Macro & Market Views

Japan: The Sun Also Rises

Japan: The Sun Also Rises

Overview

Key Takeaways

Japanese equity returns in general have been strong of late—especially when denominated in local currency—as solid corporate fundamentals have been bolstered by supportive cyclical and secular forces.

Reversing the trend of recent decades, Japan’s economic performance in 2023 has outpaced many of its large-economy peers while inflation has run above the Bank of Japan’s 2% target as of August 31, 2023.1

Signs of improvements in corporate governance best practices—including stock buybacks, higher dividends and the appointment of independent directors—suggest Japanese equities may find long-term structural support even after cyclical tailwinds fade.

Demographic issues are a prospective obstacle to the Japanese economy, and we remain vigilant for potential fiscal and monetary policy resets that could disrupt the economy and markets.

We believe Japan is home to many high-quality businesses, and the Japanese equity market continues to trade at a significant discount to the US despite its recent success. Selectivity in the market remains key, however.

When the bubble burst in the early 1990s, valuations for everything from equity indexes to commercial real estate plummeted, dragging new investment and consumption down with it and introducing a multi-decade period of sluggish economic growth, incessant deflation and lagging investment returns. In the decades that followed, the Bank of Japan employed a range of monetary policies—both conventional and unconventional—in an attempt to rouse the economy from its persistent funk, mostly to no avail.

Now, after many years of dusk, the Japanese economy may finally be on a new horizon of sustained recovery. Although we are encouraged by the country’s improved economic growth and healthier levels of inflation, we regard cyclical forces as ephemeral. However, new directives from the Tokyo Stock Exchange seeking to improve corporate governance and increase attention on shareholder value—long a blind spot within Japan’s brand of capitalism—may be a source of more durable support for Japanese equities.

Japanese markets in general currently trade at a substantial discount to the US despite their recent run of success, and we believe the country continues to offer potential opportunities to acquire high-quality businesses at attractive prices—especially in light of improved corporate governance trends. Given the impact of Japan’s aging population on domestic consumption, export-focused companies may be particularly attractive.

Are the "Lost Decades" Finally at an End?

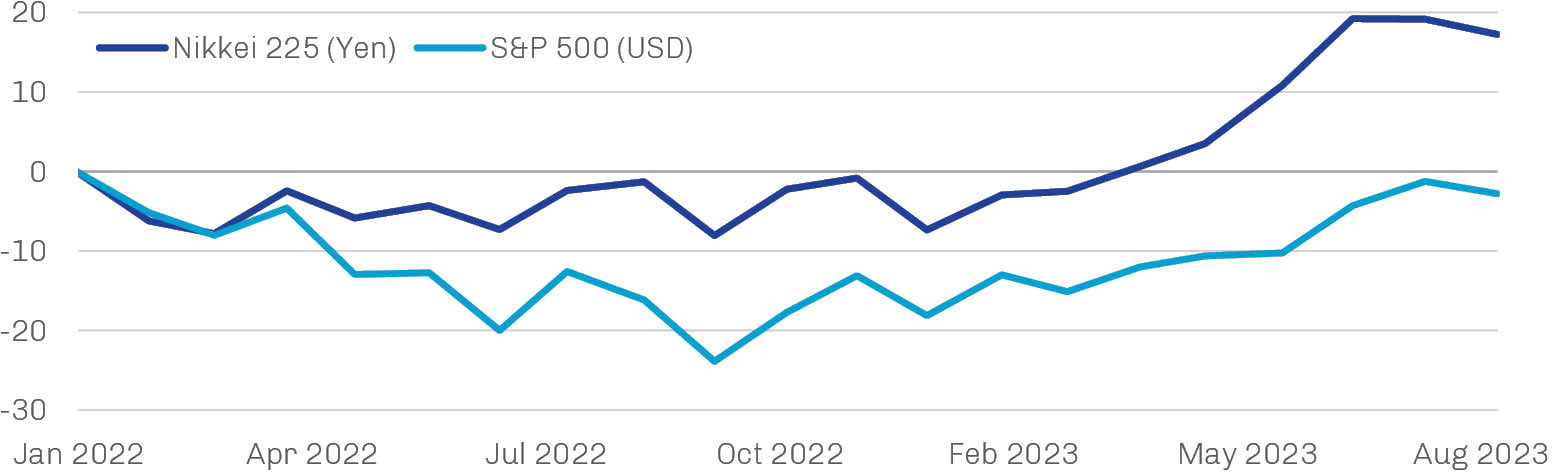

Japanese equities have delivered a strong performance year-to-date 2023, as illustrated in Exhibit 1. The benchmark Nikkei 225 Index climbed 26.5% in local-currency terms through August 31 to approach its all-time high of December 1989; the S&P 500 Index gained 18.7% during the same eight-month period. Japan’s performance has been even more impressive if we widen our lens a bit; by avoiding the worst of last year’s equity market rout, the Nikkei 225 has outpaced the S&P 500 by more than 2,000 basis points since the start of 2022. The weakening yen has been a drag for US dollar-denominated investors, however; hedged returns for the Nikkei 225 are only 13.9% and -7.2%, respectively, for the two periods referenced above.2

Exhibit 1. Japanese Equities Have Impressed of Late...

Local-Currency Returns for Nikkei 225 Index and S&P 500 Index, January 2022 through August 2023

Source: Bloomberg; data as of August 31, 2023.

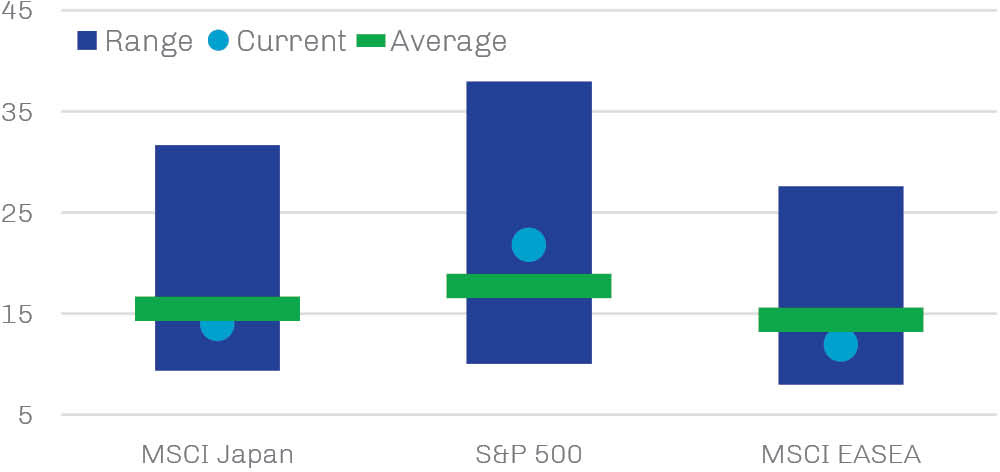

Global investors appear to have taken notice of Japan’s recent success; foreigners purchased Japanese equities during the first six months of 2023 at the strongest pace in more than 20 years, with flows exceeding those into China for the first time since 2017.3 Valuations remain attractive in our view, however; at 14.0 times earnings as of August 31, the MSCI Japan Index is trading at a significant discount to the S&P 500 Index’s multiple of 21.8 and a similar multiple to the MSCI EASEA Index (also known as the MSCI EAFE ex Japan Index) as shown in Exhibit 2. With selectivity a perpetual consideration, we maintain our constructive stance on Japanese stocks given strong fundamentals, cash-laden balance sheets and improved corporate governance.

Exhibit 2. ...But Continue to Trade at a Discount to US Markets

P/E Ratio, January 1, 2005 through August 31, 2023.

Source: FactSet; data as of August 31, 2023.

Japan’s recent success has many observers wondering if the country is finally regaining its footing after its “lost decades” of sluggish economic growth, incessant deflation and lagging investment returns. In the late 1980s, “Japan Inc.”—the anxious Western conceptualization of an economic juggernaut in which business and government interests were aligned in pursuit of commons goals—sat atop the global corporate hierarchy after decades of rapid growth. In 1989, 13 of the world’s 20 largest companies by market capitalization were based in Japan; the largest Japanese company today, Toyota, ranks 32.4 A weak yen and protectionist trade policy helped support exports by Japanese manufacturers early in the 1980s, while the very low interest rates that characterized the second half of the decade encouraged aggressive borrowing to finance business expansion and acquisitions. The latter included trophy assets abroad, including controlling stakes in such iconic American properties as Columbia Pictures, Firestone Tire & Rubber and New York City’s Rockefeller Center.5 Low rates also encouraged market speculation, and prices of Japanese assets surged, led by equity and property markets. The Nikkei 225’s increase in excess of 450% between April 1980 and October 1989 was more than twice the return of the S&P 500.6 The aggregate value of land in Japan—which is about the size of California—ultimately reached $18 trillion, almost four times the property value of the entire US.7

The asset price bubble finally burst in the early 1990s as the Bank of Japan began tightening policy to rein in speculation and forestall inflation. The Nikkei 225 lost almost 80% from its peak in October 1989 to its trough in October 2002, property values plummeted, and the economy fell into a series of bruising recessions.8 By the late 1990s, the country’s banks—once among the largest companies in the world by market capitalization— were in crisis, buried under a mountain of nonperforming loans. Nonbank corporations found themselves heavily in debt from the expansive business strategies pursued in the bubble years\ and with significant excess capacity in the face of slowing demand across industries.9 Japanese households responded to the collapse of asset prices by deferring consumption to repair their balance sheets, thus eradicating healthy inflation and stifling economic growth. The Bank of Japan intervened with a range of conventional and unconventional policies intended to stimulate demand—it cut policy rates to zero by 1999 and launched quantitative easing in 2001— and has more or less maintained these measures amid persistently sluggish economic growth and very low inflation, while also introducing new programs like yield-curve control (in 2016) in response to new challenges.10

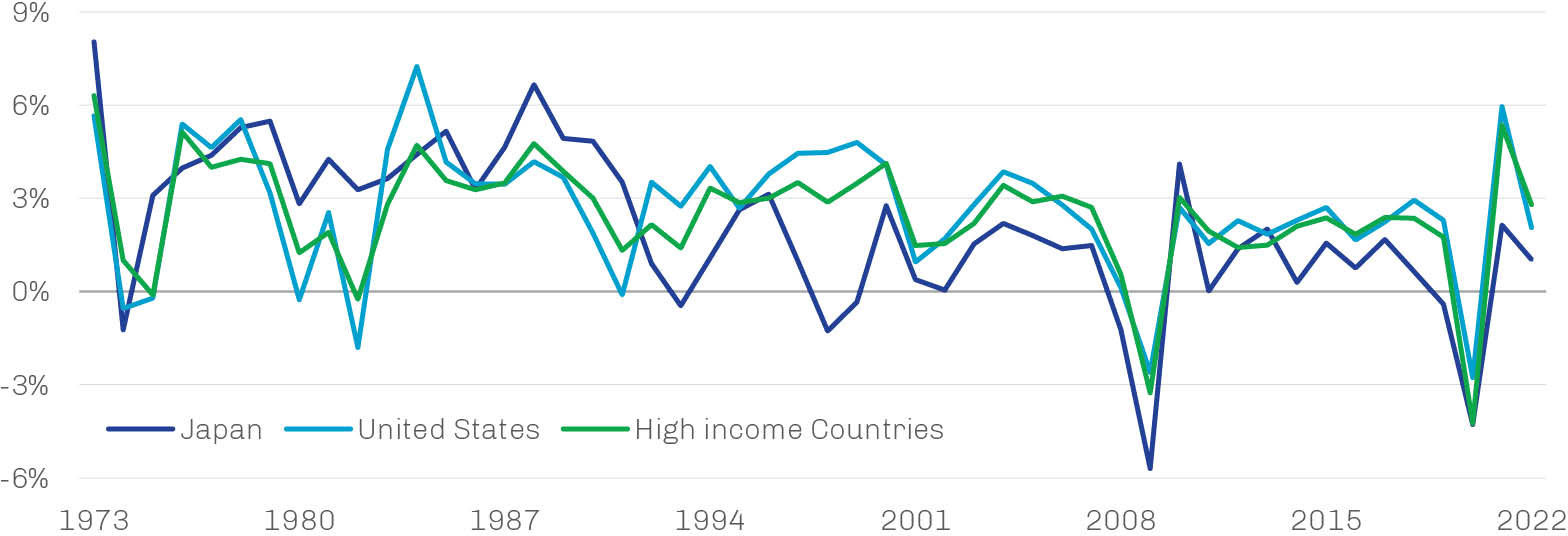

Exhibit 3. Japan Has Been in a Multi-Decade Economic Rut

Annual GDP Growth, 1973 through 2022

Source: World Bank; data as of December 31, 2022.

After more than two decades of economic growth below 2.5% (other than an aberrant spike in 2010, Shinzo Abe’s first year of office), annualized GDP for the first and second quarters of 2023 came in at 2.7% and 4.8%, respectively, bringing GDP to a record high.11 Core consumer price inflation was 3.1% in August, the 17th consecutive reading above the Bank of Japan’s 2% target.12 Very accommodative monetary policy by the Bank of Japan as other central banks have tightened aggressively has helped. The resultant weaker yen has made Japanese exports more competitive in global markets and the revenues generated abroad more valuable when translated into local currency, bolstering profits for Japan’s manufacturers. Ongoing fiscal support has been another stimulant, as the Kishida government has prioritized supporting economic growth over spending reform, at least for the time being.13

These cyclical tailwinds may be easing, however. The Bank of Japan has begun modulating its yield-curve control settings. In July, it said it would allow long rates to rise as high as 1%, and September brought news that a wider tolerance for short yields may be on the horizon, though perhaps not any time soon given lagging inflation-adjusted wages.14 Though these moves suggest the Japanese economy may be closer to standing on its own after decades of extraordinary support, tighter monetary policy may boost the yen and pressure margins for local manufacturers selling abroad. Additionally, the Kishida’s government’s desire to achieve a balanced primary budget by the fiscal year ending in March 2026 may be ambitious given current trends suggesting non-defense fiscal spending may come under scrutiny.15

Improved Corporate Governance Standards May Offer Durable Support to Japanese Equities

While cycles by definition ebb and flow, potentially durable shifts in corporate governance standards may serve as long-term structural support for Japanese equities. Historically, many Japanese companies showed little interest in cultivating outside investors, and those intrepid foreigners willing to look through the lackluster Japanese economy and wade through Japanese-language corporate reports often were frustrated by the country’s unfamiliar form of capitalism. Traditionally, Japanese corporations have sought to serve a broader range of stakeholders than is typical of Western companies, including Japanese society as a whole. As a result, managements often appeared more concerned about business durability than growth, much less the optimization of their capital structures—an attitude that generally resulted in outsized cash holdings on their balance sheets.

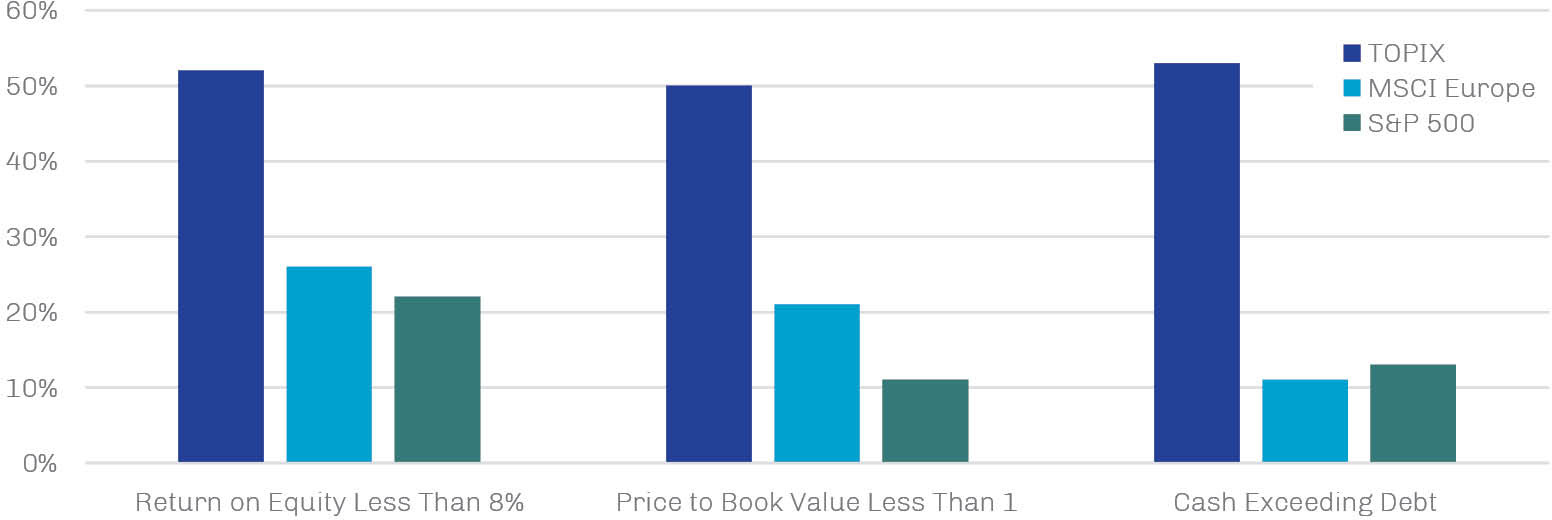

While we have seen some token concessions over the years, shareholders may at last reap their full due thanks to recent updates to the Tokyo Stock Exchange’s (TSE) Corporate Governance Code. Increasingly adopted by corporate managers, these revisions are designed to prod Japanese companies to pursue sustainable growth strategies and prioritize improving corporate value. They specifically target the broad swath of listed companies believed to have untapped potential for profitability and growth, defined as those trading below book value or with returns on equity less than 8%. As highlighted in Exhibit 4, approximately 50% of TSE listings meet these criteria.16

Exhibit 4. Japanese Companies Have Much Room to Improve Capital Allocation Policies

Percentage of Companies Within Each Index Demonstrating Indicated Characteristic

Source: FactSet; data as of August 31, 2023.

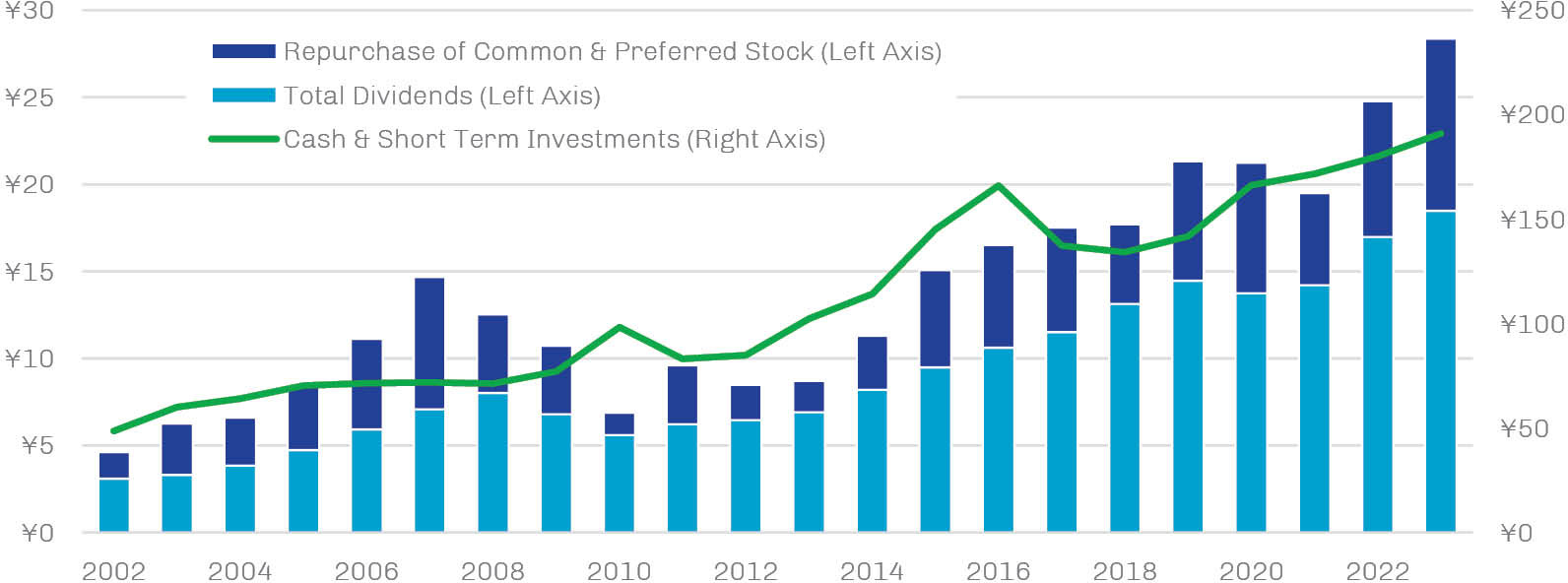

Low valuations and sub-standard returns often reflect high cash balances; with more than 50% of Japanese companies having cash balances that exceed debt as of August 31, 2023, there is ample runway to increase dividends and buy back shares.17 Perhaps triggered by TSE guidelines, the dash by managements to reduce cash by returning capital to shareholders is well underway. Payout ratios have risen and approximately 30% of Japanese companies announced dividend increases in fiscal 2024, aggregating to a new record for the third year running.18 Even as dividend payouts increase, managements have demonstrated a healthy appetite to buy back their own shares, thereby reducing their equity base and cost of capital while increasing shareholder returns. Approximately 18% of major companies listed on the TSE announced plans to buy back shares in fiscal 2023, at a volume forecast to match the record set the previous fiscal year.19 Despite dividend increases and share buybacks, however, cash reserves in general continue to grow—having almost doubled over the past decade and increasing approximately 20% since year-end 2020, as highlighted in Exhibit 5—providing potential opportunity to reward shareholders.20

Exhibit 5. Cash Continued to Accumulate Despite Increased Dividends and Share Repurchases

Trillions of Yen, 2002 through 2023

Note: 2023 data are year to date through August.

Source: FactSet; data as of August 31, 2023.

Beyond improved profitability and more prudent allocation of capital, TSE is also calling for enhancements to other governance principles, such as a reduction in cross-shareholdings, the inclusion of independent directors on boards and improved engagement with investors (including disclosures in English).

Cyclical Reversals Always Loom

While hopeful that the Japanese economy may finally be at an inflection point, we have seen false dawns before. For a very long time, the Japanese economy has been underpinned by zero or negative interest rates and aggressive government spending. Current policy settings still seem a long way from neutral, and it remains to be seen how Japanese markets will react should policies normalize. Tighter monetary policy may result in yen appreciation, dampening the profits of companies accustomed to selling prices denominated in richer currencies abroad. Very high levels of debt to GDP may prompt an appetite for fiscal consolidation, and some combination of restrained government spending or higher taxes likely would weigh on economic activity.

Perhaps the biggest obstacle to Japan’s economic rebound will be its aging (and now shrinking) population. A smaller workforce portends labor shortages, reduces productivity and decreases demand for goods and services while denting the tax revenues needed to fund higher levels of social support for retirees and the elderly, namely healthcare and pension costs. To counteract this decline, Japan has opened some positions to migrants, encouraged women to join the workforce and invested in automation to enhance productivity.21,22 Recognizing the bounded opportunities at home, many companies have sidestepped dependence on the domestic economy by instead focusing on international sales.

A recent tailwind from the apparent redirection of investment flows from China to Japan also may abate at some point. When China’s economy was booming, global investors seemed willing to discount a hostile regulatory and corporate governance environment, crackdowns on tech companies and persistent geopolitical tensions; they seemed to have become less tolerant of these factors in light of China’s cooling economy, teetering real estate markets and massive debt levels. If history is a guide, though, at some point Chinese equities may again become sufficiently cheap for investors to prioritize potentially asymmetric investment returns over near-term macro concerns, restoring flows to Chinese equities at the expense of Japanese markets.

Conclusion

The Japanese equity market has been a global standout year-to-date 2023, propelled by both cyclical and secular factors. While cyclical tailwinds come and go, secular improvements in corporate governance—highlighted by a concerted effort by companies to return capital to shareholders through stock buybacks and dividend increases and to promote corporate value—could represent a more durable foundation for Japanese equities going forward. Selectivity in this market remains key, however, and building a portfolio of strong businesses acquired at attractive prices, in our view, is the most reliable source of long-term resilience.

Source: Reuters; data as of September 21, 2023

Source: Bloomberg: data as of August 31, 2023

Source: Bloomberg; data as of June 30, 2023

Source: CNBC; data as of August 31, 2023.

Source: The Washington Post; data as of March 23, 1990

Source: FactSet; data as of August 31, 2023

Source: The New York Times; data as of December 25, 2005

Source: CNBC; data as of October 31, 2002

Source: International Monetary Fund; data as of February 13, 2003

Source: Reuters; data as of September 9, 2023

Source: Reuters; data as of September 9, 2023

Source: Reuters; data as of September 21, 2023

Source: Reuters; data as of June 7, 2023

Source: Reuters; data as of August 7, 2023

Source: Reuters; data as of July 23, 2023

Source: FactSet; data as of August 31, 2023

Source: FactSet; data as of August 31, 2023

Source: Asia Nikkei; data as of June 8, 2023

Source: Kyodo News; data as of June 10, 2023

Source: FactSet; data as of June 30, 2023

Source: Foreign Policy; data as of June 23, 2022

Source: Japan Times; data as of July 21, 2023

Video Insights

-

Investment Insights

Investment Insights with Alan Barr

-

Investment Insights

Investment Insights with Matt Lamphier

Alan Barr

Download PDF

Japan: The Sun Also Rises

After decades of rapid growth following World War II, Japan’s dynamic, export-led economy had become the envy of the capitalist world, perhaps distracting attention from the debt-fueled asset-price bubble that had

begun to emerge in the mid-1980s.

When the bubble burst in the early 1990s, valuations for everything from equity indexes to commercial real estate plummeted, dragging new investment and consumption down with it and introducing a multi-decade period of sluggish economic growth, incessant deflation and lagging investment returns. In the decades that followed, the Bank of Japan employed a range of monetary policies—both conventional and unconventional—in an attempt to rouse the economy from its persistent funk, mostly to no avail.