Macro & Market Views

Global Value Team Annual Letter

Global Value Team Annual Letter

The bulk of the year was dominated by the direction of growth stocks, particularly a small cohort of very large US companies exposed to secular trends in technologies like artificial intelligence; the so-called “Magnificent Seven” of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla returned anywhere from 50% to 235% in 2023 and comprised about 19% of the MSCI World Index as of year-end.2,3 Market performance broadened in the final months of the year, however, as the conventional wisdom appeared to coalesce around the perceived inevitability of not only a soft landing by the Federal Reserve but also a series of rate cuts in the year ahead. Government bond yields, biased higher through most of 2023, fell sharply in November and December, while measures of market volatility eased across asset classes.4

Though the broad success of risk assets in 2023 was a welcome respite from a dismal 2022, buoyant market conditions entering the new year make us wonder if hope has gotten the better of substance. In contrast with what the financial markets appear to be suggesting, we believe the investment environment is rife with challenges, the escalation of which could shake markets from their apparent complacency and inspire a newfound sense of risk aversion, to the detriment of many financial assets. To this end, we offer a series of reality checks.

Reality Check #1: Market Complacency Despite Uncertain Economic Landing

Financial market participants have spent the better part of two years considering a binary set of outcomes to the Fed’s tightening cycle and its potential impact on investment assets. The thought was we’d either have a “hard landing” in which the central bank’s efforts to tame inflation push the economy into recession, or a “soft landing” in which the pace of economic growth slows enough to bring inflation down to target levels but remains positive. Conditions entering 2024 suggest markets are complacent about the inevitability of the latter even as any sort of landing has remained elusive.

The longer the Fed circles the runway without touching down, in our view, the greater the risk of an adverse outcome. Maintaining current policy while waiting for inflation to shed those last few percentage points increases the possibility that the accumulated impact of higher interest rates will bring about a hard landing— likely solving the inflation problem but at the expense of recession and unemployment. If the Fed pivots to rate cuts before inflation fully recedes to its target level, on the other hand, pricing pressures could quickly reignite and require even higher policy rates to extinguish.

We have long been skeptical of the central bank’s ability to achieve a soft landing and remain so today. Beyond the scarcity of previous successful attempts, the continued strength of the domestic labor market makes it hard for us to envision a scenario in which wage growth spontaneously returns to a level consistent with target-level inflation—thought to be around 3.5%—absent a meaningful increase in unemployment.

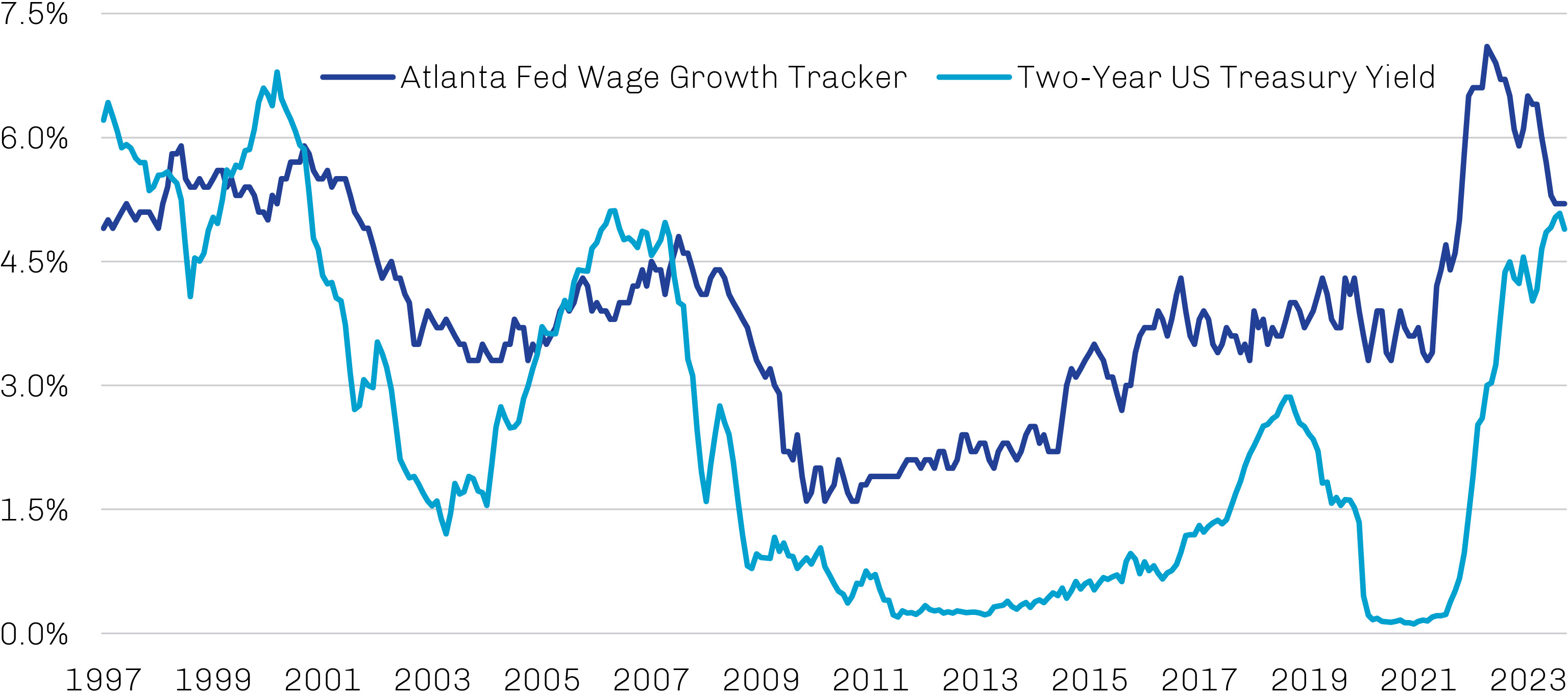

Broadly speaking, wage growth reflects two variables: the rate of change in nonfarm payrolls and their overall level. While the rate of payroll additions has moderated, the economy has continued to add jobs at a steady clip since bottoming in April 2020, and the level of payrolls as a percentage of the total population stands near a post-financial crisis high.5 Not surprisingly, wage growth has been less responsive to Fed tightening than the inflation rate; while core personal consumption expenditures (PCE) declined from 5.6% in March 2022 to 3.2% in its latest reading, wage growth (on a three-month rolling basis) fell from 6.0% to 5.2%.6 As shown in Exhibit 1, previous episodes of wage growth at or near current levels were reined in only when exceeded by two-year Treasury yields for a period of time. “Higher for longer”—and the economic slowing and job losses likely to accompany it—may be a necessity if the labor markets don’t soon begin to demonstrate some slack.

Exhibit 1. Interest Rates May Need to Remain Elevated to Pull Down Wage Growth

January 1997 through November 2023

Note: The Atlanta Fed’s Wage Growth Tracker is a three-month moving average of median wage growth based on hourly data.

Source: Bloomberg, Haver Analytics, Federal Reserve Bank of Atlanta; data as of November 30, 2023.

Reality Check #2: Political Risk in an Era of Fiscal Profligacy

Of greater long-term concern than economic cycles is the unsustainable fiscal course the US and many other economies have been on since the global financial crisis. To us, the swell of public debt outstanding in advanced economies combined with a general lack of fiscal discipline have made sovereign paper an increasingly risky proposition, one exacerbated by the regime change in interest rates and shrinking global liquidity.

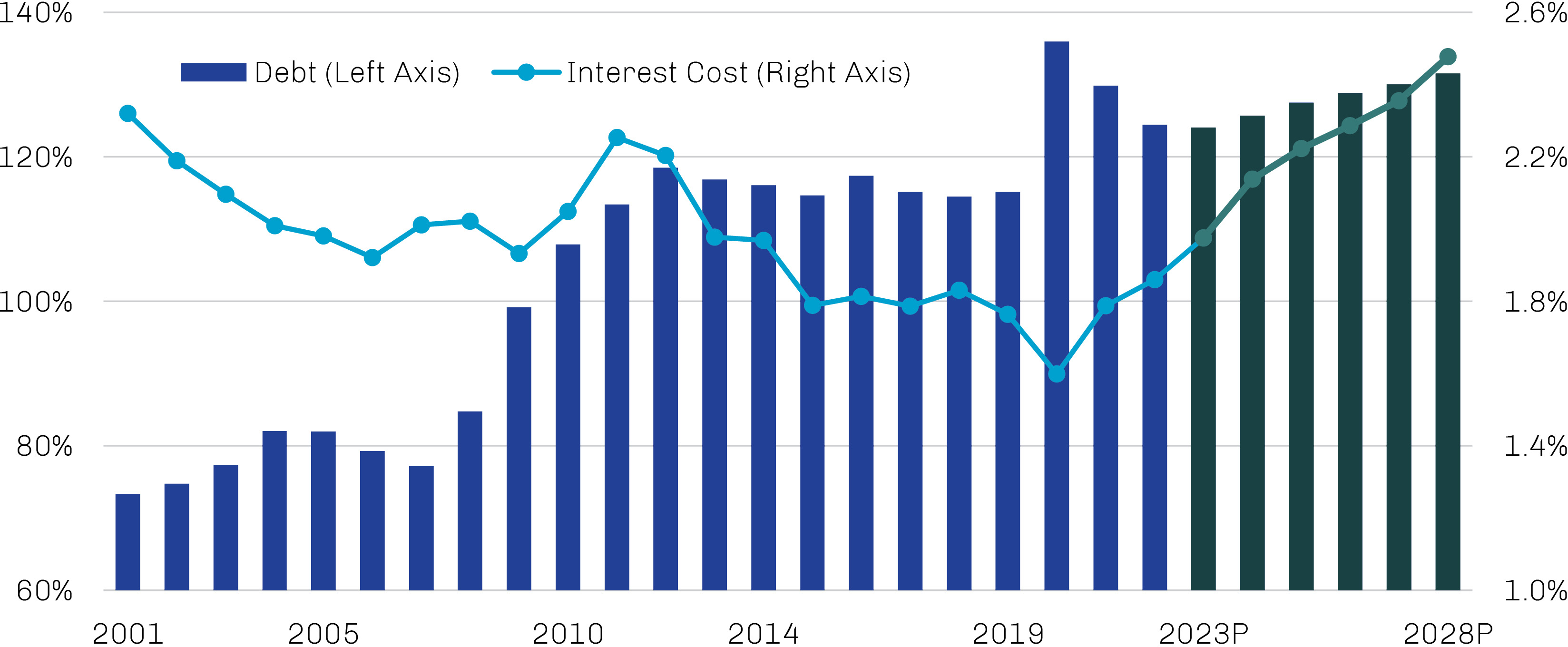

High and rising debt levels are less than ideal for an economy. In theory, high debt drives borrowing and debt-servicing costs higher, weighing on productivity and economic output, crowding out private-sector investment, undermining sovereign creditworthiness and credibility, and potentially limiting policy optionality in the event of future crises. In practice, however, financial repression via unconventional monetary policies through much of this century kept interest rates artificially low and tempered interest expenses even as debt balances continued to rise, blunting any motivation for lawmakers to make the unpopular choices necessary to clean up their fiscal houses. As shown in Exhibit 2, while the debt of the US, UK, euro zone and Japan in aggregate rose from less than 80% of GDP in 2007 to peak above 135% in 2020, the cost of servicing this debt declined steadily from 2011 until 2020. This trend in interest expense has since reversed direction and is forecast to continue rising.

Exhibit 2. Low Rates Kept Interest Costs in Check Even as Debt Levels Rose Sharply

As a Percentage of GDP for the US, UK, Euro Zone and Japan in Aggregate, 2001 through 2028

Note: Data for 2023–28 are projections.

Source: Haver Analytics, International Monetary Fund, First Eagle Investments; data as of July 31, 2023.

While the ongoing rollback of crisis-era monetary accommodations continues to alter the calculus of government borrowing, there are few indications that fiscal policy will be adjusted to reflect the new math anytime soon. Throughout the world, the “big state” continues to make evident its willingness to spend, from Bidenomics in the US and the state-sponsored energy transition in Europe to Saudi Arabia’s attempts at “sportswashing” and Russia’s imperialistic ambitions in Ukraine. We’d also include in this category military spending, which increased globally by 3.7% in real terms in 2022 to establish a new record high of $2.24 trillion, due in no small part to the elevated geopolitical tensions we discuss in reality check #3 on page 5.7

Loose government spending and aging demographics are a poor recipe for sustainable fiscal policy, and the US is a particularly acute example of the perils involved. From the end of World War II through the late 1990s, the country maintained a more or less balanced primary budget (i.e., the fiscal balance excluding interest payments), but the trend has been structurally negative since. The deficit’s current magnitude is particularly troubling given the health of the labor market; the last time unemployment was this low, in the late 1990s, the US ran a budget surplus. And it’s expected to get worse from here, as expenditures—driven by growth in mandatory spending on entitlement programs like Social Security and Medicare, as well as higher net interest outlays—are forecast to outpace revenues, resulting in persistent annual deficits and deepening federal debt.

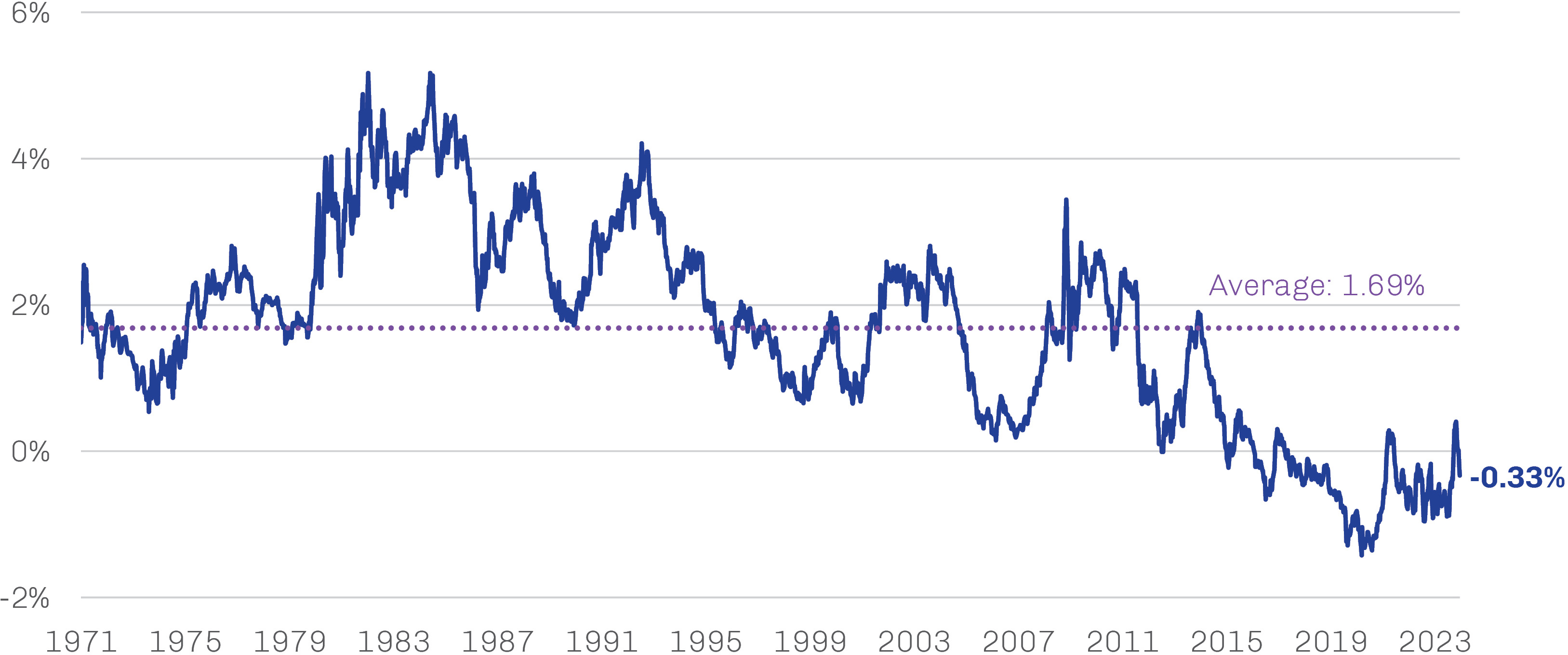

Despite widespread concerns about debt levels and few indications that meaningful fiscal consolidation is on the horizon, the term premium8 on US Treasuries trended lower following the global financial crisis and spent much of the past five-plus years in negative territory, as shown in Exhibit 3. The lack of a persistently positive term premium suggests markets may not agree with our assessment of the risks—or, at the very least, they have grown complacent amid the many potential triggers for a re-rating of US Treasuries.

Exhibit 3. Treasury Term Premium Has Been Negative for Most of the Past Five-Plus Years

10-Year US Treasury Term Premium, August 1971 through December 2023

Source: Federal Reserve Bank of New York, Federal Reserve Board; data as of December 31, 2023.

Given the apparent lack of political will to enact the spectrum of measures necessary to improve the fiscal dynamics—including tax hikes, entitlement reform and cuts to discretionary spending, as well as supply-side reforms to promote productivity growth—it’s hard to see a roadmap to lasting improvement. Keeping the fiscal settings wide open, on the other hand, increases the near-term risk of re-emerging inflation or stagflation. And while we can’t speculate about what may finally cause investors to demand meaningful premia for the uncertain fiscal trajectory of sovereign issuers, we note that changes in sentiment can happen quickly and reverberate broadly across markets.

Realty Check #3: Geopolitical Risk as Globalization Wanes

Macroeconomic risks have been further complicated by the emergence of new geopolitical theaters of uncertainty. Globalization trends of the late twentieth/early twenty-first centuries were expected to advance the widespread adoption of capitalistic liberal democracy models that promoted economic, political and personal liberties, but recent years have been marked by a hardening of governing philosophies often inconsistent with these ideals.

This has included a loose coalition of autocratic countries like China, Russia, North Korea and Iran that, not inconsequentially, control a vast, near-contiguous swath of land rich withnatural resources across Eurasia and into the Middle East and northern Africa. In recent years, this group has increased the volume and scope of its military adventurism, both directly and via proxies, and appears to have forged tighter relations as a result of a shared distaste for the liberal democracies scattered across the globe’s periphery (North and South America, Western Europe, Oceana and parts of East Asia).

At a minimum, these new alliances set the stage for greater friction in economic relations, and there are many ways in which current localized armed conflicts such as Ukraine/Russia and Israel/Hamas could escalate into something more far-reaching. As we noted at the time of Russia’s invasion of Ukraine, war is among the conditions that moves us out of the comfort zone of quantifiable risk and into the domain of uncertainty. In his fifth century BC book The History of the Peloponnesian War, Thucydides noted that “For war of all things proceeds least upon definite rules.”

Meanwhile, China’s reputed intentions in Taiwan remain vexing to diplomats and investors alike, and deteriorating relations with the West have combined with sluggish domestic economic growth, regulatory hurdles and other concerns to drive significant outflows from China’s capital markets.9 The MSCI China Index fell more than 9% in 2023 and has delivered an annualized decline in excess of 16% over the past three years.10 There is a case to be made for measured participation in select Chinese stocks given current depressed valuations, however, and some sort of geopolitical thaw or macro policy change could help drive a re-rating of the market.

Adding to the general uncertainty, federal elections loom in 2024 for more than 70 countries accounting for more than half the world’s population.11 If recent history is any guide, volatility is the likely winner here.

Ballast Amid an Agglomeration of Risks

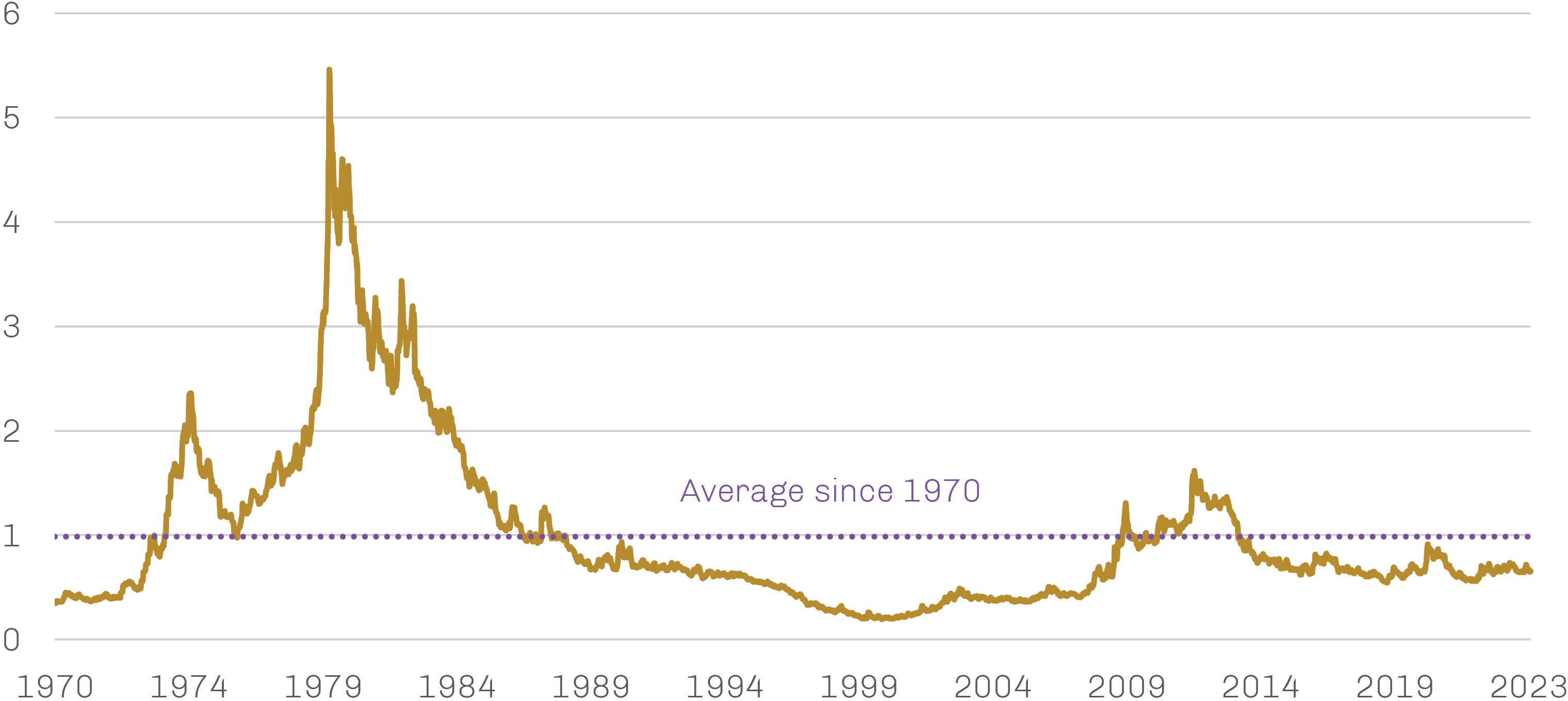

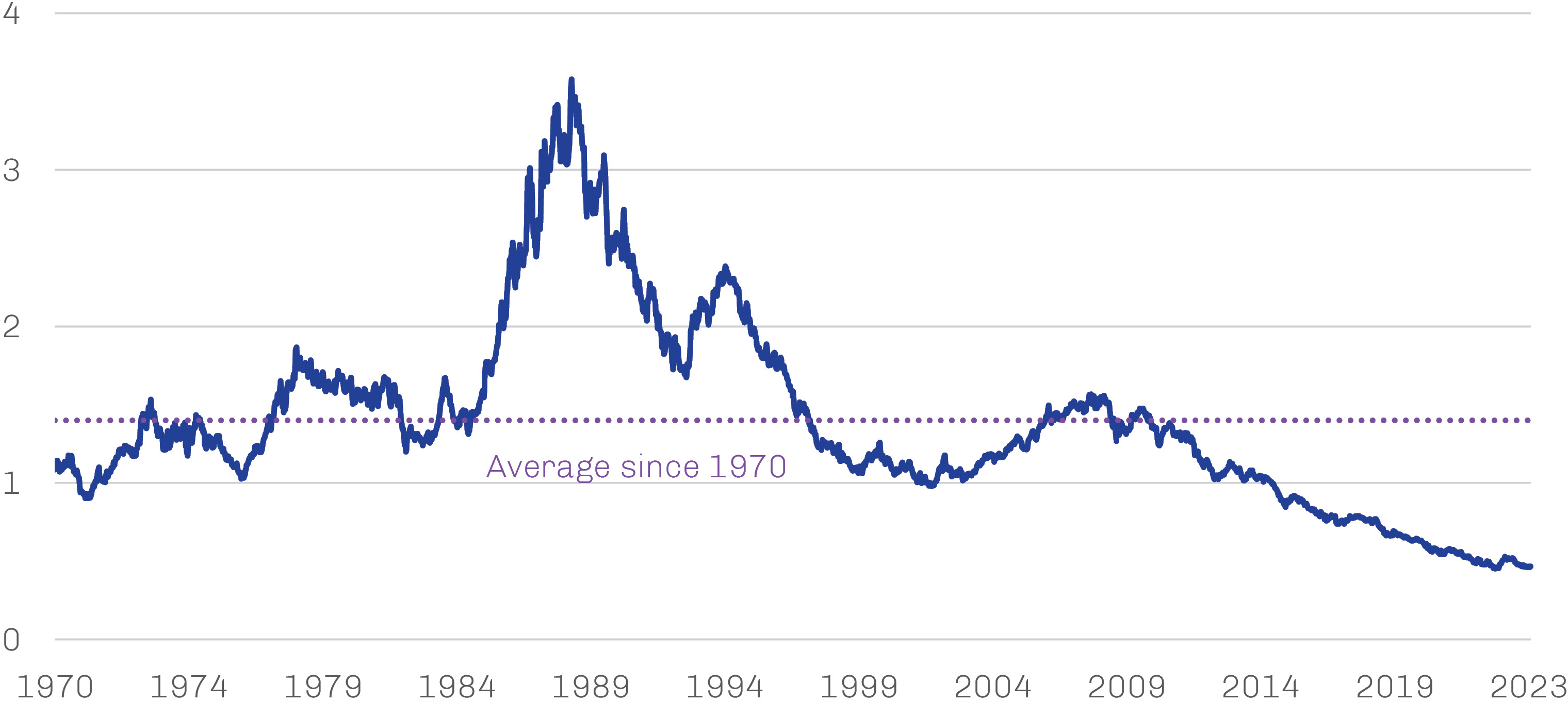

It’s possible the risks laid out above were among the factors that provided support for the price of gold amid sharply rising real interest rates. Gold’s inverse relationship with real interest rates—i.e., the difference between the nominal interest rate and the expected rate of inflation—historically has been the most important driver of its price movements. Though it sold off considerably at the onset of Fed rate hikes in March 2022, the gold price rallied to a new nominal record high by year-end 2023 even as the real interest rate (based on the yield of 10-year Treasury inflation-protected securities) spiked more than 250 basis points over this period.12 As shown in Exhibit 4, however, gold continues to trade at a historical discount relative to equities.

Exhibit 4. Despite Rally, Gold Remains Undervalued Relative to Equities

Ratio of Gold Spot Price to MSCI World Index, January 1970 through December 2023

Source: Bloomberg, First Eagle Investments; data as of December 31, 2023.

To us, gold’s resilience in the face of such a large move in real rates suggests the presence of other influences. The sovereign debt issues we cited earlier, for example, may have prompted increased interest in an asset like gold with a track record as a potential hedge against currency debasement. Increasing geopolitical tensions appear to have bolstered gold demand from central banks; central bank gold purchases in 2022 were the highest on record, and year-to-date 2023 trends imply another robust year.13 And the most visible manifestations of these geopolitical tensions—like the protracted war between Ukraine and Russia and the October outbreak of violence between Israel and Hamas—support the appeal of gold for investors seeking perceived “safe havens” in uncertain times.

To this last point, we would note that oil, despite its cyclicality, may also serve as a potential hedge against geopolitical strife. As we’ve seen over the past two years, this is especially true when important sources of supply like Russia and the Middle East are involved, and energy security becomes a critical issue for governments worldwide.

Turning to the Classics

For those of you familiar with the Global Value team, it probably comes as little surprise that we looked to our library for inspiration in this challenging landscape. As we often do, we landed upon Ben Graham’s The Intelligent Investor, first published in 1949. (Interestingly, but hopefully not prophetically, a revised edition of The Intelligent Investor was published in 1973, the dawn of a period of high capital costs, economic stagflation and military unrest in the Middle East.)

In his book, Graham—upon whose research the entire concept of value investing is rooted—seeks to decouple stock investing from price forecasting, positing that there are two possible ways by which an investor may seek to profit from the wide price fluctuations typical of common stocks: “…the way of timing and the way of pricing. By timing, we mean the endeavor to anticipate the action of the stock market to buy or hold when the future course is deemed to be upwards. By pricing, we mean the endeavor to buy stocks when they’re quoted below their fair value and to sell them when they rise above such value.” While he characterizes efforts at the former to be “absurd,” the “margin of safety” offered by the latter relieves the investor from the burden of providing an accurate estimate of the future.14

We agree. We spend the majority of our time trying to identify quality, durable businesses trading at Graham’s “margin of safety,” seeking situations that appear to offer the prospect of both security of principal and adequate returns. While we look for these opportunities from the bottom up, a top-down view can provide useful context. From this perspective, both value stocks and non-US stocks are trading at historically cheap valuations. As shown in Exhibit 5, the Russell 1000 Value Index is about as cheap relative to its growth counterpart as it has been in many decades. Most of the difference in relative valuation is attributable to multiple expansion, as the Russell 1000 Growth Index has outgrown the Value Index by only about 2% per annum on a revenue basis. Similarly, the MSCI EAFE Index is trading at a 50-year-plus low relative to the S&P 500 Index, as depicted in Exhibit 6. While conclusions drawn from index-level metrics can sometimes be misleading, these images highlight the opportunities that may be available in value and non-US stocks, and the potential to benefit from any sort of mean reversion.

Exhibit 5. Growth Stocks Appear Stretched Relative to Value…

Price Ratio of Russell 1000 Value Index to Russell 1000 Growth Index, January 1979 through December 2023

Source: Bloomberg; data as of December 31, 2023.

Source: Bloomberg; data as of December 31, 2023.

Exhibit 6.…As Do US Stocks Relative to Non-US Stocks

Price Ratio of MSCI EAFE Index to S&P 500 Index, January 1979 through December 2023

Source: Bloomberg; data as of December 31, 2023.

The spread between current and historical valuations also may suggest that the old-economy businesses commonly associated with value indexes are pricing in a more sluggish economic reality than what is implied by valuations in the new-economy-biased growth universe. Ironically, it’s possible this old-economy discount could serve as a potential shield against adverse developments while also promoting valuation elasticity to more positive economic outcomes.

Prepared for Less Than Perfect

Though financial markets generally appear unconcerned with the challenges we see heading into the new year, we believe it’s quite possible that risk aversion will at some point be higher than it is today. Though we wouldn’t hazard a guess as to when that may be, owning quality businesses with track records of consistent cash flow generation and wise capital allocation may be the least-bad option in a less-than-perfect world. Note that while we maintain our valuation sensitivity, our philosophy of value investing does not automatically preclude us from owning assets in growing segments of the market; indeed, we hold a range of stocks in areas like tech and healthcare that are exposed to secular tailwinds, but only those trading at what we believe are reasonable multiples of cash flow rather than conceptual multiples of revenues.

While even high-quality companies are unlikely to avoid losses in the event of worst-case scenarios—if the Fed’s landing proves far rougher than currently implied by equity markets, or if the fiscal challenges facing developed nations metastasize into a crisis, or if geopolitical tensions conflagrate beyond regional conflicts— they should prove resilient and potentially be well positioned to outperform once crisis recedes. Meanwhile, durable companies should also comport themselves well through less-extreme outcomes like sluggish growth or stagflation.