Macro & Market Views

Lower Middle Market Direct Lending: Same as It Ever Was

Lower Middle Market Direct Lending: Same as It Ever Was

Investors were first drawn to direct lending due to its rare combination of high current income, limited volatility and strong lender protections.

- We believe the lower middle market continues to offer characteristics that originally drew investors to the asset class including spread, leverage and structure, at deal sizes that facilitate diversification.

- Larger financing packages have become increasingly covenant-lite as lenders compete with both each other and a syndicated loan market where zero-covenant deals are de rigueur. In contrast, one or more covenants remain common in smaller transactions.*

- Structural inefficiencies and capital flight upmarket have supported loan spreads in the lower middle market, which is of particular significance in an environment of falling base rates.

- Despite many lender-friendly characteristics, smaller direct loans have consistently delivered higher risk-adjusted returns than larger ones.**

* Source: PitchBook | LCD; data as of February 28, 2026.

** Source: KBRA DLD; data as of February 11, 2026.

As the asset class grew in popularity and capital flowed in, competition in the space intensified and lending activity increasingly shifted toward larger transactions; with this shift, many of the protections that once differentiated private credit—robust covenants, conservative leverage and lender control—have materially weakened in core and upper middle market deals. In fact, direct lending transactions at the larger end of the market increasingly resemble broadly syndicated loans, but without the benefit of secondary market liquidity. At the same time, the growing popularity of negotiated out-of-court restructurings in larger deals has increased risk and reduced recoveries for minority lenders.1

In contrast, some direct loans to lower middle market companies—typically those with $5–25 million of annual EBITDA—continue to provide the structural risk mitigants and economics that originally defined the asset class and fueled its initial appeal.

We believe the current market environment is unusually favorable for the smaller, more defensively positioned segment of private credit. And as capital continues to crowd into larger transactions and lenders migrate up market with it, the shrinking cohort of specialized lenders that remain dedicated to this space could benefit from a structural capital imbalance.

The Shifting Direct Lending Landscape

Direct lending typically refers to the origination of loans by nonbank lenders—typically asset managers, business-development companies (BDCs) and other institutional investors—to mid-sized companies with financing needs that are generally too bespoke for commercial bank loans but too small to tap the capital markets for their financing needs. Middle market borrowers—broadly defined as companies with annual EBITDA anywhere from $3 million to more than $100 million—typically are privately owned and often have backing from a private equity sponsor. Once dominated by commercial banks, direct lending as we know it today emerged alongside regulatory changes in the aftermath of the global financial crisis that opened the door to nonbank lenders.

Private lending opportunities are available across the debt stack, but senior-secured loans are the most popular, providing lenders first recourse on the borrower’s assets in case of default/restructuring. Typically unrated and without a secondary market, middle market loans offer investors an illiquidity premium, complemented by floating interest rates that mitigate duration risk. These dynamics historically have resulted in a differentiated risk/return profile relative to other fixed income assets, suggesting the potential for portfolio diversification benefits. Providing less leverage than in the core or upper markets—but with slightly more leverage than available from commercial banks— creates a thriving ecosystem for lower middle market direct lenders.

The lower middle market presents a differentiated risk/return profile suggesting potential diversification benefits relative to other fixed income assets.

Dry powder seeking direct lending opportunities has grown significantly in recent years, reaching a record $141 billion in the US at the end of 2025.2 The resulting competition for deals—further exacerbated by the selective return of commercial banks to the fray—has driven a bifurcation within direct lending. Many of the features that made this asset class unique—including robust lender protections, conservative balance sheets and meaningful influence over borrower behavior—have steadily eroded among larger transactions. Today, core and upper middle market deals feature fewer covenants, higher debt levels and greater flexibility for borrowers to defer interest or incur additional debt.3

Lower Middle Market Offers Advantages for Experienced Direct Lenders

While competitive pressures erode lenders’ negotiating power on larger loans, the lower middle market continues to offer private lenders and their investors an attractive combination of stronger covenants, wider spreads and less leverage—at deal sizes that facilitate diversification across borrowers and industries while also discouraging participation by very large lenders. Further, smaller loans tend to facilitate greater access to management teams, promoting more comprehensive due diligence before the loan is written and encouraging a collaborative lender/borrower/sponsor relationship during its life—which are key factors given the lack of a secondary market for these loans. And, at the end of the day, durable exit pathways for lower middle market lenders can reduce exposure to refinancing risk.

Stronger covenants. Financial covenants have long been central to the direct lending investment case. These contractual provisions mitigate the lender’s risk by outlining actions the borrower must take, actions they cannot take and financial thresholds they must meet. Covenants essentially serve as early-warning systems for lenders, alerting them to signs of strain in the borrower’s financial condition and enabling them to engage the borrower on potential remediation—such as an equity infusion from the sponsor or deal restructuring—before they translate into default. They historically have supported higher recoveries and more stable outcomes for investors.

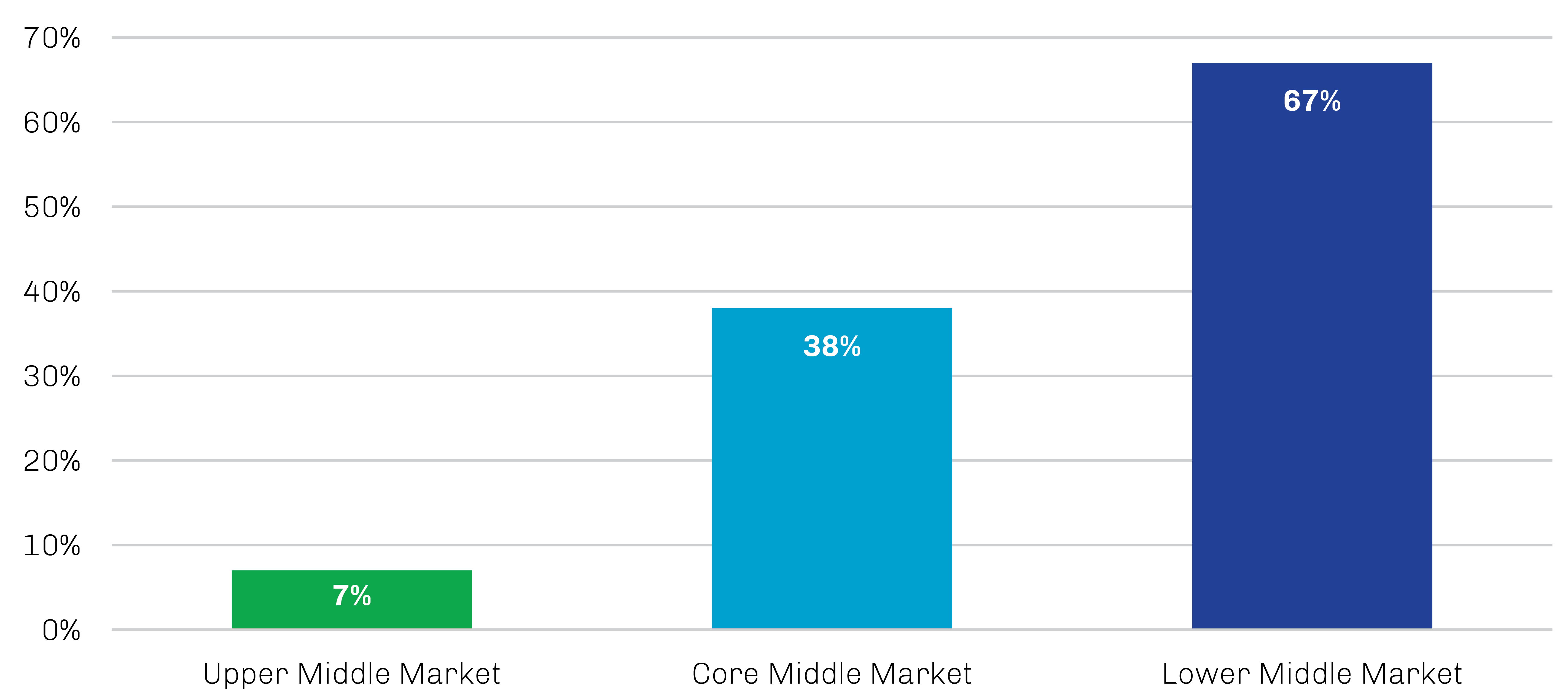

Transactions with core and upper middle market borrowers have become increasingly covenant-lite over the years as lenders compete not only with each other for business but also the syndicated loan market where zero-covenant deals are becoming the norm. As shown in Exhibit 1, covenants remain common in lower middle market transactions.

Exhibit 1. Covenants Remain Common in Smaller Transactions

Loan Population with Covenants by Loan Size

Note: Lower Middle Market = loans less than or equal to $250 million. Core Middle Market = loans of $250-$500 million. Upper Middle Market = loans in excess of $500 million.

Source: Moody’s Investors Services; data as of October 2023 (latest available).

Wider spreads. Despite the preservation of covenants, lower middle market loans continue to command wider spreads than core and upper middle market transactions, as shown in Exhibit 2.

We believe this premium is driven by structural inefficiencies rather than higher underlying credit risk. While lower middle market companies are typically established businesses with stable revenues, experienced management and, often, private equity sponsorship, their smaller size has promoted a fragmented financing market that is less intermediated and more relationship driven. Limited competition from banks and large private credit platforms in this space allow lenders to maintain pricing and structuring discipline. With base rates biased lower since the Federal Reserve began cutting its policy rate in late 2024, spreads have become an increasingly significant component of an investor’s all-in return.4

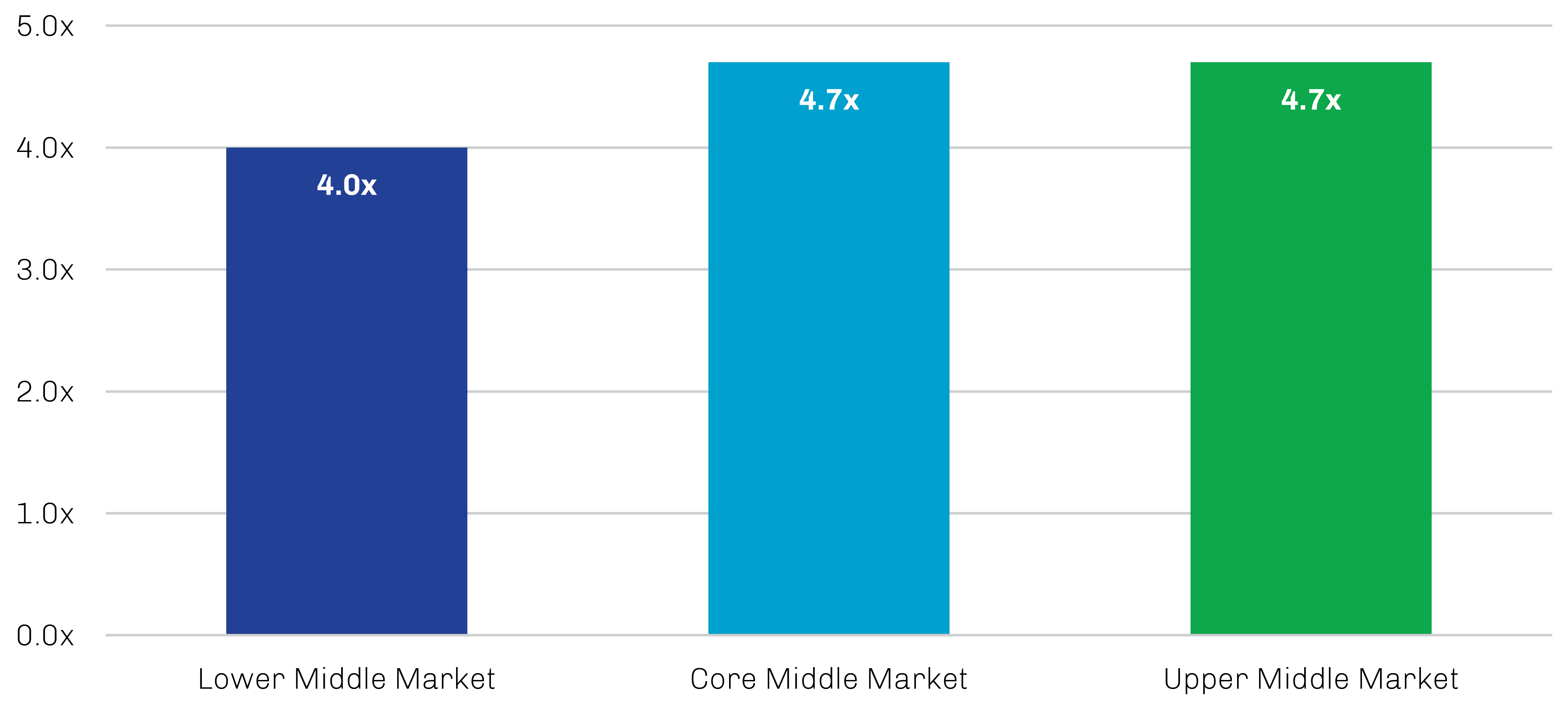

Less leverage. Despite consistently wider spreads, lower middle market transactions are typically structured with materially lower leverage than larger deals, as shown in Exhibit 2. Lower leverage means the company carries less debt relative to its earnings, and the resulting equity buffer can help absorb losses during economic downturns and promote more favorable investment outcomes. Similarly, interest coverage—earnings relative to interest expense—is more conservative in lower middle market deals.5 As these loans typically position lenders at the top of the borrowers’ capital structure, there is considerable junior debt and/or equity beneath to absorb potential losses.

Exhibit 2. Smaller Loans Typically Have Less Leverage Than Larger Loans…

Average Leverage Multiple by Borrower Size

Note: Lower Middle Market = loans less than or equal to $250 million. Core Middle Market = loans of $250–$500 million. Upper Middle Market = loans in excess of $500 million.

Source: Moody’s Investors Services; data as of October 2023 (latest available).

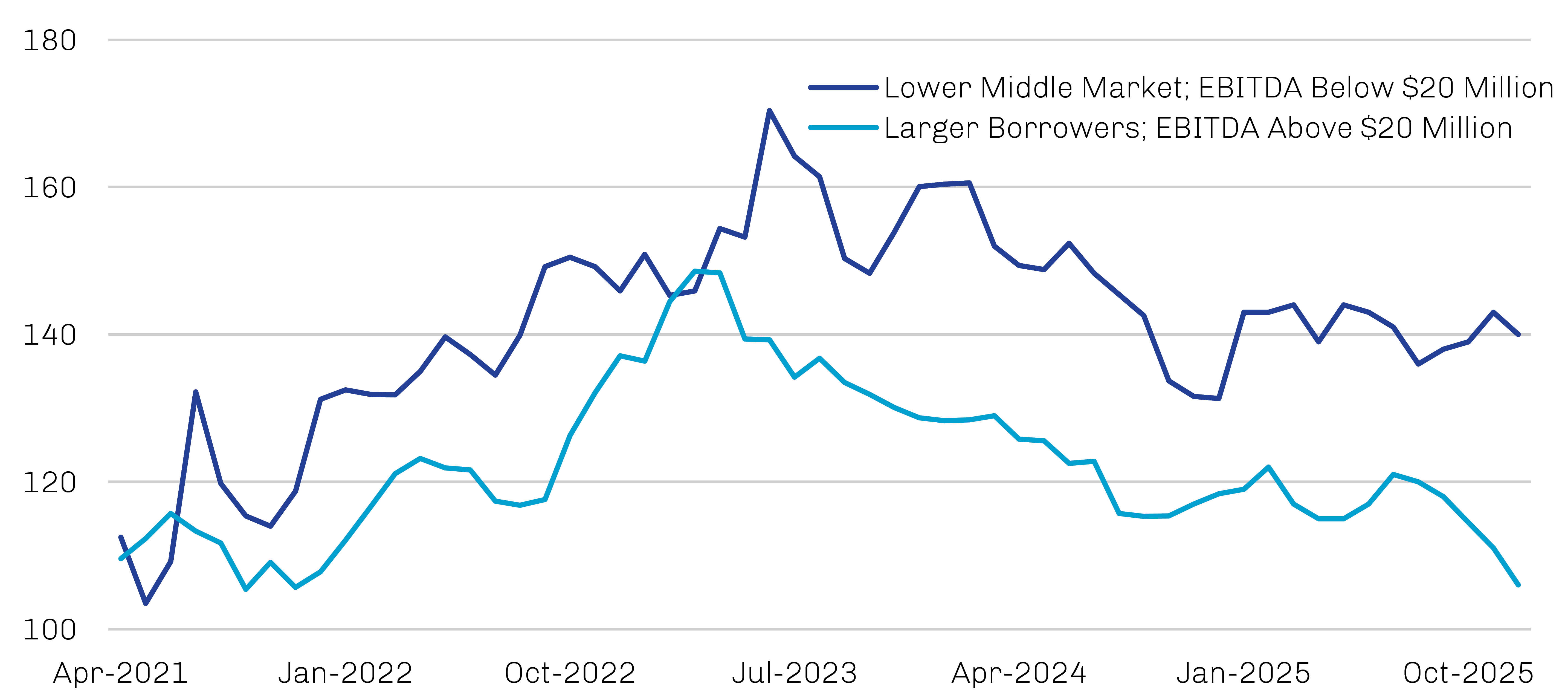

Greater leverage efficiency. Viewed together, the combination of wider spreads and lower leverage is particularly compelling. Lower middle market loans have consistently offered greater spread per turn of leverage compared to larger loans, as shown in Exhibit 3, suggesting the potential for attractive risk-adjusted returns.

Lower middle market loans typically have offered greater spread per turn of leverage compared to larger loans.

Because lower middle market transactions pair higher spreads with lower leverage, lenders have historically earned more income while assuming less financial risk. Larger transactions, by contrast, often pair tighter spreads with higher leverage multiples, resulting in lower compensation per unit of risk.

Exhibit 3. …and Have Historically Delivered Superior Risk-Adjusted Returns

Spread per Unit of Leverage, Three-Month Rolling Average

Source: KBRA DLD; data as of February 11, 2026.

Robust exit dynamics. Smaller businesses tend to be early in their institutional-ownership lifecycle and are often targeted for acquisition as they scale. As a result, realizations of lower middle market loans are often achieved through the sale of the borrower to a strategic buyer or another financial sponsor. In contrast, larger sponsor-backed loans are typically repaid when the borrower is able to refinance at more favorable terms in the broadly syndicated loan market, an activity highly sensitive to capital market conditions.

In our view, a mergers and acquisitions (M&A) driven takeout channel tied to company growth and strategic value creation—rather than the prevailing capital market environment—represents a more durable pathway to repayment for lower middle market lenders and helps mitigate the refinancing risk that characterizes larger, more liquid credit markets.

Lower Middle Market Direct Lending as a Strategic Allocation

The US middle market consists of approximately 200,000 companies, and we believe the 90% that comprise the lower middle market represents the sweet spot of direct lending, offering the most compelling combination of spread, leverage and structure at deal sizes that facilitate diversification.6

Moreover, deal flow in the lower middle market remains deep and resilient—especially M&A activity between sponsors and transactions driven by first-time predicate equity ownership—and steady origination has enabled direct lenders to remain highly selective without sacrificing the structural characteristics that originally drew investors to the asset class. In contrast, the battle over limited deal flow in the core and upper middle markets has led to significant concessions over pricing and deal terms. Since 2021, the number of transactions in the lower middle market has outpaced core and upper market activity by 1,000% as rising interest rates weighed on M&A activity.7

In a private credit market that has evolved rapidly in pursuit of scale, lower middle market lending stands out not because it has changed—it stands out because it has not. We believe lower middle market direct lending should be viewed as a diversifying core component of private credit portfolios for investors seeking durable income, conservative risk positioning and greater consistency through cycles.