Macro & Market Views

Sovereign Debt: Driving the Dynamite Truck

Sovereign Debt: Driving the Dynamite Truck

Key Takeaways

Fiscal policy has been on an unsustainable trajectory since the global financial crisis, as governments globally responded to two largescale economic dislocations. While financial repression via extraordinary monetary accommodation tempered interest expenses for some time, this trend has reversed.

Debt dynamics in the US are expected to worsen in the coming decades. Expenditures— driven by growth in mandatory spending on entitlement programs like Social Security and Medicare, as well as net interest outlays—are forecast to outpace revenues, resulting in persistent annual deficits and deepening debt.1

Given the current dysfunctional state of the US political system, it’s hard to envision lawmakers coalescing around measures needed to tackle the country’s structural fiscal issues—including tax hikes, entitlement reform and cuts to discretionary spending, as well as supply-side reforms to promote productivity growth.

Despite widespread concerns about rising debt and shaky governance, the term premium on US Treasuries has trended well below average for the past decade and has spent much of the past five-plus years in negative territory. A rerating of Treasury risk could have a significant impact on asset prices.

The twenty-first century alone has provided a number of prominent examples. The massive increase in US corporate borrowing and leverage during the 1980s and 1990s, for example, climaxed with the early-2000s impropriety-driven collapses of once-highflying companies like Enron and WorldCom. The accommodative monetary policy of subsequent years, meanwhile, fueled an increase in household debt—and mortgage debt, in particular—that culminated in the 2007–09 global financial crisis.

We believe sovereign debt is the epicenter of indebtedness today. Fiscal policy has been on an unsustainable trajectory since the global financial crisis, not just in the US but across advanced economies, as governments provided extensive support in response to two large-scale economic dislocations. This federal largesse was supported by very low interest rates that kept interest expenses manageable and by long-lived, large-scale quantitative easing programs that provided ample demand for government debt issuance. While the ongoing rollback of crisis-era monetary accommodations continues to alter the calculus of government borrowing, signs that near-term fiscal policy will be adjusted to reflect the new math are limited.

As we’ve seen throughout history, indebtedness often doesn’t seem to matter until it does—and the change in market sentiment can be swift and explosive. Given the trajectory of the US fiscal position and few indications that meaningful fiscal consolidation is on the horizon, it seems prudent to consider when investors may begin demanding greater premia for what appears to be an increasingly risky exposure. It also seems prudent to consider the impact a meaningful rerating of Treasury risk would have on the institutions that hold these securities and asset prices more broadly.

Road to Nowhere

Citing “expected fiscal deterioration over the next three years, a high and growing general government debt burden, and the erosion of governance,” Fitch Ratings on August 1 cut its long-term credit rating on US sovereign issuance from AAA to AA+. This marked only the second time that US debt was downgraded by a major ratings agency; Standard & Poor’s downgraded the US in 2011 amid similar conditions and has since maintained its AA+ rating.2

Markets appeared to take Fitch’s announcement in stride. Though Treasury yields forged higher across the curve and equity trackers like the S&P 500 Index turned lower over the next few weeks, the magnitude of these moves did not suggest panic, and measures of implied market volatility like the Cboe Volatility Index and ICE BofAML MOVE Index confirmed the lack of anxiety.3 The US dollar broke higher despite the vote of no-confidence from Fitch and ended August at pre-bank failure levels, as shown in Exhibit 1. The dollar also rallied in the weeks leading up to the debt-ceiling standoff, an event that if not averted likely would have had massive global macroeconomic implications; it also was little affected heading into the potential October 1 government shutdown (which at the eleventh hour was pushed back to November 17, likely setting up another political battle just a handful of weeks from now). In short, the dollar, as the global reserve currency, continues to attract buyers during periods of risk aversion—even if the US is the source of that risk. Of course, it’s possible that US monetary hegemony will fade, like UK hegemony before it; for now, however, the country’s role as a perceived “safe haven” appears to be providing a buffer against worst-case outcomes.

Exhibit 1. The Dollar Has Rallied in the Face of Presumed Headwinds

ICE US Dollar Index, January 1, 2023, through September 30, 2023

Source: FactSet; data as of September 30, 2023.

Though markets don’t yet appear ready to punish the US for its profligacy, Fitch’s downgrade underscored concerns we’ve voiced for some time now about both the level of the country’s debt and its likely trajectory given the apparent lack of political will to enact the spectrum of measures necessary—including tax hikes, entitlement reform and cuts to discretionary spending, as well as supply-side reforms to promote productivity growth—to rein it in. Continued dysfunction in a US political system marked by an abhorrence of compromise suggests repeated party-line standoffs may be far more prevalent than concrete progress toward fiscal consolidation.

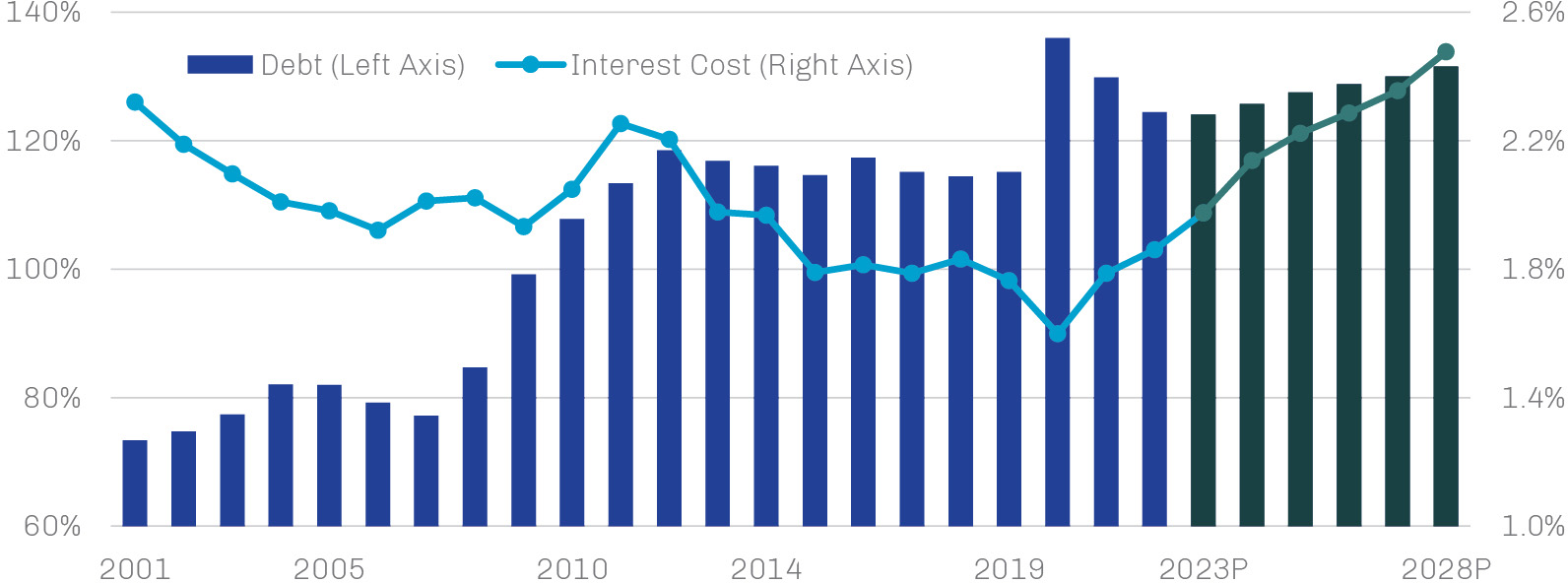

High and rising debt levels, particularly to fund noninvestment spending, are less than ideal for an economy. In theory, high debt drives borrowing and debt-servicing costs higher, weighing on productivity and economic output, crowding out private-sector investment, undermining sovereign creditworthiness and credibility, and potentially limiting policy optionality in the event of future crises. In practice, however, financial repression via unconventional monetary policies through much of this century kept interest rates artificially low and tempered interest expenses even as debt balances continued to rise, blunting any motivation for lawmakers to make the unpopular choices necessary to get their fiscal houses back in order. Exhibit 2 depicts government debt and interest payments for the US, UK, euro zone and Japan as a percentage of GDP; as shown, while debt in aggregate rose from less than 80% of GDP in 2007 to peak above 135% in 2020, the cost of servicing this debt declined steadily from 2011 until 2020. This trend in interest expense has since reversed direction and is forecast to continue its upward climb.

Exhibit 2. Low Rates Kept Interest Costs in Check Even as Debt Levels Rose Sharply

As a Percentage of GDP for the US, UK, Euro Zone and Japan in Aggregate, 2001 through 2028

Note: Data for 2023-28 are projections.

Source: Haver Analytics, International Monetary Fund, First Eagle Investments; data as of July 31, 2023.

Driven by massive issuance in response to the economic dislocations of the Covid-19 pandemic, US government debt held by the public ended 2020 at 100% of GDP, rivaling the previous high-water mark of 106% established in the aftermath of World War II in 1946.4 Debt to GDP fell steadily in the decades that followed the war—ultimately reaching 23% in 1974—as population growth and productivity improvements spurred rapid nominal GDP growth and financial repression kept real interest rates very low or negative. There are few indications that a similar scenario is likely to play out this time around, however. Though public debt outstanding has improved by a few ticks since its 2020 peak as spending related to pandemic relief waned and economic growth resumed, the Congressional Budget Office (CBO) forecasts debt to GDP to eclipse its historical peak by 2029 and get even worse from there.5

A Recipe for Persistent Deficits and Deepening Debt

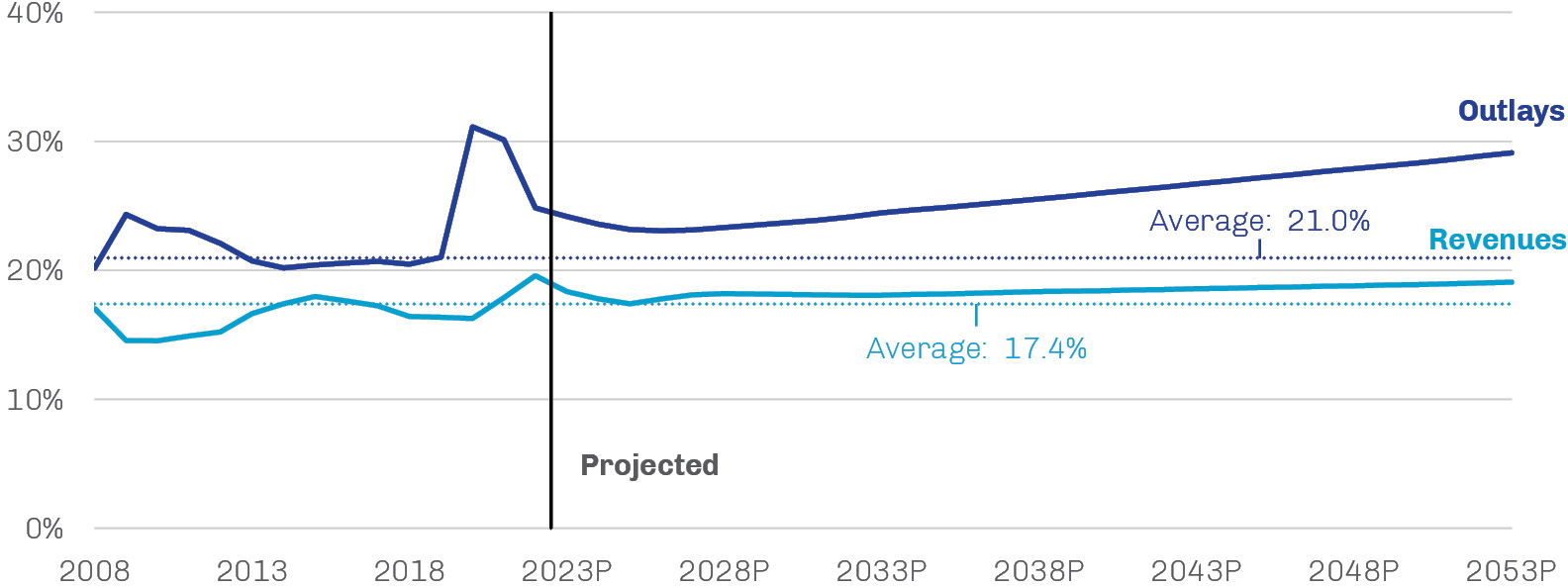

The logic supporting the CBO’s gloomy forecast is straightforward. As shown in Exhibit 3, the CBO expects expenditures to increase faster than revenues, resulting in persistent annual deficits and deepening federal debt.

Exhibit 3. With Outlays Far Outpacing Revenues, US Debt Is Forecast to Increase

As a Percentage of GDP, 2008 through 2053

Note: Average reflects 1973 through 2022. Data for 2023–2053 are projections.

Source: Congressional Budget Office; data as of June 28, 2023.

Future spending increases are expected to be driven by growth in mandatory spending and net outlays for interest on government debt. The CBO, perhaps optimistically, forecasts discretionary outlays will continue to shrink as a share of GDP, to 5.4% by 2037 from 6.6% in 2022; for context, discretionary outlays as a percentage of GDP peaked at a high of 13.1% in 1968 and has averaged 7.1% over the past 20 years.6

Mandatory spending—which is dictated by existing laws and includes major entitlement programs like Medicare and Social Security—is projected to increase over the next few decades due to rising healthcare costs and the aging US population. Also of concern, the CBO now projects that the Old-Age and Survivors Insurance Trust Fund will be exhausted in 2032; if Social Security payments were limited to annual Social Security revenues at this point, benefits would drop 25% starting in 2033.7 Net outlays for interest are projected to increase on the back of higher interest rates and expanding debt; while this cost has averaged 2% of GDP over the last 50 years, the CBO forecasts it to reach 3.6% over the next decade.8

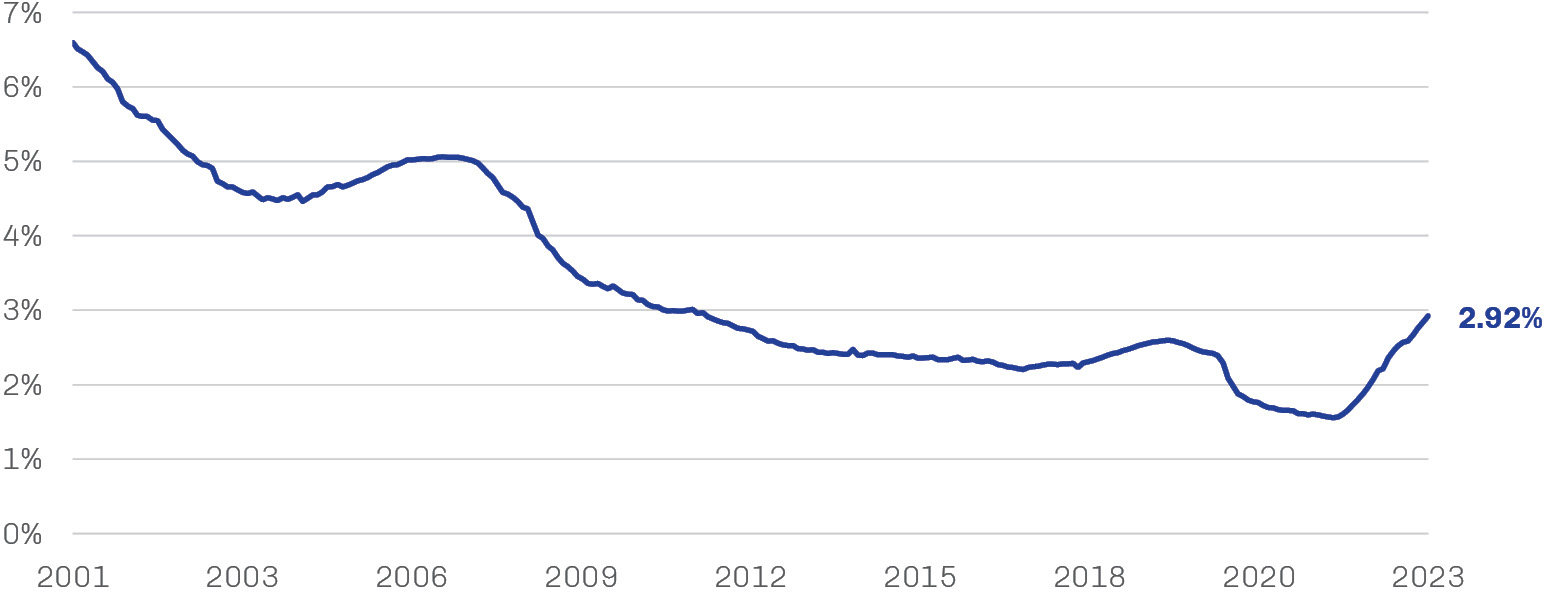

The lag with which the average interest rate on Treasuries outstanding adjusts to prevailing rate levels is a bit of a silver lining. Interest-bearing Treasury debt outstanding amounted to more than $25 trillion as of August 31 and had an average interest rate of 2.92%; while this is higher than the lows of earlier this year, it remains well below historical norms, as shown in Exhibit 4.9 Given the timing and volume of the various maturities that comprise the outstanding debt, the average interest rate paid by the Treasury is expected to increase fairly slowly, to 3.3% in 2033 per the CBO.

Exhibit 4. Though Off Covid-Era Lows, the Average Interest Rate on Treasuries Remains Very Low

Average Interest Rate on All Interest-Bearing Debt of US Treasury, January 2001 through August 2023

Source: US Department of the Treasury; data as of August 31, 2023.

To finance the budgets enacted by Congress, the Treasury has full control over the types of securities it issues and their maturities, and it seeks to “fund the government at the least cost to the taxpayer over time.” There are constraints, however, given the size of annual Treasury issuance and its key role in the functioning of the global financial system. Too large an issuer to behave opportunistically in debt markets, the Treasury prioritizes regular and predictable issuance that supports market liquidity and functioning.10 The Treasury’s responsibility to meet demand for paper across the yield curve likely prevented the Treasury from “terming-out” the maturity of its obligations during the Covid period, in contrast with other developed nations that took advantage of ultra-low rates to lock in long-term funding at cheap rates. In one extreme example, Austria in 2020 issued a 100-year bond at an interest rate of 0.85% with face value of €4.6 billion.11

Revenues, meanwhile, are expected to contract for the next couple of years due to muted capital gains before returning to growth in 2026. The increase in revenues stems from the end-2025 sunset of nearly all the individual income tax cuts and some business tax cuts from 2017’s Tax Cuts and Jobs Act. This may prove hopeful, however; tax cuts tend to be sticky, and the looming expiration of these Trump-era provisions may serve as the next Washington wedge issue when control of the White House and Congress goes up for grabs in November 2024. A number of the hopefuls for the Republican presidential nomination already have expressed their desire to extend the cuts, at a minimum, while President Biden seems likely to renew calls for higher taxes only on top earners. Extending these tax cuts would add another $3 trillion to the deficit over the 2024–33 period, excluding debt-service costs; this represents roughly 1% of GDP annually.12 Given the January 1, 2025, expiration of the country’s debt-limit extension, tax policy also may be a key element of the next contentious debt-ceiling battle.13

Fed Net Income Turns Negative

The end of Fed remittances to the Treasury is a likely drag on revenue in the near term. To fund its operations, the Fed relies on a balance sheet consisting primarily of longer-term assets (Treasuries and agency mortgage- backed securities) and very short-term liabilities (bank reserves and reverse repos). Its net income is the difference between the income generated by the former and the interest expense of the latter (less operating expenses and dividend payments). It is required by law to remit any remaining balance to the Treasury, which uses it to reduce the federal debt.

The Fed has remitted excess income to the Treasury every year since 1935. The size of the transfers grew significantly with the expansion of the Fed’s portfolio following the global financial crisis, totaling more than $1 trillion between 2010 and 2022.14 Since September 2022, however, the aggregate expenses of the Fed system have exceeded income as higher short-term rates have pushed interest expenses above the income generated by the Fed’s low-yielding assets. These shortfalls, which are accounted for on the Fed’s balance sheet as a deferred asset, amounted to $105 billion as of September 2023 and are likely to continue growing.15 Future Fed profits must be used to eliminate the entirety of the deferred asset before remittances to the Treasury can resume.

The Fed is not a profit-maximizing body; any gain or loss by a system bank is not indicative of the quality of its management; rather, it is simply a byproduct of the conduct of monetary policy. While negative net income is likely to persist in the near term, it should ease and ultimately reverse as bonds on the Fed’s balance sheet mature. That said, it’s not hard to imagine income shortfalls being used as a political lever and a potential challenge to Fed independence. While we think the Fed will remain true to its dual mandate above all else, history suggests the risk of competing influences should not be ignored.

The Curious Case of the Disappearing Term Premium

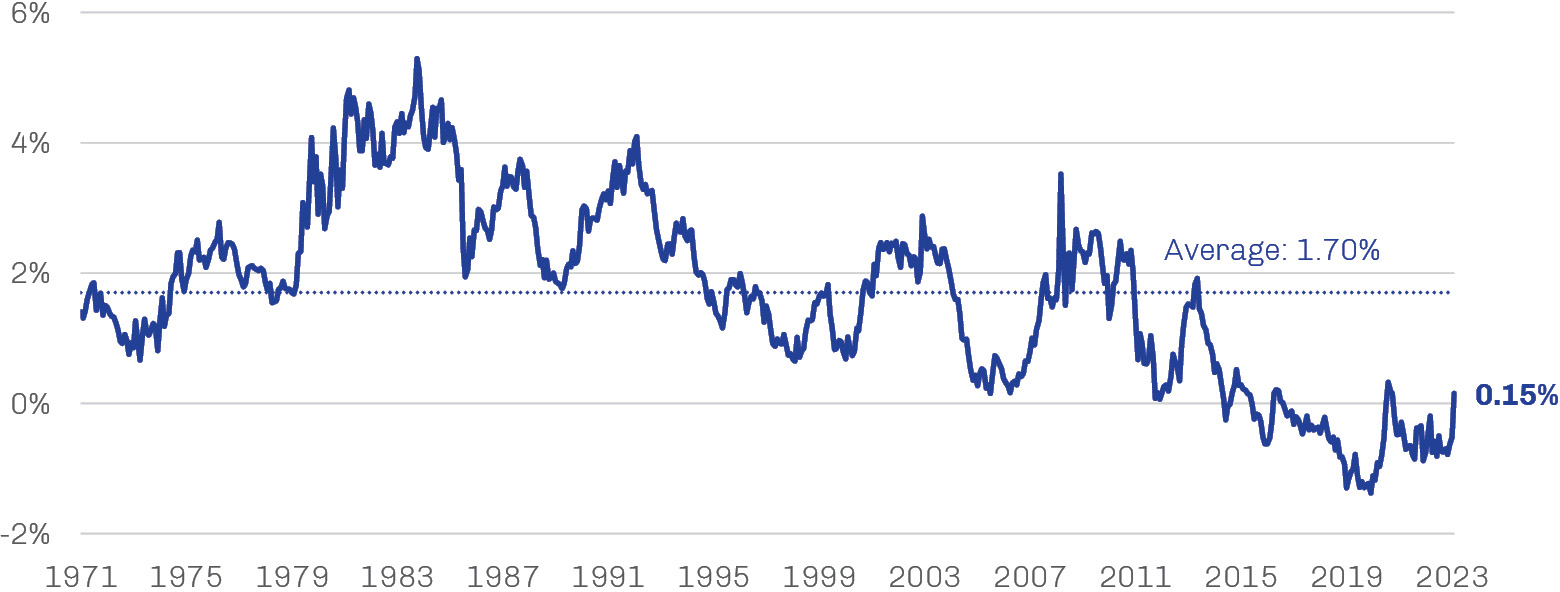

The yield on a Treasury bond can be decomposed into two parts: (1) expectations for real short-term interest rates, and (2) a term premium. The term premium is the additional return that investors require to hold a longer-dated bond as opposed to rolling over a series of short-term notes or bills over the same time frame, and it reflects the risk that the prevailing interest rate will change over the life of the long-dated bond. The term premium is not directly observable and must be estimated via a number of financial and macroeconomic variables.

Typically, the term premium is positive; that is, investors demand additional compensation in exchange for bearing the interest rate risk of a longer-maturity bond. Based on one model employed by the Federal Reserve Bank of New York, the term premium on 10-year Treasuries has averaged 1.7% since the end of the gold standard in August 1971.16,17 As shown in Exhibit 5, however, the term premium has trended lower since the global financial crisis and has spent much of the past five-plus years in negative territory despite widespread concerns about rising debt and shaky governance. Notably, the term premium returned to slightly positive territory in the waning days of September 2023; it remains to be seen if this shift represents a durable move toward more typical levels.

Exhibit 5. Treasury Term Premium Has Been Negative for Most of the Past Five-Plus Years

10-Year Treasury Term Premium, August 1971 through September 2023

Source: Federal Reserve Bank of New York, Federal Reserve Board; data as of September 30, 2023.

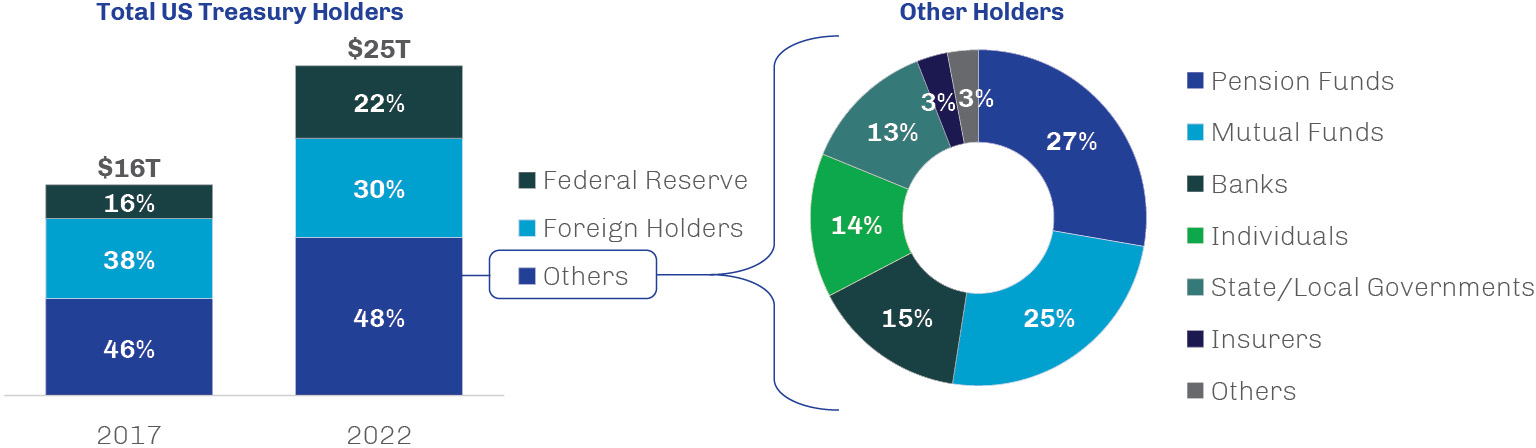

Among the potential reasons for the minimal premia is the presence of price-inelastic Treasury buyers like the Fed, whose quantitative easing programs provided consistent demand and weighed on rates. Central bank balance sheets ballooned as policymakers introduced massive bond-buying programs in response to the economic and market dislocations of the global financial crisis and the Covid-19 pandemic. One result of this buying spree was that the Fed’s ownership of outstanding Treasury debt increased from 16% in 2017 to 22% in 2022, as shown in Exhibit 6. While percentage ownership by foreigners declined over this period, “other” domestic holders—including pension and mutual funds, banks and individuals—increased their share. We think the ongoing migration of central bank policy from quantitative easing to quantitative tightening and the impact it may have on Treasury market supply/demand dynamics is a key variable to watch.18

Exhibit 6. With the Fed No Longer a Net Buyer of Treasuries, Others Will Need to Fill the Gap

Ownership of Outstanding US Treasuries

Source: Federal Reserve, Bloomberg, Securities Industry and Financial Markets Association; data as of July 18, 2023.

With inflation proving more stubborn than expected, the Fed ended its quantitative easing program in March 2022 but continued to maintain the size of its balance sheet for several months by reinvesting the proceeds of maturing securities. In June 2022, it began letting nearly $47.5 billion of such holdings—$30 billion of Treasuries and $17.5 billion of mortgage-backed securities (MBS)—roll off its balance sheet each month without replacement in what is sometimes referred to as “passive” tightening (as opposed to “active” tightening in which a central bank sells bonds from its portfolio in the secondary market). The Fed increased the rate of tightening to $95 billion per month—$60 billion in Treasuries and $35 billion in MBS—in September 2022 and continues at that pace today.19

At the end of September, total assets of the Fed stood at about $8.0 trillion, a reduction of about 11% from the pre-QT peak. Other major central banks—including the European Central Bank, the Bank of England, the Bank of Canada and the Reserve Bank of Australia, among others—have also begun some form of quantitative tightening, and it’s estimated that more than $2 trillion in liquidity will have been squeezed out of the global financial system by the end of 2024.20

Given the unprecedented nature of such large-scale quantitative tightening, its impact on the financial system is uncertain. We do know that the removal of central bank buyers will create a huge gap in sovereign demand that will need to be filled by public market participants. During the pandemic, massive central bank QE programs easily absorbed all net supply of government bond issuance. With the Fed no longer buying new issuance and letting maturing paper roll off, public markets are responsible for absorbing new deficit spending along with the refinancing of maturing paper. It remains to be seen what effect such a change to supply/demand dynamics will have on interest rates and term premia.

The Fed’s only previous attempt at quantitative tightening occurred from October 2017 to September 2019, as it sought to unwind some of the assets accumulated from three rounds of quantitative easing following the global financial crisis. The Fed let about $650 billion in Treasuries and MBS roll off its balance sheet; while this represented a reduction of more than 15% from peak levels, the Fed’s balance sheet—at around $3.8 trillion—remained more than four times as large as pre-crisis levels. Declining reserves combined with heavy Treasury issuance ultimately caused pronounced strains in the market for repurchase agreements (aka repos, or short-term interbank loans), forcing the Fed to inject liquidity directly into the market and to resume its Treasury purchases. Notably, the term premium moved lower during this period of quantitative tightening.21

Risky Business

To us, the swell of public debt outstanding in the advanced economies combined with a general dearth of fiscal discipline has made sovereign paper an increasingly risky proposition. The regime change in interest rates and shrinking global liquidity has exacerbated our concerns about sovereign credibility and highlights the pronounced vulnerabilities in today’s financial system and perhaps the potential for some sort of financial accident.

The lack of persistently positive term premia suggests markets may not agree with us—or, at the very least, they have grown complacent amid the many potential triggers for a re-rating of US Treasuries. While we can’t speculate about what may finally cause investors to demand compensation for the uncertain long-term fiscal trajectory of issuers like the US, changes in sentiment can happen quickly and reverberate broadly.

Source: The 2023 Long-Term Budget Outlook,” Congressional Budget Office (June 2023).

Source: Standard & Poor’s; data as of August 31, 2023.

Source: FactSet; data as of September 25, 2023.

Source: US Department of the Treasury, Bureau of Economic Analysis; data as of August 31, 2023. Note that “debt held by the public”

excludes intragovernmental debt“The 2023 Long-Term Budget Outlook,” Congressional Budget Office (June 2023).

“The 2023 Long-Term Budget Outlook,” Congressional Budget Office (June 2023).

“CBO’s 2023 Long-Term Projections for Social Security,” Congressional Budget Office (June 2023).

“The 2023 Long-Term Budget Outlook,” Congressional Budget Office (June 2023).

Source: US Department of the Treasury; data as of August 30, 2023.

Source: US Department of the Treasury; data as of July 17, 2023.

Source: Bloomberg; data as of July 10, 2023.

"Budgetary Outcomes Under Alternative Assumptions About Spending and Revenues,” Congressional Budget Office (May 2023).

Source: Urban-Brookings Tax Policy Center; data as of June 7, 2023.

Source: Congressional Research Service; data as of January 23, 2023.

Source: Federal Reserve; data as of September 30, 2023.

Tobias Adrian, Richard K. Crump and Emanuel Moench, “Pricing the Term Structure with Linear Regressions,” Journal of Financial Economics 110, no. 1 (October 2013).

Source: Federal Reserve Bank of New York; data as of September 30, 2023.

Source: Federal Reserve, Bloomberg, Securities Industry and Financial Markets Association; data as of July 18, 2023.

Source: Federal Reserve; data as of September 21, 2022.

Source: Fitch Ratings; data as of February 22, 2023.

Amalia Estenssoro and Kevin L. Kliesen, “The Mechanics of Fed Balance Sheet Normalization,” Economic Synopses, no. 18 (August 2023).