Macro & Market Views

Non-US Equities: An Exception to American Exceptionalism?

Non-US Equities: An Exception to American Exceptionalism?

Following a long period of US leadership, there are signs that non-US equity markets—and the broad appeal of global diversification—may be mounting a comeback.

Key Takeaways

The outperformance of US equities over non-US stocks in the years following the global financial crisis has been attributed to the notion of American “exceptionalism” amid the ongoing struggles of other developed economies.

A look back over multiple market cycles reveals that the relative performance of US and non-US stocks over time has been far more balanced than the past 15 years would suggest, driven partially by the relative strength of the US dollar.

Despite their year-to-date outperformance, valuations of non-US stocks remain at multidecade lows relative to US names, and secular trends may continue to provide durable support.

We remain concerned about the many risks investors face in the current environment and believe that selectivity remains critical amid heightened uncertainty.

The domination of US equity markets for the past 15 years or so has led some investors to conclude that continued US outperformance was the inevitable result of the country’s “exceptionalism”—i.e., its unique blend of institutional advantages, superior corporate governance and rule of law, and culture of entrepreneurship. A review of the relative performance of US and non-US stocks over time, however, suggests to us that the dynamics on display since the global financial crisis may simply be part of the natural ebb and flow of markets around the long-term mean. Further, it reveals that shifting currency exchange rates historically have had a profound impact, with US stocks outperforming when the US dollar is strong and international stocks outperforming when the US dollar is weak.

In fact, the year-to-date surge in international stocks has come alongside a weakening greenback. In our view, however, the dollar remains exceptionally strong in real terms, and the potential for additional weakness combined with stretched US equity market valuations and a multidecade-wide spread in relative performance strengthens the case for global diversification. Secular forces—such as the prospect of increased fiscal spending in China and Europe or corporate governance reforms in Asia—may also provide durable support for equities in certain geographies, even as the tailwinds of up cycles fade. In today’s uncertain environment, however, we caution that selectively remains critical.

Is the Thrill Gone?

As measured by the S&P 500 Index and the MSCI EAFE Index, respectively, US equities outperformed international stocks by more than 800% from the March 2009 global financial crisis trough through the end of January 2025, a string of dominance that had many investors questioning the continued value of global diversification.1 The rising skepticism toward this core tenet of portfolio construction was fueled in part by the notion of American exceptionalism—the idea that US companies have outperformed and would continue to do so because of a powerful and durable confluence of structural advantages that include a robust legal system, a culture of entrepreneurship and innovation, superior corporate governance, and a comparatively favorable regulatory and tax environment. The comparatively swift rebound of the US economy from the global financial crisis in the early 2010s was seen as evidence of the country’s special status, for example, as was the rise of very large US-domiciled technology companies later that decade.

However, this year has ushered in not only a change in US political leadership but also one in global equity market dynamics. Trump’s November 2024 presidential victory was initially greeted warmly by markets hopeful that campaign trail promises of pro-growth deregulation and tax policy would bolster earnings for a range of US companies amid steady economic growth and cooling inflation. This optimism soon began to fade, however, as it became clear the new administration’s policy timeline prioritized tariffs and program cuts over more supportive measures, and it wasn’t long before US stock markets—the high-flying megacap tech names, in particular—had given back all of their post-election day gains and then some. Trump’s spasmodic approach to trade policy—highlighted by early April’s Liberation Day tariff announcement and the vacillations that followed—has been particularly challenging for markets in search of direction, spawning considerable volatility and massive price swings.

While markets have recovered from April lows, the S&P 500 Index is only up 1.1% year to date through the end of May compared to the MSCI EAFE Index’s 16.9% gain.2 Perhaps the most telling sign of the sea change in sentiment has come from the currency markets, where the US dollar—the global reserve currency—has lost 7.2% of its value relative to a basket of major foreign currencies, as reflected in the ICE US Dollar Index.3 As we discuss below, the dollar’s weakness may potentially support the continued outperformance of non-US stocks.

Weakening US Dollar May Provide a Tailwind for Non-US Stocks

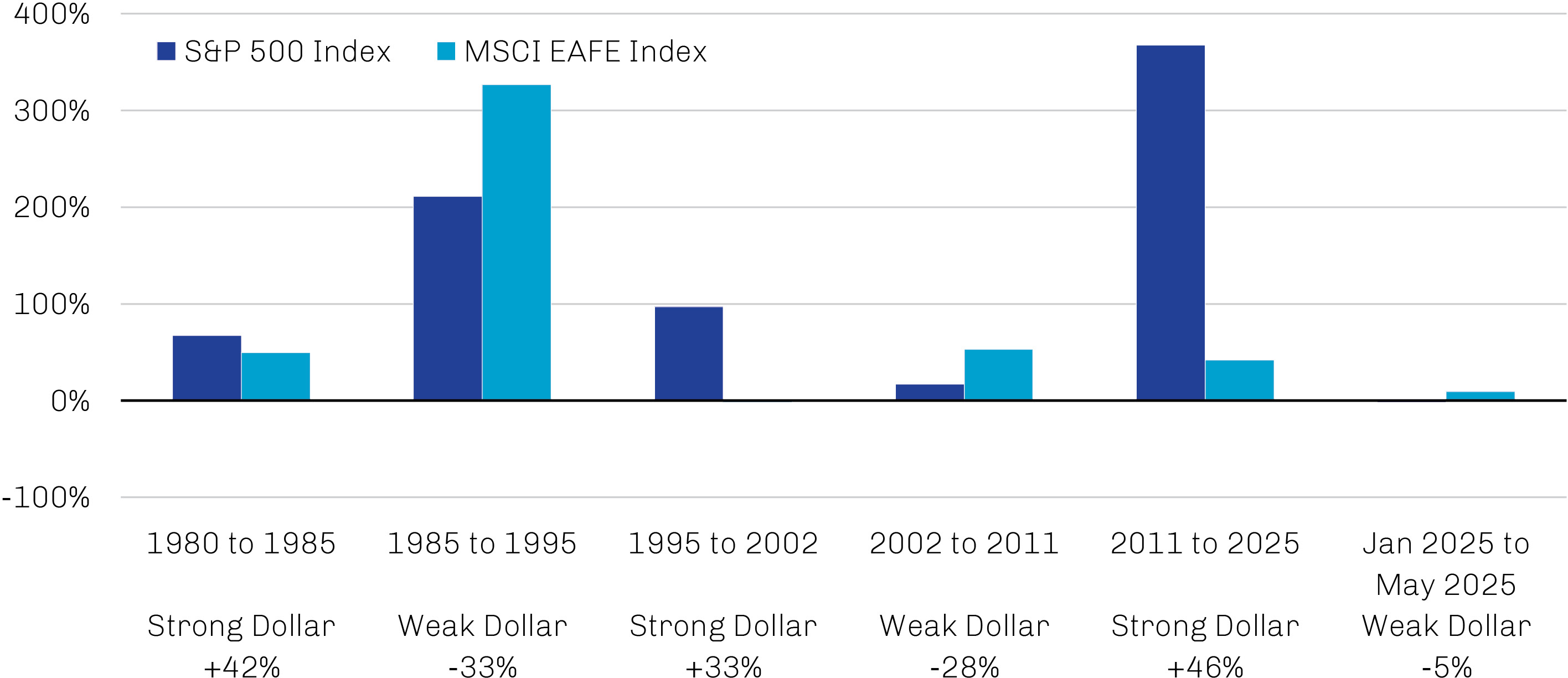

Given the dominance of US equity markets over the past 15-plus years, it can be easy to overlook that the relative performance of US and international stocks has been far more balanced over the long term. One of the key factors influencing relative performance across cycles has been pronounced shifts in the dollar’s value compared to other major currencies. As shown in Exhibit 1, US equities have tended to outperform during periods of dollar strength while non-US stocks have led during periods of dollar weakness. The latter dynamic has been intact thus far in 2025.

Exhibit 1. Changes in Dollar Strength Have Prompted Shifts in Relative Equity Performance

Index Price Return During Various Currency Regimes, January 1980 through May 2025

Note: Dollar performance is measured by changes in the Federal Reserve’s Real Broad Trade-Weighted Dollar Index.

Source: Bloomberg; data as of May 30, 2025.

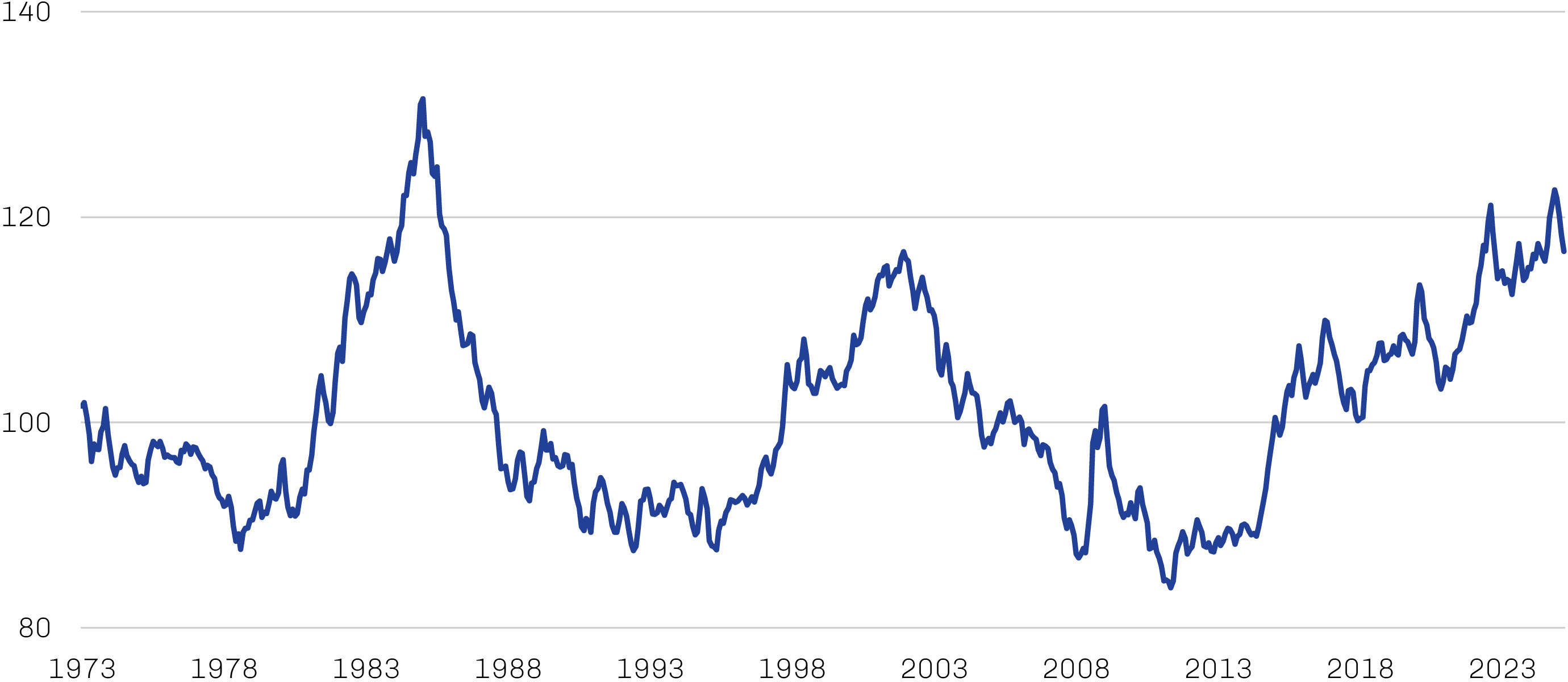

The duration of the dollar’s current pullback can be measured only in months, but there are reasons to believe further weakening is possible. From a valuation perspective having appreciated 44% from 2011 through late 2024, the dollar remains at levels not seen since the mid-1980s, as shown in Exhibit 2, and remains exceptionally strong relative to its trading partners, in our view. Moreover, with the outperformance of US assets over the past decade and half, foreign investors have found themselves overweight the US with low foreign exchange hedge ratios.4 Decisions to trim US exposures or merely to raise hedge ratios could cause material dollar weakness. Any number of factors could shift behavior ranging from cyclical valuation decisions to more structural concerns about US exposure against economic and political uncertainty. And stretched US fiscal conditions may at some point raise concerns about the soundness of the greenback.

Exhibit 2. US Dollar Index Remains Elevated Despite Recent Pullback

Real Broad Trade-Weighted Dollar Index, January 1980 through May 2025; January 2006 = 100

Source: Federal Reserve, Haver Analytics; data as of June 2, 2025.

US Exceptionalism May Be Showing Signs of Wear…

Macroeconomic indicators in the US continue to point to a generally robust and dynamic business environment, but perpetuating these advantages in recent years has come at the cost of massive fiscal deficits and ever-growing debt. To wit, while the US primary fiscal position has been more or less in balance since World War II, economic cycles since the global financial crisis have been characterized by deeper primary deficits at the bottom and shallower surpluses at the top.5 Ballooning government debt has contributed to nominal drift in the economy, to the benefit of S&P 500 earnings and valuations. But what will happen when the fiscal tide ebbs?

It seems likely to us that the US will have to pay the piper for its profligacy at some point, and we have long been sounding the alarm about the risks of unrestrained government debt accumulation. Unfortunately, there are few signs of fiscal discipline on the horizon; for example, the budget bill currently wending its way through Congress would increase the US primary debt by 7.2% over the next 10 years at a time when the cost of servicing this debt continues to climb amid higher rates and a growing base.6 We’re not the only ones who are concerned; in May, Moody’s Investors Service became the last of the three major ratings agencies to strip the US of its AAA designation—following S&P Global Ratings in 2011 and Fitch Ratings in 2023—due at least in part to fiscal concerns.7

Of course, the US is not the only advanced economy experiencing a deterioration in its sovereign debt standing. The Organisation for Economic Co-operation and Development (OECD) forecasts that sovereign debt among advanced economies will rise further in 2025 as will ratios of interest payments to gross domestic product (GDP) due to both higher interest rates and expanded issuance. Perhaps more worryingly, quantitative tightening by a number of major central banks means less demand for local sovereigns from these large, price-insensitive buyers and more supply that must be absorbed by households and foreign investors, potentially pressuring yields still higher.

…as Other Economies Take Steps to Boost Their Vitality

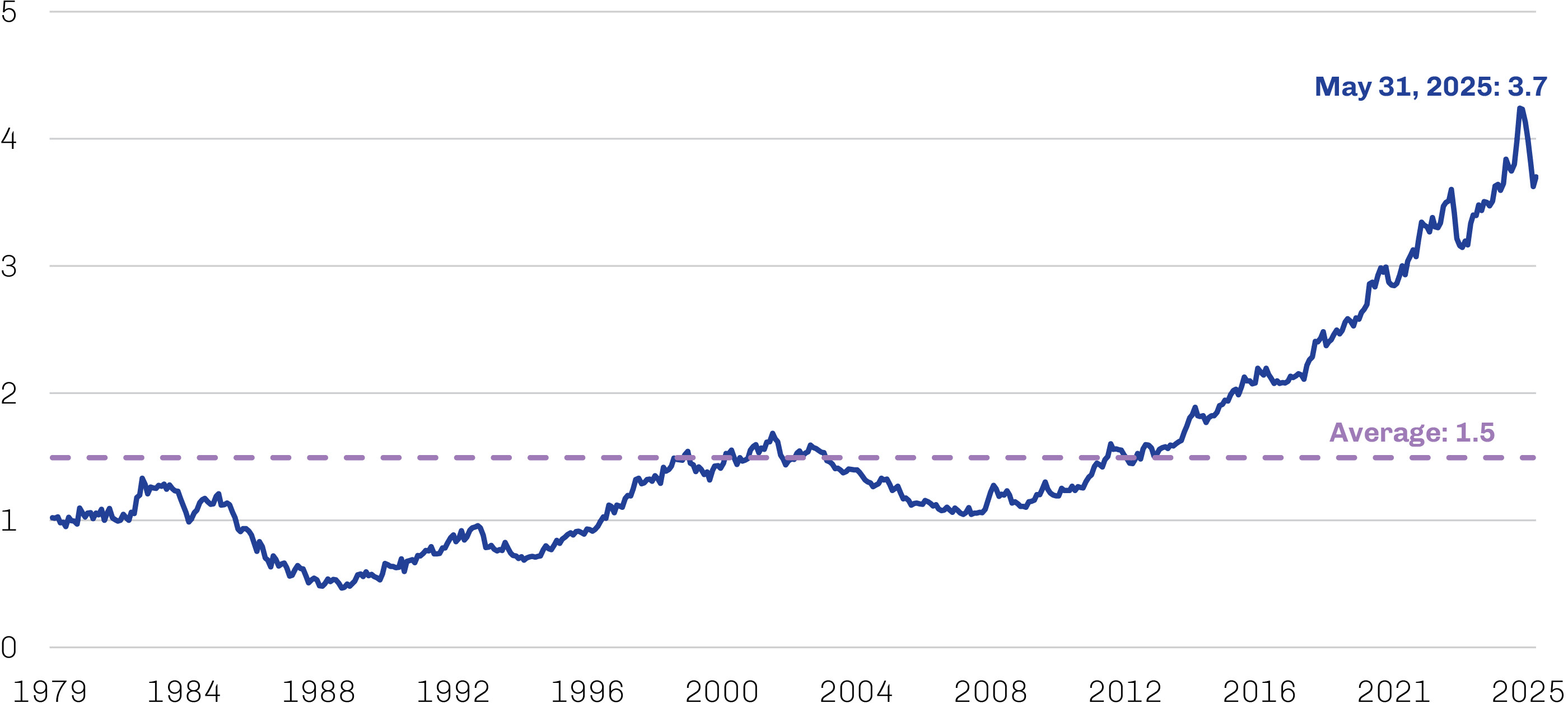

If relative valuations are any indication, the re-rating of international stocks in thus far in 2025 may reflect only the beginning of a reversion to the long-term mean after a prolonged period of underperformance, as shown in Exhibit 3. While our fundamental approach emphasizes bottom-up security selection, we are aware of secular forces outside the US that may provide durable support for local equity markets—and attract investor attention to high-quality businesses outside the US—even as cyclical tailwinds fade.

Corporate governance reform in Japan and Korea. Following many years of economic stagnation, there have been signs that Japan’s “lost decades” may finally be coming to an end—so much so that the Bank of Japan has abandoned negative interest rates to hike its key policy rate to a 17-year high and begun quantitative tightening.8 While the cyclical forces currently supporting policy normalization in Japan will shift over time, potentially durable shifts in corporate governance standards may serve as long-term structural support for Japanese equities. For example, the salutary effects of 2021 updates to the Tokyo Stock Exchange’s Corporate Governance Code continue to reverberate, as listed companies increasingly prioritize sustainable growth strategies and improving corporate value through stock buybacks, higher dividends and the appointment of independent directors.

Likewise, Korea’s Financial Services Commissions in 2024 introduced the “Corporate Value-Up Program” to combat the persistent “Korea discount” in equity valuations as a result of foreign investors’ general reluctance to invest in Korean-domiciled businesses. These reforms are focused on the expansion of fiduciary standards on corporate boards to spur changes at chaebols, the large, family-controlled conglomerates that dominate the Korean economy. While this initiative is in its early stages, we believe that it has the potential to drive a sustained interest and durable re-rating of Korean equities if it becomes a catalyst for meaningful improvements in corporate governance.

China stimulus. Earlier this year, China announced an increase in its fiscal deficit and has since front-loaded debt issuance to support economic growth. This comes on top of 2024’s actions largely focused on boosting manufacturing capacity and preventing a systemic crisis stemming from the combination of a challenged property sector, financially strained local governments and banking-sector weakness. The new initiatives include subsidized loans from the People’s Bank of China to boost consumer spending—particularly in healthcare, eldercare, childcare, tourism and entertainment—as well as providing financial support for the technology sector, which had been hamstrung by regulatory crackdowns in 2020–22. While Chinese equities have outperformed year to date, we believe that valuations remain attractive, and we continue to find cash-generative Chinese businesses with strong, entrenched market positions.9

Fiscal spending in Europe. Russia’s invasion of Ukraine in 2022 prompted an initial rearmament in Europe. However, concerns that the US would no longer guarantee European security produced a sea-change in Europe’s approach toward defense spending, Germany’s new governing coalition spearheaded legislation to permanently exempt defense spending above 1% of GDP from its restrictive constitutional debt brake and created a €500 billion infrastructure fund, measures that will allow the European country with the most fiscal space the flexibility to deploy it.10 While France is contending with fiscal consolidation and trying to reduce its deficit through spending cuts and tax increases, it has also increased defense spending to €100 billion annually by 2030, which represents approximately 3.0–3.5% of GDP.11 In the UK, the relatively new Labour government has announced hundreds of billions of pounds in capital spending planned for the next several years, including an increase of more than 7% for defense spending.12 These initiatives, if successfully implemented, could enhance European integration, bolster productivity, and materially increase long-term growth prospects across Europe.

Exhibit 3. US Equities Continue to Trade at a Signficant Valuation Premium to Their International Counterparts

Price Ratio of S&P 500 Index to MSCI EAFE Index, January 1980 to May 2025; January 1979 = 1

Source: Bloomberg; data as of May 31, 2025.

Selectivity Remains Critical

We do not believe resilient, high-quality businesses with strong balance sheets and persistent earnings power are the exclusive domain of the US—even if market dynamics over the past 15 years or so might suggest otherwise.

We are, of course, mindful of the multitude of risks facing investors in today’s uncertain environment. But it’s been our experience that challenging macro regimes have often provided micro opportunities to selectively acquire resilient businesses—those whose tangible and intangible attributes position them to generate persistent cash flows over the long term and suffer through short-term challenges if necessary—at attractive prices. Though non-US names have mounted a bit of a comeback in the first half of 2025, relative valuations suggest ample runway for continued mean reversion.