Commentaries

Global Equity ETF Commentary

Global Equity ETF Commentary

Portfolio Review

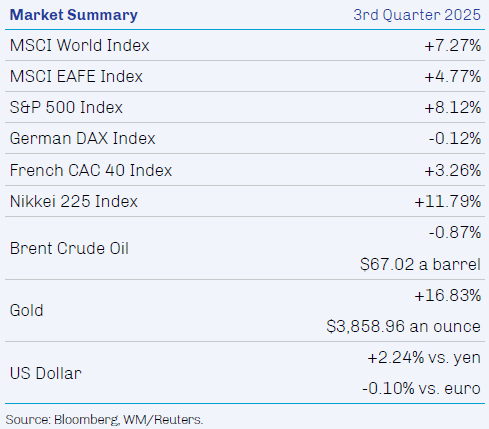

Global Equity ETF posted a return of 1.80% in third quarter 2025. All regions contributed to performance; North America and emerging markets were the leading contributors while Japan and developed Asian excluding Japan lagged. Materials and industrials were the largest contributors among equity sectors, while consumer staples detracted and real estate was flattish. The Global Equity ETF outperformed the MSCI World Index in the period.

Leading contributors in the First Eagle Global Equity ETF this quarter included Oracle Corporation, Alphabet Inc. Class C, Samsung Electronics Co Ltd Pfd Non-Voting, Barrick Mining Corporation and Newmont Corporation.

Oracle is one of the world’s largest independent enterprise software companies. The company reported a large increase in backlogs during the quarter, including a substantial, five-year cloud-computing contract with OpenAI. In addition to a significant near-term lift to Oracle’s top line from this contract, we expect margins on these revenues to expand over time.

Shares of Alphabet, the parent company of Google and YouTube, were strong during the quarter as the Department of Justice delivered favorable rulings on embedding Chrome as the default browser on phones and retaining the company’s current corporate structure with no need to divest divisions. Beyond its core ad and search businesses, Alphabet provides a full stack solution within AI: spanning research, infrastructure/data centers and integrated end products. Valuation remains reasonable, in our view, and the company continues to share its ample store of cash with investors through dividends and buybacks.

Samsung Electronics is a global technology company with leadership positions in smartphones, televisions and semiconductor memory, and is a major manufacturer of electronic components including lithium-ion batteries, semiconductors, image sensors, camera modules and displays. Shares rallied during the quarter on continued strong dynamic random-access memory (DRAM) pricing due to tight supply and surging demand for AI-driven cloud-infrastructure builds. After the quarter’s end, Samsung announced a partnership with Nvidia to supply DRAM chips for its next-generation products.

Canada’s Barrick Gold is the world’s second-largest gold producer. For its most recent quarter, Barrick reported operating and financial results in line with expectations as well as strong cost containment and a transition to a net-cash position. It also announced a significant, low-cost, gold find at its Fourmile field in Nevada. Within the context of strong results and the sizable Nevada discovery, investors were unfazed by the unexpected departure of the company’s CEO.

Newmont is one of the world’s largest gold miners and a major producer of silver. Newmont continued to deliver into both cost and production guidance during the quarter—undiminished by usual seasonality—resulting in record free cash flow generation. As part of its portfolio rationalization plan, Newmont monetized stakes in Greatland Resources and Discovery Silver in June and July, respectively, and sold its stake in Orla Mining in September; proceeds were applied to reducing debt and buying back shares. Meanwhile, investors appeared to take changes to Newmont’s executive suite—including both the unanticipated resignation of its CFO in July and the announcement of long-anticipated succession plans for its CEO—in stride.

The leading detractors in the quarter were Elevance Health, Inc., Philip Morris International Inc., Shimano Inc., Comcast Corporation Class A and Salesforce.com, Inc.

Shares of Elevance Health, the health insurer and healthcare-services provider formerly known as Anthem, traded lower on concerns about reductions in Medicaid coverage and increased utilization of services. The company reported a decline in earnings for its most recent quarter and reduced its forward guidance. We believe that margins will eventually stabilize as higher premiums cycle through its customer base. We continue to view Elevance as a well-managed company positioned to benefit from long-term secular demand for its managed care services in the US.

Tobacco company Philip Morris reported better-than-expected earnings for its most recent quarter, but slightly soft sales weighed on the stock. The company attributed the sales weakness to supply issues in Indonesia and Turkey due to regulatory changes. However, its noncombustible products continue to lead growth. We remain constructive on this cash flow-generative business and are pleased with Philip Morris’s commitment to returning cash to shareholders through reliable dividends and stock repurchases.

Japan’s Shimano, which manufacturers bicycle parts, fishing components and rowing equipment, lowered its forward guidance during the quarter because of weakness in overseas markets and ongoing inventory adjustments. Our investment thesis remains intact, as we are confident that Shimano can work through accumulated inventories after the strong but unsustainable demand for its products during the Covid-19 era. In addition to high-quality products and dominant global market share, the company has a strong history of returning capital to investors.

Comcast is the largest multinational telecommunications and media conglomerate in the US, with brands including Xfinity cable, NBCUniversal (theme parks and TV stations with Peacock streaming service) and UK-based pay-TV company Sky. The company reported better-than-expected results for its most recent quarter, but shares traded lower due to ongoing declines in broadband subscribers. Our investment thesis remains intact, as we believe Comcast has the scale, density and cost advantages to outperform both fixed wireless and other fiber internet providers over the long term. Meanwhile, the other parts of the business have been performing well, and Comcast continues to generate strong cash flows and return capital to shareholders through both dividends and share buybacks.

Shares of enterprise software developer Salesforce traded down after the company provided lower-than-expected forward sales guidance during its most recent earnings release. This prompted concerns about the company’s transformation from a software-as-a-service (SaaS) business to an AI-powered enterprise business (its Agentforce platform) and an overall slowdown in revenue growth. We believe that Salesforce is well positioned to grow and scale Agentforce over time, and we continue to like its operational strength, market dominance and focus on balancing growth with improving profitability.

We appreciate your confidence and thank you for your support.

Sincerely,

First Eagle Investments

1. Source: FactSet; data as of September 30, 2025.

2. Source: Bloomberg; data as of September 30, 2025.

3. Source: CME FedWatch; data as of October 10, 2025.

4. Source: Reuters; data as of March 21, 2025.

5. Source: NATO; data as of June 27, 2025.

6. Source: Bloomberg; data as of April 16, 2025.

7. Source: Bloomberg; data as of October 4, 2025.

8. Source: YCharts; data as of September 30, 2025.

9. Source: FactSet; data as of October 10, 2025.

10. Source: Bloomberg; data as of September 30, 2025.

11. Source: Bloomberg; data as of September 30, 2025.

12. Source: Bloomberg; data as of October 9, 2025.

The performance data quoted herein represent past performance and do not guarantee future results. Market volatility can dramatically impact the Fund’s short-term performance. Current performance may be lower or higher than figures shown. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month-end are available at www.firsteagle.com.

1. Average annual returns are historical and reflect changes in share price, reinvested dividends and are net of expenses. Operating expenses reflect the Fund’s total annual operating expenses for the share class as of the Fund’s most current prospectus, including management fees and other expenses.

First Eagle Investment Management, LLC (the “Adviser”) has contractually agreed to waive and/or reimburse certain fees and expenses so that the total annual fund operating expenses (excluding Acquired Fund Fees and Expenses (“AFFE”), brokerage commissions, extraordinary items, interest or taxes) (“annual operating expenses”) is limited to 0.50% of the Fund’s average daily net assets. These contractual limitations are in effect until 31-Dec-2025, and may not be terminated prior to that date without the approval of the Board of Trustees (the “Board”) of The RBB Fund Trust (the“Trust”).

Investments are not FDIC insured or bank guaranteed and may lose value.

Risk Disclosures

All investments involve the risk of loss of principal.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

There are risks associated with investing in securities of foreign countries, such as erratic market conditions, economic and political instability and fluctuations in currency exchange rates. These risks may be more pronounced with respect to investments in emerging markets. ETFs are subject to additional risks that do not apply to conventional mutual funds, including the risks that the market price of an ETF’s shares may trade at a premium or discount to its net asset value, an active secondary trading market may not develop or be maintained, or trading may be halted by the exchange in which they trade, which may impact an ETF’s ability to sell its shares. Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns. Investment in gold and gold-related investments present certain risks, and returns on gold related investments have traditionally been more volatile than investments in broader equity or debt markets. A principal risk of investing in value stocks is that the price of the security may not approach its anticipated value or may decline in value. “Value” investments, as a category, or entire industries or sectors associated with such investments, may lose favor with investors as compared to those that are more “growth” oriented.

Definitions

Federal funds rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis.

Gross domestic product (GDP) measures the total value of all economic output in goods and services for an economy.

Currency debasement refers to a reduction in a currency’s purchasing power.

MSCI World Index (Net) measures the performance of large and midcap equities across developed markets countries. A net-return index tracks price changes and reinvestment of distribution income net of withholding taxes.

MSCI EAFE Index (Net) measures the performance of large and midcap equities across developed markets countries around the world excluding the US and Canada. A net-return index tracks price changes and reinvestment of distribution income net of withholding taxes.

US Dollar Index is a geometrically averaged calculation of six currencies weighted against the US dollar maintained by ICE Futures US.

S&P 500 Index (Gross/Total) measures the performance of 500 of the top companies in the leading industries of the US economy and is widely recognized as a proxy for the US market as a whole. A total-return index tracks price changes and reinvestment of distribution income.

Nikkei 225 is a price-weighted index composed of 225 stocks in the Prime Market of the Tokyo Stock Exchange. It is widely recognized as a proxy for the Japanese equity market as a whole.

German DAX® Index measures the performance of the 40 largest companies listed on the Frankfurt Stock Exchange that fulfil certain minimum quality and profitability requirements. It is widely recognized as a proxy for the German equity market as a whole.

CAC 40® Index is a free-float market capitalization-weighted index that measures the performance of the 40 largest and most actively traded shares listed on Euronext Paris.

Indexes are unmanaged and do not incur management fees or other operating expenses. One cannot invest directly in an index.

The holdings mentioned herein represent the following total assets of the First Eagle Global Equity ETF as of 30-Sep-2025: Oracle Corporation 3.16%; Alphabet Inc. Class C 3.12%; Samsung Electronics Co Ltd Pfd Non-Voting 3.26%; Barrick Mining Corporation 1.86%; Newmont Corporation 2.00%; Elevance Health, Inc. 1.49%; Philip Morris International Inc. 1.40%; Shimano Inc. 0.64%; Comcast Corporation Class A 1.44%; Salesforce.com, Inc. 1.06%.

Additional Disclosures

This commentary represents the opinion of the Global Value team as of the date noted. The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation to buy, hold or sell or the solicitation or an offer to buy or sell any fund or security.

The Fund’s portfolio is actively managed and holdings can change at any time. Current and future portfolio holdings are subject to risk.

The opinions expressed are not necessarily those of the firm. These materials are provided for informational purposes only. These opinions are not intended to be a forecast of future events, a guarantee of future results or investment advice. Any statistics contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof.

Third-party marks are the property of their respective owners.

Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about our funds and may be viewed at www.firsteagle.com. You may also request printed copies by calling us at 800-747-2008. Please read our prospectus carefully before investing.

As with all ETFs, shares may be bought and sold in the secondary market at market prices. Investments involve risk. Principal loss is possible.

First Eagle ETFs are Distributed by Quasar Distributors, LLC.