflationary conditions likely would have significant implications for asset markets. For those who don’t remember the 1970s, it may be helpful to briefly highlight some of the high-level dynamics that emerged during our most recent period of stagflation. The US equity market traded sideways while the price of real assets like oil and gold surged. Pressure on the dollar helped international equities outperform US stocks during the period, as did a normalization of the outsized relative valuations that had developed during the US growth stock boom of the late 1960s. Finally, value outperformed growth, as stocks with shorter-duration cash flow streams outperformed amid high inflation. Furthermore, by the end of the 1970s, equity multiples were about half of what they are currently while fixed income yields were about double; although past performance does not guarantee future results, we could be in for a long period of adjustment were a similar pattern to emerge in the mid-2020s.

Jon Dorfman

Chief Investment Officer, Napier Park

Since the financial crisis, credit as an asset class has been pretty dull to anyone but natural credit investors. We appear to be at an inflection point, however, as credit markets seem to be consistently offering investors equity-like returns—something we haven’t seen for decades. The Fed’s hiking cycle has spawned seismic shifts in the credit market, and absolute yield relative to risk appears to be more attractive than it has been since the early 2000s, for a few specific reasons that I can see:

There has been an enormous reduction in global liquidity, as persistently high inflation forced central banks to pivot toward restrictive policies after years of very easy money.

These tighter financial conditions have resulted in a dramatic increase in the cost of capital for companies, consumers and real estate investments.

Investors that built significant private market exposures over the years as an alternative to very low public market yields may face liquidity issues as distributions from these private investments wind down. Many rely on these distributions to fund capital calls on other unrelated private commitments. It’s likely the liquidity challenges that emerge when these distributions stop will exacerbate existing issues around the availability and cost of credit for borrowers.

Despite credit’s attractive pricing, I think there are still some challenges that have not yet been fully priced into markets—something that fundamentally driven investors such as ourselves should be able to navigate.

Bank lending standards historically have been highly correlated to defaults, and they are an indicator the team pays keen attention to. Banks began tightening their standards about 18 months ago—before the Fed began hiking rates in 2022 and prior to this year’s regional bank failures. Though the cost of credit has been higher for some time, default rates have been slow to react; rising interest rates and inflation generally have a lagged impact on the real economy, and strong corporate balance sheets also have helped insulate against short-term deterioration.

We think defaults will continue to rise over time, especially relative to what market participants have become accustomed to over the past 10-plus years; however, we do expect defaults to be sector- or asset-specific rather than systemic. This is counter to what we observe in credit markets, as spreads within many sectors are uniformly pricing in a near-term recession and more elevated level of default. We regard this as a potential opportunity, one that is likely to be durable given the time it will take for the economic picture to become truly clear.

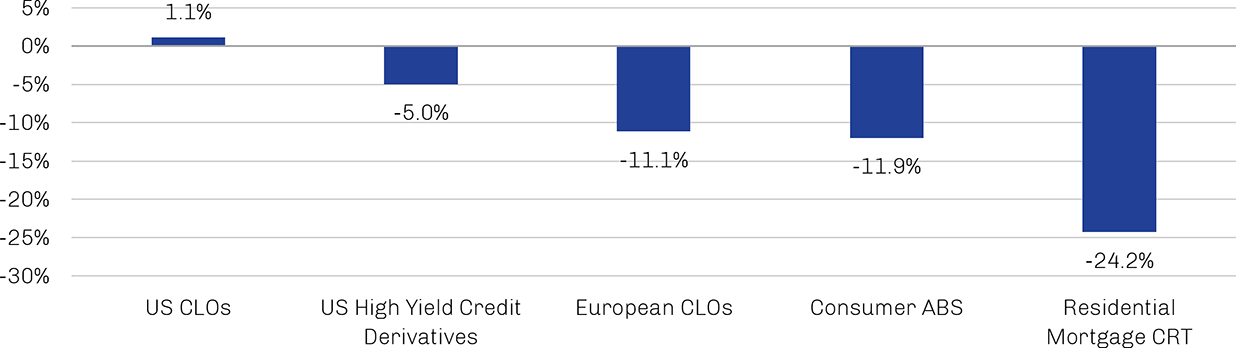

The environment of restricted capital and restricted liquidity has resulted in higher credit volatility and greater credit spread dispersion. Combined with falling trading volumes and tepid new issuance, these dynamics should continue to promote disparate changes in spreads across credit markets; as shown in Exhibit 2, this has been particularly true among the complex, structured instruments that are our areas of focus, such as US and European collateralized loan obligations (CLOs), consumer asset-backed securities (ABS) and residential mortgage credit-risk transfer (CRT) securities. In my view, these conditions should favor active credit managers.

Exhibit 2. Credit Spread Changes Have Varied Across Assets, Potentially Creating Opportunities

Percent Change in Credit Spreads, Year-to-Date 2023

Note: US CLOs = Palmer Square CLO BB Debt Index; US High Yield Credit Derivatives = Markit CDX North America High Yield Index; European CLOs = mid-level secondary-market trading spreads of euro-issued CLOs, both per- and post-crisis, as provided by JP Morgan; Consumer ABS = indicative spreads of benchmark names (LendingClub, SoFi, etc.), as provided by JP Morgan; Residential Mortgage CRT = an in-house, on-the-run B1 data set reported by Bank of America.

Note: US CLOs = Palmer Square CLO BB Debt Index; US High Yield Credit Derivatives = Markit CDX North America High Yield Index; European CLOs = mid-level secondary-market trading spreads of euro-issued CLOs, both per- and post-crisis, as provided by JP Morgan; Consumer ABS = indicative spreads of benchmark names (LendingClub, SoFi, etc.), as provided by JP Morgan; Residential Mortgage CRT = an in-house, on-the-run B1 data set reported by Bank of America.

Source: JP Morgan, BofA Securities, Bloomberg; data as of June 30, 2023.

Securitized and structured credit markets are pricing in extreme economic outcomes, to a much greater degree than other credit markets and US equities. Spreads on structured credits currently rank in the top decile to 15th percentile of their 10-year ranges, while spreads on more-liquid assets like high yield bonds and leveraged loans are closer to the 50th percentile.4 Given historically wide credit spreads and a much higher and continually rising base rate, overall yields are now at equity-like levels that we view as highly attractive. With losses on securitized credit highly likely to run well below the rate currently priced into the market, in our view, these assets may represent the kind of secular opportunity that lures non-credit investors into the credit space for the first time in 20 years.

Jim Fellows

Chief Investment Officer, First Eagle Alternative Credit

The broadly syndicated loan market has grown massively in the past few years as private providers of capital continued to disintermediate traditional Wall Street financing sources. The first half of 2023 was a different story, however, as both new-loan issuance and investor demand for loans dropped precipitously.

It’s perhaps ironic that while private lenders have been successful in disintermediating Wall Street banks, we remain dependent on these banks to drive the merger and acquisition (M&A) activity that fuels demand for the funding we provide. A rebound in equity prices and the uncertain trajectory of the economy has weighed on dealmaking this year, and M&A volumes have fallen sharply from their Covid-era peaks to deprive lenders of a key source of capital demand. Not only would an uptick in M&A activity bring more new loans to market, it also would promote price discovery and help break the stalemate in the secondary market that has resulted from wide bid-ask spreads.

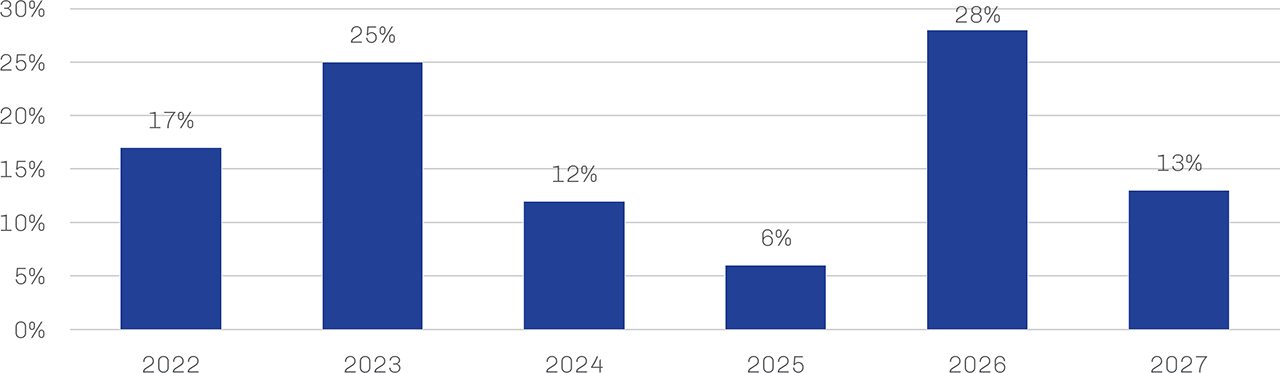

On the demand side, the lack of CLO formation has been a key headwind. CLOs have long been the primary buyers of loans, but with loan prices high and financing expensive, the economics of CLOs—particularly in the riskier tranches—is not compelling for investors. Another CLO-related source of near-term consternation for loan demand and liquidity is the unusually large percentage of outstanding CLOs exiting their reinvestment periods between now and year end. CLOs are structured to have finite lives, and there are guidelines in place that dictate what managers can and cannot buy during the various stages of a CLO’s lifecycle. While CLO managers have few restrictions on the loans they can buy and sell during the reinvestment period, they are quite constrained in their transactions during the amortization period that follows. As shown in Exhibit 3, about 40% of the CLO market will be in amortization by the end of 2023.5 This will represent a significant technical headwind to primary and secondary loan demand, while the inability of some managers to provide “amend and extend” deals to existing borrowers may push companies teetering on default over the edge. While none of this posed a problem in a world of free money and unrelenting demand for leveraged credit, the price of poker has gone up substantially.

Exhibit 3. Large Percentage of CLOs Outside Their Reinvestment Period Is a Headwind to Loan Demand

Share of CLO Market Exiting Reinvestment Period, 2022 through 2027

Source: BofA Securities, Bloomberg; data as of January 5, 2023.

Source: BofA Securities, Bloomberg; data as of January 5, 2023.

Borrower fundamentals have held up well despite the massive increase in interest rates; leverage is moderate, for example, and interest coverage ratios are fairly high. But the full impact of rate hikes has yet to be felt, and I think it’s wise to be cautious here. Rating agencies seem to agree—not surprising given the negative feedback they received for their slow response during the global financial crisis—and downgrades have outpaced upgrades for 13 consecutive months through June. Borrowers rates B- or lower now comprise a record-high 36% of the Morningstar LSTA US Leveraged Loan Index.6 Generally speaking, lower ratings tend to curb the demand for loans, and a bias toward downgrades typically results in greater price volatility, less new issuance and more refinancing challenges.

Talk of downgrades and defaults naturally leads to the topic of recoveries. From 1990 through 2022, the recovery rate on defaulted loans in the US was around 73%, meaning that lenders could expect to recover nearly three-quarters of par value, on average, in the event of a loan’s default.7 There are reasons to believe recoveries will fall short of the historical average during the current cycle, however, including the prevalence of covenant-lite loans, the sizable shrinkage of the CLO market as vehicles exit reinvestment and the lack of structure in the loan secondary market.

The pace of activity in the middle market direct lending space also has been sluggish. But deals are getting done, and investors are picking up additional yield relative to loans as an illiquidity premium. Given that the concept of syndicated loan “liquidity” appears overstated in light of the secondary-market circumstances I referenced earlier, private credit may represent an attractive place to park capital at the moment. Meanwhile, an uptick in M&A activity could provide interesting opportunities for private lenders and their massive amounts of dry powder.

Bill Hench

Head of Small Cap Team

As an investor focused on the small cap market, I find myself in a very different position than my colleagues on this panel, primarily in terms of the valuation of my investment universe. Mean reversion historically has had a powerful influence over financial markets, and the disparities from the norm that exist today suggest a strong potential tailwind for small cap stocks. In our view, this is especially true for small cap value stocks; over the long term, the Russell 2000 Value Index has outperformed the Russell 2000 Growth Index as well as the Russell 1000 Value and Growth indexes.8

While the Russell 2000 Index outpaced the S&P 500 Index for much of the first quarter, March’s bank failures appeared to have had a disproportionately large negative impact on investor sentiment toward smaller names. Given their historical volatility, it was not surprising that small caps sold off more than large caps during that crisis.9 However, we were somewhat disappointed by the performance of small caps once large caps began to rebound; historically, small companies generally lead markets in up quarters while lagging during down periods. That said, we believe the lagging response this year presented additional opportunities to acquire companies whose catalysts for positive change had yet to be recognized by the market, suggesting a potential for greater upside should long-term relationships normalize.

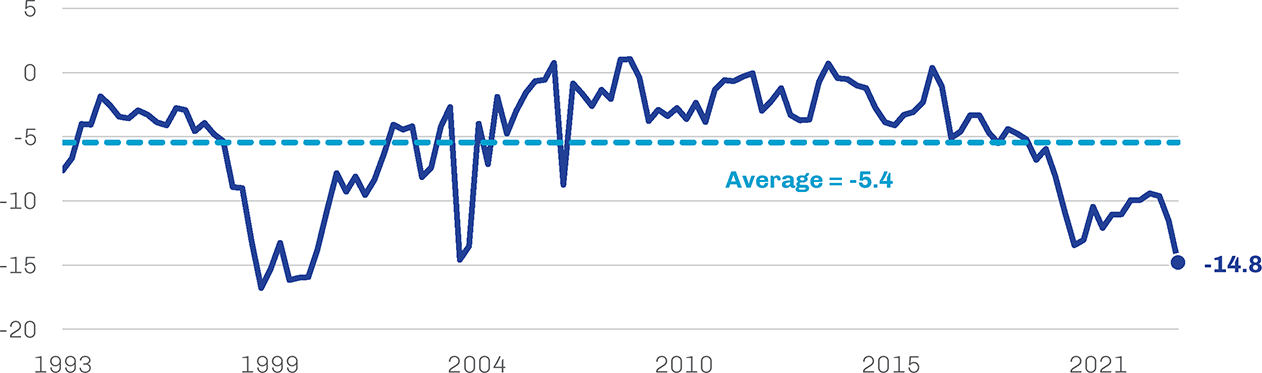

As a result of these dynamics, the Russell 2000 trades at a discount of about 30% to its long-term average priceto-earnings (P/E) ratio while the S&P 500 is again trading at a premium.10 The last time the Russell 2000 traded as cheaply was during the global financial crisis—and it delivered annual average returns of 30% for the three years that followed that bottom.11 While there’s obviously no guarantee this will happen again, it’s a nice precedent to be aware of. Though small cap stocks in general appear undervalued relative to their history, small cap value stocks look even cheaper when compared with large cap names. As shown in Exhibit 4, the spread between the P/E ratios of the Russell 2000 Value Index and the S&P 500 is at a level not seen since the early 2000s. A similar trend can be found using a variety of other valuation metrics, including price to sales and price to book.12

Exhibit 4. Small Cap Value’s Discount to Large Caps Has Widened to Early-2000s Levels

Spread Between the Weighted Average Price-to-Earnings Ratios of Russell 2000 and S&P 500 Indexes, January 1993 through June 2023

Source: FactSet; data as of June 30, 2023.

Source: FactSet; data as of June 30, 2023.

Sometimes performance on the smaller end of the capitalization spectrum, particularly among value stocks, is more about an abatement of selling pressure than any newfound buying enthusiasm. This may be part of the dynamic we witnessed in the second quarter, when small stocks moved higher but significantly lagged the mega-cap market darlings. In past cycles, little hints often emerged to suggest that the market tide may be turning in the favor of small caps. Sometimes this came in the form of M&A activity, as the same valuation discounts we see as investors are recognized by both strategic and financial buyers. While the current cost of capital may serve as a headwind, at some point the acquisition price of a company becomes too good to pass up, and we’ve begun to see a little bit of this already.

For fundamental investors, the real momentum comes when things improve at the individual stock level—as a manufacturer gets new funding, for example, or a restaurant chain improves the quality of its offering. At this point, you begin to see some separation in performance within the indexes—the newfound buying enthusiasm I mentioned earlier—especially if the broader macro environment is supportive. Those who were able to take advantage of the small cap market’s characteristic volatility to acquire quality companies at attractive prices should benefit from this revaluation, whenever it occurs.

Source: FactSet; data as of June 30, 2023.

Source: Federal Reserve; data as of June 30, 2023.

John H. Cochrane, “Fiscal Histories,” Journal of Economic Perspectives, Vol. 36, No. 4 (Fall 2022)

Source: JP Morgan; data as of March 31, 2023.

Source: BofA Securities, Bloomberg; data as of January 5, 2023.

Source: PitchBook | LCD; data as of June 30, 2023

Source: PitchBook | LCD; data as of December 31, 2022.

,9,10,11,12. Source: FactSet; data as of June 30, 2023.