Macro & Market Views

Cryptocurrencies: Hearts of Gold?

Cryptocurrencies: Hearts of Gold?

Key Takeaways

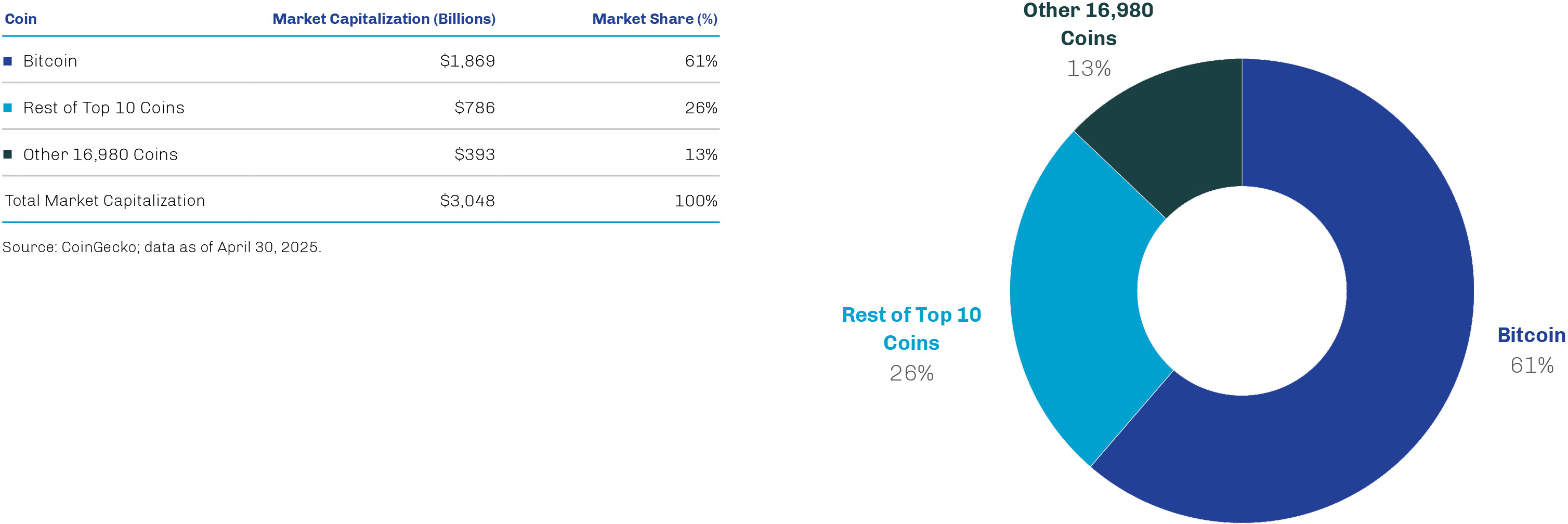

From small and obscure beginnings, cryptocurrencies have infiltrated the mainstream financial system. With a share of more than 60%, bitcoin dominates what is now a $3.0 trillion cryptocurrency market.1

The election of “crypto president” Donald Trump has ushered in a number of crypto-friendly federal actions, including the establishment of a strategic bitcoin reserve and digital assets stockpile.

Bitcoin’s characteristics, most notably its scarcity and independence from sovereign oversight, have prompted some to position it as a potential hedge and long-term store of value—i.e., “digital gold.”

Given its high volatility and tendency to trade directionally with equities, bitcoin remains a risky proposition, in our view. Instead, we continue to believe a strategic allocation to gold represents the most effective potential hedge against a range of adverse developments, as it has for millennia.

While bitcoin remains the dominant player in the space, around 17,000 active cryptocurrencies exist today—and even more have come and gone.2 Meanwhile, digital-asset payments have infiltrated the mainstream; more than 15,000 retailers worldwide accept crypto—ranging from haute couture brands like Balenciaga and Gucci to the convenience store chain Sheetz—and even more plan to do so in the near future.3 At the same time, crypto ownership has expanded beyond its tech-savvy niche to include a broad swath of retail and institutional investors, facilitated by the mainstream financial industry. Many adherents of digital assets believe these adoption trends can only accelerate under the US’s self-avowed “crypto president.”

The continued mainstreaming of crypto has inspired some of its staunchest proponents to suggest that bitcoin may represent a sort of “digital gold” for the twenty-first century, capable of serving as a modern store of value and potential hedge against inflation. We, on the other hand, would suggest bitcoin is better described as an option on potentially becoming digital gold in the future. Meanwhile, gold remains gold, and we continue to believe that a strategic allocation to the metal represents the most compelling form of potential hedge against both the seen and unseen risks facing investment portfolios.

The Birth of a New Currency

Bitcoin was introduced to the world in a 2008 white paper attributed to the pseudonymous Satoshi Nakamoto, whose identity (or -ies) remains a mystery to this day. As the global financial crisis was unfolding, Nakamoto’s paper made the case for “an electronic payment system based on cryptographic proof instead of trust, allowing any two willing parties to transact directly with each other without the need for a trusted third party.”4 To accomplish this, Nakamoto envisioned a decentralized peer-to-peer network through which both currency issuance and transactions are executed collectively—aka, the blockchain.

In early 2009, the “genesis” block of bitcoin was mined, releasing into the world the first 50 of the maximum 21 million bitcoins allowed per the software’s coding. Though bitcoin continues to dominate the crypto market—as shown in Exhibit 1—recent data show nearly 17,000 cryptocurrencies and a total market capitalization of around $3.0 trillion.5

Exhibit 1. The Massive Cryptocurrency Market Is Dominated by Bitcoin

Cryptocurrencies by Market Capitalization in US Dollars

The Mainstreaming of Crypto

Money in the traditional sense—fiat currency issued by central banks for use by financial institutions, businesses and the public—acts as a medium of exchange, a common unit of account and a store of value. While not all crypto assets are intended to serve as a substitute for fiat currency, those that are have faced significant obstacles to widespread adoption, including frictions within processing systems, relatively slow transaction speeds and gyrating valuations.

That said, crypto has come a long way from bitcoin’s early days of anonymous payments on the dark web and has gained broader acceptance as a mainstream medium of exchange. Crypto is accepted by a wide range of retailers, and some payment-system operators, including Visa and PayPal, have evolved their technologies to facilitate crypto-based transactions.

The growing acceptance of digital payments has spearheaded the rise of crypto investing; in fact, digitally native millennials and Gen Zers may be more likely to own crypto than stocks and bonds.6 Although direct ownership of even the most prominent cryptocurrencies is fraught with challenges—such as volatility, an uncertain regulatory framework and the risk of loss due to theft, hacks or forgotten private keys—pooled crypto-investment vehicles emerged in the mid-2010s to provide crypto exposure for investment purposes without the complications of direct ownership. These products initially were offered by crypto-native managers only to accredited investors, but traditional investment managers soon began to push for broader adoption. The Securities and Exchange Commission approved a bitcoin futures exchange-traded fund in 2021 and spot bitcoin and ether ETFs in 2024.7 US-listed crypto ETFs have about $120 billion in assets under management, and BlackRock, Fidelity, Van Eck and Invesco are among the mainstream managers offering them.8

Perhaps motivated by his supporters’ interest in digital assets, Donald Trump pledged during his campaign to be the “crypto president” and has moved quickly toward honoring that promise. Even before taking office, Trump and the once-and-future first lady launched a pair of eponymous meme coins—speculative tokens with no practical value. Soon after, Trump banned the continued development of a central bank digital currency by any US agency—removing from the market one potential competitor to private digital assets. He also established a working group charged with creating a regulatory framework governing digital assets and evaluating the creation of a national stockpile of said assets.9

On March 6, a national reserve of bitcoin was created via executive order and seeded with $17 billion of bitcoin seized by the US in legal cases; a stockpile of certain other digital securities was also announced.10 While some hoped these federal vehicles would provide digital assets with another leg up, the lack of government buying in the announcement left many in the crypto community disappointed. Bitcoin, for example, sold off on the news of the national reserve and, while it has since rebounded, it remains down about 14% from its record high of January 20—Trump’s inauguration day. Meanwhile, meme coins $TRUMP and $MELANIA are down 70% and 94%, respectively, from their late-January peaks.11

Gold for the Digital Age?

As crypto in general has earned broader approval, a new narrative for the utility of bitcoin appears to have taken root: bitcoin as “digital gold” that can serve as a modern store of value and potential hedge against inflation and the debasement of fiat currency in the face of trillions of dollars of government debt. We have our reservations, notwithstanding the surreality of weighing the mostly theoretical benefits of a 17-year-old cryptocurrency against those gold has offered for millennia.

While bitcoin’s supply constraints—its code enforces a supply cap at 21 million coins, and a mechanism called “halving” dictates the pace at which they can be mined—may support the concept of gold-like scarcity value, its trading history fails to make the case for it as an effective store of value. With annualized volatility of 172.7% since the start of 2011, bitcoin has been less stable across all market conditions than time-tested perceived “safe havens” such as gold (15.8%) and 10-year US Treasuries (4.5%).12 As shown in Exhibit 2, over the last five years alone, the price of bitcoin has been marked by sharp spikes and massive downturns, prolonged climbs and lengthy troughs. While this price action likely amplifies bitcoin’s appeal as a speculative vehicle, it weakens its claim as a reliable store of value.

Exhibit 2. Extreme Price Moves Belie Bitcoin’s Usefulness as a Store of Value

Bitcoin Price, January 2021 through April 2025

Source: CoinGecko; data as of April 30, 2025

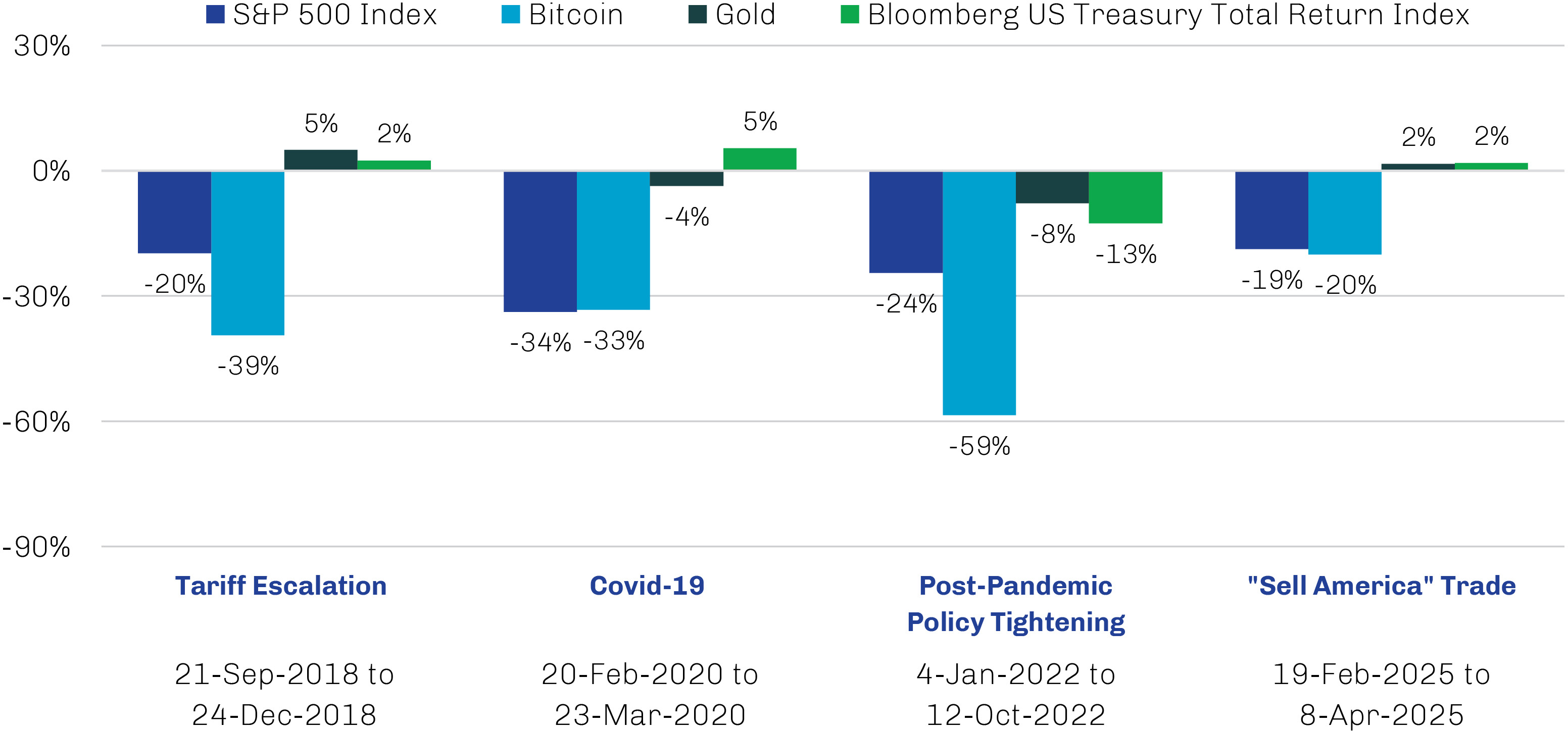

Looking more closely at recent periods of uncertainty and discord—times when a source of portfolio resilience is needed most—bitcoin’s price has generally been directionally aligned with US equities, as shown in Exhibit 3. This was evident most recently as the risk-on “Trump trade” that followed November’s election gave way to tariff-fueled “sell America” sentiment in February. Though gold initially softened with the onset of the “Trump trade,” it wasn’t long before the metal resumed the upward trend that propelled it to a succession of new record highs throughout 2024 and 2025.

Exhibit 3. Bitcoin Has Generally Followed Equities Lower During Periods of Stress

Percentage Change in Price

Source: FactSet, Bloomberg; data as of April 30, 2025

This resilience should probably come as no surprise given gold’s millennia-long track record as a store of value. The metal’s unique risk-return characteristics have enabled it to retain real purchasing power across disparate environments and through numerous existential threats, providing investors a perceived “safe haven” in uncertain times.

Gold’s reputation for providing investors shelter from the storm is well-earned. It’s been our experience that the gold market can sometimes serve as the metaphorical canary in the coalmine, sussing out potential dangers before they manifest in asset prices more broadly, and such red flags have been plentiful in recent years. It’s reasonable to think that anxieties around massive government debt levels and widespread geopolitical and macroeconomic turbulence may be supporting interest in an asset with a proven track record as a perceived “safe haven” and store of value in uncertain times.

We can see signs of this in demand from global central banks, whose efforts to diversify their reserve assets have been a key source of support for the gold price over the past few years. Annual purchases of gold by central banks have topped 1,000 tonnes for three consecutive years after averaging only 481 tonnes annually between 2010 and 2021. More recently, financial buyers have also joined the game. Physically backed gold exchangetraded funds (ETFs)— which capture investment demand from both institutional and individual investors—have seen three straight quarters of inflows after nine quarters of outflows.13

For all its appeal, bitcoin remains a young, untested asset. While bitcoin may represent an option on becoming digital gold at some point, it currently is no substitute for the real thing and its millennia-long track record as a store of value.