Macro & Market Views

Eyes on Private Debt

Eyes on Private Debt

Key Takeaways

Uncertainty pressured middle market private loan formation in 2023, as macro uncertainty and still-volatile interest rates dampened the M&A activity that drives these loans. Limited new issuance industrywide focused capital deployment on existing borrowers and smaller “add-ons” by private equity sponsors.

Demand for asset-based lending was strong during the year, as it tends to be during times when other financing options become less plentiful—a dynamic that was particularly evident in the aftermath of the regional bank challenges.

New-loan volumes may increase in 2024 as stabilizing policy rates unleash pent-up M&A activity among private equity sponsors anxious to deploy dry powder.

“Platform” buyouts were especially weak during the year, with private equity sponsors more focused on smaller “add-on” acquisitions. True to its countercyclical nature, asset-based lending (ABL) was a bright spot in the space, providing liquidity providers with diversification alongside compelling return potential.

That said, issuance headwinds are not necessarily an indicator of performance; First Eagle Alternative Credit believes a well-underwritten portfolio can still potentially generate strong returns for investors even if direct lending volume is down, as evident during the years immediately after the global financial crisis. While there were fewer opportunities overall to underwrite new loans in 2023, we believe our volume ultimately outpaced that of the broader market. Meanwhile, the limited new issuance allowed us to focus our attention on our existing borrowers, and providing flexible financing solutions is among the ways lenders generally seek to add value in what ultimately is a very relationship-driven business.

Looking forward, middle market direct lending volume has the potential to improve in 2024 as policy rates perhaps stabilize and private equity sponsors look to put their dry powder to work. Whether or not volumes accelerate, we believe the core middle market, in particular, may offer inherent advantages for nonbank providers of capital able to maintain rigorous loan underwriting and structuring standards.

Uncertainty Weighed on M&A Activity and Direct Lending Pipeline

After a challenging 2022, uncertainty was among the primary concerns facing the US private credit ecosystem—including nonbank lenders like First Eagle Alternative Credit as well as corporate borrowers and the private equity funds that sponsor them—heading into 2023. With inflation at a multidecade high and showing no indications of easing on its own, the Federal Reserve in March 2022 embarked on an interest rate-hike campaign that to date has increased the policy rate by 525 basis points and has done so at the most rapid pace ever. Significant rate volatility ensued as markets sought to divine the duration and trajectory of Fed tightening and the odds that the central bank would be able to tame inflation without tipping the economy into recession (the much-desired “soft landing”). Biased higher even before the Fed’s policy pivot, the ICE BofAML MOVE Index—which measures US interest rate volatility—accelerated its climb in 2022 and ultimately peaked in March 2023 with the bankruptcies of several US regional banks. Though it has subsequently eased, rate volatility remains elevated relative to historical levels.

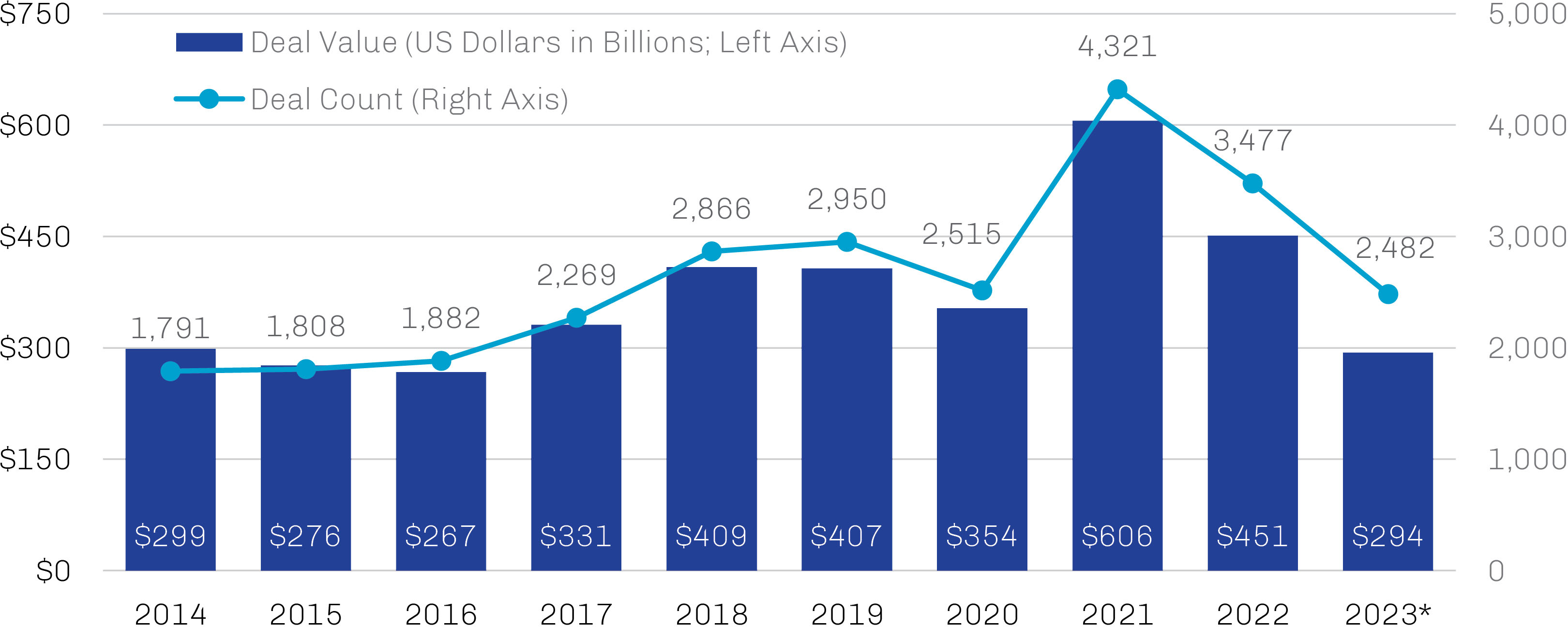

Not surprisingly, these conditions have not been very supportive of the M&A activity that serves as a major feeder to the direct lending pipeline. Private equity dealmaking, by both count and value, has declined in six of the past seven quarters and is down sharply from its 2021 peak, as shown in Exhibit 1. “Platform” buyouts—in which a private equity firm acquires a business that it intends to expand over time through the purchase of multiple smaller businesses (a.k.a. a “buy and build” strategy)—were particularly weak in the more conservative dealmaking environment, as they are typically relatively large in size and entail a fair amount of leverage. With interest rates discouraging prospective buyers from offering the type of price multiples that were common on these deals a few years ago, many private equity firms instead have opted to hold their portfolio names in hopes that conditions become more hospitable rather than exit at valuations they consider subpar.

Exhibit 1. Weak Private Equity Dealmaking Continued to Weigh on Direct Lending Volumes

US Private Equity Middle-Market Deal Activity, 2014 through September 2023

* Year-to-date through September 30, 2023; deal count is PitchBook estimate.

Source: PitchBook; data as of September 30, 2023.

In contrast, “add-ons”—the smaller acquisitions that are assimilated into a sponsor’s platform company— continued to provide private equity sponsors a way to deploy capital, albeit in smaller chunks, as they wait for markets to be more amenable to larger deals. Sponsors have continued to demonstrate a willingness to invest in their platform businesses, especially those platforms with decent capital structures and credit lines locked in at more attractive pre-2022 terms. While there are some incremental costs to the platform borrower as lenders extract small concessions, add-ons typically are a far more efficient financing mechanism than a recapitalization. Industrywide, add-ons accounted for about 76% of all private equity-sponsored buyouts in both 2022 and through the first three quarters of 2023.1

Though Other Forms of Financing Slowed, Asset-Based Lending Was Strong

First Eagle Alternative Credit focuses its direct lending activities on the US sponsored core middle market, which we define as companies with annual EBITDA of around $10–75 million. Despite the headwinds described earlier, the core middle market has been resilient even amid challenging conditions for issuance, and the past decade has seen remarkable growth in the space. Rising private company valuations have prompted private equity sponsors to look toward the smaller end of the middle market for more cost-effective platform opportunities; in our view, the lower middle market currently has a more balanced supply/demand dynamic, which has provided managers greater opportunities for diversification on behalf of clients.

While there were fewer opportunities overall to underwrite new loans in 2023, we expect our volume ultimately to outpace that of the broader market during the year based on deals booked and committed through year-end. Meanwhile, the limited new issuance allowed us to focus our attention on our existing borrowers, and add-ons—as they did for the market as a whole—represented the majority of our capital deployment during the year. We don’t view this as a negative. A well-underwritten portfolio can still generate strong returns for investors even if volume is down, as we saw in the years immediately after the global financial crisis, for example. Moreover, private lending is a relationship-driven business at the end of the day, and the ability to provide flexible financing solutions for our sponsors without compromising our stringent underwriting standards is among the ways we add value to these relationships. It’s been our experience that strong relationships with sponsors can help support consistent deal flow over time, even when markets in general appear unstable.

As a complement to cash flow-based loan underwriting, our robust asset-based lending (ABL) capability provides diversification to our platform and to our investors. Secured by specific assets of the borrower—such as inventory, accounts receivable, real estate, machinery and equipment, and intellectual property—ABL facilities generally appeal to companies with high working-capital needs and substantial assets but also inconsistent cash flows that limit access to other types of financing; examples include retailers that maintain large inventories or industrials renting high-capex equipment.

Demand for ABL historically has been countercyclical. Though the need for these facilities is always present to some extent, borrower interest tends to increase when other financing options grow scarce—a dynamic that was evident during the year, particularly in the aftermath of the regional bank challenges.

We Believe Ample Capital Remains to be Deployed

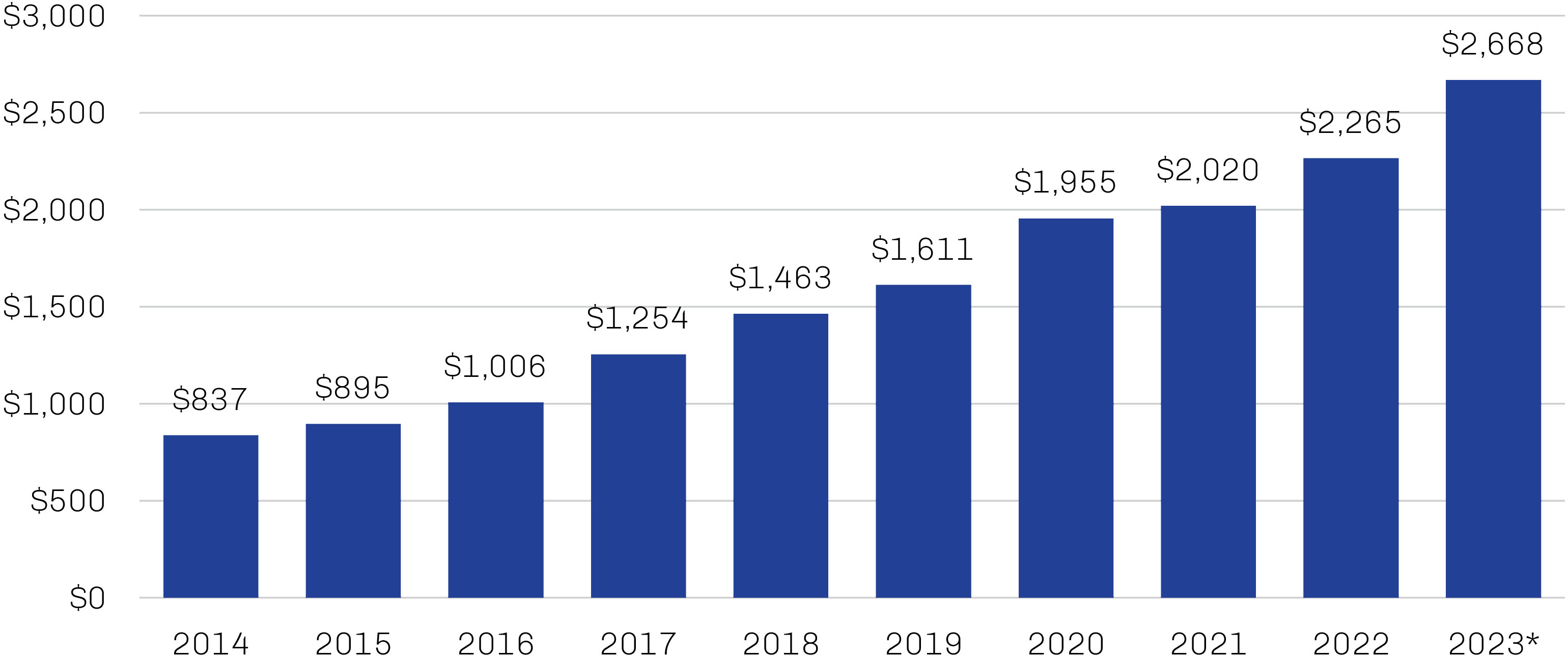

Though dealmaking has been challenged for much of the past 18 months, there are signs the leveraged-buyout space may be thawing. We wouldn’t necessarily describe the mood of private equity sponsors as upbeat, but we’ve seen new-issue activity pick up as sponsors appear less anxious about worst-case outcomes for the economy and more confident that policy rates have stabilized. The potential release of pent-up M&A energy bodes well for new-loan volumes ahead, especially given the amount of private equity dry powder waiting for a target, as shown in Exhibit 2 below; putting more than $2.5 trillion of dry powder to work on acquisitions at a conservative loan-to-value ratio of 50% would require $1.25 trillion of private credit capital. Meanwhile, add-on volume seems likely to persist as lenders and sponsors continue to manage their existing portfolios, and refinancings may even come back into play if rates ease, as futures markets currently forecast.

Exhibit 2. Massive Amount of Private Equity Dry Powder May Support Direct Lending Pipeline

US Dollars in Billions, 2014 through October 2023

* Year-to-date through October 30, 2023

Source: Preqin; data as of December 11, 2023.

In certain verticals, we have already seen sponsors begin to lay the groundwork for deals they hope to close in early 2024. This includes segments within healthcare, where sponsors have been waiting for portfolio company operations to normalize from Covid-19; the pandemic disrupted many high-margin activities within healthcare and unleashed significant wage-cost pressures on what is a very labor-intensive industry, weighing on margins. A stabilization in debt markets and easing labor costs may provide attractive exit opportunities for sponsors of certain healthcare companies. Technology is another people-heavy sector in which sponsors may be eager to strike a deal and return some capital to their limited partners.

Be True

Direct lending as an industry has a track record of opportunism. Nonbank lenders emerged in earnest following the global financial crisis because traditional banks were limited in their ability to provide liquidity, and these lenders continue to scour the credit market for capital needs that are not being met by the traditional participants.

Recently, a number of larger private lenders have attempted to put their ample capital stores to work by moving into deal sizes usually associated with broadly syndicated loans, stealing share by offering speed and certainty of funding during periods when more complicated financing structures are bogged down in disruptions, as was the case with the onset of Covid-19 in 2020 or the regional bank crisis earlier this year. In effect, these transactions refinance public debt as private debt, with the attendant decrease in liquidity for investors but little or no change in the credit profile of the borrower. Moreover, the overwhelmingly covenant-lite nature of the leveraged loan market suggests that competing private structures may need to make compromises on contractual provisions to compete for these deals consistently. It will be interesting to see what impact the competition between public and private structures may have on the risk/return profiles of such debt, especially if traditional private credit deal flow remains challenged.

Whether or not deal activity improves in 2024, it’s likely there will still be opportunities to potentially generate good risk-adjusted returns in the core middle market when the right borrower, sponsor and lender intersect. While we believe the core middle market offers inherent advantages for nonbank providers of capital, including diversification potential, it ultimately comes down to the quality of underwriting. For us, that has meant targeting borrowers with stable historical earnings, strong cash flows and private equity sponsorship, and mitigating risk through a first-lien position in the borrower’s capital structure complemented by at least one financial covenant and/or liquidity test.