Macro & Market Views

Gold in Investment Portfolios: FAQs

Gold in Investment Portfolios: FAQs

Many of the diversified equity portfolios managed by First Eagle’s Global Value team maintain a strategic allocation to gold and gold-related securities.

- For investors with long time horizons, gold’s differentiated risk-return characteristics have enabled it to maintain its real value across disparate macroeconomic environments and through existential disruptions to markets, a feat we consider truly rare.

- Investors seeking the potential hedging features of gold may find different levels of exposure and different asset mixes suitable, depending on their risk-return objectives and macroeconomic and market expectations.

- First Eagle’s Global Value team views bullion and gold-related equities as complementary methods to gaining gold exposure. We actively but patiently manage our relative allocations to gold bullion and gold stocks from the bottom up.

- Given the inherent uncertainty of the gold market and the many complex factors that drive its movement, we believe a strategic allocation to gold in certain of our portfolios is the most compelling way to gain exposure to its characteristics as a potential hedge against adverse market conditions.

Driven by our belief that the permanent impairment of capital is the greatest risk facing investors over the long term, gold serves as a long-duration potential hedge that we believe can provide portfolios with a source of resilience across a wide variety of adverse circumstances— including both inflationary and deflationary environments as well as equity bear markets and sharp near-term selloffs—while also supporting real purchasing power across market cycles.

After decades of persistently low interest rates and periodic bouts of extraordinary stimulus, less-accommodative policy has been the norm in recent years. In addition to a higher cost of capital, investors today also face a litany of acute risks, including massive sovereign debt levels, ongoing fiat currency debasement, complex political and geopolitical dynamics, and general systemic fragility—all of which we believe highlight the value of a potential hedge like gold.

Our conversations with clients and advisors have revealed increased interest in the metal, and this paper responds to some of the questions we are asked most frequently when discussing gold and its application in diversified portfolios.

Q: How can investment portfolios potentially benefit from gold?

We believe the differentiated risk-return characteristics of gold make it a potential all-weather hedge against a variety of market, macroeconomic and geopolitical disruptions, as well as a store of value across these same conditions. With a low correlation to most major asset classes since 1971— when it began to trade freely following the collapse of the Bretton Woods system—gold historically has served as a diversifying complement to portfolios under a range of circumstances and has been supportive of long-term investment, based on our research.

Q: Should gold be viewed as a potential hedge against inflation or against tail risk? How does it compare with other potential hedges?

For long-term investors, gold has maintained its real value across disparate macroeconomic environments and through existential disruptions to markets, a truly rare feat in our view. Over the past two centuries alone, gold has withstood inflationary episodes and deflationary spirals, political revolutions and rapid technological evolution, localized conflicts and world wars, pandemics and treatments for them.

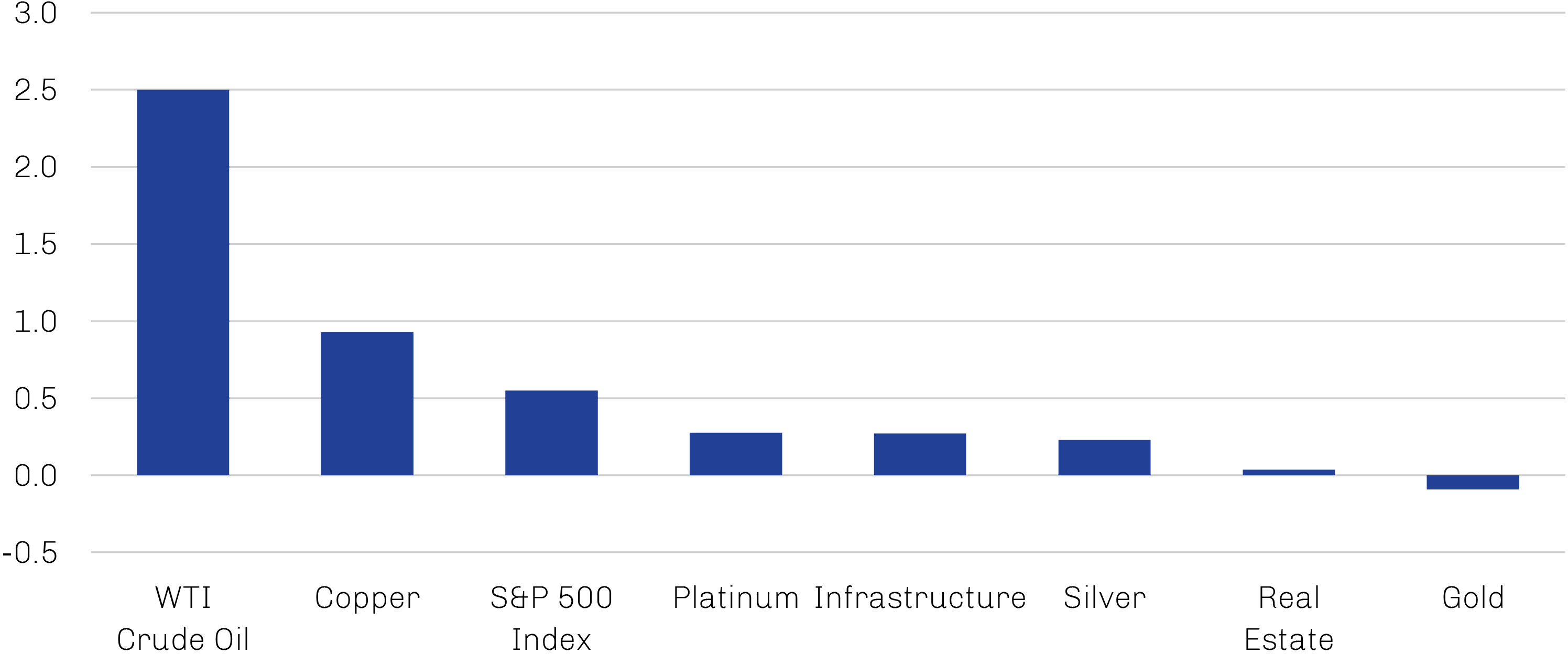

Unlike other commodities and real assets that investors may consider for their inflation-hedging potential—such as copper, oil, silver and platinum—gold has limited industrial application and slightly negative beta to business activity over the last decade, as shown in Exhibit 1. While these assets share gold’s relative limited supply and history of retaining their real value during periods of inflation as the value of fiat declines, their sensitivity to economic activity impairs their reliability as hedges in periods of economic weakness and/or deflation.

Exhibit 1. Gold Has Slightly Negative Beta to Business Conditions over the Last Decade

Beta to US Economic Activity (as Represented by Institute for Supply Management’s PMI), April 2015 through April 2025

Note: Commodity prices are represented by the generic front-month futures contract on the respective underlying commodity. Infrastructure = S&P Global Infrastructure Index; Real Estate = FTSE Nareit All Equity REITs Index.

Source: Bloomberg; data as of April 30, 2025.

Gold’s qualities also are differentiated from financial assets that investors often consider as potential hedges. Massive levels of sovereign debt in the developed world have significantly increased the risk government bonds now carry even as both nominal and real yields have returned to levels not seen since the global financial crisis of the mid-2000s, while structural issues also impair the use of government bonds as a long-duration potential hedge. Options and other derivatives contracts are another financial alternative but come with their own set of limitations, including implementation expense, relatively limited liquidity and counterparty risk.

Cryptocurrencies are another asset class that in recent years has entered the potential hedge discussion—so much so that many of its backers refer to bitcoin, the world’s largest cryptocurrency by far in terms of market value and trading volume, as “digital gold.”1 For all of their broadening appeal, cryptocurrencies represent a very young asset whose behaviors across varying macroeconomic and market regimes are theoretical at best; in our view, they can be more accurately described as an option on becoming digital gold. In contrast, actual gold has served as a store of value for millennia, and its differentiated risk-return characteristics have enabled it to maintain its real purchasing power over time across disparate environments and through numerous existential threats, providing investors a perceived “safe haven” in times of need.

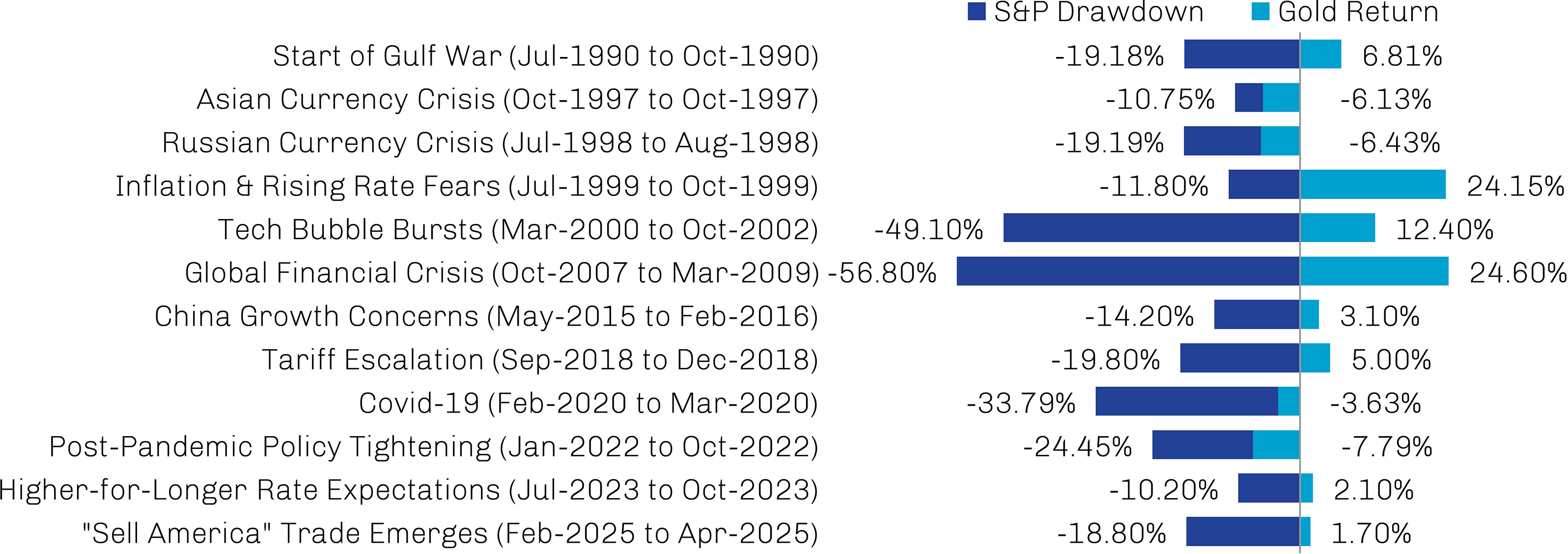

In terms of tail risk, gold’s countercyclical tendencies have been particularly evident during periods of extreme equity market distress, as illustrated in Exhibit 2.

Exhibit 2. Gold Exposure Has Mitigated the Impact of Recent Market Corrections

Price Changes During All 10%-Plus Drawdowns in the S&P 500 Index Since 1990

Note: Gold returns are represented by the Bloomberg gold spot price in US dollars per troy ounce. All returns calculated daily.

Source: Bloomberg, FactSet; data as of April 30, 2025.

Past performance does not guarantee future results.

Q: How much gold is needed to achieve a potential hedge? What investment “bucket” should it be in?

There doesn’t seem to be a “one size fits all” approach to gold allocation among investors. Those seeking the potential hedging features of the metal may adopt different levels of exposure and different asset mixes, depending on their risk-return objectives and macroeconomic and market expectations. Generally speaking, portfolios with higher levels of risk require higher allocations to gold to harness its attributes as a potential hedge. For example, a well-diversified portfolio of 100% equities may require a greater gold allocation than a traditional 60/40 portfolio, while a concentrated equity portfolio or a portfolio of illiquid assets may need more than both.

Achieving a meaningful level of gold exposure likely would require a standalone allocation rather than secondary exposure through other broad investment vehicles. For example, gold comprises 5.1% of the S&P GSCI, a popular production-weighted index based on futures contracts for physical commodities.2 This suggests that a multiasset portfolio with 10% of its assets benchmarked to this index would achieve a gold allocation of about 0.5%, a level too small to have a material impact.

Q: How do you view the various types of gold exposure? How do you manage your relative allocation of bullion and miners?

There are several ways to gain strategic exposure to gold, all of which have different risk-return profiles and liquidity characteristics. As investors, the Global Value team views bullion and gold-related equities as complementary methods to gaining gold exposure. We actively manage our relative allocations to gold bullion and gold stocks from the bottom up in an extremely patient way. Generally, we seek to own gold companies we view as undervalued based on the current gold spot price and our assessment of their quality, and we will keep client capital invested in bullion until such opportunities emerge.

Gold bullion is viewed as one of the most conservative forms of gold ownership because it tends to carry the least risk; the asset is already out of the ground, so it is free and clear of mining risk, and it has minimal counterparty risk. On the other hand, a bar of gold offers no yield and costs money to store, which means that gold bullion may not always be the most cost-effective way to invest in gold ounces. Our preference is to own the physical asset directly in an allocated account (as local jurisdictions permit). While physical ownership entails storage expenses, bullion—unlike exchange-traded funds (ETFs), futures or any other gold-proxy structures—does not have any counterparty risk, which we consider a key benefit during times of stress.

Gold in the dirt can be as useful as gold in the vault; for us, shares of gold-related equities—including miners and royalty and streaming companies—can sometimes be a cheaper way to gain exposure to the metal than buying bullion. This approach comes with increased risk and volatility, however, as the performance of gold-related stocks has tended to be leveraged to the price of gold, meaning that changes in the price of the underlying metal can have an outsized impact on stock prices.

Miners face the operational risk of getting gold out of the ground and potential political risks related to the countries in which mines are located, among other challenges common to industry participants. Nonetheless, gold-mining stocks may offer investors differentiated opportunities; historically, the ability of certain higher-quality gold miners to increase their production per share and/or gold reserves per share over time— whether through operational execution, countercyclical capital allocation or exploration success—has added value for shareholders and highlighted the importance of stock selection when investing in this space.

As they provide financing to miners in exchange for an ongoing economic interest in the mineral production of a property, gold royalty and streaming companies face the same risks as miners, but to a lesser degree. These companies typically diversify their risk exposure by having agreements on multiple mines at various stages of production or development,and historically have demonstrated less price volatility than miners as a result.

Q: Should gold exposure be managed tactically or strategically?

Given the inherent uncertainty of the gold market and the many complex factors that drive its movement, we believe a strategic allocation to gold is a compelling way to gain exposure to its characteristics as a potential hedge against adverse market and macroeconomic conditions.

The Global Value team takes the humble view that while disruptive episodes are inevitable, they also are impossible to predict. Because of this, many of our diversified portfolios maintain a strategic allocation to gold as a long-duration potential hedge against adverse outcomes. Of all the available potential hedging options, both real and financial, we believe gold’s differentiated risk-return characteristics enable it to serve as a source of resilience in the widest variety of adverse circumstances—including both inflationary and deflationary environments as well as in equity bear markets—while also supporting real purchasing power across market cycles.

Q: How has gold performed over time?

While First Eagle’s strategic approach to gold allocation relieves us of the impossible task of forecasting its price, certain lessons can be gleaned from the historical movements in the price of gold.

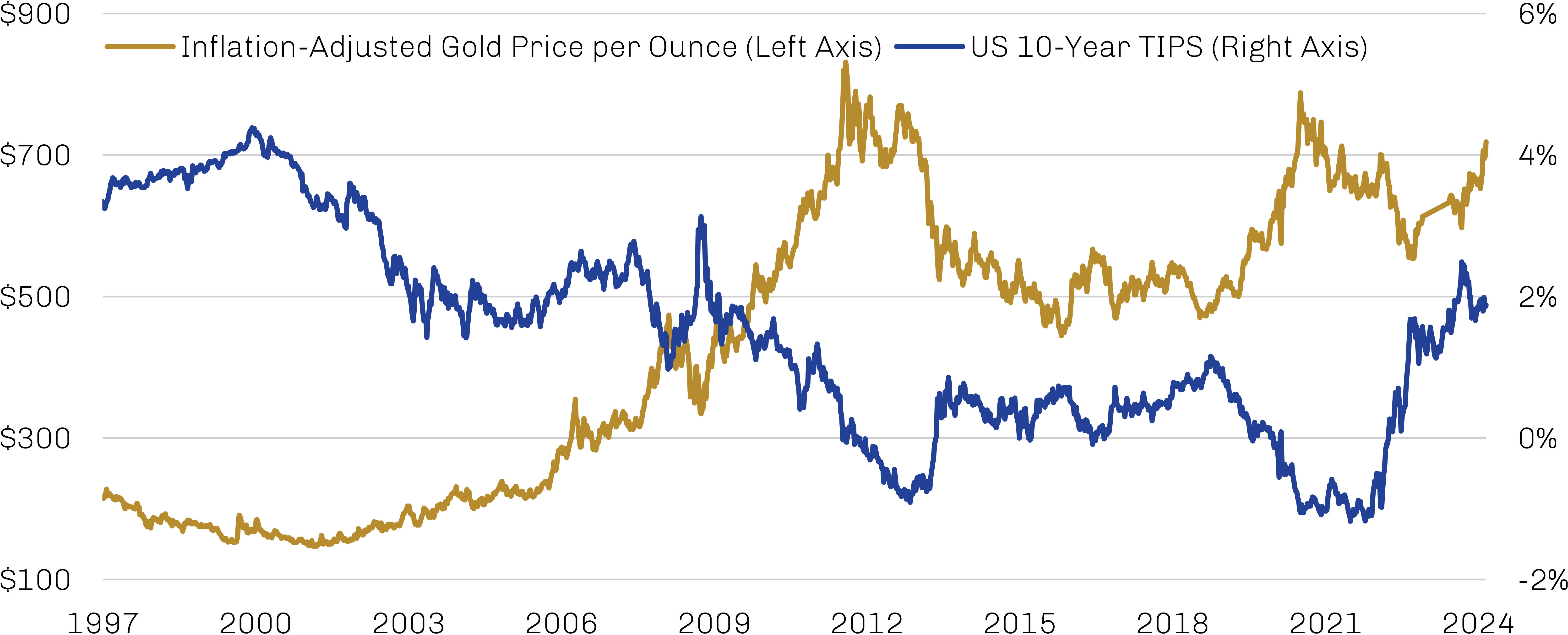

Most notable of these is gold’s inverse relationship with real interest rates (i.e., the difference between nominal interest rates and inflation). While there can be short-term aberrations in this relationship, we believe real interest rates are the most important driver of the gold price over the medium and long term. Throughout history, gold prices have tended to be at their highest—and real interest rates at their lowest—when the economy is weak and/or experiencing inflation, periods that have tended to coincide with low levels of confidence in the economy and government and thus a greater inclination among investors to hold a universal currency like gold rather than its man-made substitute. As shown in Exhibit 3, when real interest rates have moved lower, the gold price, despite some lead/lag effects, historically tended to move higher and vice versa.

Exhibit 3.Gold Historically Has Been Inversely Related to Real Interest Rates

January 1997 through April 2025; Consumer Price Index, 1982–84 = 100

Source: Bloomberg; data as of April 30, 2025.

Past performance does not guarantee future results.

Though the years do not align perfectly with inflection points, as depicted in Exhibit 4, it may be helpful to consider the pricing dynamics of gold by decade.

1970s: Untethered from the US dollar in 1971 upon the demise of the Bretton Woods agreement, gold rallied sharply for the rest of the decade to reach its inflation-adjusted peak in January 1980. Across a decade marked by inflation, oil shocks and geopolitical turmoil, gold posted a cumulative return of more than 2,000%.

1980s/90s: The Fed’s extraordinary efforts to combat inflation in the early 1980s pushed real interest rates sharply higher and brought an end to gold’s post-Bretton Woods rally. The re-emergence of confidence in the monetary regime left investors with little interest in a perceived “safe haven” like gold for the rest of the century, while some central banks concluded that gold was no longer critical to their foreign reserves and sold it in large quantities. By 1999, the gold spot price had swooned to around $250, reinforcing the widespread skepticism about the utility of gold prevalent at the time.

2000s: Gold returned to prominence early in the twenty-first century, as economies and equity markets were battered by a variety of adverse events, including the bursting of the dot-com bubble in the early 2000s and the global financial crisis of 2007–09, the aftermath of which pushed real interest rates steadily lower and ultimately into negative territory.

2010s: While gold’s strength persisted through the first few years of this decade as economies globally struggled to reflate their economies, a rebound in interest rates sent its price to a post-financial crisis bottom in 2015. It bounced around slightly above that level for several years before embarking on another leg higher in late 2018 as evidence of a cooling economy forced the Federal Reserve to pause—and ultimately reverse—its policy tightening.

2020s: The shifting policy, macroeconomic and geopolitical conditions that have characterized the first half of the current decade have been evident in movements of the gold price. While the massive policy response to the Covid-19 outbreak in 2020 suppressed interest rates and helped drive gold to a new all-time nominal high above $2,000/oz in August of that year, the price eased considerably with the renewed economic optimism that accompanied the rollout of vaccines. Gold spent much of 2021 in a trading range as investors sought to get a read on the direction of monetary policy, but Russia’s early-2022 invasion of Ukraine had the metal again testing the $2,000 level. The commencement of the Fed’s rate-hike cycle in March 2022 brought that rally to a quick end, and by autumn gold was trading in the mid-$1,600s. However, a resurgence in central bank buying later in the year sparked a durable rally in the gold price even as real interest rates continued to climb, and central bank demand has continued to provide massive support. Gold again eclipsed $2,000/oz in late 2023 and hasn’t looked back, setting a string of new nominal highs and finishing April 2025 above $3,300/oz. We discuss current gold-market dynamics in more detail in the next question.

Exhibit 4. Gold Price Regimes Have Varied over Recent Decades

Gold Spot Price per Ounce at Month-End, January 1970 through April 2025

Source: Bloomberg; data as of April 30, 2025.

Past performance does not guarantee future results.

Another way to consider the performance of gold over time is to view its price changes in the context of money supply growth. In that respect, we believe gold has unequivocally shined. Gold supply growth has tended to be steady at levels well below that of fiat currency and, thus, the nominal demand for gold. Gold production from 1900 to 2021 compounded at a rate of less than 2% per year, for example, while M2 money supply in the US has posted a compound annual growth rate of close to 7% over the past 50 years.3 As a result, the purchasing power of gold has increased as that of fiat currencies has continued to erode.

Q: What is fueling the recent surge in the gold price?

Since bottoming at around $1,630/oz in October 2022, the price of gold has more than doubled.4 Perhaps most remarkable about the current rally has been its persistence; the metal’s price plowed unceasingly higher through conditions both hospitable to gold appreciation and otherwise.

It’s been our experience that the gold market can sometimes serve as the metaphorical canary in the coalmine, sussing out potential dangers before they manifest in asset prices more broadly. We believe such dangers have been plentiful in recent years. Increasing sensitivity to the massive accumulation of debt by governments worldwide, for example, may support interest in an asset like gold with a track record as a potential hedge against currency debasement. Investors looking for potential “safe havens” in uncertain times, meanwhile, have ample reasons to consider gold amid a turbulent geopolitical backdrop marked by wars both hot and cold, threats to US hegemony and the global order, and fraying traditional alliances.

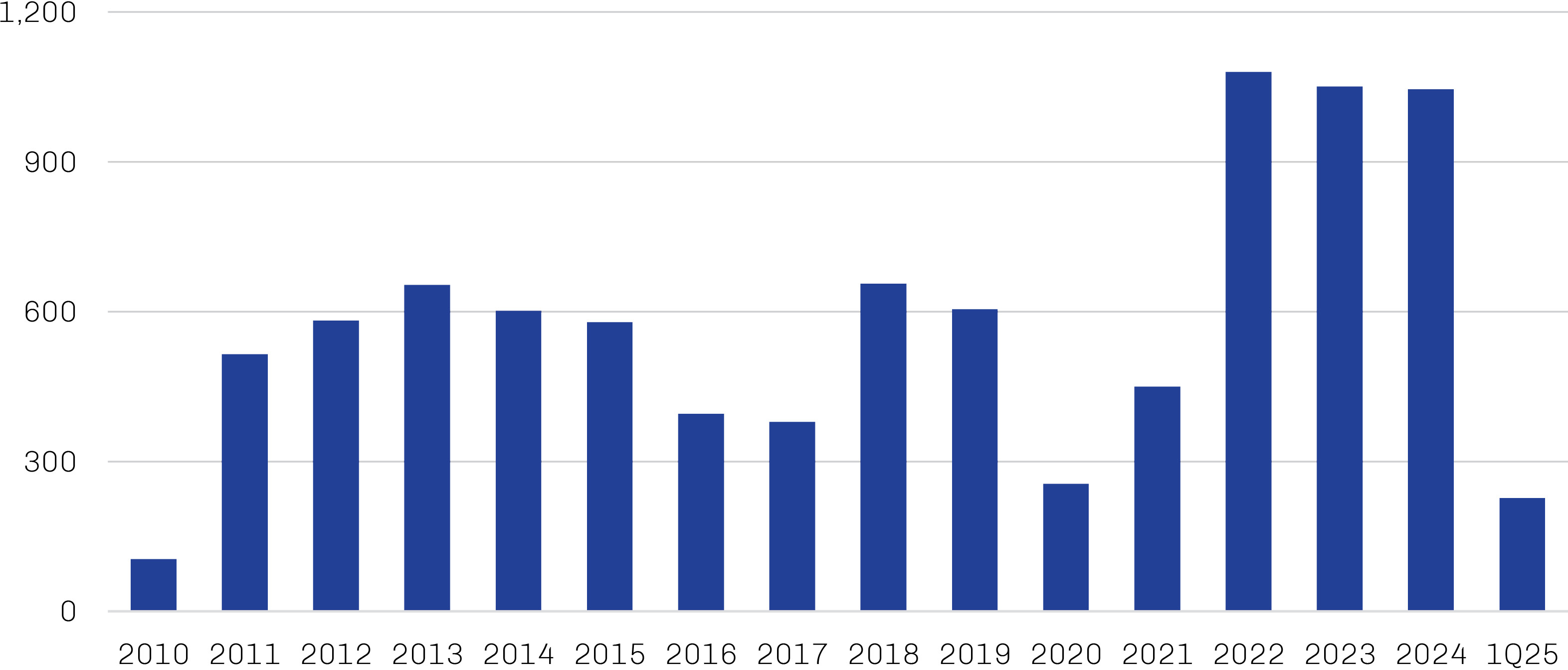

These issues may also be stoking the global central bank demand that has been a key source of support for the gold price over the past few years. Central banks purchased 1,045 tonnes of gold in 2024, making it three consecutive years of 1,000-tonneplus buying; purchases averaged only 481 tonnes annually between 2010 and 2021. This momentum has persisted into 2025 despite the high gold price, with authorities adding another 244 tonnes of gold in the first quarter. More recently, financial buyers have also gotten into the game. Physically backed gold exchange-traded funds ETFs—which capture investment demand from both institutional and individual investors—have seen three straight quarters of inflows after nine of outflows. First quarter 2025’s increase of 226 tonnes represented the largest quarterly inflow since Russia invaded Ukraine in first quarter 2022.5

Exhibit 5. Massive Central Bank Gold Buying Has Helped Buoy Prices

Central Bank Net Purchases in Tonnes, January 2010 through April 2025

Source: Metals Focus, Refinitiv GFMS, World Gold Council; data as of April 30, 2025.

Q: What are the ESG (environmental, social and governance) considerations of gold investment?

We view sustainability as a key element of a gold mining company’s long-term viability and ultimately its value to investors. To operate a mine effectively, miners may require not only formal approval from the governing bodies responsible for the jurisdiction in which the mine is located but also an informal “social license” from a variety of local stakeholders, including community members, employees and unions. These stakeholders stand to most directly benefit from—or to be most adversely impacted by—a miner’s practices during and after the mine’s productive life. We’ve observed that in order to obtain and maintain these social licenses, ethical miners may seek to demonstrate respect for the rights and needs of the local population and employees, protect the local environment during mining operations, and develop site-specific plans to mitigate environmental impacts upon the end of the mine’s productive life. High-quality governance is essential to nurturing these relationships.

A number of prominent miners have acknowledged the carbon intensity of their activities and have proactively sought—either singly or through organizations like the UN Global Compact, the World Gold Council or National Mining Association—to mitigate their footprint through new technologies and processes. In terms of issues related to climate change, the calculus around bullion ownership may be somewhat different than it is for miners, as the vast majority of gold in existence has already been mined and the emission intensity of storing it is low; as of end-2024, there were approximately 216,285 metric tons of gold above ground in one form or another, a volume that has compounded at an annual rate of less than 2% for more than a century.6 This was among the reasons that led the World Gold Council to conclude that an allocation to gold (or gold-backed investment products) may reduce a multi-asset portfolio’s carbon footprint, increase its alignment with climate-decarbonization pathways and reduce its vulnerability to climate-transition risks—all without adversely affecting the portfolio’s risk-return profile.7

Ultimately, gold investors need to make judgments on the opportunities and risks that ESG factors represent and how they align with their unique portfolio goals and guidelines. As with the evaluation of any intangible asset, we believe this is best done through analysis and reflection.