Macro & Market Views

Global Value Team Annual Letter

Global Value Team Annual Letter

As in 2023, diversification failed to matter in 2024.

For two years now, those seeking outsized equity gains likely would have been best served by focusing their investment on the most concentrated, highest-growth segment of the world’s largest stock market; that is, tech-oriented US stocks. As proxied by the “Magnificent Seven,” this cohort advanced 67% in 2024 to help fuel a 25% gain in the S&P 500 Index. The S&P 500’s gain excluding these seven stocks, which accounted for more than one-third of the index’s total market capitalization at year-end, amounted to a far more pedestrian 16%. The MSCI World Index’s 19% return was similarly bolstered by the outperformance of these megacap names.1,2

But when we decompose the factors driving the one-dimensional equity market performance of recent years, it’s not difficult to arrive at a mindset in which diversification regains its reputation as a potential driver of attractive long-term risk-adjusted returns and an essential element of a well-balanced investment portfolio.

Most notable to us has been the pronounced post-pandemic decoupling of the US and China, whose symbiotic relationship represented a primary driver of global macroeconomic activity and financial markets performance for much of the past several decades. In fact, economic historians Niall Ferguson and Moritz Schularick in 2007 coined the term “Chimerica” to describe the interconnectivity of the world’s most rapidly growing emerging market (at the time) and its dominant economic power (still).

The US was happy to buy the competitively priced products mass produced in China, China was happy to lend the resulting trade surplus back to the US through the purchase of Treasuries, and the world’s benchmark interest rate was kept in check.3 But like so many celebrity portmanteaus, Chimerica may not have been built to last.

In contrast, risk perception in China has been high, and for good reason. While China managed to avoid the early-2020s inflation spike that bedeviled the majority of the world, its economy has faced its own set of complications, some self-inflicted. China’s aggressive zero-Covid policy—begun in early 2020 and maintained until the end of 2022, long after most nations had significantly reduced or eliminated pandemic-related restrictions—resulted in an uneven recovery that stymied private investment and household spending. An ideologically driven crackdown on the rapidly expanding domestic tech industry, launched in late 2020, hamstrung what had been among the most dynamic sectors of China’s economy and in the process wiped out trillions of dollars in market capitalization and cost countless jobs.4 The debt-fueled bubble in China’s property market—which once accounted for about 25% of the country’s gross domestic product (GDP)—burst with the default of developer Evergrande in 2021, and it continues its structural and cyclical reset to a lower base.5

As a result of these and other factors, China’s animal spirits have all but been put out to pasture; the MSCI China Index finished 2024 down more than 50% from its early-2021 peak, while yields on 10-year government bonds fell to all-time lows.6 Certain other countries in China’s orbit have been similarly afflicted.

Good News for People Who Love Bad News

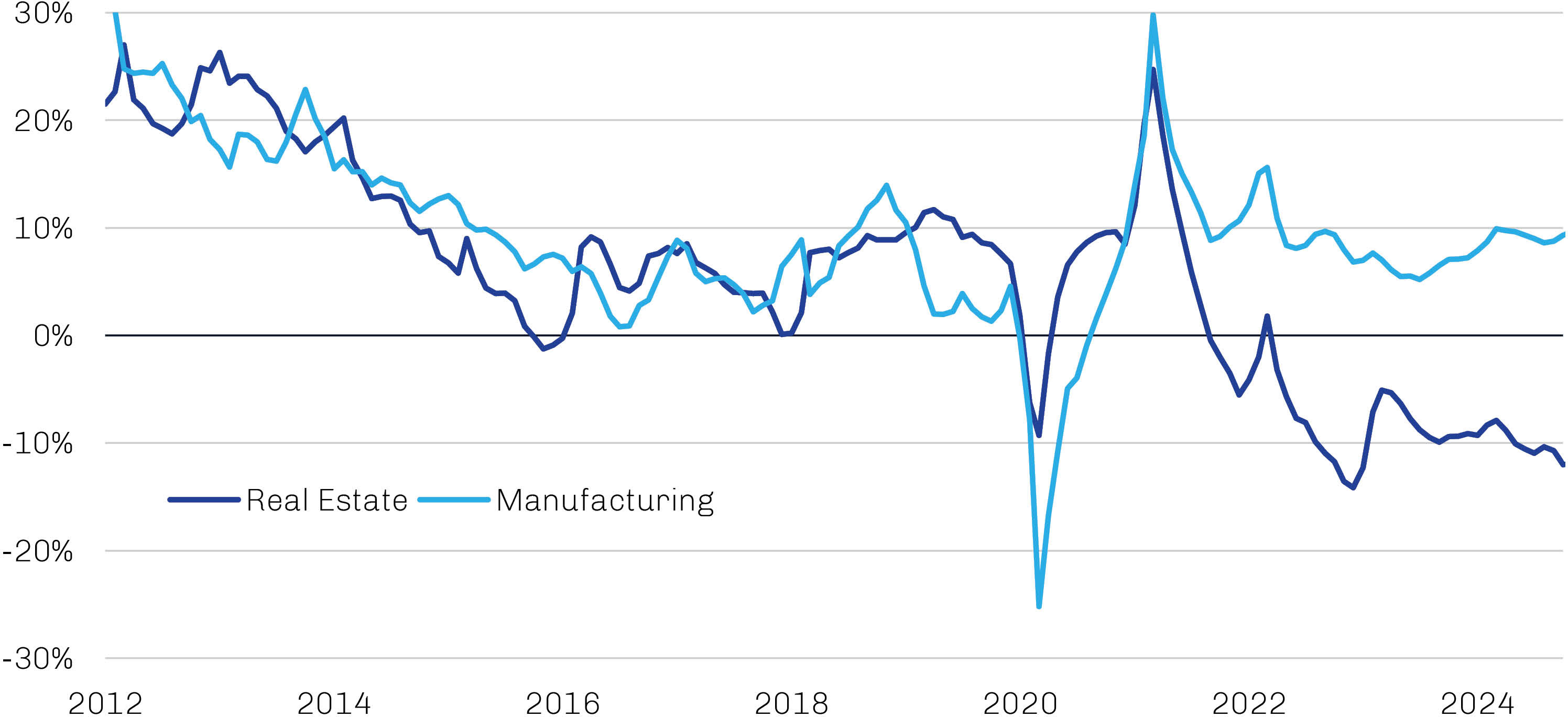

In the past, signs of strain in the Chinese economy were typically viewed as bad news for global activity broadly, and risk assets responded accordingly. This time around, however, the effects of China’s malaise have been more nuanced. China’s property market collapse, for example, is at least partly responsible for the cyclically moderating inflation pressures in the US and many other countries. As shown in Exhibit 1, fixed-asset investment in China has shifted away from real estate and toward manufacturing, and the resulting excess capacity has weighed on export prices and provided China’s trading partners with a strong disinflationary impulse. Meanwhile, waning confidence among Chinese businesses and households has depressed imports and caused a range of economically sensitive commodities—everything from oil to copper to wheat—to derate versus gold, which has been another exogenous source of downward pressure on global inflation.

Exhibit 1. China’s Re-Emphasis on Manufacturing Has Served as a Disinflationary Impulse Globally

Year-over-Year Percent Change in China Fixed-Asset Investment, Three-Month Moving Average; January 2012 through September 2024

Source: UBS, First Eagle Investments; data as of September 30, 2024.

More recently, however, there are signs that the tides may be changing. With unrelentingly downbeat economic data appearing to disabuse them of any notion that their growth targets remained obtainable without intervention, China’s policymakers late in the year announced a series of stimulus measures to combat deflationary pressures, stabilize housing and rebuild market optimism. In September, the People’s Bank of China (PBOC) cut the reserve requirement ratio for banks and its benchmark short-term reverse repo rate, while instructing commercial banks to trim rates on outstanding mortgages and introducing new liquidity mechanisms to support equity markets.7 Though authorities hinted that significant fiscal support was also on tap, the initial package announced soon after the November US elections was underwhelming in size and scope—$1.4 trillion in local government bond issuance to refinance maturing and higher-yielding local government debt rather than injected directly into the economy. However, it stands to reason that Beijing may look to keep some of its powder dry until it has better visibility on potential tariffs from the incoming Trump administration.8

The US may find itself vulnerable to a reversal of China’s fortunes, in our view, as its battle against inflation to date has reached only a fragile peace. Our concerns are underpinned by the behavior of the US labor market throughout the Federal Reserve’s tightening cycle. As shown in Exhibit 2, the labor market—unusually—softened during this period even as payrolls continued to grow, suggesting that the increase in the unemployment rate from its cyclical low of 3.4% to 4.1% by year-end 2024 was driven by increased participation rates. One theory for this phenomenon is that the massive increase in public debt outstanding post-Covid led to a nominal rebasing of the US economy that bolstered corporate profits in the face of contracting margins and supported a moderation in payroll growth rather than an outright decline. With financial conditions having since loosened, both corporate profits and profit margins have inflected higher in nominal terms, and it’s reasonable to think that payrolls and wage growth may follow suit should this trend continue. Though down from its peak of 6.7%, wage inflation of 4.3% remains inconsistent with the Fed’s 2% inflation goal, and this stickiness is likely among the reasons why consumer price index prints have stubbornly persisted above target even as other components have retreated.9

Exhibit 2. US Payrolls Continued to Expand Even as the Unemployment Rate Increased

January 2022 through November 2024

Source: US Bureau of Labor Statistics, Federal Reserve Board of St. Louis; data as of December 9, 2024.

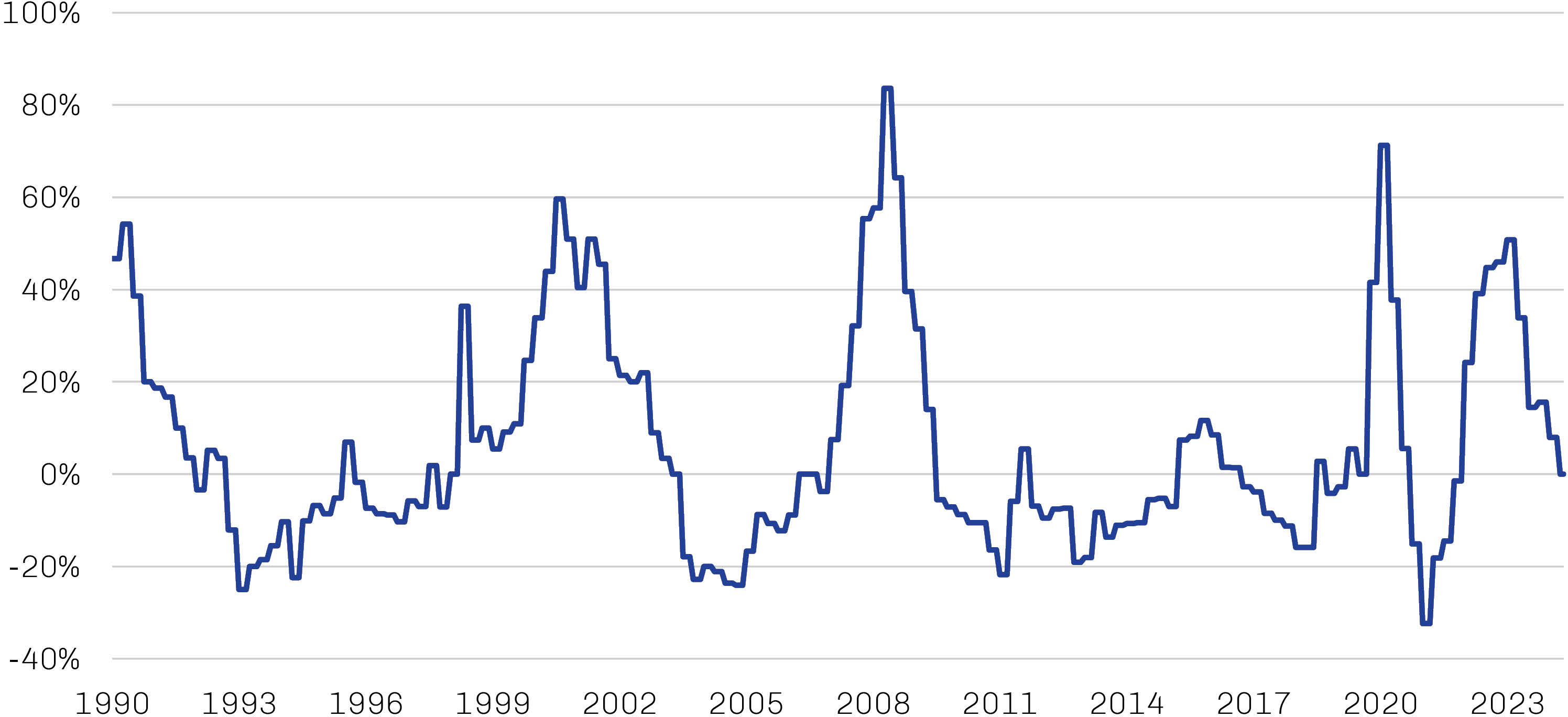

Easing monetary policy presents another potential source of inflationary pressure. With the inflation rate well off its cyclical peak, the Fed in September began to recalibrate its settings, kicking off a much-anticipated rate-cut cycle with a 50 basis point reduction. The Fed followed up that move with two additional 25 basis point cuts in November and December to bring its key policy rate to 4.25–4.50% by year-end, and the latest summary of economic projections suggest an additional 50 basis points of cuts are coming in 2025.10 In response to easier policy, bank lending standards have gone from tight to neutral (as shown in Exhibit 3) and credit spreads have retreated. With market valuations high and earnings expectations buoyant, a Fed shift back to a hawkish policy bias sooner than expected could prompt investors to recalibrate their risk appetites and herald an untimely end to the US Goldilocks tale.

Exhibit 3. More Accommodative US Banks Highlight Easing Financial Conditions

Net Percentage of Domestic Banks Tightening Standards for Commercial and Industrial Loans to Large and Middle Market Firms, January 1990 through November 2024

Source: Bloomberg; data as of November 30, 2024.

From Politicking to Policymaking

Though the US and China may be decoupling economically, their mutual affection for public debt persists, and their large and growing debt loads—not unique to them by any means—reflect long-term risks to stability even as they support near-term growth. Unrestrained government debt globally has raised the specter of currency debasement and other adverse financial outcomes, and the longer fiscal imbalances go unaddressed, in our view, the more difficult they will be to unwind.

In the US, the federal fiscal deficit expanded again in fiscal 2024 (ended September) to 6.4% of GDP and has only worsened since, coming in at 7.1% for the last 12 months through November; the 50-year average is 3.8%.¹¹ While the policy specifics moving forward are uncertain given January’s leadership changes, higher deficits and debt levels seem likely under the incoming Trump administration (as they would have with a Harris victory).¹²

The Tax Cuts and Jobs Act of 2017, which will see many of its provisions for individual taxpayers expire at year-end 2025 absent Congressional action, is likely to take fiscal center stage next year. A unified Republican government suggests a high possibility that the Trump administration’s key tax priorities will be extended, but the means by which that lost revenue will be offset remain uncertain. A reduction of regulatory hurdles impairing business activity seems likely to promote investment and economic growth. Some in the administration—including Scott Bessent, Trump’s pick to run Treasury—have argued that tariffs “can increase revenue to the Treasury” if used strategically.¹³ But the Congressional Budget Office’s review of tariff increases in 2018–19 found that the initial boost in customs revenues soon declined as imports slowed and were sourced from countries subject to lower duties.14

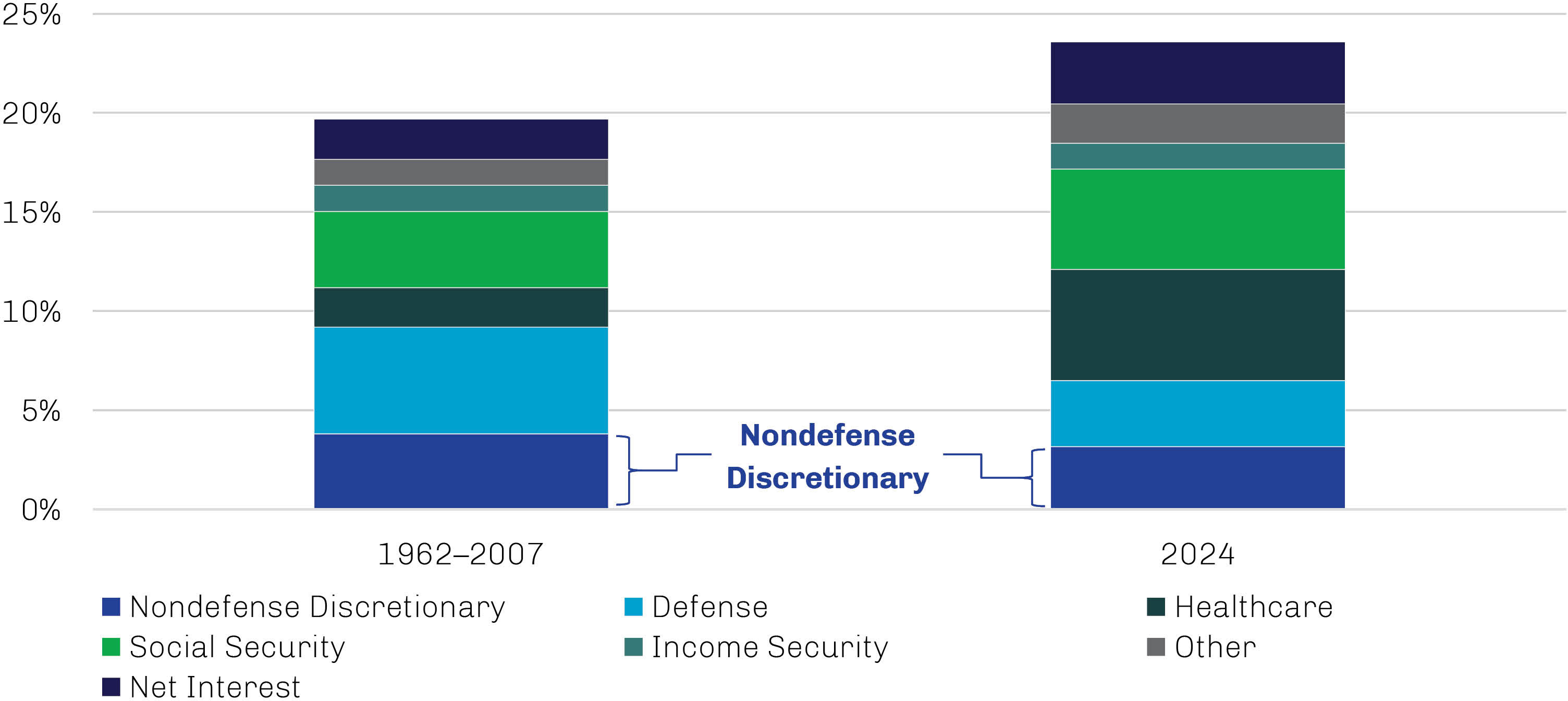

Spending cuts are another avenue to reducing the deficit, and Trump tapped Elon Musk and Vivek Ramaswamy to take on the challenge as co-heads of the Department of Government Efficiency (DOGE). While there is certainly room to cut federal spending and eliminate wastefulness, public discussion has been focused mostly on nondefense discretionary spending, which accounts for only about 15% of total federal outlays and has actually decreased slightly as a percentage of GDP in recent years, as shown in Exhibit 4. Any attempt to meaningfully move the needle on the country’s debt burden likely would require reforms to popular—and seemingly sacrosanct—entitlements like Social Security, Medicare and Medicaid. Mustering the necessary political will for changes to programs so broadly popular with voters seems like an insurmountable challenge. While there is also talk of slashing the government’s workforce of 2.3 million civilians located across all 50 states, their aggregate salary amounts to less than 1.5% of GDP.15

Exhibit 4. Nondefense Discretionary Spending Offers US Legislators Limited Savings Opportunities

Federal Spending by Category as a Percentage of GDP

Source: US Department of the Treasury, US Bureau of Economic Analysis; data as of November 30, 2024.