Macro & Market Views

Structured Credit: Seeing the Forest for the Trees

Structured Credit: Seeing the Forest for the Trees

Structured credit typically refers to the process by which groups of similar, income-generating assets are pooled together into marketable fixed income securities. The assets comprising these pools may include traditional debt instruments (like residential mortgages and corporate loans), more esoteric cash streams (like airplane leases and music licensing revenues) or derivatives contracts (like swaps and options).

From a macroeconomic perspective, the securitization process effectively transfers the risk of a large amount of mostly illiquid debt from the original provider of capital—typically, banks or specialty finance companies—to investors, providing the seller with term, non-recourse financing while also increasing the supply of credit in the system and promoting broader price discovery. For investors, structured credit offers the potential for higher returns, portfolio diversification and tailored credit-risk exposure.

While certain risks typical of structured credit—such as complexity, illiquidity and volatility—suggest a yield premium over traditional credit investments is warranted, we believe other factors also may play a role. Perhaps most notable among these is what we view as a persistent disconnect between the ratings assigned to the structured products and their realized default rate. By consistently applying more punitive criteria to the evaluation of structured credit investments compared to traditional corporate or consumer debt, rating agencies historically have created durable opportunities for investors experienced in the asset class to harvest meaningful incremental yield with manageable incremental risk. Given the attractive risk-adjusted returns structured credit has generated over time, we believe the asset class may represent a compelling strategic allocation for many long-term portfolios, as appropriate.

A Large and Diverse Asset Class

Structured credit instruments most commonly start with the bundling of income-producing credit assets and subsequent issuance of multiple debt securities collateralized by their cash flows. Also gaining popularity in recent decades have been synthetic structures in which a basket of derivative contracts (like credit default swaps, or CDS) are grouped together and issued as an exchange-traded security (the credit default swap index, or CDX). Claims on these cash flows or derivative payments are divided into tranches that stratify credit risk based on seniority, providing investors the opportunity to target a range of risk/return profiles. Investors higher in the capital structure have a priority claim on the asset pool’s cash flows and receive a relatively lower yield as a result, while those further down in the structure are most susceptible to impairments and defaults but also receive greater compensation for these risks. In addition to multiple debt tranches, securitizations typically include a first-loss equity tranche—often owned in part by the originator to promote an alignment of interests— that has a claim on all residual cash flows once interest and principal is paid in full to debtholders.

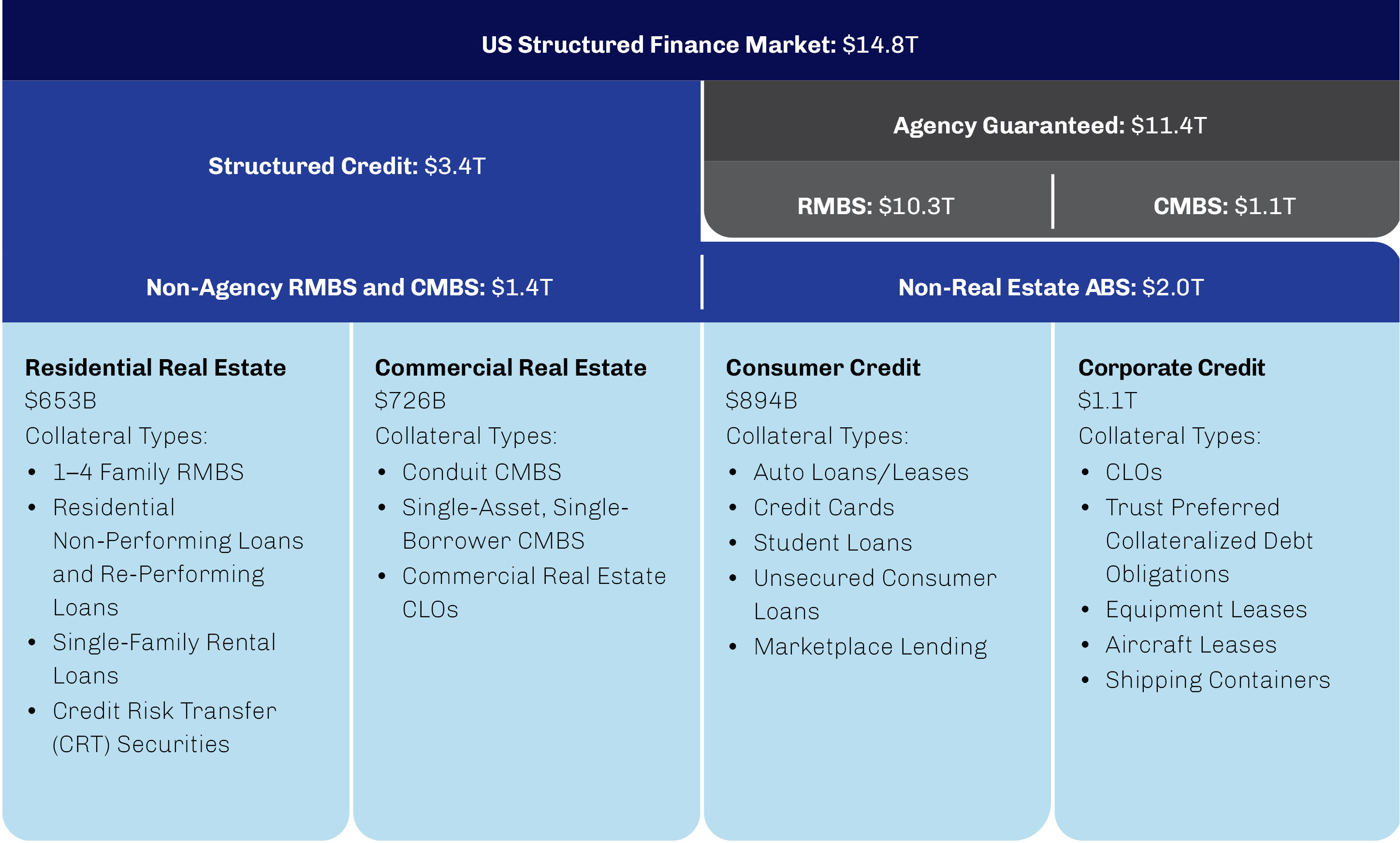

The market for structured credit is vast and varied. Structured credit outstanding in the US alone amounts to nearly $15 trillion across a range of instruments and backed by a variety of collateral; this represents about 25% of all debt outstanding in the US, second only to Treasuries.1 Highlighted in shades of blue in Exhibit 1, the $3.4 trillion of securitized debt outstanding in the non-agency-guaranteed structured credit market is divided between securities backed by loans on real estate (both residential and commercial) and those backed by other forms of consumer and corporate credit. Collateralized loan obligations (CLOs), which are backed by pools of broadly syndicated corporate loans, and asset-backed securities (ABS), backed by consumer debt such as student loans and credit card balances, are the most prominent forms of the latter category. But more esoteric products also are available, with cash flows backed by everything from aircraft and shipping containers leases to music royalties (aka “Bowie Bonds” in honor of the first musician to participate in such a securitization).

Exhibit 1. Structured Credit Is a Large and Diverse Subset of the US Bond Market

Source: BofA Global Research; data as of March 31, 2025.

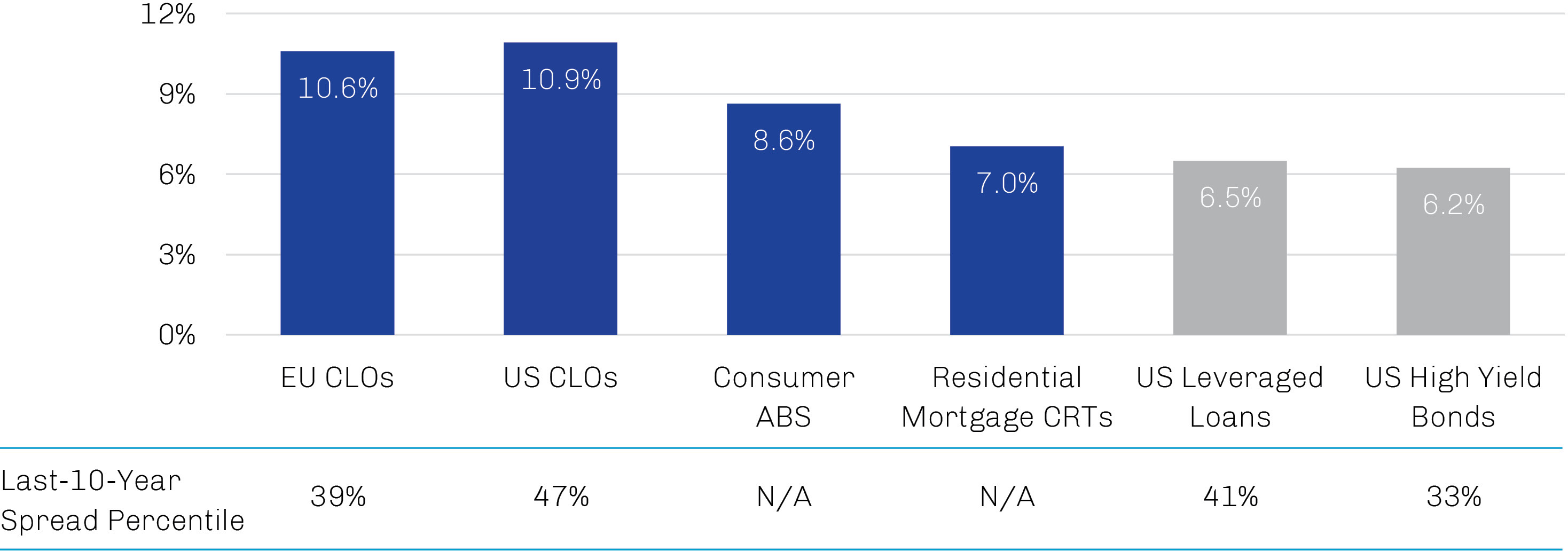

The growth in structured credit since its emergence in the 1980s should not come as a surprise. For banks and other originators, securitization provides a conduit through which they can manage credit risk and serves as an efficient alternative source of term, nonrecourse financing for a wide range of commercial and consumer loans. For investors, structured credit offers a number of features potentially beneficial to diversified portfolios, not the least of which is an attractive risk-adjusted yield. As shown in Exhibit 2, yields on certain structured credit instruments appear quite appealing thanks to normalized base rates and attractive spreads.

Exhibit 2. Structured Credit Markets Currently Offer Attractive Yields and Spreads

Note: EU CLOs = midpoint pricing levels of BB rated EU CLOs observed by the JPMorgan trading desk, with yield hedged to US dollar; US CLOs = BB rated US CLOs from PricingDirect; Consumer ABS = BB rated marketplace consumer loans of benchmark names (LendingClub, SoFi, etc.) observed by the JPMorgan trading desk; Residential Mortgage CRTs = Agency CRT B2s from PricingDirect; US Leveraged Loans = BB rated loans with pricing data from PricingDirect; US High Yield Bonds = BB rated bonds with pricing data from PricingDirect. Source: JPMorgan; data as of May 6, 2025.

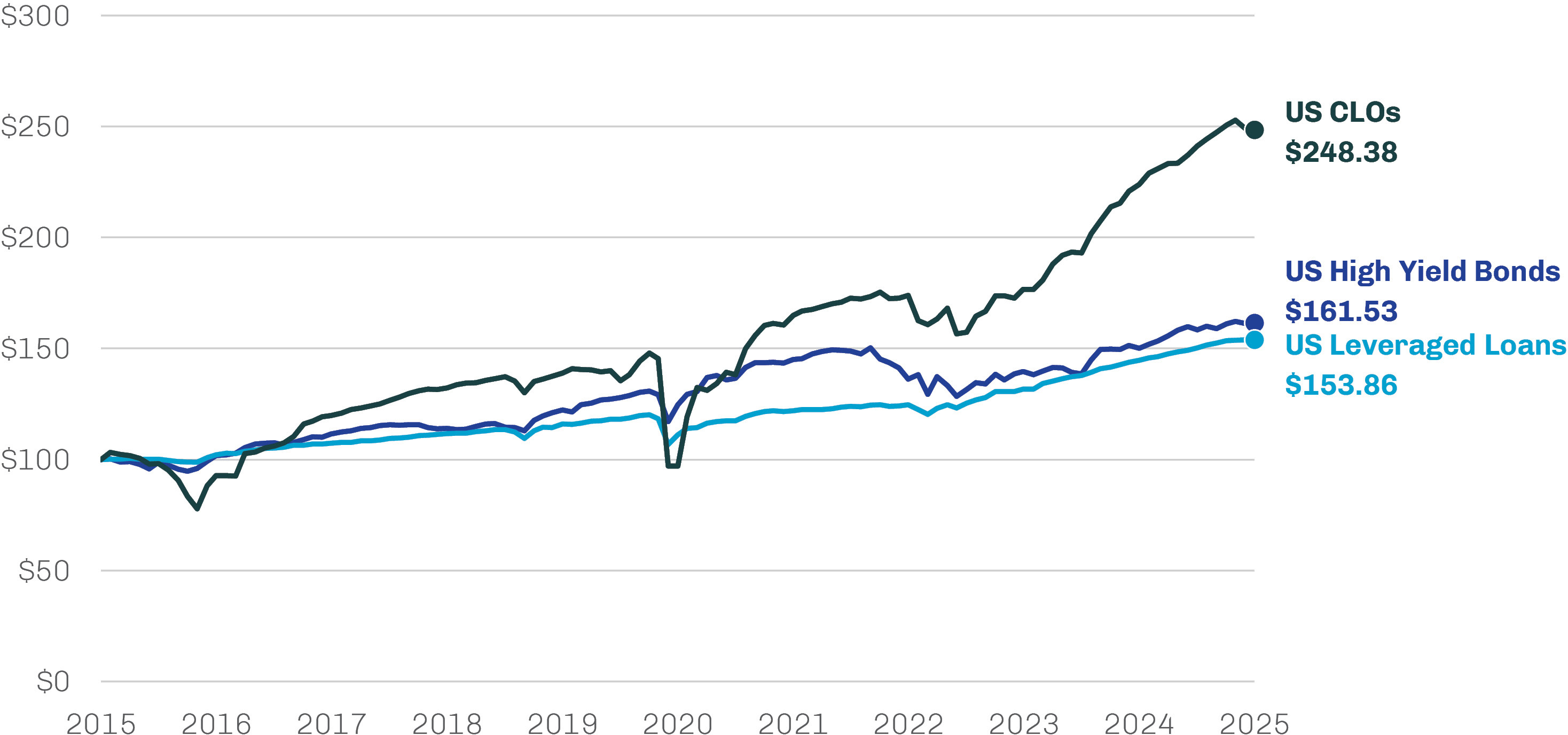

Historical total returns have been compelling as well. Exhibit 3 illustrates the cumulative growth of selected assets over the past 10 years, a period during which structured credit (as represented by BB rated US CLOs) more than doubled the performance of BB rated high yield bonds and leveraged loans—and highlighted that all ratings are not necessarily equal.

Exhibit 3. Structured Credit Has Delivered a Compelling Cumulative Return over the Past 10 Years

Growth of $100, May 2015 through April 2025

Note: US CLOs = BB rated subindex of the JPMorgan Collateralized Loan Obligation Index (CLOIE); US High Yield Bonds = Bloomberg US Corporate High Yield Index; US Leveraged Loans = Return from Pitchbook | LCD. Please refer to Index disclaimer at the end of document. Source: JPMorgan, Pitchbook | LCD, Bloomberg; data as of April 30, 2025

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. ACTUAL RESULTS MAY VARY.

Yield Premia of Structured Credit Belies a Track Record of Limited Defaults

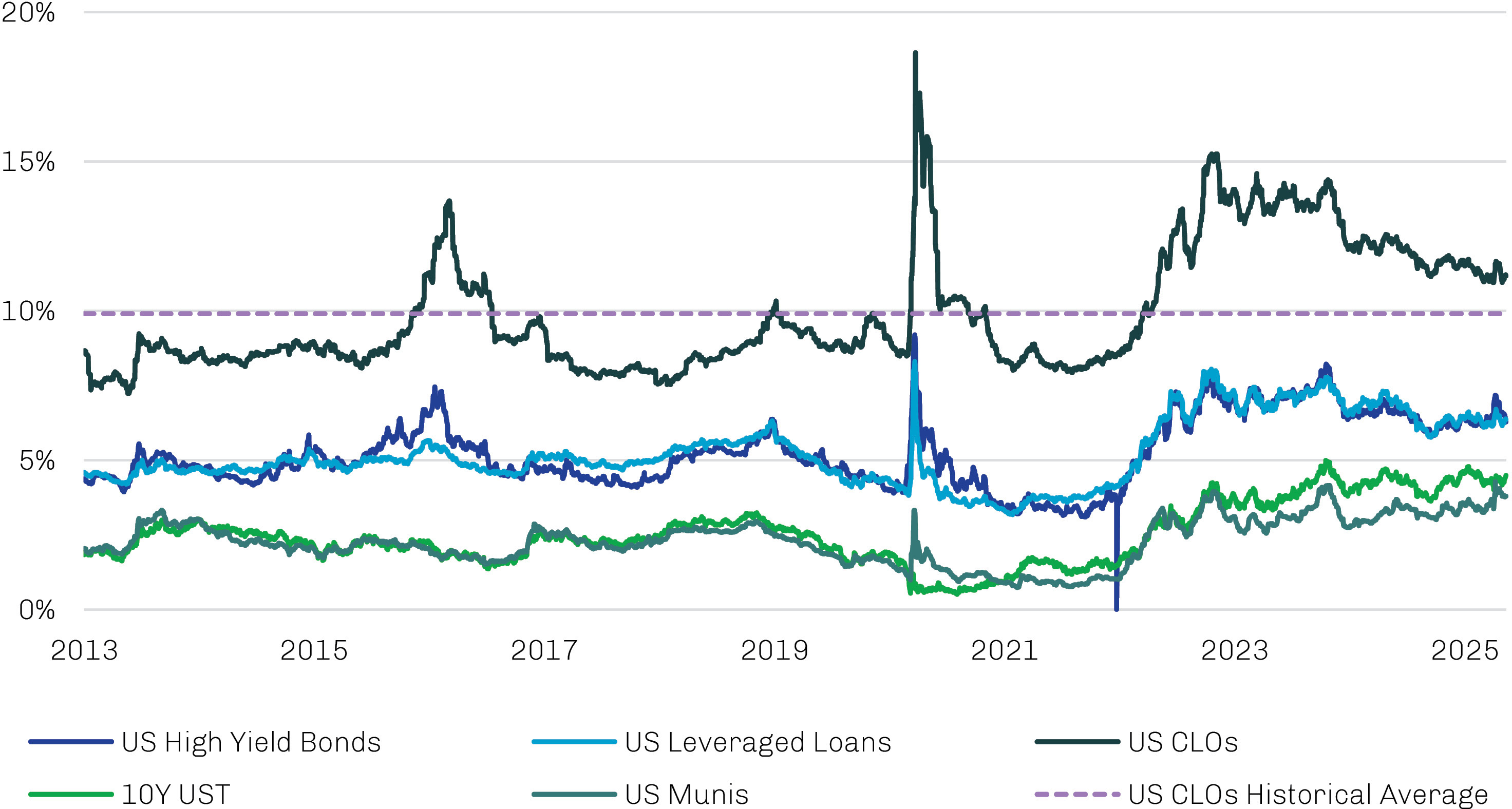

Though the yield differential between structured and traditional credit currently is wider than typical, the existence of such a gap is far from novel; as shown in Exhibit 4, structured credit instruments historically have offered an attractive yield pickup relative to traditional fixed income investments. While there are a number of valid reasons for the structured credit premium—including greater complexity, reduced liquidity and pronounced price volatility, as we’ll discuss— we believe that greater credit risk is not one of them.

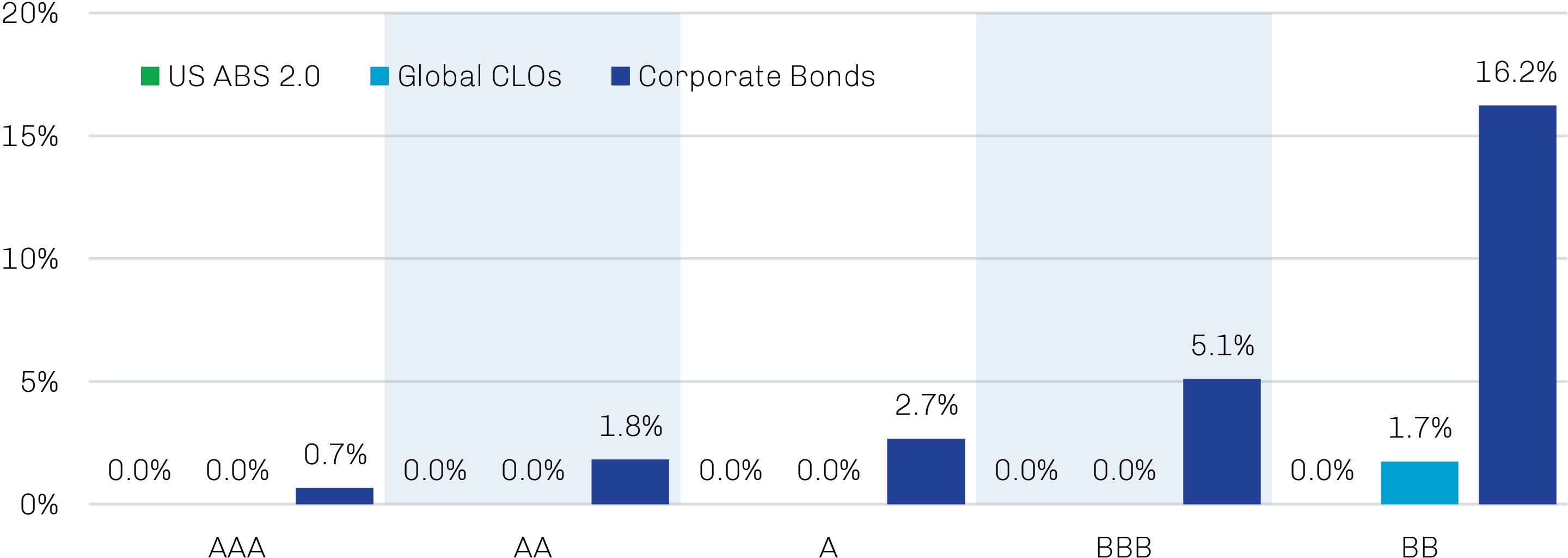

In fact, as depicted in Exhibit 5, certain structured products historically have realized significantly lower defaults than their like-rated traditional counterparts—including, in many cases, none at all. Even among non-investment grade tranches, the difference is stark; the 16.2% default rate on BB rated corporate bonds is more than nine times greater than the 1.7% default rate of BB rated CLOs and significantly greater than zero-default ABS of the same rating. The fact that corporate bonds pay a significantly lower yield despite much higher levels of historical default suggests to us a persistent mis-rating of structured credit by the ratings agencies—one that has promoted an ongoing yield premium in the markets and a potential corresponding opportunity for investors experienced in the space to generate attractive risk-adjusted returns over the long term.

Exhibit 4. Structured Credit Historically Has Offered Higher Yields than Traditional Fixed Income and Corporate Debt Investments…

Yields of Select Fixed Income Sectors, January 2013 through May 2025

Note: 10Y UST = 10-Year US Treasury Bond; US Munis = Bloomberg 10-Year Municipal Bond Index; US High Yield Bonds = JPMorgan High Yield BB Index; US Leveraged Loans = JPMorgan Leveraged Loan BB Index; US CLOs = BB rated CLO spreads from PricingDirect plus five-year US Treasury yields. Refer to Disclaimer for index information at the end of the document. Source: JPMorgan, Bloomberg; data as of May 13, 2025.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. ACTUAL RESULTS MAY VARY.

Exhibit 5. …Despite Meaningfully Lower Default Rates

Cumulative 10-Year Impairment/Default Rate by Original Rating

Note: US ABS 2.0 and Global CLOs reflect originations over 2009–23 (i.e., after the global financial crisis) and are not adjusted for issuers whose ratings were withdrawn. US ABS 2.0 data exclude home equity loans. Corporate bonds data reflect issuer-weighted defaults over 1920–2023. Source: BofA Global Research, Moody’s Investors Services; data as of June 30, 2024.

The ratings scales employed by S&P Global Ratings, Moody’s Investors Services and others are intended to be comparable across issuers; that is to say, a BBB rated CLO is considered as capable and willing to meet its financial commitments as a BBB rated corporate or BBB sovereign bond. Referring back to the default rates depicted in Exhibit 5, however, it seems ratings agencies have been more conservative in assigning ratings to structured credits than they have been with generic credit instruments. In our opinion, one could argue that the BB rated cohorts of ABS and CLOs depicted in the chart likely were deserving of investment grade ratings given realized default rates less than that of both BBB and A rated corporates. We believe investors able to differentiate between an instrument’s rating and its actual credit risk through detailed underwriting of the underlying collateral and vigorous structural analysis may take advantage of agency mis-ratings to seek incremental income.

Though often collateralized by the cash flows of the non-investment grade and unrated debt that comprise their reference pools, structured credit securities are issued with ratings across the spectrum, including investment grade (AAA to BBB). There are several key—and, in our view, generally underappreciated—elements in these securities’ design that contribute to this transformation and have been factors behind their lower default rates.

Diversification. By design, each structured credit security is backed by a pool of hundreds or even thousands of individual credits, spreading out the risk of any single default. We believe such broad diversification helps cushion the impact of potential losses, assuming the underlying assets are somewhat independent of each other.

Subordination. As noted earlier, cash flows from the collateral pool are divided into different levels of priority, with senior tranches receiving payments before junior ones. This “waterfall” structure means that junior tranches are the first to absorb losses in case of defaults, while senior tranches have a larger cushion.

Overcollateralization. Typically, the value of the underlying pool of assets exceeds the debt issued by the securitization which serves as a cushion for investors. Regular checks are also conducted to ensure this cushion remains sufficient, and a failure to meet minimum levels may result in cash flows being redirected to more senior securities from junior ones.

Excess spread. Structured credit products usually are designed such that the income generated by the assets exceeds the obligations to debtholders. This surplus (aka excess spread) serves as another buffer against defaults. While often distributed to equity investors, it can be diverted in support of the debt tranches if necessary.

Amortization. Many structured assets benefit from amortization through the distribution of excess spread during the life of the securitization. This results in a steady reduction of exposure and leverage, which can lead to credit rating upgrades for the issue’s mezzanine bonds as its senior debt is retired.

Guilt by Association

So if credit risk isn’t driving the yield differential between structured credit and traditional corporate bonds and loans, what is? While there are a number of concrete reasons why investors might demand additional compensation for investing in a structured credit product, as we will discuss below, we can’t help but think the reputation of these acronymic products has been tarnished by their perceived association with the global financial crisis.

The swiftly growing popularity of structured credit during the early 2000s may have proved a double-edged sword for the instruments. While the ability to decouple lending from risk inspired considerable innovation and the development of new and useful financial instruments, it also fostered an environment of lax oversight, deteriorating underwriting standards and the mis-assessment of risk—factors that many believe helped stoke the global financial crisis. Certain types of structured assets that emerged in this period were consigned to history just as fast they were created; this included products that purchased and re-securitized the lower-rated tranches of outstanding subprime mortgage-backed securities, which are often identified as being among the key archetypes of the crisis.2 Others, however, like CLOs, performed very well when held to maturity even while displaying extreme interim price volatility. And while the post-crisis regulatory overhaul—most notably through provisions within the Dodd-Frank Act of 2010—further bolstered investor safeguards embedded in structured assets, many market participants, both investors and ratings agencies, continue to approach all structured credits with trepidation. (See text box below for more information.)

This is not to say there aren’t a number of risks that are more pronounced in a structured credit product relative to a similarly rated bond or loan. These risks are the primary source of incremental return, and experienced investors can seek to manage them as part of an active portfolio strategy. Perhaps most notable among the risks of structured credit are complexity and illiquidity.

Complexity. While the structural characteristics described earlier in this paper have helped support the strong performance of these assets over time, they also introduce a level of complexity that many investors find daunting. A structured credit product comprised of hundreds or even thousands of individual collateral assets and subject to a range of idiosyncratic deal terms and contractual obligations is far more difficult to appraise than the generic bond of a single corporate issuer. The required investment of time, resources and technology, not to mention the necessary real-world expertise needed to invest successfully, serves as a hurdle for many institutional investors and constrains the buyer base for structured credit despite the large size of these markets.

Liquidity. With an active investor base already narrowed by the inherent complexity of structured products, particularly for non-investment grade or mezzanine issuance, liquidity has been further impaired by regulatory changes following the global financial crisis that forced banks to curtail their market-making activities. Of course, these rules have not been limited to structured credit, and trading activity across fixed income markets at the onset of the Covid-19 pandemic in 2020 serves as a good example of how even assets viewed as conservative can be impacted by liquidity concerns when turmoil strikes.

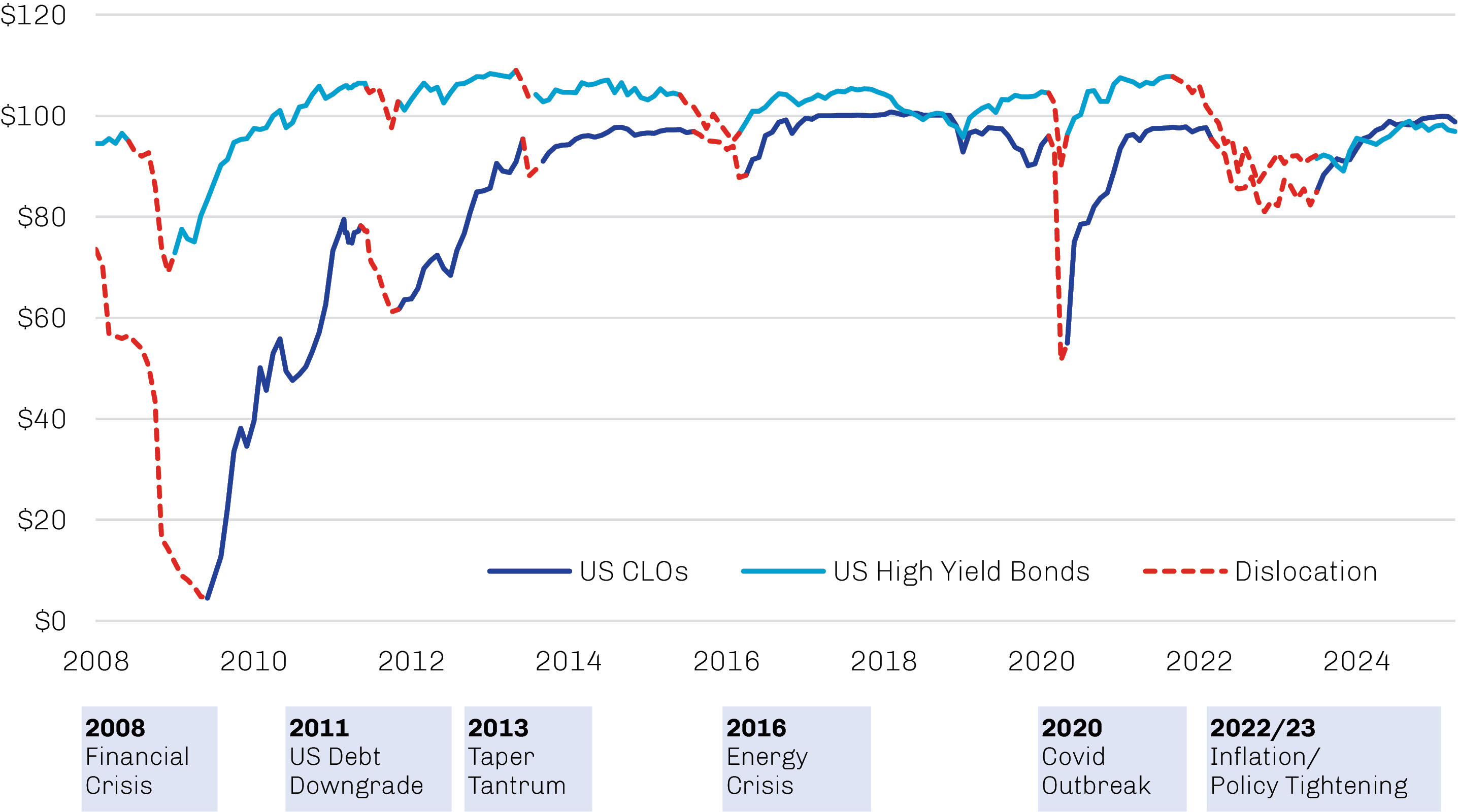

Illiquidity in any asset tends to amplify its price movements to both the upside and downside. While the volatility in structured credit can be disquieting for some investors in challenging markets, it historically has proven transitory. Not only has the impairment of principal in structured credit been infrequent, but market price dislocations often have also been followed by meaningful recoveries. As shown in Exhibit 6, structured credit drawdowns in response to adverse events since the global financial crisis typically have been around double that of same-rated high yield bonds, though recoveries have been far more substantial. We believe this price action creates periodic opportunities for active managers like ourselves to acquire assets at a discount and potentially generate alpha through active portfolio rotation.

Exhibit 6. Structured Credit Prices Have Been Marked by Deep Selloffs and Furious Rebounds

Asset Prices, January 2008 through April 2025

Note: US CLOs = BB rated CLO prices from PricingDirect plus five-year US Treasury yields; US High Yield Bonds = Bloomberg High Yield BB Index. Source: Citi, Bloomberg; data as of April 30, 2025.

Incorporating Structured Credit into a Diversified Portfolio

Though a relatively new asset class compared to traditional fixed income assets, structured credit has become an integral part in the financial system, offering potential benefits for borrowers, lenders and investors alike. While the complexity of the structured credit opportunity set can be daunting to some, we believe experienced, research-driven managers are well positioned to generate meaningful incremental yield with manageable incremental risk as well as key diversification benefits.

When it comes to asset allocation, there are multiple ways to position structured credit in a diversified portfolio.

Fixed Income Plus. We believe structured credit may represent a compelling option for portfolios seeking to enhance the return potential of their fixed income bucket without potentially adding significant marginal risk. Not only has structured credit historically offered higher yields than traditional fixed income assets, the credit exposures underlying these securities—which as we noted earlier includes everything from consumer and commercial mortgages to consumer credit and more esoteric corporate cash flows—provide an avenue to diversify the interest rate and corporate risk that dominates traditional fixed income portfolios.

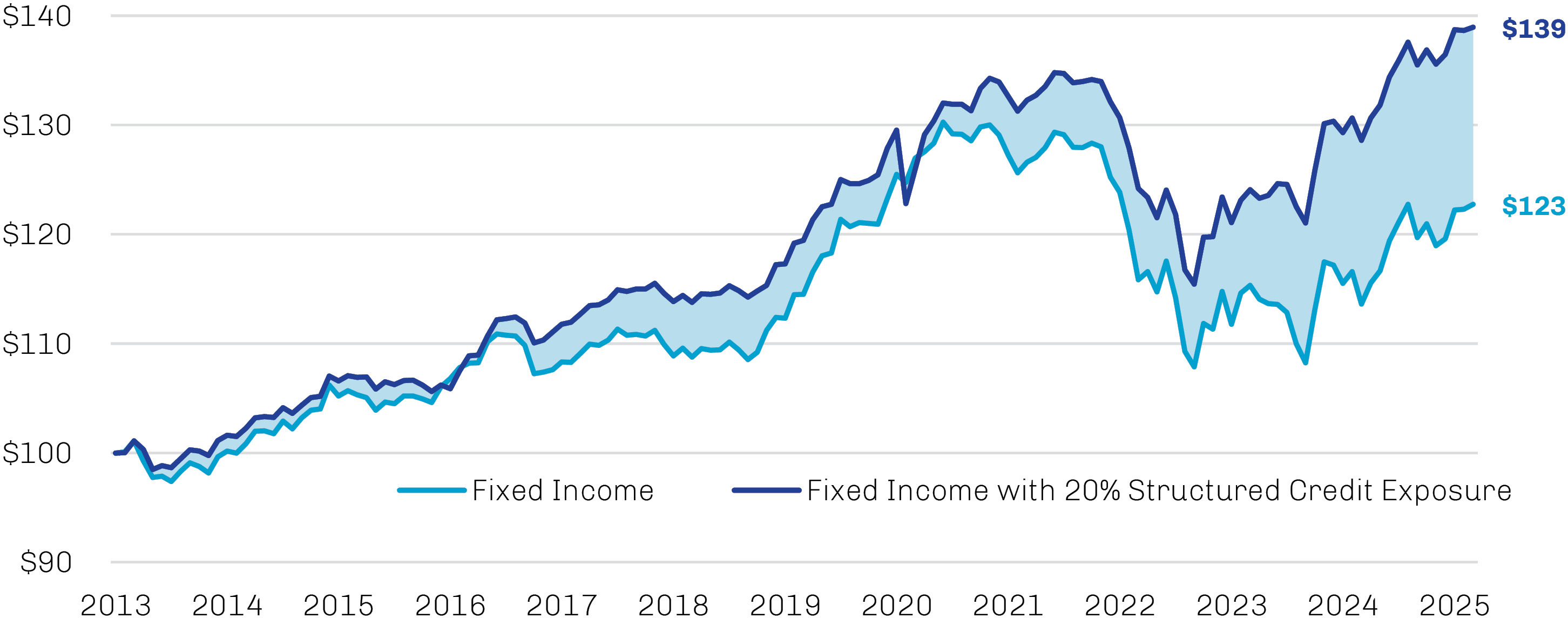

To illustrate how this might work in practice, consider a hypothetical pension fund seeking to enhance the returns of its fixed income bucket by apportioning 20% of its fixed income allocation to investment grade structured credit. The example depicted in Exhibit 7 demonstrates a 70% improvement in cumulative returns over the 10-year-plus period.

Exhibit 7. An Allocation to Structured Credit May Meaningfully Enhance the Performance of a Fixed Income Portfolio

Growth of $100, March 2013 through April 2025

Note: Fixed Income = Bloomberg US Aggregate Bond Index; Structured Credit = JPMorgan Collateralized Loan Obligation BBB Index. Source: Bloomberg, JPMorgan; data as of April 30, 2025 PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS. ACTUAL RESULTS MAY VARY.

Opportunistic Credit. Structured credit can be an attractive complement to traditional sponsor-backed direct lending exposure for certain investors, as appropriate. Access to a diversified range of credit assets with a track record of high returns—both private and public—provides the flexibility to rotate among credit sectors opportunistically in response to changing market conditions, giving portfolios the potential to generate return profiles that may not be available to either direct lending or structured credit alone.

Absolute Return. A portfolio’s absolute return bucket typically seeks to leverage manager skill to generate positive returns over time across different market conditions. As noted earlier, the relative illiquidity of many structured credit markets often provides potential opportunities for skilled managers to capitalize on mispricings and structural inefficiencies among performing credit assets and generate total returns in excess of the yields of the underlying assets through active rotation. Moreover, the design elements of structured credit may help mitigate credit losses during challenging periods and thus promote higher rates of capital appreciation over the long term.