Macro & Market Views

Seeking Prime Opportunities in the Primary Market

Seeking Prime Opportunities in the Primary Market

After struggling with both supply and demand challenges amid Federal Reserve rate hikes in 2022–23, the municipal bond market came storming back in 2024.

- More stable interest rates promoted record muni bond new issuance in 2024, and 2025 is anticipated to be on pace to be even stronger.

- Investment managers and other institutional investors dominate the muni bond primary market, as it represents an effective and efficient way to build scale in and enhance the diversification of large portfolios.

- Active investors with strong underwriter relationships may be able to influence the terms of certain primary offerings and ultimately secure favorable allocations. They also may be able to access limited public offerings or private placement deals made available to only a handful of investors—or sometimes only to a single investor.

- Unrated muni bonds—whether newly issued or trading in the secondary market—offer Investment managers opportunities to identify potential value through skilled credit analysis.

Two years of heavy investor outflows from municipal bond mutual funds and exchange-traded funds (ETFs) turned to inflows last year as policy rates peaked and began to ease. Issuance, meanwhile, established a new annual high in 2024 as issuers sought financing in what had become a more stable interest rate environment.

While muni bond market technicals grew more complicated in 2025 alongside the barrage of policy changes early in the second Trump administration—the early April announcement of a new tariff regime, in particular—the impact on demand proved fleeting. We believe inflows are likely to continue recovering from the dislocations of 2022-23, fueled by high absolute and tax-equivalent yields. Muni bond supply, in contrast, hasn’t missed a beat this year, and new issuance is anticipated to be on pace for another annual record as municipalities seek to fund increasingly expensive projects amid the waning glow of Covid-era federal stimulus and post-Covid tax windfalls.

A healthy new-issue market provides investors—particularly the portfolio managers and other institutional investors that buy the vast majority of primary market issuance—opportunities to enhance diversification and build scale within their portfolios. And as it often does in the secondary market, rigorous credit analysis may uncover new municipal securities whose risk/reward profiles are particularly compelling, in our view.

Market Technicals Rebalance after Brief Disruption

After a strong 2024, municipal bond mutual funds and ETFs continued to attract assets at a robust pace in early 2025, fueled by high absolute and tax-equivalent yields. While the broad-based market volatility that followed the Liberation Day tariff announcements in early April weighed on flows, the impact proved relatively short-lived. After seven consecutive weeks of outflows from mid-March through the end of April, coincident with seasonal weakness approaching Tax Day, inflows soon resumed and stand at $9.4 billion year to date.1

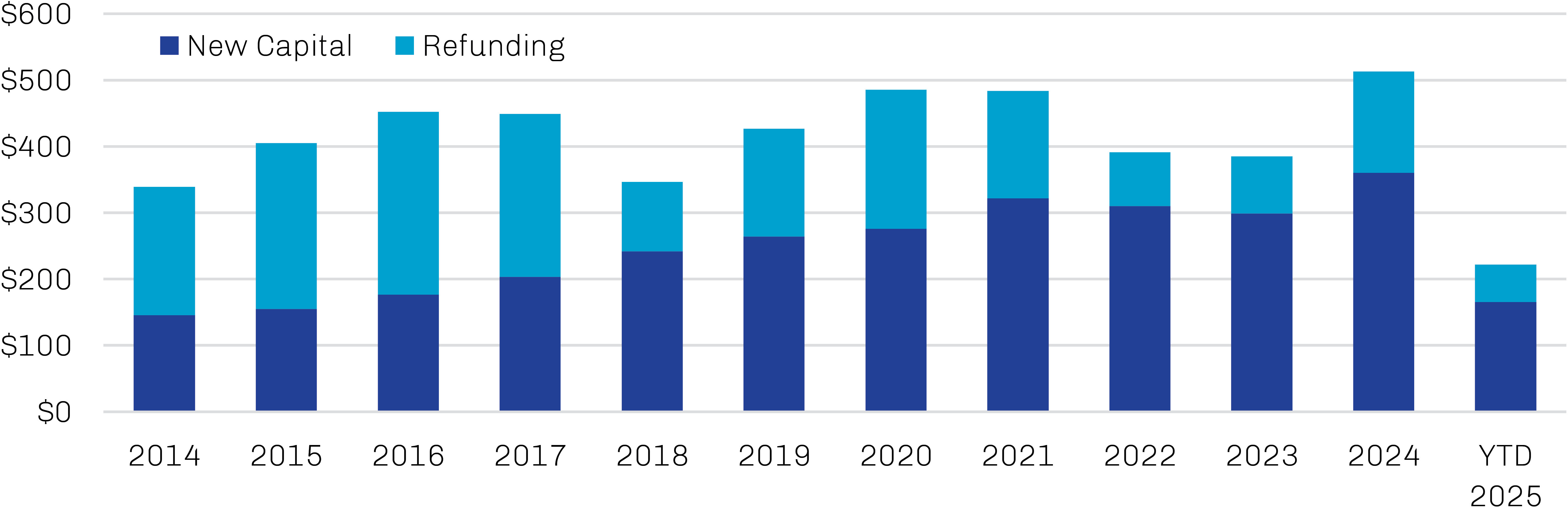

Bond supply, in contrast, was largely unaffected by shifting trade policy and renewed interest rate volatility. In fact, muni bond issuance accelerated in April and May, and the year-to-date total of $222 billion puts 2025 on pace to beat 2024’s record $533 billion.2 Some of this activity may have been pulled forward on the calendar as a result of issuer concerns about the continued tax treatment of municipal bonds. There had been chatter in DC circles about potential modifications to muni bonds’ tax exemption to generate additional federal revenue; while the House of Representative’s version of the budget reconciliation bill left muni bonds unscathed, changes remain possible, if highly unlikely, until a final bill is signed into law.

Exhibit 1. Muni Issuance Has Rebounded from the Fed’s Rate-Hike Cycle

Annual Municipal Bond Issuance in Billions, 2014 through May 2025

Source: SIFMA Research; data as of June 12, 2025.

Despite the macroeconomic and legislative noise, municipalities generally remain in strong fiscal condition. States, for example, took advantage of outsized federal funding as a result of two large Covid-related bills in 2020 and 2021 to bolster their reserves and rainy-day funds, and strong tax receipts in the years that followed have supported balance sheets even as federal transfers returned to more normal levels. Defaults remain very low, even by the standards of an asset class accustomed to very low default activity.3

Multiple Avenues to the Market

Rather than dipping into current cash flows or reserves, a municipality looking to fund a large capital project— the construction of a new bridge, say, or the renovation of a public school—may turn to the capital markets for cost-effective, large-scale financing that can be repaid over an extended period.

Lacking the broad spectrum of in-house expertise necessary to successfully launch and market a bond offering, most prospective municipal issuers instead engage a group of external specialists to assist in the process. Hiring a municipal advisor is usually among the first items on the to-do list. Registered with both the Securities and Exchange Commission and the Municipal Securities Rulemaking Board, municipal advisors have a fiduciary duty to help their clients obtain the necessary funding at the lowest possible borrowing cost. As such, these professionals guide municipalities through the bond-offering process, providing advice around structuring, pricing and ultimately the most effective way to go to market.

There are two pathways by which municipalities can approach the primary market: competitive bids and negotiated sales. The best approach for a particular offering depends on a host of factors, including deal size and complexity, the issuer’s sector and credit quality, and prevailing market conditions. Notably, the method chosen will determine how and when the issuer engages an underwriter for its deal (that is, the investment bank or syndicate of banks that will buy the new bond issue in its entirety and re-sell it to investors).

The competitive bid process is unique to municipal bonds. In it, the issuer and its advisors first establish nearly all the parameters of a bond offering—its size, maturity schedule, call features, credit rating, etc.—and then solicit bids from underwriters through a public notice of sale. The underwriters’ bids include the interest rate to be paid on the bonds and the underwriter’s discount, which together represent the true interest cost (TIC) to the issuer. The underwriter whose bid represents the lowest TIC is awarded the business and immediately goes about trying to sell the bonds it now owns.

Competitive bid sales are generally best suited for higher-grade issuers that have demonstrable track records in the muni bond market and plan to issue relatively plain-vanilla bonds; that is to say, bonds underwriters expect to be able to re-sell to investors without difficulty and without structural adjustments.

The negotiated sale process for a new municipal bond offering is similar to the process employed in most other securities offerings. The issuer chooses an underwriter—through a formal request for proposals process or an existing relationship—it believes will be able to execute its bond issuance at the lowest borrowing cost. While final decisions on the bond’s structure and pricing ultimately fall to the issuer, the underwriter can influence the terms of the deal until the bond purchase agreement is signed; it will premarket the offering to its network of institutional investors to gauge interest/generate demand and use this information to shape a bond offering it believes will be easily salable.

Negotiated sales generally are best suited for lower investment grade or high yield issuers. Structurally complex bonds or those that represent refunding transactions also may benefit from a negotiated sales process. Given the higher level of engagement between underwriter and issuer and more accommodative timeline, a negotiated sale also lends itself to limited public offerings in which a new issue is marketed and resold to only a small group of institutional investors.

While the ratio of competitive to negotiated offerings has tended to be fairly even by deal count—48% of the muni primary market offerings in 2019–23 were competitive, while 52% were negotiated—negotiated deals have been far more popular in terms of par amount issued—73% to 27% over the same five-year period. As could be surmised, the average size of negotiated issues ($50 million) has tended to be far larger than competitive sales ($20 million).4

A smaller subset of municipalities may find a private placement to be their most cost-effective financing option, especially if the public market appears unreceptive to a bond issuance. In a private placement, a municipality— typically with the assistance of a placement agent—negotiates loan terms directly with a single institutional investor or a small group of them, with no underwriter involved. Given the additional complexity and limited secondary-market liquidity, private placements typically entail more rigorous structural provisions and higher yields than competitive or negotiated public deals.

Institutional Investors Dominate Primary Market

Though new-issue muni bond volume pales in comparison to secondary market trading activity, the primary market has long been an attractive way for portfolio managers to put inflows to work. Indeed, investment managers and other institutions historically have been the main participants in the primary municipal bond market; from 2018 to 2022, for example, 99% of the par amount of primary issuance was purchased by buyers characterized as institutional or primarily institutional.5

Primary offerings can be an effective and efficient way for portfolio managers to build scale and enhance diversification, potentially providing access to large blocks of new bonds at prices we believe are superior to similar secondary market bonds. Active investors with strong underwriter relationships may be able to influence the terms of negotiated offerings in the premarketing stage and ultimately secure favorable allocations upon issuance. Close underwriter relationships may also provide access to limited public offerings that are made available to only a handful of investors—or sometimes only to a single investor.

Such offerings—which are more typical in the high yield space, where issues tend to be smaller in size—can be beneficial to both the issuer and investor, providing the former with access to capital at a fair price and the latter an asset with a differentiated risk/return profile. To meet the true interest cost limitations of the issuer, the investor may negotiate some sort of contractual inducement to help mitigate risk, such as tailored call features or amortization structure, additional covenants, or a subordinate loan to the issuer from a third party.

Unrated Bonds May Offer Particular Value

With more than $4.2 trillion distributed across more than one million distinct municipal bonds and 50,000 issuers, the municipal bond market is large but highly fragmented.6 Historically, this has resulted in significant dispersion of yields and prices for similar bonds—and an opening to identify potential value through skilled credit analysis.

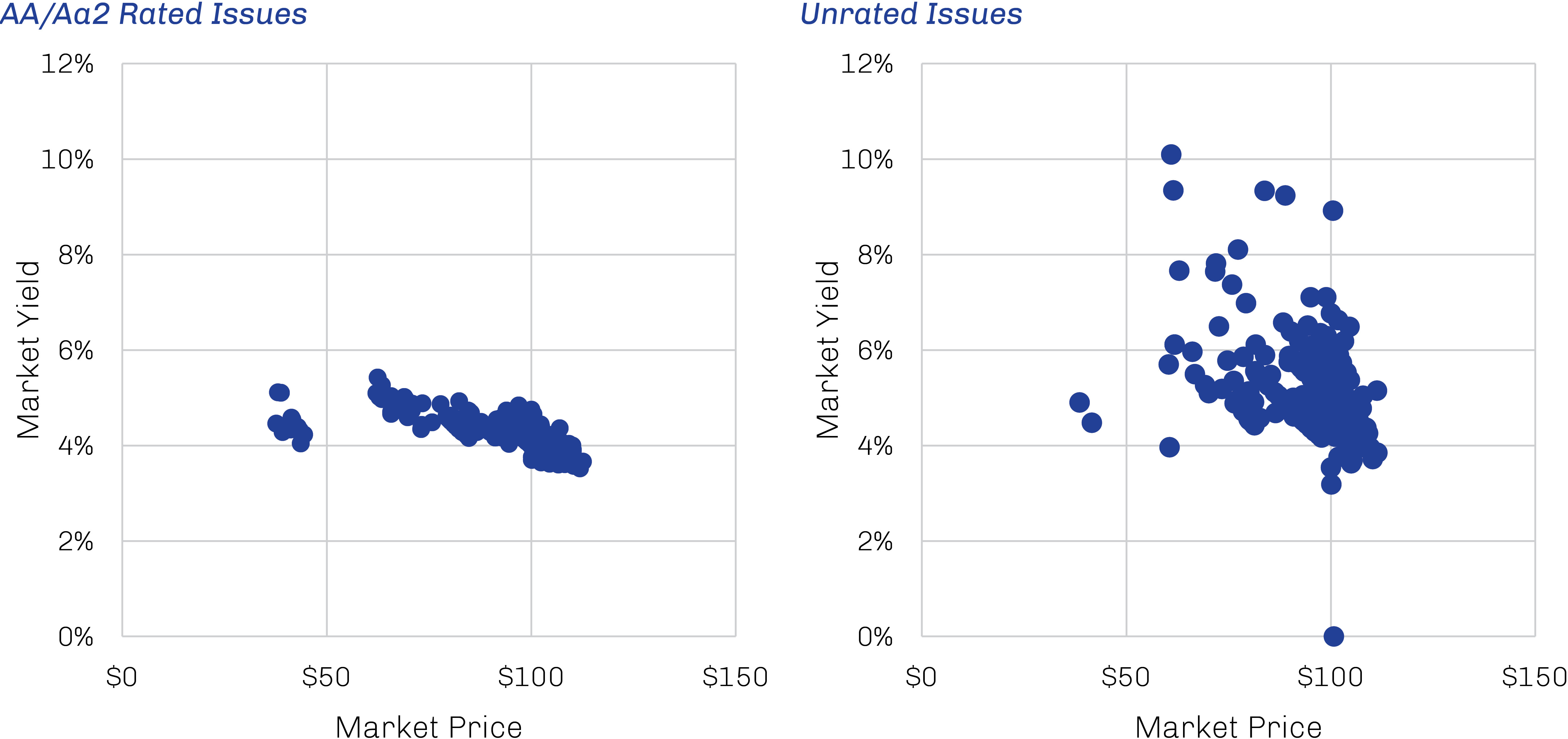

As shown in Exhibit 2, dispersion has tended to be higher among unrated bonds, providing skilled credit managers ample opportunity to identify potential mispricings and enhance portfolio performance. This is no small cohort; a recent study found that 34% of the 200,000 municipal bonds issued from 1998 to 2017—or 14% of the $3.7 trillion in par value—did not obtain a credit rating from a nationally recognized statistical rating organization (NRSRO).7 On the secondary market, unrated bonds, which by default are considered noninvestment grade, currently comprise approximately two-thirds of the S&P Municipal Bond High Yield Index based on number of constituents.8

Exhibit 2. Significant Price and Yield Dispersion Exists Among Individual Credits

Comparison of Bonds in the S&P Municipal Yield Index with 2044 Maturities

Source: Bloomberg; data as of January 31, 2025.

While unrated bonds have not been subject to the proprietary scrutiny of the likes of Moody’s or S&P Global Ratings, we don’t believe their lack of rating should be interpreted as a reflection of the borrower’s capacity to meet its financial commitments. There are a number of reasons a muni issue may go unrated at the time of issuance, the most straightforward of which is the cost; small offerings—which are not unusual in the muni space—may not find the expense of a rating worthwhile relative to the proceeds raised. To compensate for their greater complexity and information risk, however, unrated bonds typically pay investors a higher yield compared to rated issuers of similar quality, and we believe skilled credit managers may find favorable risk/return profiles within this opportunity set. The credit work, in our view, may be especially rewarding given the low historical default rate of high yield municipal bonds in general—speculative-grade municipal bonds had an average trailing- 12-month default rate of 1.2% for the period 1970 to 2023 compared to 4% for similarly rated corporates.9

Making Credit, Work, Work

Despite some hiccups in the spring, the municipal bond market appears to have gotten back on track. Mutual fund and ETF flows are again positive, and issuance is anticipated to be on track for another new record. We believe these positive technical dynamics are likely to persist as the municipal bond market continues to recover from the disruptions of the Fed rate-hike cycle of 2022–23, providing experienced, research-driven credit managers with a range of potential opportunities.

Whether in the primary or secondary market, First Eagle’s Municipal Credit team looks for securities we believe are undervalued relative to the general market. Through rigorous underwriting, we seek bonds we believe have the potential for attractive returns from a combination of price improvement and yield, characterized by solid debt service coverage, and a priority lien on hard assets, dedicated revenue streams or tax resources. Often, this includes what we consider hidden gems that are well managed and well positioned in their markets while offering compelling yields and dollar prices that we believe adequately compensate for the risks.