Retirement

A Better Framework for Fund Evaluation

A Better Framework for Fund Evaluation

Today’s defined contribution plan menus generally are reviewed with a focus on returns not outcomes; theoretical asset class risk rather than prevailing market dynamics; cost as opposed to the value that can be added through wealth creation. We believe that the “quantitative” scoring systems currently used by fund sponsors and their advisors to assemble and review fund lineups are a blunt instrument for what is a far more nuanced task. They often fail to accurately evaluate funds that do not fit squarely in a style box or to leverage the wide range of investment solutions that may help participants in their pursuit of retirement readiness.

By failing to capture the more “qualitative” aspects of fund evaluation such as fund manager philosophy and consistency, investment style and portfolio objectives, scoring systems may produce a number of second-order impacts that may result in suboptimal plan lineups. For example, the strong relative performance of US markets—driven by outsized appreciation in certain popular stocks and sectors—in many cases has also increased the risks of investing in these markets moving forward, especially in passive equity strategies benchmarked to them. While such strategies may benefit plan participants in a relentlessly bouyant market, they also may offer a false impression of how wealth is likely to be created over the multidecade period that comprises the retirement journey.

Key messages

- Equity market dynamics since the global financial crisis have skewed fund analyses in favor of a distinct cohort of strategies, potentially depriving retirement plan participants of investment approaches designed to generate long-term wealth rather than outsized short-term gains.

- Plan sponsors and their advisors tend to focus on short-term performance metrics when constructing retirement plan lineups. Given that retirement wealth is built over the long term across disparate investment environments, however, we believe that mapping long-term fund performance against shifting market conditions may help fiduciaries assemble a collection of investment strategies offering participants complementary styles, philosophies and goals.

- In our view, a fund’s proven ability to grow assets in specific investment environments may be a good indicator of its ability to contribute to the retirement readiness of plan participants going forward.

For those in the workforce today, a retirement journey of 70 years or more—filled with bull markets, bear markets and occasions of gut-wrenching crisis—would not be unusual. In our view, it is essential that the fiduciaries are mindful of the long-term nature of the goals being solved for when evaluating manager performance. Commonly used metrics such as annualized total return and upside/downside capture can be misleading given the one-dimensional investment environment—marked by a pronounced bias toward large domestic growth stocks—that has prevailed over the past decade. Typical fund scoring systems have a range of flaws, many of which are exacerbated in today’s capital markets, including timeframe, investment-environment and benchmark bias; peer-group mischaracterization; and the impact of low benchmark volatility.

Building a retirement-outcome-focused investment lineup involves more than merely checking off various style boxes; it requires decomposing the long-term performance of investment products to establish a track record of performance in different invest¬ment regimes. While we’re continually warned that past performance is not an indicator of future results, mapping multicycle historical performance patterns against prevailing market conditions—outperformance in down markets, for example, or higher risk-adjusted returns over full cycles—may help plan sponsors assemble a lineup of investment strategies with complementary styles, philosophies, and goals. In our view, such an approach likely would better align manager evaluation criteria with participant time horizons, temper participant impulses to overreact to short-term anomalies and improve plan sponsors’ prudent fiduciary processes.

To better reflect historical tendencies and thus potential fund behavior across future investment environments, today’s scoring systems would benefit from subtle—but essential—changes to their methodology. For example, while annualized total returns—over one, three, five and/or 10-year periods—tend to be the primary consideration for plan lineup inclusion and a major focus of plan participants, fiduciaries may be better served by highlighting a fund’s track record over time. In our view, a fund’s proven ability to grow assets in specific investment environments may be a good indicator of its potential ability to contribute to the retirement readiness of plan participants going forward. Similarly, identifying the predictability of absolute fund performance across markets—up, down and sideways—may provide a better understanding of potential future returns compared to aggregated upside or downside ratios that merely capture relative returns when the benchmark moves in a certain way.

While plan participants have a range of unique time horizons, investment objectives and market acumen, 401(k) plan lineups must be structured to meet the broad retirement savings needs of the group as a whole. As such, it is paramount that fiduciaries understand—and effectively communicate—how their plan lineups may be utilized to support the goals of individual participants across the disparate investment backdrops likely to occur over the multidecade retirement savings timeframe. We believe this is best done through a selection methodology that evaluates historical fund performance in various market environments—not only for the strong equity performance of the past 13 years but also down periods and periods in which market leadership is less clear-cut.

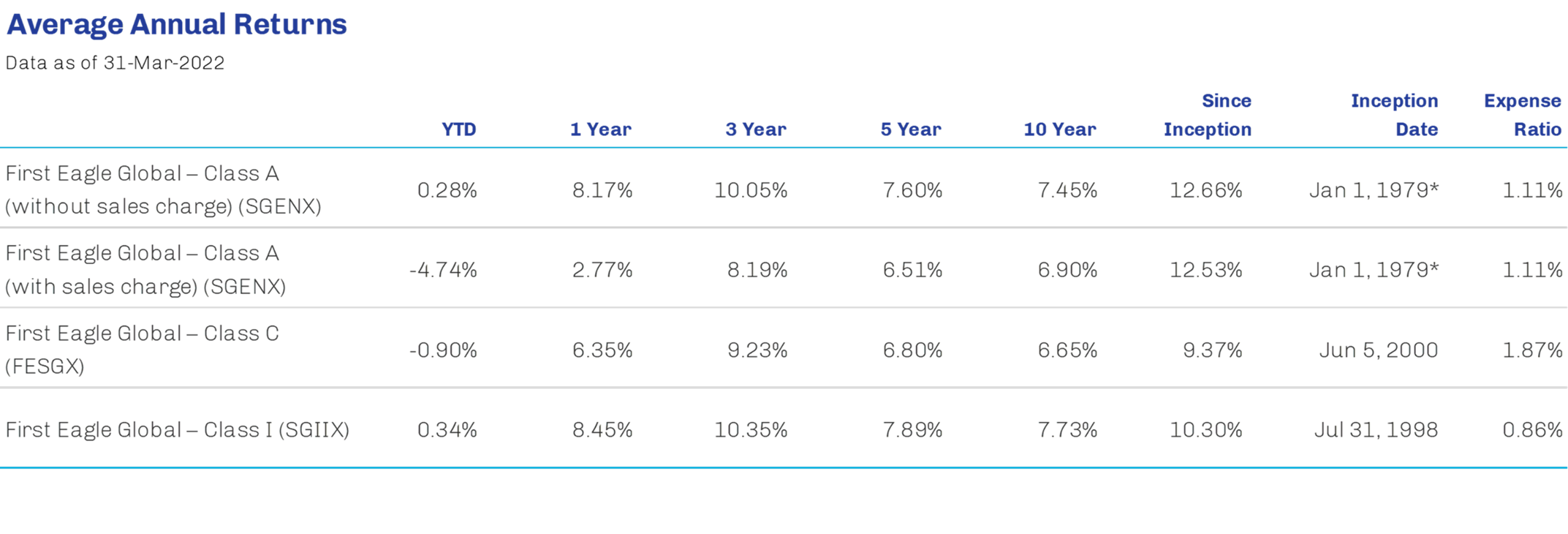

To illustrate the application of the outcome-based methodology described above, let’s consider First Eagle Global Fund. Global Fund is a globally diversified, benchmark-agnostic portfolio focused on absolute returns with an emphasis on mitigating losses in difficult market environments. In a 401(k) context, Global Fund has historically been used as a balanced fund replacement, a qualified default investment alternative or as a complement to other funds in a plan’s core menu. Morningstar has classified Global Fund in its World Allocation category, which has roughly 450 funds that vary considerably in terms of asset allocation, investment philosophy and portfolio application.

Many funds under evaluation in this framework will not have track records that cover multiple and varying market environments; as such, consider looking at performance metrics in quarterly increments as well as annualizing these quarterly results in order to generate a greater number of data points for analysis. Note that the First Eagle Global Fund has more than 40 years1 of performance, with an investment philosophy that has remained consistent across the varying market environments.

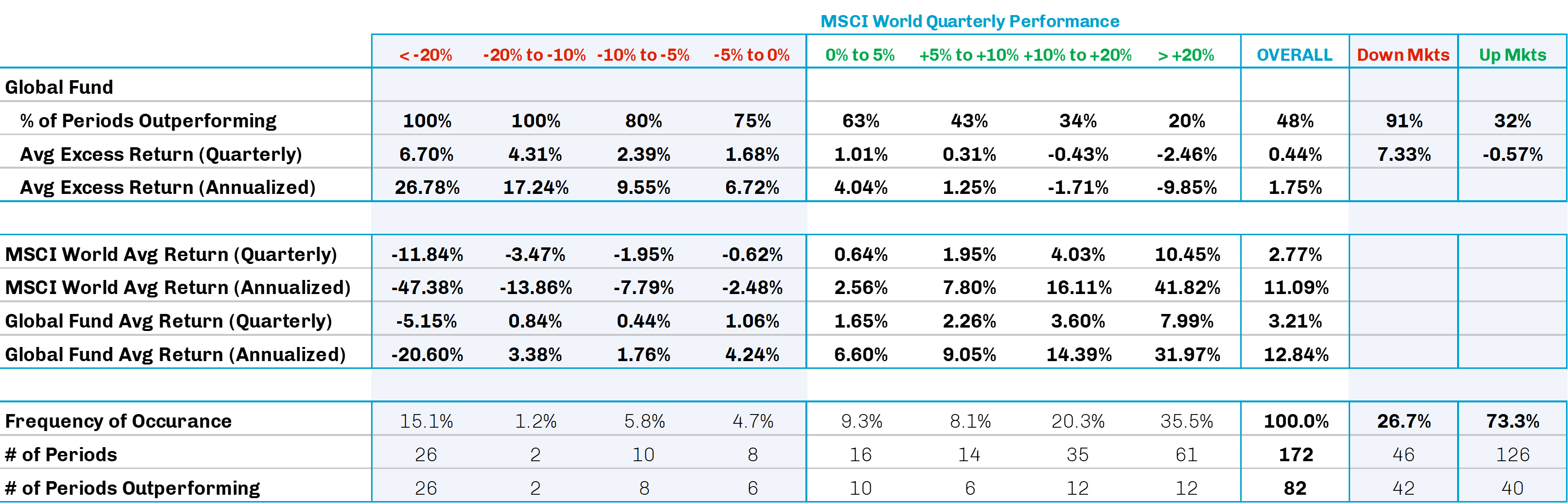

In Figure 1, we sort Global Fund’s average quarterly returns and the annualization of these average quarterly returns into bands based on performance from the fund’s inception of January 1, 1979 to December 2021—172 measurement periods. These performance bands start with returns below -20% and increase in 5% or 10% increments until reaching the final band of returns in excess of 20%. Returns of the MSCI World Index are then mapped to the Global Fund’s performance over contemporaneous periods, enabling comparisons on both an absolute and relative basis and allowing conclusions to be drawn about the fund.

Performance of First Eagle Global Fund Class A Shares (without sales charge) and MSCI World Index, January 1979 through December 2021

Source: FactSet; data as of December 21, 2021.

Performance information is for Class A Shares without the effect of sales charges and assumes all distributions have been reinvested and if sales charge was included values would be lower. Past performance does not guarantee future results.

Having bucketed the returns of Global Fund and its benchmark into performance ranges, frequencies of occurrence can be calculated to contextualize relevance. This data also can be summarized to measure relative performance trends in down and up markets. As shown in the chart above, Global Fund outperformed the MCSCI World Index in 42 of the 46 quarters in which the MSCI World Index declined—or 91% of the time—and did so by an average of about 7.3%. This outperformance in down markets, in our view, more than offsets the underperformance—0.57%—during up markets, driving the fund’s outperformance of the benchmark through the 40-plus year measurement period. Said in another way, a fund that mitigates declines in the broader markets generally spends less time scrabbling for breakeven and more time attempting to build wealth over the plan participant’s long-term investment horizon.

With its flexible, benchmark-agnostic approach, Global Fund seeks to do just that. In addition to seeking companies worldwide whose market prices offer what we believe to be a “margin of safety,” or discount to our estimate of their “intrinsic values”, Global Fund maintains a strategic allocation to gold as a potential hedge against adverse market events and holds Short-term Investments and Cash/Cash Equivalents as deferred purchasing power when attractive equity opportunities are scarce. This philosophy has allowed the Fund to historically outperform its benchmark since its inception, and in our view, it ranks favorably among strategies that may be considered by plan fiduciaries for their potential to create wealth over time.

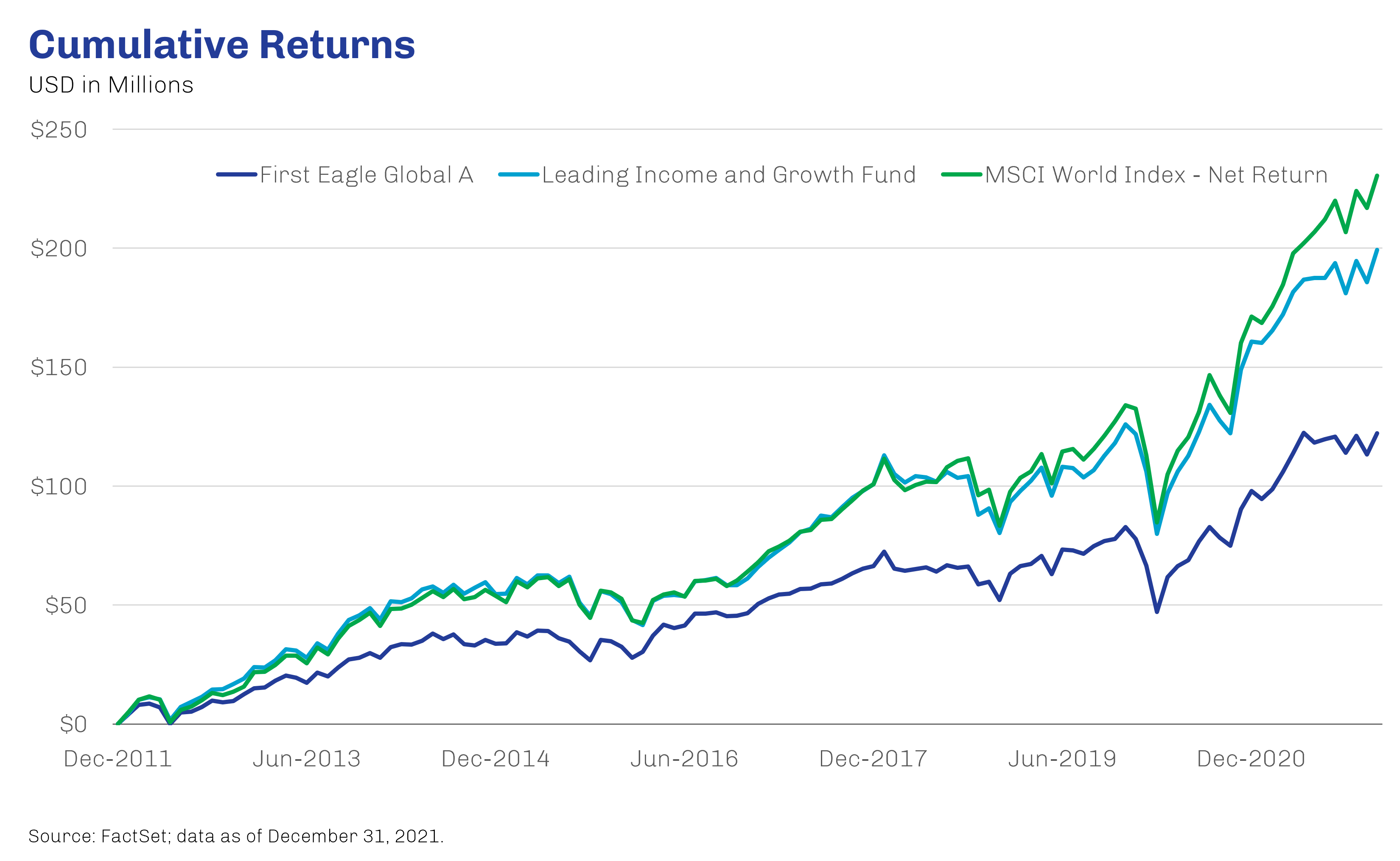

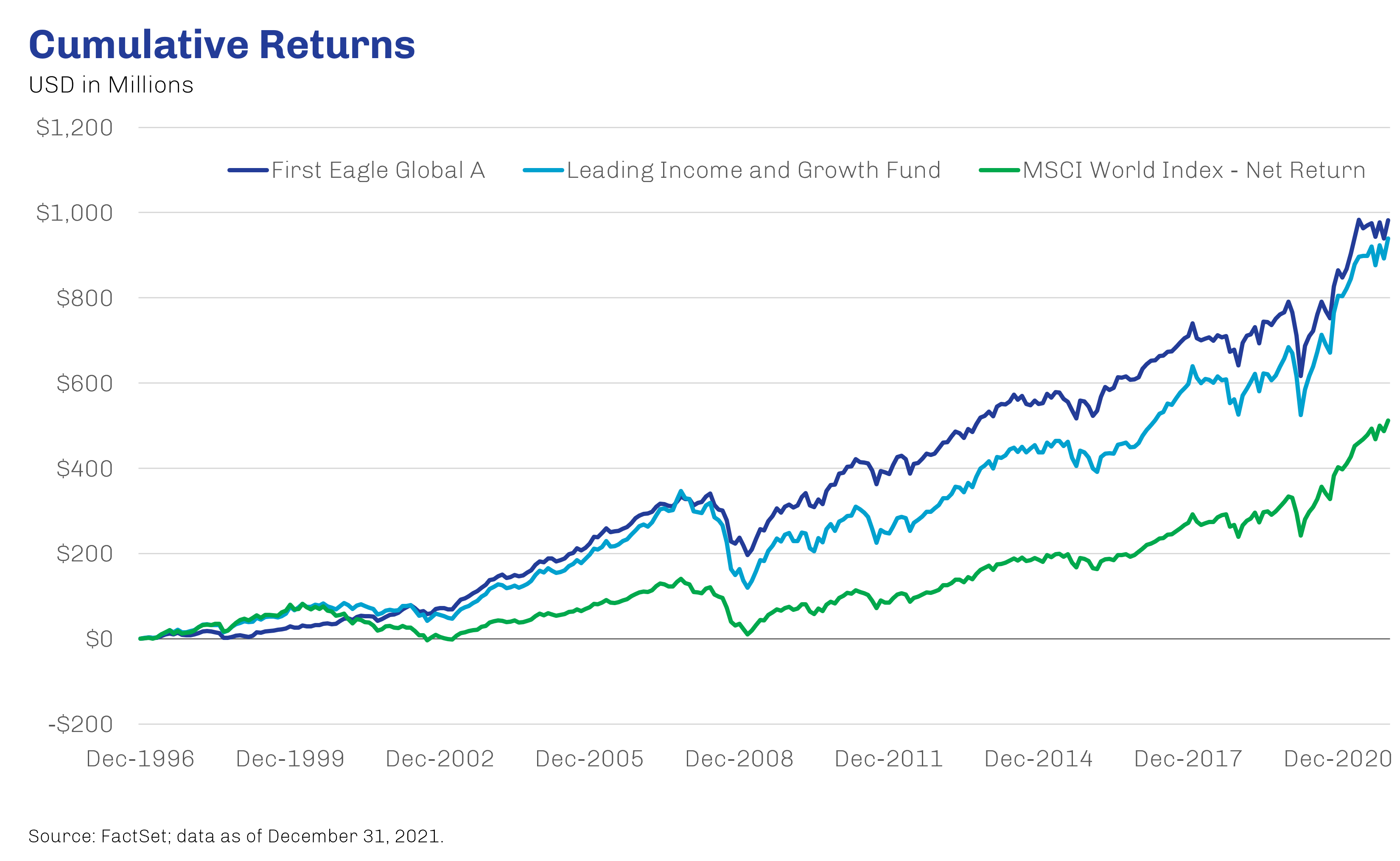

As demonstrated in Exhibits 2 and 3, “over time” is an important qualifier, particularly given the market dynamics that have prevailed for much of the time since the global financial crisis. The charts below compare the performance of First Eagle Global Fund and a leading income and growth fund over 10- and 25-year periods ended December 31, 2021. The latter, one of the largest funds in Morningstar’s World Large-Stock Blend category, seeks global growth with a dividend focus and had near-equal exposure to domestic (47.9%) and foreign (48.2%) stocks as of end-2021.2

Buoyed by a very strong market in which equity market exposure—and US large-cap equity exposure, in particular—was historically rewarded, the leading growth and income fund outperformed the more diversified Global Fund over the past 10 years; both funds were bested by the MSCI World Index and its 69% weighting in US companies, however.3

In contrast, the 25-year view—which includes three US recessions and three massive global equity market selloffs—provides a longer, more varied timeframe over which to evaluate performance and underscores the impact market downturns can have on the potential of plan participants to accumulate wealth over time. Perhaps not surprisingly, First Eagle Global Fund and its emphasis on downside mitigation combined with potential upside participation—driven by thoughtful security selection, gold as a potential hedge, and short-term investments and cash and cash equivalents as deferred purchasing power—was better able to navigate this more tumultuous time period, outperforming the more equity-focused growth and income fund and the MSCI World Index for the period shown.

Performance information is for Class A Shares without the effect of sales charges and assumes all distributions have been reinvested and if sales charge was included values would be lower. Past performance does not guarantee future results.

Performance information is for Class A Shares without the effect of sales charges and assumes all distributions have been reinvested and if sales charge was included values would be lower. Past performance does not guarantee future results.

Subjecting all funds in a particular Morningstar category to this analysis can help fiduciaries isolate them into appropriate peer groups, such as downside mitigators, upside optimizers and benchmark mirrors (likely the indexed portfolios). These subsets would sharpen comparisons among similarly behaved funds, allowing, for example, an evaluation of First Eagle Global Fund against only downside mitigators. With this data, a fiduciary can select individual funds that reflect the desired outcome for that category or sleeve and provide participants with a lineup of differentiated funds rather than a series of beta plays that may have similar outcomes in all market environments.

At First Eagle, we seek to build all-weather investment portfolios focused on generating attractive real returns over time while avoiding the permanent impairment of capital. Our benchmark-agnostic approach enables us to focus on absolute returns—that is, seeking to grow participant wealth in pursuit of their individual retirement goals, not tracking the ups and downs of an arbitrary market index.

For plan sponsors and advisors, we believe there are many positive aspects to the adoption of a flexible fiduciary scoring methodology. It would better position them to create plan lineups that better capture the investible universe. It may encourage them to spend their active risk budget on managers that pursue specific and potentially achievable outcomes for plan participants through risk-return profiles differentiated from the benchmark. It can also facilitate the selection of funds and managers that offer tailored selections designed to encourage proper asset allocation and true diversification in today’s “do-it-for-me” environment, such as managed accounts and custom target date and other Qualified Default Investment Alternative vehicles.

1Prior to January 1, 2000, the strategy was managed by a prior portfolio manager while he served at a firm different from First Eagle Investment Management, LLC.

2Source: Capital World Growth and Income Fund Fact Sheet; data as of December 31, 2021.

3Source: MSCI; data as of December 31, 2021.

This material is for informational purposes only and is not to be construed as specific tax, legal, or investment advice. You are strongly encouraged to consult with your independent financial professional, lawyer, accountant, or other advisors as to investment, legal, tax and related matters.

The opinions expressed are not necessarily those of the firm. These materials are provided for informational purpose only. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. Any statistic contained herein have been obtained from sources believed to be reliable, but the accuracy of this information cannot be guaranteed. The views expressed herein may change at any time subsequent to the date of issue hereof. The information provided is not to be construed as a recommendation or an offer to buy or sell or the solicitation of an offer to buy or sell any fund or security.

* Performance for periods prior to 01-Jan-2000 occurred while a prior portfolio manager of the Fund was affiliated with another firm. Inception date shown is when this prior portfolio manager assumed portfolio management responsibilities.

The performance data quoted herein represents past performance and does not guarantee future results. Market volatility can dramatically impact the fund’s short-term performance. Current performance may be lower or higher than figures shown. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance data through the most recent month end is available at www.firsteagle.com or by calling 800-334-2143. The average annual returns for Class A Shares "with sales charge" of First Eagle Global Fund give the effect to the deduction of the maximum sales charge of 5.00%.

Risk Disclosures

All investments involve the risk of loss of principal.

There are risks associated with investing in securities of foreign countries, such as erratic market conditions, economic and political instability and fluctuations in currency exchange rates.

The principal risk of investing in value stocks is that the price of the security may not approach its anticipated value or may decline in value.

Investment in gold and gold-related investments present certain risks and returns on gold related investments have traditionally been more volatile than investments in broader equity or debt markets.

World Allocation Morningstar Category: World-allocation portfolios seek to provide both capital appreciation and income by investing in three major areas: stocks, bonds, and cash. While these portfolios do explore the whole world, most of them focus on the U.S., Canada, Japan, and the larger markets in Europe. It is rare for such portfolios to invest more than 10% of their assets in emerging markets. These portfolios typically have at least 10% of assets in bonds, less than 70% of assets in stocks, and at least 40% of assets in non-U.S. stocks or bonds.

A bull market is the condition of a financial market in which prices are rising or are expected to rise.

A bear market is when a market experiences prolonged price declines. Beta is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole.

First Eagle defines “margin of safety” as the difference between a company’s market value and our estimate of its intrinsic value. An investment made with a margin of safety is no guarantee against loss.

“Intrinsic value’’ is based on our judgment of what a prudent and rational business buyer would pay in cash for all of the company in normal markets.

Diversification does not guarantee investment returns and does not eliminate the risk of loss.

Upside capture is the ratio of a fund's overall return to global equity market returns evaluated over periods when equities have risen.

Downside capture is the ratio of a fund's overall return to global equity market returns evaluated over periods when equities have fallen.

The MSCI World Index is a widely followed, unmanaged group of stocks from 23 developed market countries and is not available for purchase. The index provides total returns in U.S. dollars with net dividends reinvested. One cannot invest directly in an index.

Indexes are unmanaged and one cannot invest directly in an index.

FEF Distributors, LLC (Member SIPC) distributes certain First Eagle products; it does not provide services to investors. As such, when FEF Distributors, LLC presents a strategy or product to an investor, FEF Distributors, LLC does not determine whether the investment is in the best interests of, or is suitable for, the investor. Investors should exercise their own judgment and/or consult with a financial professional prior to investing in any First Eagle strategy or product.

Investors should consider investment objectives, risks, charges and expenses carefully before investing. The prospectus and summary prospectus contain this and other information about the Funds and may be viewed online or calling us at 800.747.2008. Please read the prospectus carefully before investing. Investments are not FDIC insured or bank guaranteed and may lose value.

The First Eagle Funds are offered by FEF Distributors, LLC, a subsidiary of First Eagle Investment Management, LLC, which provides advisory services.

First Eagle Investments is the brand name for First Eagle Investment Management, LLC and its subsidiary investment advisers.

First Eagle Investment Management, LLC | 1345 Avenue of the Americas, New York, NY 10105-0048 | www.feim.com

© 2022 First Eagle Investment Management, LLC. All rights reserved.