Commentaries

Overseas Fund Commentary

Overseas Fund Commentary

Portfolio Review

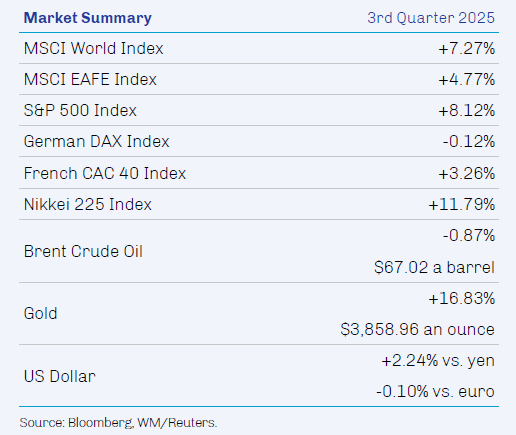

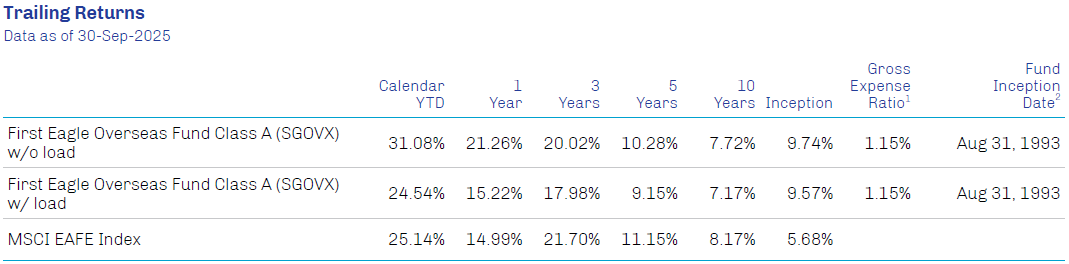

Overseas Fund A Shares (without sales charge*) posted a return of 9.20% in third quarter 2025. All regions contributed to performance; emerging markets and North America were the leading contributors while Japan and developed Asia excluding Japan lagged. Materials and consumer discretionary were the largest contributors by equity sector while communication services was flattish and healthcare also lagged. The Overseas Fund outperformed the MSCI EAFE Index in the period.

Leading contributors in the First Eagle Overseas Fund this quarter included gold bullion, Alibaba Group Holding Ltd., Prosus N.V. Class N, Imperial Oil Limited and Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR.

The gold price continued to set new record nominal highs during the quarter, propelled by a rare convergence of monetary policy uncertainty, attacks on Federal Reserve independence, disruptive trade policy, shifting fiscal policies, heightened local and geopolitical tensions, and high sovereign debt levels.

Shares of tech giant Alibaba were strong during the quarter. With large infrastructure/data centers and leading open-source models, the company’s cloud business has accelerated to capitalize on the AI boom in China. Its partnership with Nvidia, announced in September, further underscores Alibaba’s commitment to its AI and cloud operations. At the same time, the company’s core e-commerce business continues to grow, with improved operating efficiencies that enable it to return cash to shareholders through dividends and stock repurchases.

Prosus is a global technology company domiciled in Holland with a portfolio of private equity investments and an approximate 25% ownership stake in China’s publicly traded technology company Tencent, which is Prosus’s largest holding. Tencent delivered strong topline growth and margin expansion during the quarter and investors seemed to applaud Prosus’s shift away from smaller, riskier acquisitions toward more established businesses at reasonable multiples. Driven by positive cash flow from operations, Prosus continues to buy back shares.

Imperial Oil is a Canadian integrated oil company that is 70% owned by Exxon Mobil. The company reported strong upstream production during the quarter and continued to restructure and consolidate its asset base, reducing the need for future reinvestment. Announced staff reductions and the sale and leaseback of the company’s headquarters should enhance profitability. Imperial’s strong record of returning cash to shareholders through both buybacks and dividends continues unabated.

Taiwan Semiconductor (TSMC) is the world’s largest semiconductor foundry, a primary manufacturer of advanced chips used in generative artificial intelligence for clients including Nvidia, Broadcom, Intel, Advanced Micro Devices and Apple. As the main foundry for Nvidia, TSMC shares were strong during the quarter on continued strong demand for AI processors.

The leading detractors in the quarter were Shimano Inc., SMC Corporation, FUCHS SE Pref Registered Shs, Haleon PLC and Ambev SA Sponsored ADR.

Japan’s Shimano, which manufacturers bicycle parts, fishing components and rowing equipment, lowered its forward guidance during the quarter because of weakness in overseas markets and ongoing inventory adjustments. Our investment thesis remains intact, as we are confident that Shimano can work through accumulated inventories after the strong but unsustainable demand for its products during the Covid-19 era. In addition to high-quality products and dominant global market share, the company has a strong history of returning capital to investors.

SMC is a Tokyo-domiciled industrial automation company providing pneumatic control systems to factory floors around the world. The company reported disappointing results for its most recent quarter. SMC has begun to see a recovery in demand for electrical machinery and electric vehicle-related industry in the greater China region, but semiconductor demand in Japan, North America and Korea is still tepid. We continue to like its dominant market position, and the company has been gaining market share despite the weakness in its end markets.

Germany based-FUCHS is a global manufacturer and distributor of high-value-add industrial lubricants for a range of applications. The company reported weaker-than-expected results for its most recent quarter due to the impact of tariffs, low industrial output in Europe and geopolitical tensions. We believe these challenges are cyclical in nature, and we continue to like the company’s ability to generate cash flow and grow its business. With concentrated family ownership and a limited free float that restricts buybacks, management has consistently returned capital to shareholders through dividends.

Consumer health company Haleon was spun off from pharmaceutical giant GSK in 2022 and owns a diverse portfolio of brands that include Tums, Advil, Sensodyne and Centrum. The company reported disappointing sales for its most recent quarter and reduced its forward revenue guidance due to softening consumer and retail demand in North America. We like Haleon’s portfolio of brands and its focus on improving productivity and returning cash to shareholders through dividends and share repurchases.

Brazilian brewer Ambev, a subsidiary of Anheuser-Busch InBev, is the largest brewer in Latin America. The company reported weaker-than-expected sales for its most recent quarter due to lower consumption caused by unfavorable weather; this, however, was mitigated by Ambev’s focus on reducing expenses. We appreciate Ambev’s dominant position in markets with favorable demographics and solid operations that are able to deliver strong cash flows to support a strong balance sheet.

We appreciate your confidence and thank you for your support.

Sincerely,

First Eagle Investments

* Performance for Class A shares without the effect of sales charges and assumes all distributions have been reinvested, and if a sales charge was included values would be lower.

1. Source: FactSet; data as of September 30, 2025.

2. Source: Bloomberg; data as of September 30, 2025.

3. Source: CME FedWatch; data as of October 10, 2025.

4. Source: Reuters; data as of March 21, 2025.

5. Source: NATO; data as of June 27, 2025.

6. Source: Bloomberg; data as of April 16, 2025.

7. Source: Bloomberg; data as of October 4, 2025.

8. Source: YCharts; data as of September 30, 2025.

9. Source: FactSet; data as of October 10, 2025.

10. Source: Bloomberg; data as of September 30, 2025.

11. Source: Bloomberg; data as of September 30, 2025.

12. Source: Bloomberg; data as of October 9, 2025.

The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short term performance. Current performance may be lower or higher than figures shown. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than their original cost. Past performance data through the most recent month end is available at www.firsteagle.com or by calling 800.334.2143. The average annual returns are historical and reflect changes in share price, reinvested dividends and are net of expenses. “With sales charge” performance for Class A Shares gives effect to the deduction of the maximum sales charge of 3.75% for periods prior to March 1, 2000, and of 5.00% thereafter. The average annual returns for Class C Shares reflect a CDSC (contingent deferred sales charge) of 1.00% in the year-to-date and first year only. Class I Shares require $1MM minimum investment and are offered without sales charge. Class R6 Shares are offered without sales charge. Operating expenses reflect the Fund’s total annual operating expenses for the share class as of the Fund’s most current prospectus, including management fees and other expenses.

1. The annual expense ratio is based on expenses incurred by the fund, as stated in the most recent prospectus.

2. The Fund commenced operation August 31, 1993. Performance for periods prior to January 1, 2000 occurred while a prior portfolio manager of the Fund was affiliated with another firm. Inception date shown is when this prior portfolio manager assumed responsibilities.

Investments are not FDIC insured or bank guaranteed and may lose value.

Risk Disclosures

All investments involve the risk of loss of principal.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

There are risks associated with investing in securities of foreign countries, such as erratic market conditions, economic and political instability and fluctuations in currency exchange rates. These risks may be more pronounced with respect to investments in emerging markets. Investment in gold and gold-related investments present certain risks, and returns on gold related investments have traditionally been more volatile than investments in broader equity or debt markets. A principal risk of investing in value stocks is that the price of the security may not approach its anticipated value or may decline in value. “Value” investments, as a category, or entire industries or sectors associated with such investments, may lose favor with investors as compared to those that are more “growth” oriented.

Definitions

Federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis.

Gross domestic product (GDP) measures the total value of all economic output in goods and services for an economy.

Currency debasement refers to a reduction in a currency’s purchasing power.

MSCI World Index (Net) measures the performance of large and midcap equities across developed markets countries. A net-return index tracks price changes and reinvestment of distribution income net of withholding taxes.

MSCI EAFE Index (Net) measures the performance of large and midcap equities across developed markets countries around the world excluding the US and Canada. A net-return index tracks price changes and reinvestment of distribution income net of withholding taxes.

US Dollar Index is a geometrically averaged calculation of six currencies weighted against the US dollar maintained by ICE Futures US.

S&P 500 Index (Gross/Total) measures the performance of 500 of the top companies in the leading industries of the US economy and is widely recognized as a proxy for the US market as a whole. A total-return index tracks price changes and reinvestment of distribution income.

Nikkei 225 is a price-weighted index composed of 225 stocks in the Prime Market of the Tokyo Stock Exchange. It is widely recognized as a proxy for the Japanese equity market as a whole.

German DAX® Index measures the performance of the 40 largest companies listed on the Frankfurt Stock Exchange that fulfil certain minimum quality and profitability requirements. It is widely recognized as a proxy for the German equity market as a whole.

CAC 40® Index is a free-float market capitalization-weighted index that measures the performance of the 40 largest and most actively traded shares listed on Euronext Paris.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The holdings mentioned herein represent the following total assets of the First Eagle Overseas Fund as of 30-Sep-2025: gold bullion 8.96%; Alibaba Group Holding Ltd. 1.93%; Prosus N.V. Class N 2.82%; Imperial Oil Limited 3.45%; Taiwan Semiconductor Manufacturing Co., Ltd. Sponsored ADR 2.36%; Shimano Inc. 1.21%; SMC Corporation 1.26%; FUCHS SE Pref Registered Shs 0.65%; Haleon PLC 0.98%; Ambev SA Sponsored ADR 1.11%.

Additional Disclosures

This commentary represents the opinion of the Global Value team as of the date noted. The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation to buy, hold or sell or the solicitation or an offer to buy or sell any fund or security.

The Fund’s portfolio is actively managed and holdings can change at any time. Current and future portfolio holdings are subject to risk.

The Fund may invest in gold and precious metals through investment in a wholly-owned subsidiary of the Fund organized under the laws of the Cayman Islands (the “Subsidiary”). Gold Bullion and commodities include the Fund’s investment in the Subsidiary.

The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof.

Third-party marks are the property of their respective owners.

FEF Distributors, LLC (“FEFD”) (SIPC), a limited purpose broker-dealer, distributes certain First Eagle products. FEFD does not provide services to any investor but rather provides services to its First Eagle affiliates. As such, when FEFD presents a fund, strategy or other product to a prospective investor, FEFD and its representatives do not determine whether an investment in the fund, strategy or other product is in the best interests of, or is otherwise beneficial or suitable for, the investor. No statement by FEFD should be construed as a recommendation. Investors should exercise their own judgment and/or consult with a financial professional to determine whether it is advisable for the investor to invest in any First Eagle fund, strategy or product.

Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about our funds and may be viewed at www.firsteagle.com. You may also request printed copies by calling us at 800-747-2008. Please read our prospectus carefully before investing.

First Eagle Funds are offered by FEF Distributors, LLC, a subsidiary of First Eagle Investment Management, LLC, which provides advisory services.